Private and Public Cloud in Financial Service Market

Private and Public Cloud in Financial Service Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708689 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Private and Public Cloud in Financial Service Market Size

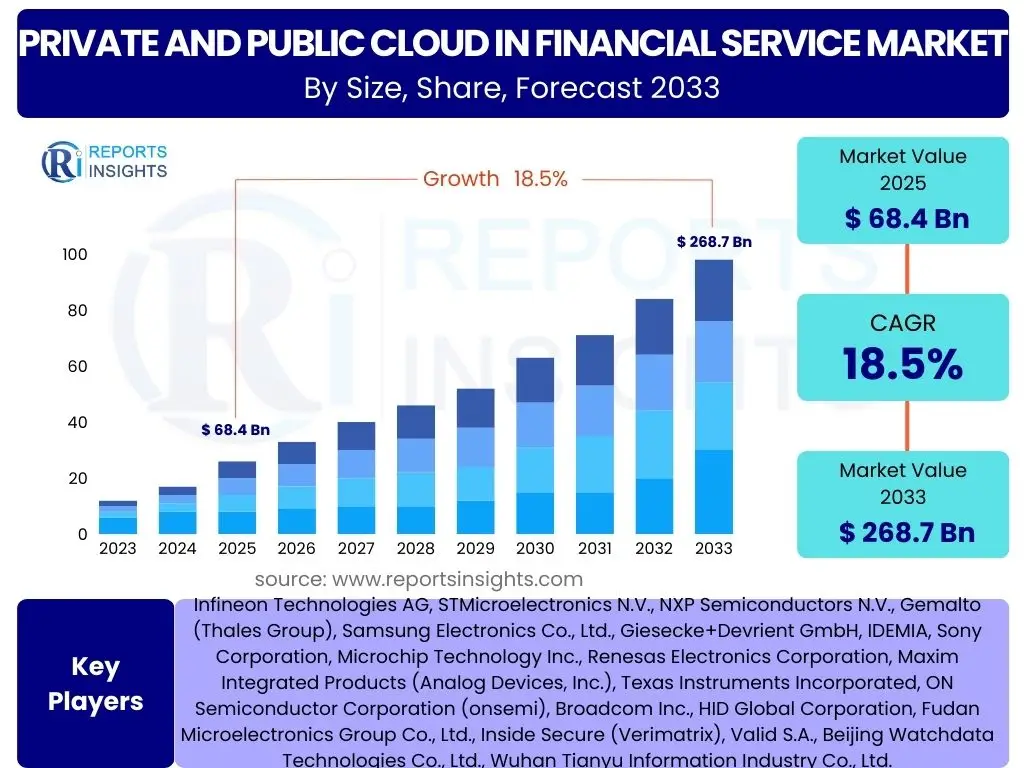

According to Reports Insights Consulting Pvt Ltd, The Private and Public Cloud in Financial Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 68.4 billion in 2025 and is projected to reach USD 268.7 billion by the end of the forecast period in 2033. This significant expansion is driven by the increasing need for agile, scalable, and secure IT infrastructure within the financial sector, enabling institutions to meet evolving customer demands, navigate stringent regulatory environments, and embrace digital transformation initiatives. Both private and public cloud deployments offer distinct advantages, with hybrid and multi-cloud strategies becoming increasingly prevalent to balance control, cost-efficiency, and innovation.

The growth trajectory is further fueled by the imperative for financial institutions to modernize legacy systems, reduce operational costs, and enhance data analytics capabilities. Public cloud offers unparalleled scalability and access to advanced services, while private cloud provides a higher degree of control and compliance assurance for sensitive financial data. The convergence of these models into hybrid architectures is empowering financial entities to optimize their cloud strategy, leveraging the best of both worlds to foster innovation in areas such as FinTech, blockchain, and artificial intelligence, all while maintaining robust security postures and regulatory adherence.

Key Private and Public Cloud in Financial Service Market Trends & Insights

User inquiries frequently highlight the shift towards hybrid and multi-cloud strategies, the rising importance of specialized financial cloud offerings, and the continuous evolution of security and compliance frameworks. There is strong interest in how cloud adoption impacts operational efficiency, global expansion capabilities, and the integration of emerging technologies like AI and machine learning. Additionally, concerns about vendor lock-in and data residency requirements are prominent, shaping deployment choices.

- Hybrid and Multi-Cloud Adoption: Financial institutions are increasingly deploying hybrid and multi-cloud strategies to optimize workloads, enhance resilience, and avoid vendor lock-in, integrating on-premise infrastructure with multiple public cloud providers.

- Cloud-Native Development: A growing emphasis on cloud-native applications and microservices architectures to achieve greater agility, scalability, and resilience for financial services.

- Regulatory Compliance Specialization: Cloud providers are offering specialized services and certifications tailored to stringent financial regulations, such as GDPR, PCI DSS, and regional financial authority guidelines, easing the compliance burden for institutions.

- Focus on Data Sovereignty and Residency: Increasing demand for solutions that ensure data remains within specific geographical boundaries, driven by evolving data privacy laws and national security concerns.

- Enhanced Security Offerings: Continuous innovation in cloud security, including advanced encryption, identity and access management (IAM), threat detection, and data loss prevention (DLP) solutions, is critical for sensitive financial data.

- Rise of FinTech and Neobanks: The proliferation of FinTech startups and challenger banks, which are inherently cloud-first, is pushing traditional financial institutions to accelerate their cloud adoption to remain competitive.

- Sustainable Cloud Practices: Growing interest in environmentally friendly cloud solutions and energy-efficient data centers to meet corporate social responsibility goals and reduce operational carbon footprints.

AI Impact Analysis on Private and Public Cloud in Financial Service

User questions related to AI's impact on cloud in financial services often center on its role in fraud detection, risk management, personalized customer experiences, and operational automation. There's significant interest in how AI capabilities, particularly machine learning, are leveraged within cloud environments to derive insights from vast datasets, enhance decision-making, and create innovative financial products. Users also express concerns about the ethical implications of AI, data bias, and the need for robust governance frameworks when deploying AI on the cloud within regulated financial contexts.

The integration of artificial intelligence and machine learning within private and public cloud environments is profoundly transforming the financial services landscape. Cloud platforms provide the scalable computing power and data storage necessary to run complex AI models, enabling financial institutions to analyze massive datasets for fraud detection, credit scoring, algorithmic trading, and personalized customer service. AI-driven analytics help identify patterns, predict market movements, and automate compliance checks, leading to more efficient operations and reduced risk. This symbiotic relationship between AI and cloud computing is accelerating digital transformation, allowing financial firms to innovate faster and deliver more sophisticated services.

- Enhanced Fraud Detection: AI algorithms deployed on the cloud analyze transactional data in real-time to identify anomalous patterns indicative of fraud, significantly reducing financial losses.

- Personalized Customer Experiences: Cloud-based AI platforms enable financial institutions to process customer data and interactions, offering tailored products, services, and advice at scale.

- Optimized Risk Management: Machine learning models leverage cloud resources to assess credit risk, market risk, and operational risk with greater precision, improving capital allocation and regulatory compliance.

- Automated Compliance and Regulatory Reporting: AI helps automate the monitoring of regulatory changes, flag non-compliant activities, and streamline reporting processes, reducing manual effort and errors.

- Algorithmic Trading and Investment Strategies: Cloud infrastructure supports complex AI-driven trading algorithms, allowing for high-frequency trading, market prediction, and optimized portfolio management.

- Operational Efficiency through Automation: AI-powered chatbots, Robotic Process Automation (RPA), and intelligent document processing in the cloud automate repetitive tasks, improving back-office efficiency and reducing operational costs.

- Data-Driven Decision Making: AI tools on cloud platforms facilitate deeper insights from large and diverse datasets, empowering financial institutions with more informed strategic and tactical decisions.

Key Takeaways Private and Public Cloud in Financial Service Market Size & Forecast

Common user questions regarding market takeaways often revolve around the most significant growth drivers, the primary challenges to adoption, and the regions poised for the strongest expansion. There is also keen interest in understanding the long-term strategic implications of cloud migration for financial institutions and the critical success factors for leveraging cloud technology effectively. Users seek clarity on how ongoing regulatory scrutiny and technological advancements will shape future market dynamics.

The Private and Public Cloud in Financial Service Market is on a robust growth trajectory, driven by the sector's unyielding demand for digital transformation, operational efficiency, and enhanced security. The forecasted CAGR of 18.5% indicates a rapid shift towards cloud-centric IT infrastructure as financial institutions increasingly recognize the imperative to modernize legacy systems and embrace agile development methodologies. Hybrid cloud deployments are emerging as the preferred strategy, offering a balanced approach to innovation, compliance, and control. This market expansion represents a critical evolution, enabling financial entities to navigate complex global markets and deliver next-generation services.

- Strong Growth Trajectory: The market is projected for substantial growth, indicating accelerated cloud adoption across all segments of the financial services industry.

- Hybrid Cloud Dominance: Hybrid cloud models, combining private and public cloud resources, will be pivotal for balancing security, compliance, and scalability needs.

- Digital Transformation Catalyst: Cloud adoption is a fundamental enabler for financial institutions to achieve digital transformation goals, including improved customer experiences and operational efficiency.

- Regulatory Compliance Innovation: Cloud providers are increasingly offering specialized features and compliance frameworks tailored to the financial sector, reducing the burden on institutions.

- Geographic Expansion Potential: Emerging markets and regions undergoing rapid economic digitization present significant untapped opportunities for cloud service providers.

- AI and ML Integration: The synergy between cloud computing and AI/ML will continue to drive innovation in areas like fraud detection, personalized banking, and risk assessment.

- Focus on Cybersecurity: Enhanced cybersecurity measures and data encryption will remain a top priority for financial institutions leveraging cloud services.

Private and Public Cloud in Financial Service Market Drivers Analysis

The Private and Public Cloud in Financial Service Market is primarily propelled by the urgent need for digital transformation across the banking, financial services, and insurance (BFSI) sectors. Financial institutions are under immense pressure to modernize outdated legacy systems, which are costly to maintain and lack the agility required for today's fast-paced digital economy. Cloud adoption offers a scalable, flexible, and cost-effective alternative, enabling rapid deployment of new services, enhanced operational efficiency, and improved data analytics capabilities. This shift is crucial for maintaining competitiveness against agile FinTech startups and meeting evolving customer expectations for seamless digital experiences.

Another significant driver is the increasing demand for enhanced data security and regulatory compliance. While initial concerns about cloud security were prevalent, cloud providers have invested heavily in robust security frameworks and compliance certifications tailored specifically for the financial industry. These advanced security measures, combined with the ability to ensure data residency and sovereignty, are alleviating concerns and driving adoption. Furthermore, the global drive for cost optimization, particularly in IT infrastructure, encourages financial firms to leverage the economies of scale offered by cloud services, reducing capital expenditure and converting it into operational expenditure, which is often more predictable and manageable.

| Drivers | Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Digital Transformation Imperative | +4.2% | Global, particularly North America, Europe, Asia Pacific | Short to Mid-Term (2025-2029) |

| Cost Optimization and Operational Efficiency | +3.8% | Global | Mid to Long-Term (2026-2033) |

| Growing Demand for Scalability and Agility | +3.5% | Global, especially emerging markets | Short to Mid-Term (2025-2029) |

| Enhanced Data Security and Compliance Offerings | +3.1% | Global, particularly highly regulated regions | Mid to Long-Term (2026-2033) |

| Rise of FinTech and Neobanks | +2.7% | Global, significant in APAC and Europe | Short to Mid-Term (2025-2030) |

Private and Public Cloud in Financial Service Market Restraints Analysis

Despite the numerous advantages, the Private and Public Cloud in Financial Service Market faces significant restraints, primarily stemming from stringent regulatory and compliance requirements. Financial institutions operate under complex frameworks such as GDPR, HIPAA, PCI DSS, and various national banking regulations, which dictate how data must be stored, processed, and secured. Migrating sensitive customer and transaction data to the cloud raises concerns about data sovereignty, audit trails, and the ability to meet regulatory obligations, especially in multi-cloud or hybrid environments. The onus often falls on the financial institution to ensure compliance, even when leveraging third-party cloud services, creating a significant hurdle.

Another key restraint is the inherent complexity and cost associated with migrating legacy systems. Many financial institutions rely on decades-old, highly customized mainframe systems that are difficult to untangle and re-architect for cloud environments. The migration process can be time-consuming, expensive, and carries significant operational risks, including potential service disruptions. Furthermore, concerns about vendor lock-in, where institutions become overly reliant on a single cloud provider, can deter broad adoption, as it limits flexibility and bargaining power. Addressing these challenges requires careful strategic planning, significant investment, and a phased approach to cloud integration.

| Restraints | Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Regulatory and Compliance Requirements | -3.7% | Global, highly prominent in Europe and North America | Short to Long-Term (2025-2033) |

| Legacy System Migration Complexity and Costs | -3.2% | Global, particularly established institutions | Short to Mid-Term (2025-2030) |

| Data Residency and Sovereignty Concerns | -2.8% | Europe, Asia Pacific, various national jurisdictions | Mid to Long-Term (2026-2033) |

| Perceived Security Risks and Trust Issues | -2.5% | Global | Short to Mid-Term (2025-2029) |

| Vendor Lock-in Concerns | -2.1% | Global | Mid to Long-Term (2026-2033) |

Private and Public Cloud in Financial Service Market Opportunities Analysis

The Private and Public Cloud in Financial Service Market presents significant growth opportunities, particularly in the realm of specialized cloud solutions tailored for the financial sector. As regulatory requirements become more specific and complex, cloud providers that offer industry-specific compliance frameworks, data residency guarantees, and enhanced security features gain a competitive edge. This specialization allows financial institutions to accelerate their cloud adoption with greater confidence, knowing that their chosen platform is designed to meet their unique operational and legal demands. Furthermore, the rise of FinTech innovations and the increasing need for real-time data analytics create substantial opportunities for cloud providers to offer robust platforms that support these emerging technologies, facilitating faster development and deployment of new financial products and services.

Another crucial opportunity lies in leveraging hybrid and multi-cloud strategies to optimize workload placement and enhance business continuity. Financial institutions can strategically distribute their applications and data across various cloud environments, balancing the cost-effectiveness and innovation of public clouds with the control and security of private clouds. This approach not only improves resilience and disaster recovery capabilities but also empowers institutions to select the best-fit cloud for each specific application, avoiding vendor lock-in and maximizing efficiency. The untapped potential in emerging markets, where rapid digitalization and less entrenched legacy infrastructure exist, also offers a fertile ground for cloud adoption and expansion of financial services, including digital banking and mobile payments.

| Opportunities | Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Industry-Specific Cloud Solutions | +4.0% | Global, particularly North America and Europe | Short to Mid-Term (2025-2030) |

| Expansion in Emerging Markets | +3.6% | Asia Pacific, Latin America, Africa | Mid to Long-Term (2026-2033) |

| Leveraging AI, ML, and Blockchain on Cloud | +3.3% | Global | Short to Mid-Term (2025-2029) |

| Growth of Hybrid and Multi-Cloud Architectures | +3.0% | Global | Short to Long-Term (2025-2033) |

| Managed Cloud Services for Compliance and Security | +2.8% | Global | Mid to Long-Term (2026-2033) |

Private and Public Cloud in Financial Service Market Challenges Impact Analysis

The Private and Public Cloud in Financial Service Market faces significant challenges, notably the complex issue of data governance and management across distributed cloud environments. Financial institutions handle vast amounts of sensitive customer data and transactional information, requiring meticulous attention to data lineage, quality, and access control. In a hybrid or multi-cloud setup, ensuring consistent data policies, auditability, and compliance with varying regional data protection laws becomes exceptionally intricate. The lack of standardized data governance frameworks across different cloud providers can lead to inconsistencies and increase the risk of non-compliance, posing a substantial hurdle for seamless cloud integration.

Another critical challenge is the persistent cybersecurity threat landscape. While cloud providers invest heavily in security, the shared responsibility model means financial institutions retain significant accountability for securing their data and applications within the cloud. The rise of sophisticated cyberattacks, including ransomware, phishing, and insider threats, necessitates continuous vigilance and advanced security expertise. Moreover, a significant talent gap exists in cloud security and architecture, making it difficult for financial institutions to recruit and retain personnel with the specialized skills needed to manage complex cloud environments securely and efficiently. This skill deficit can impede migration efforts and increase operational risks.

| Challenges | Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Governance and Management Complexity | -3.5% | Global | Short to Long-Term (2025-2033) |

| Cybersecurity Threats and Data Breaches | -3.0% | Global | Short to Long-Term (2025-2033) |

| Skill Gap in Cloud Expertise and Security | -2.7% | Global, particularly developed economies | Short to Mid-Term (2025-2030) |

| Integration with Existing Legacy Infrastructure | -2.3% | Global, especially traditional banks | Short to Mid-Term (2025-2029) |

| Performance and Latency Issues | -1.9% | Global, critical for high-frequency trading | Short to Mid-Term (2025-2028) |

Private and Public Cloud in Financial Service Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Private and Public Cloud in Financial Service Market, offering a detailed understanding of market dynamics, growth drivers, restraints, opportunities, and challenges. It includes an extensive segmentation analysis covering deployment models, service types, applications, and organizational sizes, alongside a thorough regional assessment. The report also highlights the competitive landscape, featuring profiles of key market players and their strategic initiatives, to deliver actionable insights for stakeholders. The objective is to provide a holistic view of the market's current state and future trajectory, enabling informed decision-making for businesses operating within or looking to enter this dynamic sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 68.4 billion |

| Market Forecast in 2033 | USD 268.7 billion |

| Growth Rate | 18.5% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amazon Web Services (AWS), Microsoft Azure, Google Cloud, IBM, Oracle, Salesforce, SAP, Alibaba Cloud, Tencent Cloud, Huawei Cloud, Rackspace Technology, VMware, Cisco Systems, Dell Technologies, Hewlett Packard Enterprise (HPE), Accenture, Capgemini, Infosys, Wipro, TCS |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Private and Public Cloud in Financial Service Market is comprehensively segmented to provide granular insights into its diverse components and drivers. These segmentations are critical for understanding market dynamics, identifying high-growth areas, and tailoring strategies to specific industry needs. Each segment reflects unique operational requirements, regulatory considerations, and technological preferences within the financial services ecosystem. This detailed breakdown enables stakeholders to pinpoint opportunities and challenges across different deployment models, service types, applications, organization sizes, and specific financial service verticals.

The market's segmentation by deployment model into Public, Private, and Hybrid Cloud illustrates the varied approaches financial institutions adopt based on their risk appetite, data sensitivity, and control requirements. Service type segmentation (SaaS, PaaS, IaaS) highlights the prevalent modes of cloud consumption, from ready-to-use applications to foundational infrastructure. Furthermore, dissecting the market by application (e.g., core banking, fraud detection, risk management) reveals the specific areas where cloud technology delivers the most significant value. Organizational size and financial service type segments provide further granularity, distinguishing the needs of large incumbent banks from agile FinTech startups or specialized insurance providers, thereby offering a multifaceted view of the market's structure.

- Deployment Model: Public Cloud, Private Cloud, Hybrid Cloud

- Service Type: Software as a Service (SaaS), Platform as a Service (PaaS), Infrastructure as a Service (IaaS)

- Application: Core Banking, Payment Processing, Fraud Detection and Security, Risk Management, Data Analytics, Customer Relationship Management (CRM), Asset Management, Trading & Brokerage, Others

- Organization Size: Large Enterprises, Small and Medium-sized Enterprises (SMEs)

- Financial Service Type: Banking (Retail Banking, Corporate Banking, Investment Banking), Insurance (Life Insurance, Non-Life Insurance), Capital Markets (Brokerage, Asset Management, Wealth Management), Others (FinTech, Lending Platforms)

Regional Highlights

North America is projected to hold a significant share of the Private and Public Cloud in Financial Service Market, driven by the presence of major financial hubs, early adoption of cloud technologies, and substantial investments in digital transformation initiatives. The region benefits from a robust technological infrastructure and a strong innovation ecosystem, with financial institutions leveraging cloud for advanced analytics, AI-driven services, and enhanced cybersecurity. Stringent regulatory frameworks also push institutions towards compliant and secure cloud solutions, fostering a mature market.

Europe is also a key market, characterized by strong regulatory emphasis on data privacy and sovereignty, which fuels the adoption of private and hybrid cloud models. Countries like the UK, Germany, and France are leading the way in cloud migration within the financial sector, supported by initiatives like the Digital Single Market. Asia Pacific (APAC) is anticipated to exhibit the highest growth rate, propelled by rapid digital transformation, increasing internet penetration, the rise of digital-native banks and FinTechs, and growing investments in cloud infrastructure, particularly in countries like China, India, Japan, and Australia. Latin America and the Middle East & Africa (MEA) are emerging markets with significant potential, driven by financial inclusion initiatives, modernization of banking systems, and government support for cloud adoption, albeit at an earlier stage of maturity.

- North America: Dominant market share due to technological maturity, early cloud adoption, and significant investments by large financial institutions. Strong focus on hybrid cloud for security and compliance.

- Europe: High adoption driven by GDPR and other data privacy regulations, favoring private and hybrid cloud solutions. UK, Germany, and France are leading countries.

- Asia Pacific (APAC): Highest growth potential owing to rapid digital transformation, burgeoning FinTech sector, and increasing cloud spending in emerging economies like China and India.

- Latin America: Growing market fueled by financial inclusion efforts, modernization of banking infrastructure, and increasing demand for cost-effective cloud solutions.

- Middle East and Africa (MEA): Emerging market with increasing government initiatives for digital economy and smart cities, driving cloud adoption in the financial sector for efficiency and innovation.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Private and Public Cloud in Financial Service Market.- Amazon Web Services (AWS)

- Microsoft Azure

- Google Cloud

- IBM

- Oracle

- Salesforce

- SAP

- Alibaba Cloud

- Tencent Cloud

- Huawei Cloud

- Rackspace Technology

- VMware

- Cisco Systems

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- Accenture

- Capgemini

- Infosys

- Wipro

- Tata Consultancy Services (TCS)

Frequently Asked Questions

Analyze common user questions about the Private and Public Cloud in Financial Service market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate for the Private and Public Cloud in Financial Service Market?

The Private and Public Cloud in Financial Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033, reaching an estimated USD 268.7 billion by the end of the forecast period.

What are the primary drivers for cloud adoption in the financial sector?

Key drivers include the imperative for digital transformation, cost optimization, demand for scalability and agility, enhanced data security offerings, and the rise of FinTech innovations, all pushing financial institutions towards cloud-based solutions.

How do regulatory compliance and data sovereignty impact cloud choice for financial services?

Regulatory compliance and data sovereignty are significant factors, often leading financial institutions to adopt hybrid or private cloud models. These models offer greater control over data location and robust security features required to meet stringent regulations like GDPR and specific regional data residency laws.

What role does AI play in the Private and Public Cloud in Financial Service Market?

AI significantly impacts the market by enabling enhanced fraud detection, personalized customer experiences, optimized risk management, automated compliance, and algorithmic trading, leveraging the scalable computing power and data storage capabilities of cloud platforms.

Which regions are leading in cloud adoption within financial services?

North America currently holds a dominant market share due to its technological maturity and early adoption. Europe is also a significant market. Asia Pacific is expected to exhibit the highest growth rate driven by rapid digital transformation and FinTech expansion.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted