Printed Circuit Board Market

Printed Circuit Board Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705510 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Printed Circuit Board Market Size

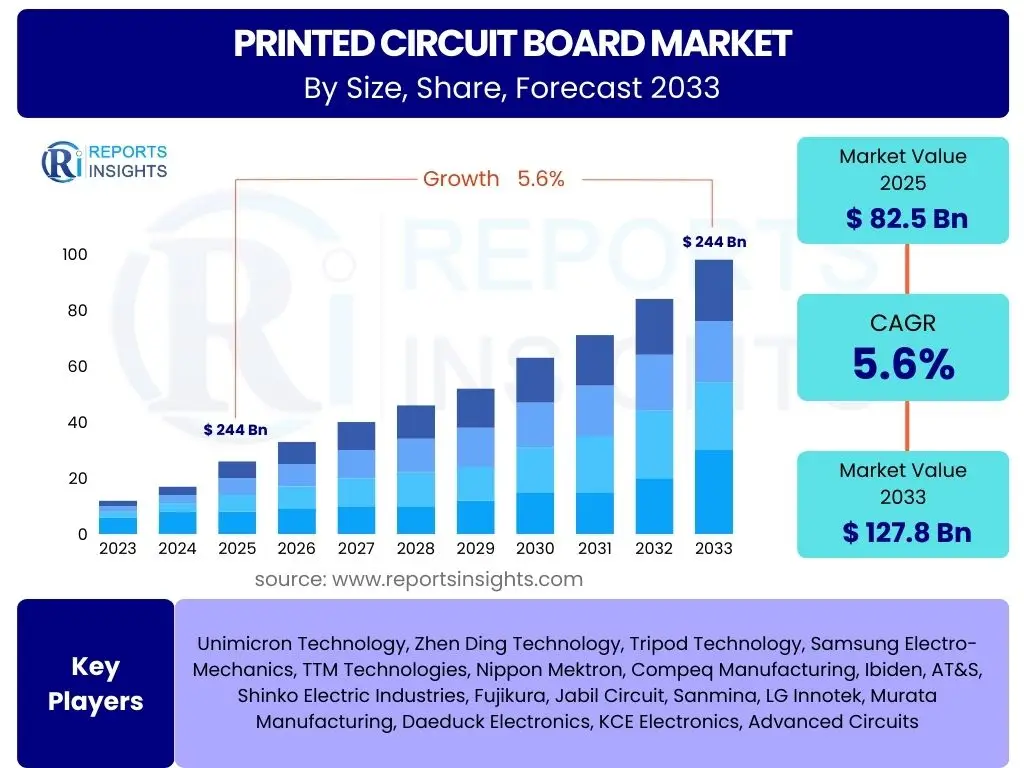

According to Reports Insights Consulting Pvt Ltd, The Printed Circuit Board Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.6% between 2025 and 2033. The market is estimated at USD 82.5 billion in 2025 and is projected to reach USD 127.8 billion by the end of the forecast period in 2033.

Key Printed Circuit Board Market Trends & Insights

The Printed Circuit Board (PCB) market is undergoing significant transformation, driven by advancements in various end-use sectors and technological innovations. Key trends reflect a shift towards enhanced performance, miniaturization, and integration, alongside an increasing emphasis on sustainable manufacturing practices. Market participants are responding to the demand for higher density interconnects, flexible solutions, and specialized PCBs capable of handling high frequencies and power requirements. This evolution is crucial for supporting the next generation of electronic devices across consumer, industrial, automotive, and telecommunications applications, influencing design, material science, and manufacturing processes.

User inquiries frequently highlight the rising adoption of advanced PCB technologies such as High-Density Interconnect (HDI) PCBs, flexible and rigid-flex PCBs, and the integration of smart functionalities directly into the board. There is also considerable interest in how geopolitical factors and supply chain resilience are shaping market dynamics, particularly concerning raw material sourcing and manufacturing localization. Furthermore, the push for eco-friendly production methods and the development of biodegradable or recyclable PCB materials are emerging as critical considerations for industry stakeholders and consumers alike.

- Miniaturization and High-Density Interconnect (HDI) Adoption

- Increased Demand for Flexible and Rigid-Flex PCBs

- Integration of Smart Functionalities and IoT Devices

- Growth in Automotive Electronics and ADAS Applications

- Development of Advanced Materials for High-Frequency Applications

- Emphasis on Green Manufacturing and Sustainable Practices

- Expansion of 5G and Data Center Infrastructure

- Rise of Advanced Packaging Technologies

AI Impact Analysis on Printed Circuit Board

Artificial intelligence (AI) is set to profoundly impact the Printed Circuit Board (PCB) industry across its entire value chain, from design and manufacturing to quality assurance and supply chain management. User questions often revolve around how AI can enhance efficiency, reduce costs, and improve the reliability of PCBs. The primary focus is on leveraging AI for complex design optimization, where algorithms can rapidly evaluate millions of layout permutations to identify the most efficient and performant designs, significantly reducing development cycles and human error. This capability is particularly vital for intricate multi-layer and high-density boards.

Furthermore, AI's role in manufacturing processes is generating considerable interest. Predictive maintenance using AI models can monitor equipment performance and anticipate failures, thereby minimizing downtime and optimizing production flows. In quality control, AI-powered visual inspection systems can detect microscopic defects with unparalleled accuracy and speed, surpassing human capabilities and ensuring higher product reliability. Supply chain optimization through AI also addresses user concerns about resilience, enabling better forecasting, inventory management, and risk assessment in a volatile global market. The integration of AI is not merely an incremental improvement but a fundamental shift towards more intelligent, autonomous, and efficient PCB production.

- AI-driven PCB Design Optimization: Automated layout, routing, and component placement for enhanced performance and reduced design cycles.

- Predictive Maintenance in Manufacturing: AI algorithms analyze sensor data from production equipment to forecast failures, optimizing uptime and throughput.

- Enhanced Quality Control and Defect Detection: AI-powered vision systems for rapid and accurate identification of manufacturing flaws, improving yield rates.

- Supply Chain Optimization: AI for demand forecasting, inventory management, and logistics, ensuring resilient and efficient material flow.

- Simulation and Prototyping Acceleration: AI reduces physical prototyping needs by enabling more accurate and faster virtual simulations of PCB performance.

- Intelligent Material Selection: AI assists in choosing optimal materials based on performance requirements, cost, and environmental impact.

- Automated Test Program Generation: AI can accelerate the creation of test scripts, making verification processes more efficient.

Key Takeaways Printed Circuit Board Market Size & Forecast

The Printed Circuit Board (PCB) market is poised for robust expansion, driven primarily by the relentless innovation in electronic devices and the increasing demand for high-performance computing across various sectors. The market's significant Compound Annual Growth Rate (CAGR) from 2025 to 2033 underscores its foundational role in the global electronics industry. Key takeaways from the market size and forecast analysis reveal a dynamic landscape where technological advancements, such as miniaturization and the proliferation of IoT, serve as central growth accelerators. Users frequently inquire about the longevity of the market's growth and the primary sectors fueling this expansion, indicating a strong interest in long-term investment and strategic planning within the electronics ecosystem.

The projected substantial increase in market value by 2033 reflects a continued reliance on advanced PCBs for applications ranging from sophisticated consumer electronics and automotive systems to critical industrial automation and telecommunications infrastructure. This growth is not merely volume-driven but also stems from the increasing complexity and value of PCBs, including multi-layer, HDI, and flexible boards. Furthermore, the forecast highlights the opportunities within emerging economies and the strategic importance of research and development in new materials and manufacturing techniques to sustain market momentum. Understanding these core growth drivers and their long-term implications is essential for stakeholders navigating the evolving technological landscape.

- Consistent Growth Trajectory: The market is set for sustained growth with a 5.6% CAGR, indicating a healthy and expanding industry.

- Significant Market Value Increase: Projected to reach USD 127.8 billion by 2033 from USD 82.5 billion in 2025, showing substantial market expansion.

- Driven by Technology Proliferation: Growth is primarily fueled by advancements in consumer electronics, automotive, 5G, IoT, and industrial automation.

- High-Performance PCB Demand: Increasing adoption of HDI, flexible, rigid-flex, and advanced material PCBs contributes significantly to market value.

- Strategic Importance in Electronics: PCBs remain a critical component, underpinning nearly all modern electronic systems and innovations.

- Opportunities in Emerging Markets: Developing regions present significant untapped potential for market penetration and growth.

Printed Circuit Board Market Drivers Analysis

The Printed Circuit Board (PCB) market's growth is propelled by a confluence of technological advancements and increasing adoption across diverse end-use industries. A primary driver is the relentless innovation in consumer electronics, where demand for smaller, more powerful, and feature-rich devices necessitates highly sophisticated PCBs. This includes everything from smartphones and wearables to advanced home appliances. Concurrently, the proliferation of the Internet of Things (IoT) devices across all sectors, from smart homes to industrial automation, significantly boosts the need for compact, energy-efficient, and reliable PCBs capable of handling complex sensor data and connectivity requirements.

Another crucial driver is the rapid expansion of the automotive electronics sector. Modern vehicles are becoming increasingly reliant on electronic systems for everything from advanced driver-assistance systems (ADAS) and infotainment to powertrain management and safety features. This trend mandates the use of robust, high-performance PCBs designed to withstand harsh operating environments and ensure critical system functionality. Furthermore, the global rollout of 5G infrastructure and the continuous expansion of data centers contribute substantially to market growth, driving demand for high-frequency, high-speed, and high-layer count PCBs capable of supporting massive data transfer rates and complex network architectures.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Consumer Electronics | +1.5% | Asia Pacific, North America, Europe | 2025-2033 |

| Expansion of Automotive Electronics | +1.2% | Europe, North America, Japan, China | 2025-2033 |

| Proliferation of IoT Devices | +1.0% | Global | 2025-2033 |

| Advancements in 5G Technology and Data Centers | +0.9% | North America, Asia Pacific, Europe | 2025-2033 |

| Industrial Automation and Smart Manufacturing | +0.8% | Europe, North America, Asia Pacific | 2025-2033 |

Printed Circuit Board Market Restraints Analysis

Despite robust growth prospects, the Printed Circuit Board (PCB) market faces several significant restraints that could impede its trajectory. One prominent challenge is the volatility and increasing cost of raw materials. Key materials like copper, various resins, and specialized laminates are subject to global supply chain disruptions, geopolitical tensions, and fluctuating commodity prices. These cost pressures directly impact manufacturing expenses, potentially leading to higher end-product prices and compressed profit margins for PCB manufacturers, especially for high-volume, low-margin applications. This volatility necessitates strategic sourcing and inventory management to mitigate risks.

Another substantial restraint is the complexity associated with the manufacturing of advanced PCBs, such as High-Density Interconnect (HDI) boards and flexible PCBs. These boards require specialized equipment, highly skilled labor, and stringent quality control processes, which translates to higher capital expenditure and operational costs. The miniaturization trend, while a driver, also exacerbates manufacturing challenges, increasing the likelihood of defects and demanding more precise fabrication techniques. Furthermore, stringent environmental regulations regarding chemical usage and waste disposal in PCB manufacturing facilities impose additional compliance costs and operational complexities, particularly in developed regions with strict environmental protection policies. The need for significant investment in advanced technology and expertise to meet evolving design requirements also acts as a barrier for smaller players to enter or compete effectively in the high-end segments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Raw Material Prices | -0.7% | Global | 2025-2030 |

| High Manufacturing Complexity and Costs | -0.6% | Global, particularly advanced segments | 2025-2033 |

| Strict Environmental Regulations | -0.5% | Europe, North America, East Asia | 2025-2033 |

| Intense Price Competition | -0.4% | Asia Pacific, Global | 2025-2033 |

| Technological Obsolescence and Rapid Innovation Cycles | -0.3% | Global | 2025-2028 |

Printed Circuit Board Market Opportunities Analysis

The Printed Circuit Board (PCB) market is rich with opportunities, primarily stemming from the continuous evolution of electronic applications and the growing demand for specialized board types. A significant avenue for growth lies in the burgeoning adoption of High-Density Interconnect (HDI) PCBs. As electronic devices become smaller and more functional, HDI technology, with its finer lines, smaller vias, and increased routing density, becomes indispensable. This creates substantial opportunities for manufacturers capable of producing such intricate boards, particularly for premium consumer electronics, medical devices, and advanced networking equipment, where space is at a premium and performance is critical. Furthermore, the rapid expansion of the electric vehicle (EV) market presents a massive opportunity, as EVs require a multitude of high-reliability PCBs for power management, battery management systems, infotainment, and charging infrastructure.

Another promising area is the increasing integration of artificial intelligence (AI) and machine learning (ML) capabilities into various systems, which necessitates specialized PCBs optimized for high-speed data processing and thermal management. This includes PCBs for AI accelerators, edge computing devices, and advanced robotics. The growing emphasis on sustainable electronics also opens doors for innovation in eco-friendly PCB manufacturing processes and materials. Companies investing in biodegradable substrates, lead-free solders, and reduced chemical waste can gain a competitive advantage and appeal to environmentally conscious consumers and regulations. Lastly, the expansion of healthcare technology, particularly medical wearables and diagnostic equipment, offers a stable and high-value market segment for advanced, reliable, and often flexible PCBs.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Demand for High-Density Interconnect (HDI) PCBs | +1.3% | Global | 2025-2033 |

| Growth in Electric Vehicle (EV) Electronics | +1.1% | Europe, North America, China | 2025-2033 |

| Integration of AI/ML in Electronic Systems | +1.0% | North America, Asia Pacific | 2025-2033 |

| Development of Sustainable and Eco-friendly PCBs | +0.9% | Europe, North America | 2028-2033 |

| Expansion of Medical and Healthcare Electronics | +0.8% | North America, Europe, Asia Pacific | 2025-2033 |

Printed Circuit Board Market Challenges Impact Analysis

The Printed Circuit Board (PCB) market, while growing, is not immune to significant challenges that can impact its sustained development. One primary challenge is the intensifying global competition, particularly from Asian manufacturers who often offer highly competitive pricing due to lower labor costs and economies of scale. This pressure can erode profit margins for manufacturers in other regions and necessitate continuous investment in automation and efficiency to remain competitive. Moreover, the rapid pace of technological change within the electronics industry presents a constant challenge. PCBs must evolve quickly to support new semiconductor technologies, higher frequencies, and more complex functionalities, requiring significant R&D investment and a flexible manufacturing infrastructure to adapt to these shifts rapidly.

Another critical challenge is the inherent complexity of advanced PCB manufacturing, which demands specialized expertise and precision. Producing multi-layer, HDI, and flexible PCBs with high yields is technically challenging and requires sophisticated equipment, skilled technicians, and robust quality control systems. This complexity contributes to higher production costs and longer lead times for custom or advanced orders. Furthermore, geopolitical tensions and trade disputes pose significant supply chain risks, potentially disrupting the availability of critical raw materials or specialized components, and impacting production schedules. Cybersecurity threats targeting manufacturing control systems and intellectual property are also emerging concerns, demanding robust protective measures and ongoing vigilance from PCB manufacturers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intensifying Global Competition | -0.8% | Global | 2025-2033 |

| Rapid Technological Obsolescence | -0.7% | Global | 2025-2030 |

| Skilled Labor Shortages and Workforce Training | -0.6% | North America, Europe | 2025-2033 |

| Supply Chain Disruptions and Geopolitical Risks | -0.5% | Global | 2025-2028 |

| High Capital Investment Requirements | -0.4% | Global, particularly new entrants | 2025-2033 |

Printed Circuit Board Market - Updated Report Scope

This market research report provides an in-depth analysis of the global Printed Circuit Board (PCB) market, offering comprehensive insights into its current size, historical performance, and future growth projections. The scope includes detailed segmentation by type, application, material, and laminate, allowing for a granular understanding of market dynamics. It further delves into regional market trends and competitive landscape analysis, identifying key players, their strategies, and market positioning. The report serves as a strategic tool for stakeholders to comprehend market opportunities, challenges, and the impact of emerging technologies like AI, enabling informed decision-making and strategic planning within the dynamic electronics industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 82.5 Billion |

| Market Forecast in 2033 | USD 127.8 Billion |

| Growth Rate | 5.6% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Unimicron Technology, Zhen Ding Technology, Tripod Technology, Samsung Electro-Mechanics, TTM Technologies, Nippon Mektron, Compeq Manufacturing, Ibiden, AT&S, Shinko Electric Industries, Fujikura, Jabil Circuit, Sanmina, LG Innotek, Murata Manufacturing, Daeduck Electronics, KCE Electronics, Advanced Circuits |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Printed Circuit Board (PCB) market is extensively segmented to reflect the diversity of products, materials, and applications that drive its growth. This detailed segmentation allows for a nuanced understanding of specific market niches and their unique dynamics. By breaking down the market into various types of PCBs, such as single-sided, double-sided, multi-layer, and advanced categories like HDI, flexible, and rigid-flex, the report provides clarity on the technological complexity and market demand for each. Each PCB type caters to distinct performance requirements, cost considerations, and design constraints, ranging from basic electronic components to highly sophisticated systems found in aerospace and medical applications.

Further segmentation by laminate type, including commonly used FR-4, high-Tg FR-4, and flexible laminates, highlights the importance of material science in PCB manufacturing. The choice of laminate directly impacts the board's electrical performance, thermal properties, and mechanical durability, which are critical for various end-use environments. Application-based segmentation, encompassing consumer electronics, automotive, telecommunications, and industrial sectors, illustrates how diverse industries rely on customized PCB solutions. This comprehensive breakdown underscores the market's adaptability and its integral role in supporting a vast array of electronic devices and systems worldwide, enabling targeted strategic planning for market participants.

- By Type: Single-Sided PCB, Double-Sided PCB, Multi-Layer PCB, High-Density Interconnect (HDI) PCB, Flexible PCB, Rigid-Flex PCB, Other PCB Types

- By Laminate Type: FR-4, High-Tg FR-4, Flexible Laminates, CEM, Polyimide, Teflon, Others

- By Application: Consumer Electronics, Automotive, Telecommunications, Industrial Electronics, Medical Devices, Aerospace & Defense, Computers, Others

- By End-Use Industry: Communications, Computers, Consumer Electronics, Industrial, Military/Aerospace, Medical, Automotive

Regional Highlights

The global Printed Circuit Board (PCB) market exhibits distinct regional dynamics, influenced by manufacturing capabilities, technological adoption rates, and end-use industry concentration. Asia Pacific, particularly China, Taiwan, South Korea, and Japan, dominates the market due to its extensive electronics manufacturing ecosystem, low labor costs, and high production volumes of consumer electronics, telecommunications equipment, and automotive components. This region is a global hub for PCB fabrication, benefiting from well-established supply chains and continuous investment in advanced manufacturing technologies. The increasing disposable income and growing demand for electronic devices further solidify APAC's leading position, making it a critical market for both production and consumption.

North America and Europe represent significant markets for high-value and specialized PCBs, driven by strong R&D, advanced industrial automation, medical device manufacturing, and aerospace and defense sectors. These regions prioritize quality, reliability, and advanced functionalities, leading to higher adoption of HDI, flexible, and high-performance multi-layer PCBs. While their production volumes may be lower compared to APAC, the average selling price and technological complexity of PCBs in these regions are significantly higher. Latin America and the Middle East & Africa (MEA) are emerging markets, showing increasing potential due to growing industrialization, infrastructure development, and rising consumer demand for electronic goods, gradually expanding their share in the global PCB landscape.

- Asia Pacific (APAC): Dominant market in terms of production and consumption, driven by robust electronics manufacturing, consumer electronics demand, and telecommunications infrastructure. Countries like China, Taiwan, South Korea, and Japan are key players.

- North America: A significant market for high-performance and specialized PCBs, with strong demand from aerospace, defense, medical, and advanced computing sectors. Focus on technological innovation and high-value applications.

- Europe: Characterized by strong automotive electronics, industrial automation, and medical device industries. Emphasis on high-quality, reliable, and often custom-engineered PCB solutions, with Germany and the UK leading.

- Latin America: Emerging market with growing manufacturing capabilities and increasing demand for consumer electronics and automotive applications, particularly in Brazil and Mexico.

- Middle East and Africa (MEA): Gradually expanding market driven by infrastructure development, increasing digitalization, and investments in telecommunications and industrial sectors, though still smaller in comparison to other regions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Printed Circuit Board Market.- Unimicron Technology

- Zhen Ding Technology

- Tripod Technology

- Samsung Electro-Mechanics

- TTM Technologies

- Nippon Mektron

- Compeq Manufacturing

- Ibiden

- AT&S

- Shinko Electric Industries

- Fujikura

- Jabil Circuit

- Sanmina

- LG Innotek

- Murata Manufacturing

- Daeduck Electronics

- KCE Electronics

- Advanced Circuits

Frequently Asked Questions

Analyze common user questions about the Printed Circuit Board market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Printed Circuit Board market?

The Printed Circuit Board (PCB) market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.6% between 2025 and 2033, reflecting steady expansion.

Which factors are driving the growth of the PCB market?

Key drivers include the surging demand for consumer electronics, the expansion of automotive electronics (especially EVs), the proliferation of IoT devices, and advancements in 5G technology and data center infrastructure.

How is AI impacting the Printed Circuit Board industry?

AI significantly impacts the PCB industry through optimized design, predictive maintenance in manufacturing, enhanced quality control for defect detection, and more efficient supply chain management, leading to improved efficiency and cost reduction.

What are the primary challenges facing the Printed Circuit Board market?

Major challenges include the volatility of raw material prices, high manufacturing complexity and costs for advanced PCBs, intense global competition, and strict environmental regulations affecting production processes.

Which region holds the largest share in the Printed Circuit Board market?

Asia Pacific (APAC) currently holds the largest market share in the Printed Circuit Board market, driven by its robust electronics manufacturing ecosystem and high production volumes.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted