Pressure Vessel Market

Pressure Vessel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704909 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

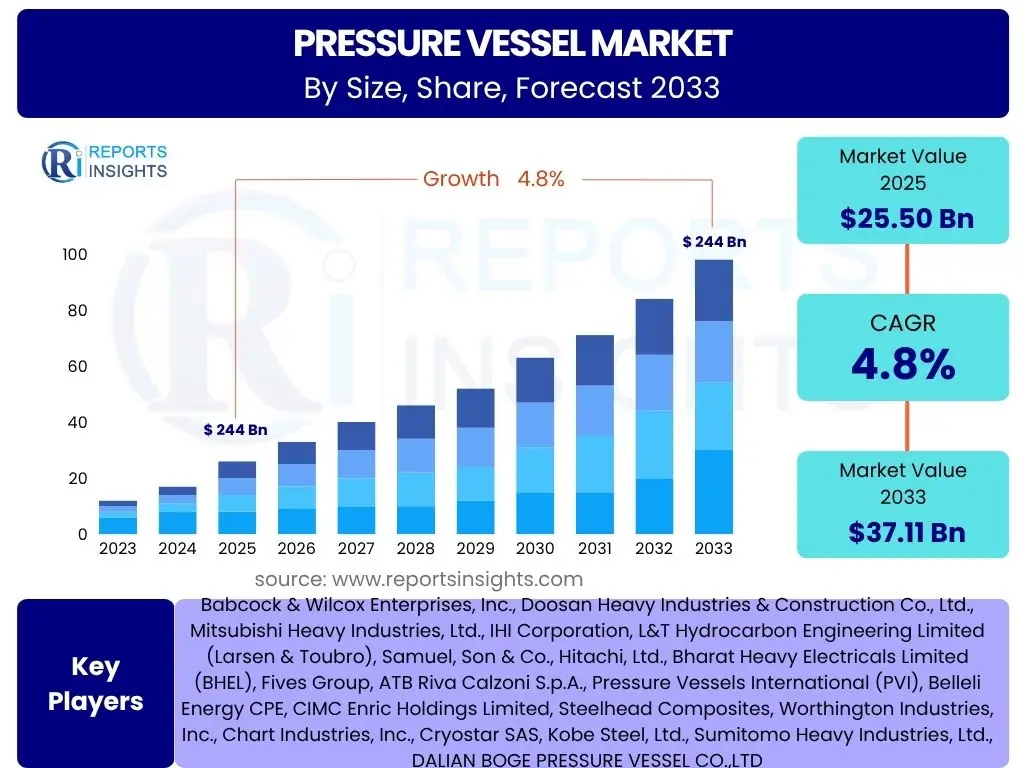

Pressure Vessel Market Size

According to Reports Insights Consulting Pvt Ltd, The Pressure Vessel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 25.50 Billion in 2025 and is projected to reach USD 37.11 Billion by the end of the forecast period in 2033. This consistent growth trajectory is primarily driven by expanding industrial applications across various sectors globally, coupled with a persistent demand for energy and chemical processing infrastructure. The market's valuation reflects its critical role in supporting industrial operations that rely on the safe containment of gases and liquids under high pressure or temperature conditions.

The projected growth underscores the essential nature of pressure vessels in modern industrial landscapes, from the foundational energy sector to advanced chemical manufacturing and renewable energy initiatives. Investment in new industrial projects, upgrades to existing facilities, and the stringent regulatory environment necessitating robust and reliable equipment all contribute to the sustained demand. Furthermore, the market's expansion is buoyed by technological advancements, including the development of new materials and manufacturing techniques that enhance vessel performance, safety, and operational efficiency, thereby expanding their applicability and lifespan.

Key Pressure Vessel Market Trends & Insights

Common user inquiries about the Pressure Vessel market frequently center on evolving industry practices, material innovations, and the adoption of new technologies. Analysis reveals a strong interest in understanding how global energy transitions, particularly the shift towards cleaner energy sources, are influencing demand and design requirements. Users are also keen to identify the impact of increasingly stringent safety and environmental regulations on manufacturing processes and operational standards.

A significant trend observed is the increasing emphasis on advanced materials, such as high-strength alloys and composites, which enable the design of lighter, more durable, and corrosion-resistant vessels capable of operating under extreme conditions. This material evolution is critical for new applications in areas like hydrogen storage and carbon capture. Concurrently, there is a growing trend towards modularization and standardization in vessel design and construction, aiming to reduce project timelines, mitigate costs, and enhance the scalability of industrial facilities. This approach supports rapid deployment and simplifies maintenance, particularly in large-scale projects.

The market is also witnessing a push towards greater operational efficiency and safety through the integration of digital technologies. This includes the adoption of smart sensors, IoT devices, and data analytics for real-time monitoring, predictive maintenance, and performance optimization. Furthermore, geopolitical shifts and global supply chain reconfigurations are prompting a re-evaluation of manufacturing locations and procurement strategies, leading to a more diversified and resilient supply network for pressure vessel components and finished products.

- Increased adoption of advanced materials (e.g., high-strength steel, composites) for enhanced durability and performance.

- Growing demand from the energy transition sector, particularly for hydrogen storage and carbon capture technologies.

- Emphasis on modularization and standardization to optimize manufacturing and deployment efficiency.

- Integration of smart technologies, IoT, and data analytics for real-time monitoring and predictive maintenance.

- Stringent regulatory frameworks driving demand for higher safety standards and compliant designs.

- Geographic shift in manufacturing and supply chain optimization towards regionalization.

- Rising focus on lifecycle cost optimization, including maintenance and operational efficiency.

AI Impact Analysis on Pressure Vessel

Common user questions regarding AI's influence on the Pressure Vessel industry typically revolve around how artificial intelligence can enhance design, manufacturing, operational efficiency, and safety. There is significant curiosity about AI's potential to optimize complex engineering calculations, streamline fabrication processes, and improve predictive maintenance capabilities, thereby reducing downtime and extending equipment lifespan. Users are also exploring how AI can contribute to real-time risk assessment and regulatory compliance, addressing critical safety concerns inherent in pressure vessel operations.

The primary impact of AI in the pressure vessel market is the revolutionization of design and engineering processes. AI algorithms can rapidly analyze vast datasets to optimize vessel geometries, material selection, and structural integrity, significantly reducing prototyping time and costs. This enables engineers to explore more innovative designs that meet specific operational demands while adhering to strict safety standards. Furthermore, AI-powered simulations can predict material behavior under various stress conditions, identifying potential failure points before physical construction begins, thereby enhancing overall product reliability and safety.

In manufacturing and operations, AI's role extends to predictive maintenance and quality control. Machine learning models analyze sensor data from operational vessels to predict equipment failures, enabling proactive maintenance scheduling and preventing costly unplanned downtime. AI-driven vision systems and robotic automation are also improving precision in welding and fabrication, ensuring higher quality welds and reducing human error. This comprehensive application of AI from design to deployment and maintenance is set to dramatically improve efficiency, safety, and cost-effectiveness across the pressure vessel lifecycle.

- Optimized Design and Engineering: AI algorithms for material selection, geometric optimization, and structural analysis, reducing design cycles and improving performance.

- Predictive Maintenance: AI-powered analytics of sensor data to forecast equipment failures, minimizing downtime and extending operational life.

- Enhanced Manufacturing Processes: AI-driven robotics and machine vision for precision welding, automated quality control, and reduced defects.

- Real-time Safety Monitoring: AI systems for continuous risk assessment, anomaly detection, and immediate alerts for operational deviations.

- Supply Chain Optimization: AI for demand forecasting, inventory management, and logistics, improving efficiency and resilience in material procurement.

Key Takeaways Pressure Vessel Market Size & Forecast

Analysis of user inquiries about the Pressure Vessel market size and forecast highlights a keen interest in understanding the factors driving its consistent growth, particularly in the context of global industrialization and energy transitions. Users frequently seek clarity on which end-use industries are major contributors to demand and how future technological advancements are expected to reshape the market landscape. There is also significant emphasis on identifying key investment areas and market segments poised for accelerated expansion over the forecast period.

A key takeaway from the market forecast is the robust and sustained demand for pressure vessels across a diversified range of industries, including oil and gas, chemicals, power generation, and emerging sectors like hydrogen and carbon capture. This pervasive demand underscores the non-negotiable role of these critical components in industrial infrastructure globally. The market's resilience is further bolstered by the continuous need for facility upgrades, maintenance, and the expansion of industrial capacities in developing economies, ensuring a stable growth trajectory.

Another crucial insight is the increasing influence of technological advancements and stringent regulatory mandates on market dynamics. Innovation in materials, design optimization, and smart monitoring technologies are not only enhancing the safety and efficiency of pressure vessels but also expanding their application scope. Furthermore, the global drive towards cleaner energy solutions is creating new avenues for growth, positioning the pressure vessel market as a pivotal enabler of the energy transition, particularly in the context of storing and transporting new energy carriers.

- The Pressure Vessel Market is poised for consistent growth, driven by expansion across key industrial sectors and global energy demands.

- Technological advancements, including new materials and digital integration, are critical enablers for market expansion and operational efficiency.

- Strict safety and environmental regulations are consistently shaping market requirements and driving innovation in vessel design and manufacturing.

- Emerging applications in the hydrogen economy and carbon capture, utilization, and storage (CCUS) represent significant growth opportunities.

- Geographic expansion of industrial infrastructure in developing regions will be a primary contributor to market demand.

Pressure Vessel Market Drivers Analysis

The Pressure Vessel Market is primarily driven by the ongoing expansion and modernization of industrial infrastructure across the globe. Key sectors such as oil and gas, chemicals, and power generation consistently require new vessels for capacity expansion, as well as replacements and upgrades for aging equipment to ensure operational safety and efficiency. The increasing global energy demand, coupled with growing investments in refining and petrochemical complexes, further fuels the market's growth, as these facilities are critically dependent on pressure vessels for various processes.

Furthermore, the intensifying focus on stringent safety and environmental regulations worldwide is a significant driver. Compliance with international codes and standards, such as ASME, PED, and others, necessitates the use of high-quality, certified pressure vessels, driving demand for new and compliant products. This regulatory push often leads to the replacement of older, non-compliant vessels, ensuring a continuous upgrade cycle within the market. Innovations in material science and manufacturing technologies also contribute to market growth by enabling the production of more efficient, durable, and application-specific vessels.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Industrialization & Infrastructure Development | +1.5% | Asia Pacific, Middle East & Africa, Latin America | 2025-2033 |

| Rising Demand from Oil & Gas and Chemical Industries | +1.2% | North America, Middle East, Europe, APAC | 2025-2033 |

| Stringent Safety and Environmental Regulations | +0.8% | Global, particularly Europe, North America, China | 2025-2033 |

| Advancements in Material Science & Manufacturing Technologies | +0.7% | Global | 2025-2033 |

| Investment in Renewable Energy Infrastructure (Hydrogen, CCUS) | +0.6% | Europe, North America, China, Japan | 2027-2033 |

Pressure Vessel Market Restraints Analysis

Despite the positive growth outlook, the Pressure Vessel Market faces several significant restraints that could impede its full potential. One of the primary challenges is the high capital expenditure required for manufacturing and procurement. The complex engineering, specialized materials, and rigorous testing involved in producing pressure vessels contribute to their elevated costs, which can deter investments, especially for smaller enterprises or in regions with limited financial resources. This cost intensity can lead to extended project timelines and budget constraints for end-users.

Another key restraint is the volatility of raw material prices, particularly for steel, nickel, and other alloys essential for vessel construction. Fluctuations in commodity markets directly impact manufacturing costs, making it difficult for manufacturers to maintain stable pricing and profit margins. Furthermore, the stringent and evolving regulatory landscape, while a driver for safety, can also act as a restraint. Adhering to diverse international and regional standards requires significant investment in compliance, testing, and certification, adding complexity and cost to the manufacturing process and potentially delaying market entry for new products.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Costs & Manufacturing Complexity | -0.9% | Global, impacts emerging economies more | 2025-2033 |

| Volatility in Raw Material Prices | -0.7% | Global, affects manufacturers | 2025-2030 |

| Stringent & Evolving Regulatory Landscape | -0.5% | Europe, North America (mature markets) | 2025-2033 |

| Shortage of Skilled Labor & Expertise | -0.4% | Global, particularly developed economies | 2025-2033 |

| Economic Downturns & Geopolitical Instability | -0.6% | Global, varies by region | Short to Medium Term (2025-2028) |

Pressure Vessel Market Opportunities Analysis

The Pressure Vessel Market is presented with substantial opportunities arising from the global energy transition and the increasing focus on sustainable industrial practices. The burgeoning hydrogen economy, for instance, requires specialized high-pressure vessels for production, storage, and transportation, opening a significant new market segment. Similarly, the growing adoption of Carbon Capture, Utilization, and Storage (CCUS) technologies necessitates bespoke pressure vessels designed to handle CO2 under specific conditions, representing a burgeoning area for innovation and demand.

Furthermore, the digital transformation sweeping across industrial sectors offers immense opportunities for market players. The integration of IoT, AI, and advanced analytics for smart manufacturing, predictive maintenance, and remote monitoring of pressure vessels can enhance operational efficiency, reduce lifecycle costs, and improve safety standards. This technological leap allows manufacturers to offer value-added services and develop next-generation 'smart' vessels. Additionally, the increasing demand for modular and compact industrial plants provides an opportunity for manufacturers to innovate in design, offering integrated pressure vessel solutions that simplify installation and reduce overall project complexity.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Hydrogen Economy (Production, Storage, Transport) | +1.0% | Europe, North America, Japan, South Korea, China | 2027-2033 |

| Expansion in Carbon Capture, Utilization, and Storage (CCUS) | +0.8% | North America, Europe, Middle East | 2026-2033 |

| Digital Transformation (IoT, AI, Predictive Maintenance) | +0.7% | Global, particularly developed markets | 2025-2033 |

| Modularization & Compact Plant Designs | +0.6% | Global, diverse industries | 2025-2033 |

| Demand from Emerging Economies & Infrastructure Projects | +0.5% | Asia Pacific, Latin America, Africa | 2025-2033 |

Pressure Vessel Market Challenges Impact Analysis

The Pressure Vessel Market faces several pervasive challenges that demand strategic responses from industry participants. Intense global competition is a significant hurdle, as numerous manufacturers vie for market share, leading to price pressures and reduced profit margins. This competition is exacerbated by the presence of both established players with extensive capabilities and emerging manufacturers, particularly from Asia, who offer cost-effective solutions, pushing established players to innovate and differentiate their offerings beyond mere price.

Managing complex and often fragile global supply chains presents another major challenge. Disruptions caused by geopolitical events, trade disputes, or natural disasters can severely impact the availability and cost of specialized raw materials and components, leading to production delays and increased operational costs. Furthermore, the imperative to continuously adhere to evolving and increasingly stringent international safety standards and environmental regulations adds significant complexity and cost to manufacturing processes, requiring substantial investment in research, development, and compliance infrastructure to meet diverse regional requirements.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Global Competition & Price Pressures | -0.8% | Global, especially in mature markets | 2025-2033 |

| Supply Chain Disruptions & Material Volatility | -0.6% | Global, affects all manufacturers | 2025-2030 |

| Adherence to Diverse International Standards & Regulations | -0.5% | Global, particularly for exports/imports | 2025-2033 |

| Lifecycle Cost Management & Maintenance Burden | -0.4% | Global, impacts end-users | 2025-2033 |

| Cybersecurity Risks in Smart & Connected Vessels | -0.3% | Developed economies with advanced infrastructure | 2026-2033 |

Pressure Vessel Market - Updated Report Scope

This report provides an in-depth analysis of the global Pressure Vessel market, offering comprehensive insights into its current size, historical trends, and future growth projections. It meticulously examines market dynamics, including key drivers, restraints, opportunities, and challenges influencing the industry landscape. The scope encompasses detailed segmentation analysis across various parameters such as material, type, and end-use industry, alongside a thorough regional assessment to highlight market performance across different geographies. The report further provides an exhaustive profiling of leading market players, offering strategic intelligence for stakeholders and investors.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.50 Billion |

| Market Forecast in 2033 | USD 37.11 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 256 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Babcock & Wilcox Enterprises, Inc., Doosan Heavy Industries & Construction Co., Ltd., Mitsubishi Heavy Industries, Ltd., IHI Corporation, L&T Hydrocarbon Engineering Limited (Larsen & Toubro), Samuel, Son & Co., Hitachi, Ltd., Bharat Heavy Electricals Limited (BHEL), Fives Group, ATB Riva Calzoni S.p.A., Pressure Vessels International (PVI), Belleli Energy CPE, CIMC Enric Holdings Limited, Steelhead Composites, Worthington Industries, Inc., Chart Industries, Inc., Cryostar SAS, Kobe Steel, Ltd., Sumitomo Heavy Industries, Ltd., DALIAN BOGE PRESSURE VESSEL CO.,LTD |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Pressure Vessel Market is extensively segmented based on material, type, application/end-use industry, manufacturing process, and design code, reflecting the diverse requirements and technological advancements within the sector. Each segmentation provides a granular view of market dynamics, enabling a more precise understanding of demand patterns and growth opportunities. The material segmentation highlights the shift towards high-performance alloys and composites for specialized applications, while the type segmentation delineates the varied functional roles pressure vessels play across industries, from fundamental storage to complex chemical reactions and heat exchange.

The application-based segmentation further illustrates the critical dependence of key industries, such as oil & gas, chemicals, and power generation, on pressure vessel technology for their core operations. Emerging applications in renewable energy and environmental management are also creating new segments, signifying the market's adaptability and expansion into novel areas. Understanding these intricate segmentations is crucial for market participants to identify lucrative niches, tailor product offerings, and devise effective market penetration strategies.

- By Material:

- Carbon Steel: Widely used for its cost-effectiveness and strength in general industrial applications.

- Stainless Steel: Preferred for applications requiring corrosion resistance and hygiene, common in food & beverage and pharmaceutical industries.

- Alloy Steel: Utilized for high-temperature and high-pressure environments, often in power generation and petrochemicals.

- Composites: Gaining traction for lightweight and high-strength applications, especially in aerospace, automotive, and hydrogen storage.

- Others: Includes materials like Titanium and Nickel Alloys for highly corrosive or specialized conditions.

- By Type:

- Boilers: Generate steam or hot water for power generation and process heating.

- Reactors: Facilitate chemical reactions under controlled conditions.

- Separators: Used to separate different phases (liquid-liquid, liquid-gas, gas-solid) in processes.

- Storage Vessels: Store gases or liquids at high pressures or low temperatures.

- Heat Exchangers: Transfer heat between fluids without direct contact.

- Columns: Used for distillation, absorption, or stripping processes.

- Others: Includes accumulators, filters, and pulsation dampeners.

- By Application/End-Use Industry:

- Oil & Gas: Encompassing upstream (exploration & production), midstream (transport & storage), and downstream (refining & petrochemicals) operations.

- Chemicals & Petrochemicals: For various processes including synthesis, separation, and storage of chemicals.

- Power Generation: Crucial for conventional thermal, nuclear, and emerging renewable energy plants.

- Food & Beverage: For processing, pasteurization, and storage of food products.

- Pharmaceuticals: Essential for sterile processing and storage in drug manufacturing.

- Water Treatment: Utilized in desalination plants and industrial water purification systems.

- Mining: For mineral processing and slurry transport.

- Others: Includes applications in automotive, aerospace & defense, and wastewater treatment.

- By Manufacturing Process:

- Forged Vessels: Offer high strength and integrity, suitable for extreme pressures.

- Welded Vessels: Most common type, versatile for various sizes and shapes.

- Seamless Vessels: High strength and integrity, used for gas cylinders.

- By Design Code:

- ASME (American Society of Mechanical Engineers): Dominant in North America.

- PED (Pressure Equipment Directive): Mandatory in the European Union.

- AD 2000: German standard.

- China GB Code: Chinese national standards.

- Others: Including JIS, BS, etc., depending on regional requirements.

Regional Highlights

- North America: A mature market characterized by significant demand from the oil and gas sector, particularly for shale gas extraction and processing. Stringent safety regulations and substantial investments in upgrading existing infrastructure and developing new energy projects drive market growth. The region is also at the forefront of adopting advanced materials and digital technologies in pressure vessel manufacturing and operation.

- Europe: Dominated by strict regulatory frameworks like the Pressure Equipment Directive (PED), ensuring high safety standards. The region is a key innovator in clean energy technologies, driving demand for pressure vessels in renewable energy projects, hydrogen infrastructure, and carbon capture initiatives. Industrial modernization and a strong chemical processing industry further contribute to market demand.

- Asia Pacific (APAC): The fastest-growing market, propelled by rapid industrialization, increasing energy demand, and significant investments in manufacturing, chemicals, and power generation across countries like China, India, and Southeast Asia. The region benefits from large-scale infrastructure projects and a growing focus on expanding industrial capacities, leading to high demand for all types of pressure vessels.

- Latin America: Experiencing growth due to ongoing investments in its vast oil and gas reserves, particularly in Brazil, Mexico, and Argentina. The development of mining industries and chemical plants also contributes to the demand for pressure vessels. Economic stability and foreign direct investment are key factors influencing market expansion in this region.

- Middle East and Africa (MEA): Heavily influenced by large-scale oil and gas exploration, production, and refining activities, leading to substantial demand for high-pressure and high-temperature vessels. Significant investments in petrochemical complexes and infrastructure development projects across the GCC countries and parts of Africa are major market drivers.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Pressure Vessel Market.- Babcock & Wilcox Enterprises, Inc.

- Doosan Heavy Industries & Construction Co., Ltd.

- Mitsubishi Heavy Industries, Ltd.

- IHI Corporation

- L&T Hydrocarbon Engineering Limited (Larsen & Toubro)

- Samuel, Son & Co.

- Hitachi, Ltd.

- Bharat Heavy Electricals Limited (BHEL)

- Fives Group

- ATB Riva Calzoni S.p.A.

- Pressure Vessels International (PVI)

- Belleli Energy CPE

- CIMC Enric Holdings Limited

- Steelhead Composites

- Worthington Industries, Inc.

- Chart Industries, Inc.

- Cryostar SAS

- Kobe Steel, Ltd.

- Sumitomo Heavy Industries, Ltd.

- DALIAN BOGE PRESSURE VESSEL CO.,LTD

Frequently Asked Questions

Analyze common user questions about the Pressure Vessel market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate for the Pressure Vessel Market?

The Pressure Vessel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033, reaching an estimated value of USD 37.11 Billion by 2033.

Which industries are the primary drivers of demand for pressure vessels?

The primary drivers of demand are the oil and gas, chemicals and petrochemicals, and power generation industries, along with emerging demand from the hydrogen economy and carbon capture sectors.

How is artificial intelligence (AI) impacting the Pressure Vessel industry?

AI is impacting the industry through optimized design and engineering, enhanced predictive maintenance, improved manufacturing processes, and real-time safety monitoring, leading to greater efficiency and safety.

What are the key materials used in pressure vessel manufacturing?

Key materials include Carbon Steel, Stainless Steel, Alloy Steel, and Composites, chosen based on application requirements for strength, corrosion resistance, and operational conditions.

Which regions are expected to show significant growth in the Pressure Vessel Market?

The Asia Pacific (APAC) region is expected to be the fastest-growing market due to rapid industrialization, while North America and Europe continue to be significant markets driven by regulatory compliance and technological adoption.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted