Power Semiconductor Switche Device Market

Power Semiconductor Switche Device Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710352 | Last Updated : January 05, 2026 |

Format : ![]()

![]()

![]()

![]()

Power Semiconductor Switche Device Market Size

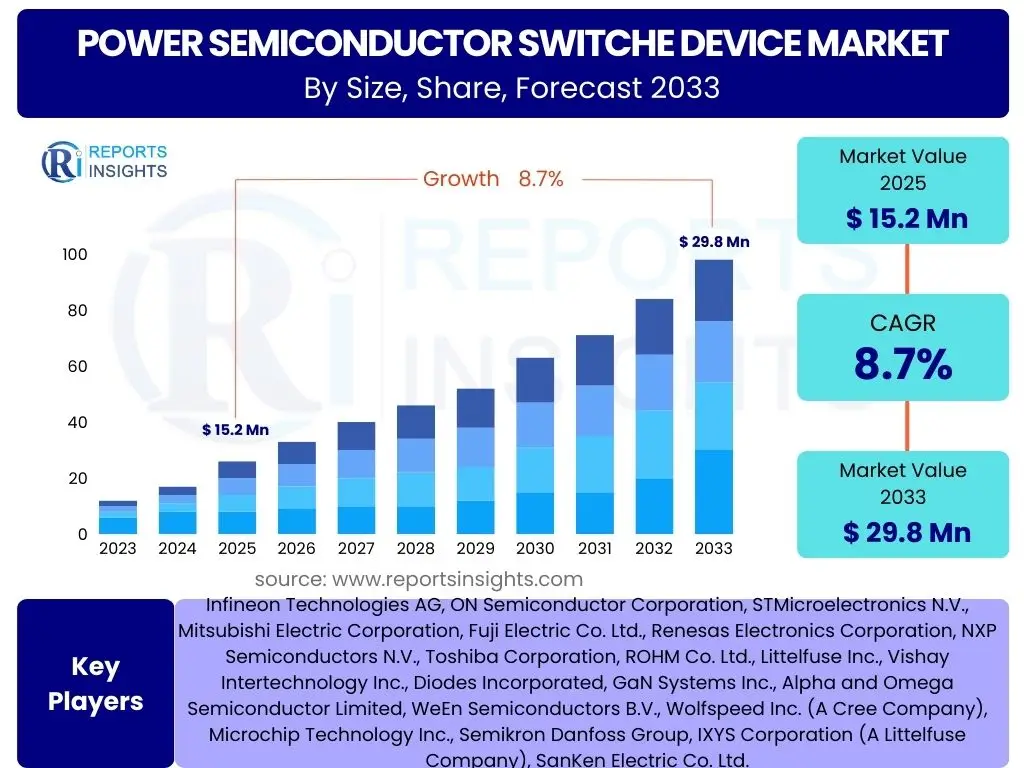

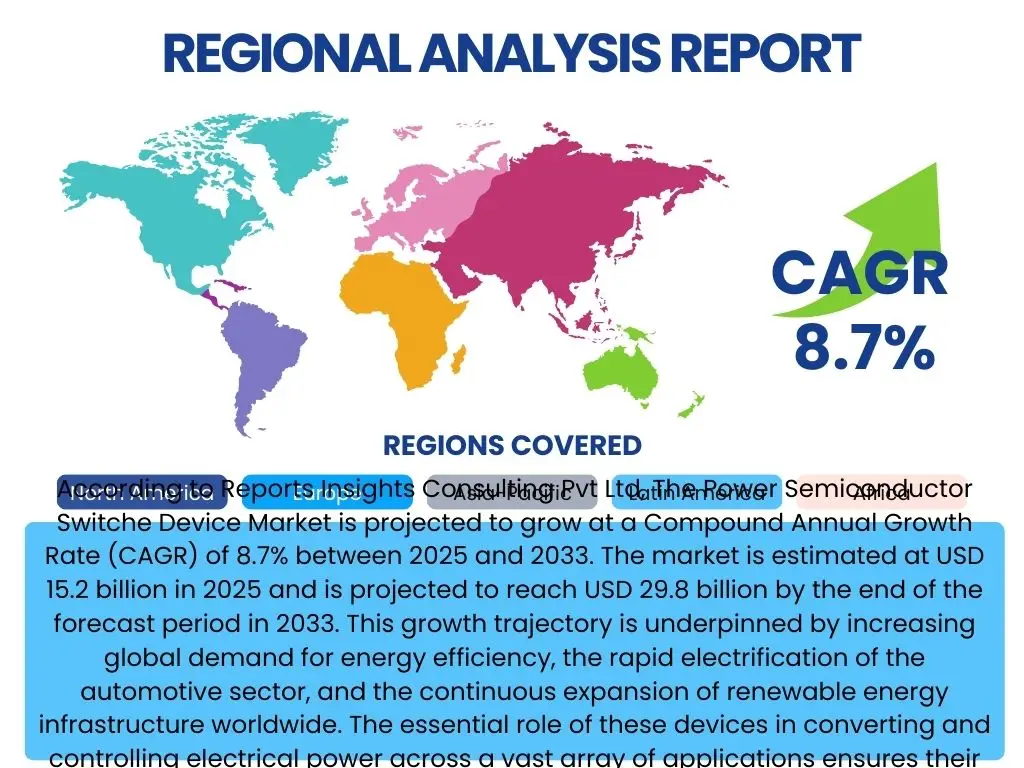

According to Reports Insights Consulting Pvt Ltd, The Power Semiconductor Switche Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. The market is estimated at USD 15.2 billion in 2025 and is projected to reach USD 29.8 billion by the end of the forecast period in 2033. This growth trajectory is underpinned by increasing global demand for energy efficiency, the rapid electrification of the automotive sector, and the continuous expansion of renewable energy infrastructure worldwide. The essential role of these devices in converting and controlling electrical power across a vast array of applications ensures their sustained market expansion.

The market's valuation reflects significant investments in advanced material research and development, particularly for Wide Bandgap (WBG) semiconductors like Silicon Carbide (SiC) and Gallium Nitride (GaN). These materials offer superior performance characteristics, including higher efficiency, faster switching speeds, and enhanced thermal management capabilities compared to traditional silicon-based devices. Such technological advancements are crucial for meeting the stringent performance requirements of modern power electronics across industrial, automotive, and consumer applications. The forecast period anticipates continued innovation, further solidifying the market's upward trend.

Key Power Semiconductor Switche Device Market Trends & Insights

The Power Semiconductor Switch Device market is experiencing a significant transformation driven by several critical trends. Users frequently inquire about the shift towards more compact, higher-performance, and thermally efficient power solutions, driven by macro trends such as global electrification, sustainable energy initiatives, and the proliferation of connected devices. The integration of Wide Bandgap (WBG) materials, notably Silicon Carbide (SiC) and Gallium Nitride (GaN), is a frequently discussed topic due to their superior performance characteristics over traditional silicon-based devices. These materials enable higher power density, reduced energy losses, and operation at elevated temperatures, which are crucial for next-generation applications.

Furthermore, there is a strong emphasis on smart power management and advanced packaging technologies. As power requirements in various applications become more complex, the demand for integrated solutions that offer enhanced control, diagnostic capabilities, and robust thermal management intensifies. Miniaturization, coupled with improved reliability and efficiency, remains a central theme, as industries strive to reduce the form factor and power consumption of electronic systems. These evolving requirements are pushing manufacturers to innovate across the entire value chain, from material science to circuit design and manufacturing processes.

- Growing adoption of Wide Bandgap (WBG) materials (SiC, GaN) due to superior efficiency and performance.

- Increasing demand for energy-efficient power conversion across all end-use sectors.

- Rapid electrification of vehicles, including Electric Vehicles (EVs) and Hybrid Electric Vehicles (HEVs).

- Expansion of renewable energy generation (solar, wind) and associated grid infrastructure.

- Miniaturization and higher power density requirements in electronic devices and systems.

- Development of advanced packaging technologies for improved thermal management and reliability.

- Integration into IoT devices, smart appliances, and industrial automation systems.

- Emergence of smart power modules with integrated control and protection features.

AI Impact Analysis on Power Semiconductor Switche Device

The integration of Artificial Intelligence (AI) is profoundly impacting the Power Semiconductor Switch Device market, a topic frequently raised by users keen on understanding its transformative potential. AI algorithms are increasingly employed across various stages, from the initial design and simulation of power semiconductor devices to their operational deployment and maintenance. For instance, AI-driven tools can optimize device structures and material compositions for enhanced efficiency and reliability, significantly reducing development cycles and improving product performance. This application of AI addresses complex design challenges that are often intractable with traditional simulation methods, leading to more innovative and high-performing power solutions.

Beyond design, AI plays a crucial role in enhancing the operational efficiency and reliability of systems utilizing power semiconductors. Predictive maintenance in power grids, industrial automation, and electric vehicle power trains is being revolutionized by AI, which analyzes vast datasets to forecast potential failures, optimize performance, and extend the lifespan of components. AI also facilitates real-time monitoring and anomaly detection, enabling quicker responses to operational issues and ensuring system stability. This integration of AI not only leads to more robust and intelligent power management systems but also unlocks new levels of energy optimization and resource efficiency across diverse applications, ultimately driving innovation and competitive advantage within the market.

- AI-driven optimization of power semiconductor device design and material selection.

- Predictive maintenance algorithms enhancing reliability in power systems and industrial applications.

- Improved efficiency and control in smart grid operations through AI-powered energy management.

- Real-time monitoring and anomaly detection for power electronics, preventing failures.

- Automation of testing and quality assurance processes for power semiconductor manufacturing.

- Optimization of energy consumption in data centers and industrial facilities via AI control.

- Enhanced thermal management systems utilizing AI for dynamic temperature regulation.

Key Takeaways Power Semiconductor Switche Device Market Size & Forecast

The Power Semiconductor Switch Device market is poised for robust expansion, reflecting its foundational role in modern electrical and electronic systems. Users frequently inquire about the primary drivers sustaining this growth, the most impactful technological advancements, and the key sectors propelling demand. A critical takeaway is the strong growth trajectory, forecasted at a Compound Annual Growth Rate (CAGR) of 8.7% from 2025 to 2033, which is indicative of the increasing global investment in energy efficiency, renewable energy, and electric mobility. This growth is not merely incremental but represents a fundamental shift towards more efficient and powerful electronic systems across industries.

Another significant insight pertains to the transformative impact of Wide Bandgap (WBG) materials, such as Silicon Carbide (SiC) and Gallium Nitride (GaN). These materials are not just improving existing applications but are also enabling entirely new functionalities and performance benchmarks in power conversion. The automotive sector, particularly with the rapid adoption of Electric Vehicles (EVs), stands out as a paramount driver, demanding high-performance and reliable power switches. Similarly, the expansion of industrial automation and data center infrastructure further solidifies the market's promising outlook, highlighting the broad-based demand for advanced power semiconductor solutions globally.

- The market is set for strong growth, projected to nearly double from 2025 to 2033, driven by energy transition and electrification.

- Wide Bandgap materials (SiC, GaN) are key enablers for higher performance, efficiency, and power density in devices.

- The automotive industry, especially Electric Vehicles (EVs), represents the most significant growth catalyst for power switches.

- Increased adoption of renewable energy sources and smart grid technologies is expanding demand for efficient power management.

- Industrial automation, data centers, and consumer electronics continue to be crucial application areas.

- Continuous innovation in packaging and integration technologies is vital for market competitiveness.

Power Semiconductor Switche Device Market Drivers Analysis

The power semiconductor switch device market is significantly propelled by the global imperative for energy efficiency and the ongoing electrification across various industries. Increased adoption of electric vehicles (EVs) and hybrid electric vehicles (HEVs) represents a substantial driver, demanding high-performance, compact, and reliable power switches for inverters, chargers, and motor control units. The transition from internal combustion engines to electric powertrains fundamentally relies on advanced power semiconductors to manage and convert electrical energy with minimal losses, thereby extending range and improving overall vehicle performance. This sector's growth is exponential, ensuring a sustained demand for innovative power switching solutions.

Furthermore, the expansion of renewable energy infrastructure, including solar and wind power, requires advanced power management solutions for efficient energy conversion and grid integration. Power semiconductors are critical components in inverters for solar panels, wind turbine converters, and battery energy storage systems, ensuring stable and efficient power delivery to the grid. The global push for decarbonization and sustainable energy sources directly translates into heightened demand for these devices. Additionally, the proliferation of industrial automation, smart grids, and data centers, which necessitate robust and efficient power management for continuous operation and reduced energy consumption, collectively creates a robust and sustained demand for sophisticated power semiconductor switches.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Electrification of Automotive Sector (EV/HEV) | +2.5% | Global (APAC, Europe, North America) | Long-term |

| Growth in Renewable Energy Generation & Grid Infrastructure | +2.0% | Global (Europe, APAC, North America) | Medium-to-Long-term |

| Increasing Demand for Energy Efficiency & Power Density | +1.5% | Global | Long-term |

| Expansion of Industrial Automation & Data Centers | +1.2% | North America, Europe, APAC | Medium-term |

Power Semiconductor Switche Device Market Restraints Analysis

Despite the robust growth prospects, the power semiconductor switch device market faces several significant restraints that could impede its expansion. One primary challenge is the high cost associated with the research, development, and manufacturing of advanced Wide Bandgap (WBG) materials like Silicon Carbide (SiC) and Gallium Nitride (GaN). These materials require specialized fabrication processes and facilities, leading to higher production costs compared to conventional silicon-based devices. While offering superior performance, the initial investment and subsequent higher unit cost can act as a barrier to widespread adoption, particularly in cost-sensitive applications and emerging markets.

Another restraint involves the complex design and integration challenges associated with new power semiconductor technologies. Incorporating SiC and GaN devices into existing systems often requires significant redesign of power electronics, including gate drivers, packaging, and thermal management solutions, due to their different electrical characteristics and operating conditions. This complexity can extend development cycles and increase engineering costs, deterring some manufacturers from quickly transitioning to newer technologies. Furthermore, intense competition and price pressure from established silicon-based power devices, which benefit from mature supply chains and economies of scale, continue to pose a restraint, forcing WBG manufacturers to innovate rapidly to justify their higher price points.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Cost of Wide Bandgap (WBG) Materials | -1.8% | Global | Medium-term |

| Complex Design and Integration Challenges for New Technologies | -1.5% | Global | Short-to-Medium-term |

| Intense Price Pressure from Traditional Silicon Devices | -1.0% | Global | Medium-term |

| Supply Chain Vulnerabilities and Geopolitical Tensions | -0.8% | Global (particularly APAC) | Short-to-Medium-term |

Power Semiconductor Switche Device Market Opportunities Analysis

The Power Semiconductor Switch Device market is ripe with opportunities driven by several emerging technological and market trends. The burgeoning demand for Electric Vehicles (EVs) and associated charging infrastructure presents a significant avenue for growth, particularly for high-efficiency Silicon Carbide (SiC) and Gallium Nitride (GaN) power devices. As EV adoption accelerates globally, there is an increasing need for power switches that can handle higher voltages, offer faster switching speeds, and reduce power losses in vehicle powertrains, onboard chargers, and charging stations. This expansion creates a fertile ground for innovation and market penetration for advanced power semiconductor solutions.

Another substantial opportunity lies in the continued investment and expansion of renewable energy systems, including solar, wind, and energy storage solutions. These systems require highly efficient power converters to maximize energy capture and seamless integration into smart grids. The development of advanced industrial automation and robotics also opens new doors, as these applications demand rugged, reliable, and precise power control. Furthermore, the increasing focus on miniaturization and integration in consumer electronics and portable devices creates opportunities for compact, high-performance power management solutions. Strategic collaborations, technological advancements, and expansion into these high-growth sectors will be critical for market players to capitalize on these opportunities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Electric Vehicle (EV) and Charging Infrastructure | +3.0% | Global (APAC, Europe, North America) | Long-term |

| Further Development in Renewable Energy and Smart Grid Technologies | +2.5% | Global | Medium-to-Long-term |

| Growth in Advanced Industrial Automation and Robotics | +1.8% | North America, Europe, APAC | Medium-term |

| Miniaturization and Integration in Consumer Electronics & Portable Devices | +1.0% | APAC, North America | Short-to-Medium-term |

Power Semiconductor Switche Device Market Challenges Impact Analysis

The power semiconductor switch device market faces several intricate challenges that could impede its growth and widespread adoption. One significant hurdle is the ongoing issue of supply chain volatility and the scarcity of critical raw materials, which can lead to production delays and increased costs. Geopolitical tensions and trade policies further exacerbate these vulnerabilities, impacting the global availability and pricing of essential components for semiconductor manufacturing. This instability requires companies to invest heavily in supply chain diversification and resilience, adding complexity and cost to operations.

Another major challenge is the steep learning curve and lack of skilled professionals required to design, manufacture, and integrate advanced power semiconductor technologies, particularly those based on Wide Bandgap (WBG) materials. The specialized knowledge in material science, device physics, and power electronics necessary for these innovations is not widely available, leading to a talent gap. Moreover, the stringent regulatory standards and the need for rigorous testing and certification in critical applications like automotive and aerospace pose substantial technical and financial challenges. Adhering to these evolving standards demands continuous investment in R&D and quality control, potentially slowing market entry for new products and smaller players.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Volatility and Raw Material Scarcity | -1.5% | Global (particularly APAC) | Short-to-Medium-term |

| Technical Complexity and Integration Challenges for New Materials | -1.2% | Global | Medium-term |

| Lack of Skilled Workforce and Expertise for WBG Technologies | -1.0% | Global | Long-term |

| Stringent Regulatory Standards and Certification Processes | -0.7% | North America, Europe | Medium-to-Long-term |

Power Semiconductor Switche Device Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Power Semiconductor Switch Device market, offering detailed insights into its current state, historical performance, and future growth projections. The scope encompasses a thorough examination of market dynamics, including key drivers, restraints, opportunities, and challenges that shape the industry landscape. Special attention is given to the impact of emerging technologies, such as Wide Bandgap materials and Artificial Intelligence, on market evolution. The report segments the market by various parameters, providing a granular view of different product types, materials, applications, voltage ranges, and end-use industries across major global regions.

The study also includes a competitive landscape analysis, profiling leading companies and their strategic initiatives, product offerings, and market share. Its objective is to equip stakeholders with actionable intelligence to make informed business decisions, identify potential investment areas, and understand the strategic positioning within this rapidly evolving market. The updated report scope integrates recent market developments and provides a forward-looking perspective, essential for navigating the complexities of the power semiconductor industry from 2025 to 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.2 billion |

| Market Forecast in 2033 | USD 29.8 billion |

| Growth Rate | 8.7% |

| Number of Pages | 257 |

| Key Trends | |

| Segments Covered | |

| Key Companies Covered | Infineon Technologies AG, ON Semiconductor Corporation, STMicroelectronics N.V., Mitsubishi Electric Corporation, Fuji Electric Co. Ltd., Renesas Electronics Corporation, NXP Semiconductors N.V., Toshiba Corporation, ROHM Co. Ltd., Littelfuse Inc., Vishay Intertechnology Inc., Diodes Incorporated, GaN Systems Inc., Alpha and Omega Semiconductor Limited, WeEn Semiconductors B.V., Wolfspeed Inc. (A Cree Company), Microchip Technology Inc., Semikron Danfoss Group, IXYS Corporation (A Littelfuse Company), SanKen Electric Co. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Power Semiconductor Switch Device market is meticulously segmented to provide a comprehensive understanding of its diverse components and evolving dynamics. This segmentation allows for a granular analysis of market trends, competitive landscapes, and growth opportunities across various technological parameters and application areas. Understanding these distinct segments is crucial for stakeholders to tailor strategies, optimize product development, and identify high-potential market niches. The market is primarily categorized by device type, material, application, and voltage range, each revealing unique growth drivers and technological advancements that shape the overall industry.

Each segment reflects specific performance requirements and market demands. For instance, the material segment highlights the shift from traditional silicon to advanced Wide Bandgap materials, indicative of the industry's pursuit of higher efficiency and performance. Similarly, the application segments underscore the critical role power semiconductors play in rapidly growing sectors like electric vehicles and renewable energy, illustrating the broad impact of these devices across modern technological infrastructure. This detailed segmentation analysis is essential for identifying strategic investment areas and understanding the complex interplay of factors driving market expansion.

- By Device Type: MOSFET, IGBT, Thyristor, Diode, Others

- By Material: Silicon (Si), Silicon Carbide (SiC), Gallium Nitride (GaN), Others

- By Application: Automotive (EV/HEV, Charging Infrastructure), Industrial (Motor Drives, Power Supplies, Robotics), Energy & Utility (Solar Inverters, Wind Converters, Smart Grid), Consumer Electronics (Adapters, Home Appliances), IT & Telecom (Data Centers, Base Stations), Aerospace & Defense, Medical, Others

- By Voltage Range: Low Voltage (0-100V), Medium Voltage (100V-1000V), High Voltage (>1000V)

Regional Highlights

- Asia Pacific (APAC): Dominates the market due to robust manufacturing activities, high adoption of consumer electronics, significant investments in EV production, and rapid expansion of renewable energy infrastructure, especially in China, Japan, South Korea, and India.

- North America: A major growth region driven by technological advancements, strong automotive industry, increasing adoption of industrial automation, and substantial R&D investments in WBG materials and smart grid solutions, particularly in the United States and Canada.

- Europe: Exhibits strong growth owing to stringent energy efficiency regulations, significant government support for renewable energy projects, leading EV manufacturing hubs, and advanced industrial sectors in countries like Germany, France, and the UK.

- Latin America: Expected to show moderate growth, supported by growing industrialization, increasing investments in renewable energy, and expanding automotive manufacturing, particularly in Brazil and Mexico.

- Middle East and Africa (MEA): Emerging market with potential growth fueled by infrastructure development projects, increasing energy demands, and diversification efforts into non-oil sectors, leading to investments in power generation and industrial applications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Power Semiconductor Switche Device Market.- Infineon Technologies AG

- ON Semiconductor Corporation

- STMicroelectronics N.V.

- Mitsubishi Electric Corporation

- Fuji Electric Co. Ltd.

- Renesas Electronics Corporation

- NXP Semiconductors N.V.

- Toshiba Corporation

- ROHM Co. Ltd.

- Littelfuse Inc.

- Vishay Intertechnology Inc.

- Diodes Incorporated

- GaN Systems Inc.

- Alpha and Omega Semiconductor Limited

- WeEn Semiconductors B.V.

- Wolfspeed Inc. (A Cree Company)

- Microchip Technology Inc.

- Semikron Danfoss Group

- IXYS Corporation (A Littelfuse Company)

- SanKen Electric Co. Ltd.

Frequently Asked Questions

What are Power Semiconductor Switch Devices?

Power semiconductor switch devices are electronic components designed to control and convert electrical power efficiently. They function by rapidly switching between ON and OFF states, enabling precise regulation of voltage and current in various applications, from power supplies to motor drives and renewable energy systems.

What is driving the growth of the Power Semiconductor Switch Device market?

The market's growth is primarily driven by the rapid electrification of the automotive industry (EVs/HEVs), the global expansion of renewable energy generation and smart grids, increasing demand for energy-efficient power conversion, and the proliferation of industrial automation and consumer electronics.

What role do Wide Bandgap (WBG) materials play in this market?

Wide Bandgap (WBG) materials like Silicon Carbide (SiC) and Gallium Nitride (GaN) are crucial for market advancement. They offer superior performance characteristics, including higher efficiency, faster switching speeds, and better thermal management, enabling more compact, powerful, and reliable power devices compared to traditional silicon.

How is AI impacting Power Semiconductor Switch Devices?

AI is transforming the market by optimizing device design, enabling predictive maintenance in power systems, enhancing control and efficiency in smart grid applications, and facilitating real-time monitoring and anomaly detection. This leads to more intelligent, reliable, and efficient power management solutions.

What are the key applications for Power Semiconductor Switch Devices?

Key applications include electric vehicles (EVs and charging infrastructure), industrial motor drives and robotics, solar inverters and wind power converters, power supplies for IT & telecom (data centers), and a wide range of consumer electronic devices and home appliances.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted