Power Management IC Market

Power Management IC Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701552 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

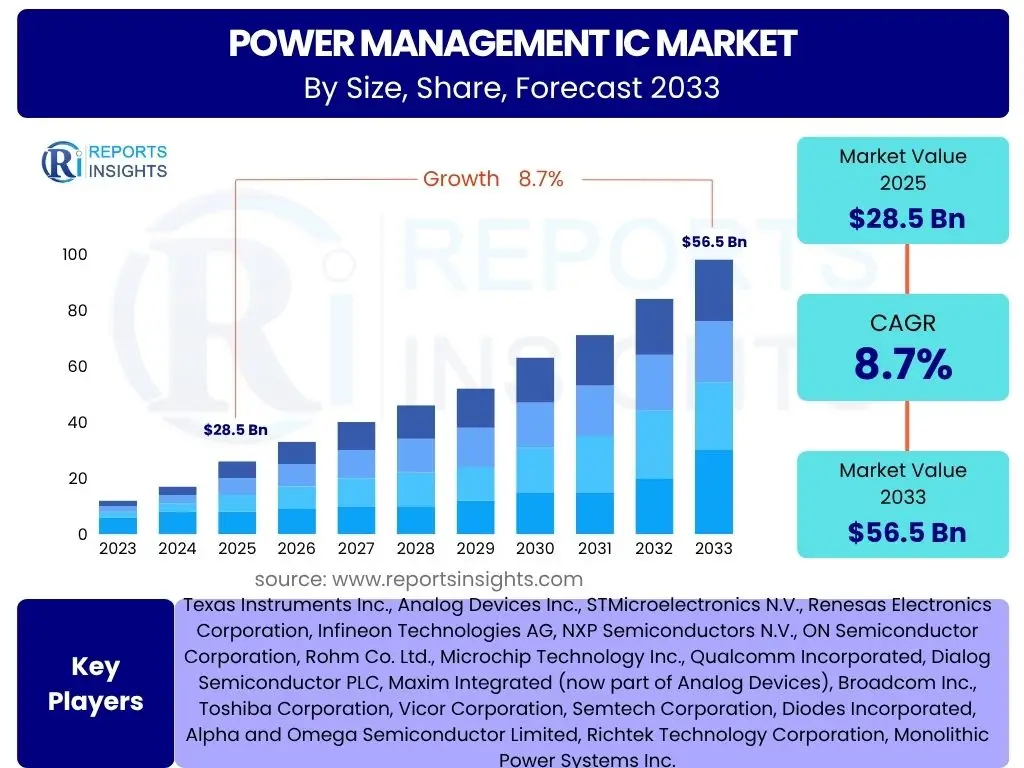

Power Management IC Market Size

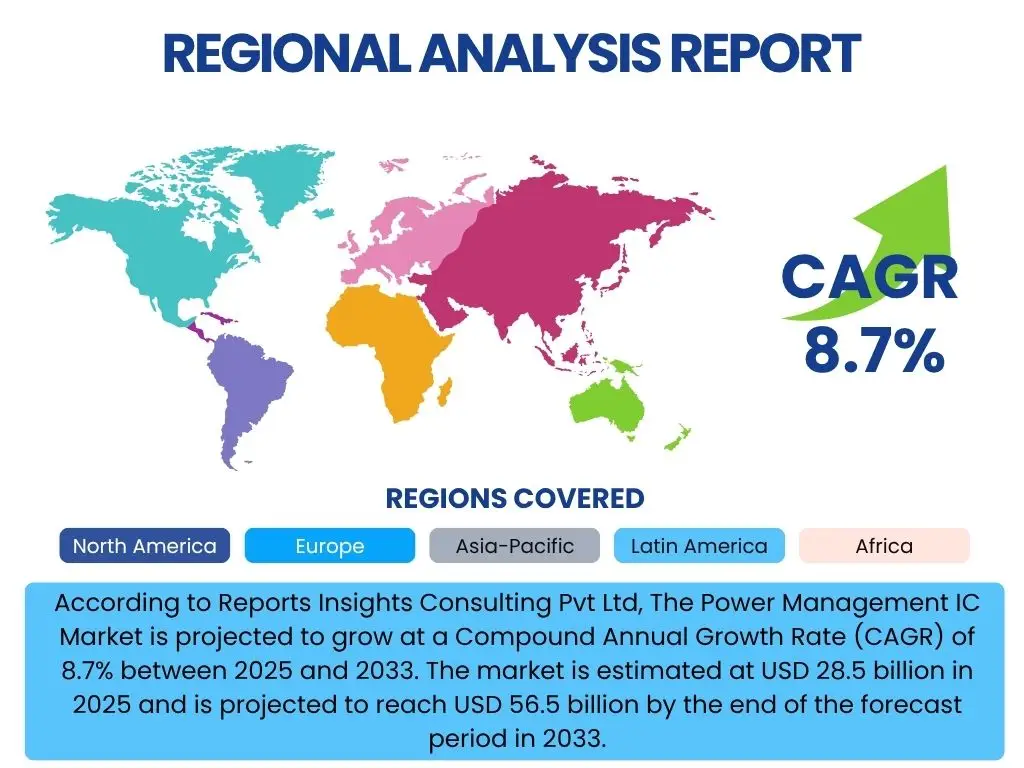

According to Reports Insights Consulting Pvt Ltd, The Power Management IC Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. The market is estimated at USD 28.5 billion in 2025 and is projected to reach USD 56.5 billion by the end of the forecast period in 2033.

Key Power Management IC Market Trends & Insights

The Power Management IC (PMIC) market is undergoing significant transformation driven by the increasing demand for energy-efficient and compact electronic devices across various sectors. Key trends indicate a robust evolution, with a strong emphasis on integration, miniaturization, and enhanced power density. Consumers and industries alike are seeking solutions that not only extend battery life but also reduce the overall size and thermal footprint of their electronic systems. This necessitates innovative PMIC designs that can handle complex power requirements efficiently.

Another prominent trend is the widespread adoption of Wide Band Gap (WBG) materials like Gallium Nitride (GaN) and Silicon Carbide (SiC) in power electronics. These materials offer superior performance characteristics, including higher switching frequencies, lower power losses, and improved thermal conductivity compared to traditional silicon-based components. This shift is particularly impactful in high-power applications such as electric vehicles, data centers, and renewable energy systems, where efficiency gains translate into substantial operational benefits and reduced environmental impact. The integration of advanced features such as intelligent power management and digital control within PMICs is also becoming standard, enabling greater flexibility and optimization.

Furthermore, the convergence of multiple functionalities into single-chip solutions, often referred to as System-on-Chip (SoC) PMICs, is gaining momentum. This integration reduces Bill of Material (BOM) costs, simplifies design processes, and enhances reliability. The expansion of IoT devices, 5G infrastructure, and advanced automotive electronics necessitates such highly integrated and efficient power solutions. This trend reflects a broader industry movement towards more sophisticated and adaptable power management systems capable of meeting the diverse and evolving needs of modern electronic ecosystems.

- Miniaturization and higher power density in PMIC designs.

- Increased adoption of Wide Band Gap (WBG) materials (GaN, SiC) for enhanced efficiency.

- Integration of multiple functionalities into single-chip PMICs (SoC PMICs).

- Rising demand for intelligent and digitally controlled power management solutions.

- Growing application in electric vehicles, 5G infrastructure, and IoT devices.

- Emphasis on energy efficiency and thermal management across all end-use sectors.

AI Impact Analysis on Power Management IC

The advent and proliferation of Artificial Intelligence (AI) are profoundly influencing the Power Management IC (PMIC) market, primarily by creating a heightened demand for highly efficient and adaptive power solutions. AI-enabled devices, ranging from edge AI processors in consumer electronics to high-performance computing (HPC) systems in data centers, consume significant power. Users are increasingly concerned with how AI processing affects battery life, thermal management, and overall device performance. This drives the need for PMICs that can dynamically adjust power delivery to optimize energy consumption during varying AI workloads, ensuring both performance and extended operational time.

Beyond simply powering AI, AI itself is beginning to be leveraged within PMIC design and operation. Machine learning algorithms are being employed to predict power demands, optimize power distribution, and even detect potential power anomalies in real-time. This allows for more sophisticated power sequencing, voltage regulation, and fault detection than traditional analog or fixed-logic PMICs. Consumers and industry professionals anticipate PMICs that can intelligently adapt to different operational scenarios, learning from usage patterns to provide unprecedented levels of power efficiency and reliability, which is crucial for the continuous operation of complex AI systems.

Moreover, the integration of AI functionalities into devices necessitates advancements in power integrity and noise reduction, as AI chips are highly sensitive to power fluctuations. PMICs are evolving to incorporate more precise voltage regulators, advanced filtering techniques, and rapid transient response capabilities. The future of PMICs will likely involve on-chip AI elements for autonomous power management, enabling devices to manage their own power profiles with minimal external intervention. This convergence promises not only to optimize energy use for AI applications but also to streamline the design and deployment of next-generation intelligent electronics.

- Increased demand for efficient PMICs to power AI-enabled devices (edge AI, HPC).

- Dynamic power delivery optimization for varying AI workloads.

- Utilization of AI/ML algorithms in PMIC design for predictive power management.

- Enhanced power integrity and noise reduction for sensitive AI chips.

- Development of autonomous, AI-driven on-chip power management systems.

- Facilitation of longer battery life and improved thermal management in AI devices.

Key Takeaways Power Management IC Market Size & Forecast

The Power Management IC (PMIC) market is positioned for substantial growth, driven by an escalating global demand for energy-efficient electronic devices across diverse sectors. The forecast period indicates a robust CAGR, reflecting the critical role PMICs play in optimizing power consumption, extending battery life, and enabling advanced functionalities in modern electronics. This growth is significantly influenced by macro trends such as the electrification of the automotive industry, the expansion of IoT ecosystems, and the continuous advancements in consumer electronics, all of which necessitate sophisticated power management solutions.

A significant insight is the foundational impact of technological innovation, particularly the adoption of Wide Band Gap (WBG) materials like GaN and SiC. These materials are revolutionizing power efficiency and density, paving the way for smaller, more powerful, and less heat-intensive devices. Furthermore, the increasing complexity of electronic systems and the imperative for sustainable energy consumption are accelerating the integration of intelligent and adaptive PMICs. The market's future trajectory is strongly tied to ongoing R&D in materials science, chip design, and smart power algorithms.

Overall, the market size projection underscores a robust industry poised for consistent expansion. Key stakeholders, including manufacturers, designers, and end-users, are increasingly prioritizing power efficiency and reliability. The projected market value by 2033 highlights the long-term confidence in PMICs as indispensable components for driving innovation across consumer, industrial, automotive, and telecommunications sectors. This sustained growth is a testament to the essential nature of power management in an increasingly electrified and intelligent world.

- Robust market growth projected with a significant CAGR through 2033.

- Market expansion driven by increasing demand for energy-efficient electronics across all sectors.

- Technological advancements, including WBG materials (GaN, SiC), are crucial growth enablers.

- Integration, miniaturization, and intelligent power management are core to future PMIC development.

- Automotive electrification, IoT, and consumer electronics are primary growth accelerators.

- Long-term market confidence driven by essential role of PMICs in modern technological ecosystems.

Power Management IC Market Drivers Analysis

The global surge in demand for energy-efficient electronic devices is a primary driver for the Power Management IC (PMIC) market. As electronic devices become more sophisticated and ubiquitous, there is an inherent need to optimize power consumption to extend battery life, reduce heat generation, and minimize overall energy footprints. This driver is prevalent across various industries, from portable consumer electronics to large-scale data centers, where even marginal gains in power efficiency can lead to significant operational savings and environmental benefits. Manufacturers are continuously innovating to develop PMICs that can deliver higher power density with lower losses, directly addressing this pervasive market need.

The rapid expansion of the automotive sector, particularly the accelerating transition towards electric vehicles (EVs), hybrid electric vehicles (HEVs), and advanced driver-assistance systems (ADAS), is profoundly influencing the PMIC market. EVs and HEVs require highly efficient and reliable power management solutions for their battery systems, inverters, and onboard charging units. ADAS and infotainment systems also demand precise power delivery to ensure safe and robust operation. This automotive electrification trend necessitates robust, high-performance PMICs capable of operating under demanding conditions, driving significant investment and innovation in the sector and boosting market growth globally.

Furthermore, the widespread adoption of 5G technology and the Internet of Things (IoT) devices are significant catalysts for the PMIC market. 5G infrastructure, including base stations and end-user devices, requires sophisticated power management to handle high data rates and maintain energy efficiency. IoT devices, characterized by their small size and need for prolonged battery life, depend heavily on highly integrated and ultra-low-power PMICs. The proliferation of these connected devices across smart homes, industrial automation, and healthcare creates a vast and growing market for specialized power management solutions, emphasizing efficiency and miniaturization.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Energy-Efficient Devices | +2.1% | Global (APAC, North America, Europe) | 2025-2033 (Long-term) |

| Rapid Adoption of Electric Vehicles (EVs) & HEVs | +1.8% | China, Europe, North America, Japan | 2025-2033 (Mid to Long-term) |

| Expansion of 5G Infrastructure and IoT Devices | +1.5% | APAC, North America, Europe | 2025-2030 (Mid-term) |

| Increasing Demand for Consumer Electronics | +1.2% | APAC (China, India), North America, Europe | 2025-2033 (Long-term) |

| Advancements in Data Centers and Cloud Computing | +0.9% | North America, Europe, China | 2025-2033 (Long-term) |

| Growth in Renewable Energy Systems | +0.7% | Europe, North America, China, India | 2028-2033 (Long-term) |

Power Management IC Market Restraints Analysis

One significant restraint impacting the Power Management IC (PMIC) market is the escalating complexity of design and integration. As electronic devices become more compact and multifunctional, the task of designing PMICs that can efficiently manage power across numerous components with diverse voltage requirements becomes increasingly challenging. This complexity extends to thermal management, electromagnetic interference (EMI) mitigation, and ensuring power integrity across the system. The intricate design cycles often lead to extended development timelines and higher R&D costs, which can slow down product innovation and market entry, particularly for smaller manufacturers or startups.

Another major challenge confronting the PMIC market is the volatility and disruptions within the global supply chain for semiconductor components. PMICs rely on a complex ecosystem of raw materials, manufacturing processes, and specialized fabs. Geopolitical tensions, natural disasters, and unforeseen events, such as the recent global chip shortages, can severely impact the availability of materials and manufacturing capacity. This leads to increased lead times, higher production costs, and reduced predictability in component supply, forcing manufacturers to grapple with inventory management and production delays. Such instabilities can deter investments and limit market expansion, making it difficult to meet rising demand consistently.

Furthermore, intense price competition and continuous margin pressure are significant restraints in the mature segments of the PMIC market. While innovative and specialized PMICs for emerging applications command higher prices, basic and commodity PMICs face fierce competition, particularly from manufacturers in cost-sensitive regions. This competitive landscape often leads to aggressive pricing strategies, which can erode profit margins for companies operating in these segments. Maintaining profitability while investing in the extensive R&D required for next-generation PMICs becomes a delicate balancing act, potentially limiting the resources available for diversification and advanced technological development.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Design Complexity and Integration Challenges | -1.5% | Global (High-tech Manufacturing Regions) | 2025-2033 (Long-term) |

| Global Supply Chain Disruptions and Material Shortages | -1.2% | Global (Interconnected Markets) | 2025-2028 (Mid-term) |

| Intense Price Competition and Margin Pressure | -0.9% | APAC, Europe (High-volume Segments) | 2025-2033 (Long-term) |

| High R&D Investment and Long Product Cycles | -0.7% | Global | 2025-2033 (Long-term) |

| Regulatory Hurdles and Compliance Standards | -0.5% | Europe, North America (Automotive, Medical) | 2025-2033 (Long-term) |

| Thermal Management Challenges in Miniaturized Devices | -0.4% | Global | 2025-2033 (Long-term) |

Power Management IC Market Opportunities Analysis

The burgeoning adoption of Wide Band Gap (WBG) semiconductors, particularly Gallium Nitride (GaN) and Silicon Carbide (SiC), presents a significant growth opportunity for the Power Management IC (PMIC) market. These next-generation materials offer superior performance characteristics, including higher breakdown voltage, faster switching speeds, and lower on-resistance compared to traditional silicon. This translates into more efficient, compact, and lighter power solutions, which are crucial for high-power applications such as electric vehicles, fast chargers, and data center power supplies. PMIC manufacturers can capitalize on this by developing specialized GaN- and SiC-based power controllers and drivers that unlock the full potential of these materials, leading to highly optimized power systems and opening new market segments.

The increasing focus on energy harvesting and low-power applications also offers a substantial opportunity for PMIC innovation. As the Internet of Things (IoT) expands into diverse environments, there is a growing need for devices that can operate with minimal or no external power sources, relying instead on ambient energy (e.g., solar, thermal, kinetic, RF). This drives demand for ultra-low-power PMICs and energy harvesting circuits that can efficiently convert and manage minute amounts of harvested energy. Developing highly integrated PMICs with advanced energy harvesting capabilities will enable the proliferation of truly autonomous IoT devices, medical implants, and wearable electronics, creating a specialized, high-growth niche within the market.

Furthermore, the rising complexity of electronic systems and the imperative for real-time power optimization are fostering opportunities for PMICs with integrated Artificial Intelligence (AI) and Machine Learning (ML) capabilities. Future PMICs are expected to dynamically analyze power consumption patterns, predict future needs, and autonomously adjust voltage and current to maximize efficiency and performance. This intelligence can lead to adaptive power solutions that self-optimize for varying workloads and environmental conditions. Investing in research and development for AI-enabled PMICs, particularly those with embedded ML algorithms for predictive power management, represents a strategic opportunity to capture market share in high-value, performance-critical applications like advanced computing, automotive AI, and smart industrial systems.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Adoption of GaN and SiC in Power Electronics | +1.9% | Global (Automotive, Data Centers, Consumer) | 2026-2033 (Mid to Long-term) |

| Growth in Energy Harvesting and Ultra-Low Power Applications | +1.5% | Global (IoT, Wearables, Medical) | 2027-2033 (Long-term) |

| Integration of AI/ML for Intelligent Power Management | +1.3% | North America, Europe, APAC (High-performance Computing) | 2028-2033 (Long-term) |

| Emergence of Industrial Automation and Robotics | +1.0% | Europe, North America, APAC (Germany, Japan, China) | 2025-2033 (Long-term) |

| Demand for Custom and Application-Specific PMICs | +0.8% | Global | 2025-2033 (Long-term) |

| Expansion in Medical and Healthcare Electronics | +0.6% | North America, Europe, Japan | 2025-2033 (Long-term) |

Power Management IC Market Challenges Impact Analysis

One of the persistent challenges in the Power Management IC (PMIC) market is the ongoing demand for miniaturization while simultaneously increasing power density. As consumer electronics, wearables, and IoT devices become smaller and more feature-rich, PMICs must shrink in size without compromising on power efficiency, thermal performance, or functionality. This requires advanced packaging technologies, innovative circuit designs, and often, the integration of multiple power management functions into a single chip. Achieving this balance is technically complex and can lead to significant R&D expenditures, potentially slowing down product development cycles and increasing manufacturing costs, particularly when dealing with heat dissipation in confined spaces.

Ensuring power integrity and managing electromagnetic interference (EMI) are critical technical challenges, especially with the proliferation of high-frequency and high-speed electronic systems. Modern processors, 5G modems, and sophisticated sensors demand extremely clean and stable power supplies with minimal noise, even during rapid load changes. At the same time, the high switching frequencies used in many PMICs can generate significant EMI, which can disrupt the operation of sensitive components within a device. Designing PMICs that effectively mitigate noise and ensure stable power delivery across a wide range of operating conditions, while also meeting stringent EMI compliance standards, adds considerable complexity and cost to the design and testing phases.

The rapid pace of technological evolution and the associated risk of technological obsolescence pose a significant challenge for PMIC manufacturers. With new materials (like GaN and SiC), advanced manufacturing processes, and evolving application requirements constantly emerging, PMIC designs can quickly become outdated. Companies must continuously invest in research and development to stay at the forefront of innovation, ensuring their products meet the next generation of performance and efficiency benchmarks. Failure to adapt swiftly can lead to a loss of market share and declining profitability. This perpetual need for innovation requires substantial capital investment and a highly skilled workforce, putting pressure on companies to manage their R&D portfolios effectively.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization with High Power Density & Thermal Management | -1.3% | Global (Consumer Electronics, IoT) | 2025-2033 (Long-term) |

| Ensuring Power Integrity and Mitigating EMI | -1.0% | Global (High-speed Digital Systems) | 2025-2033 (Long-term) |

| Rapid Technological Evolution and Obsolescence | -0.8% | Global | 2025-2030 (Mid-term) |

| Cybersecurity Risks for Connected PMICs | -0.6% | Global (IoT, Automotive) | 2026-2033 (Long-term) |

| Intellectual Property (IP) Infringement and Litigation | -0.4% | Global | 2025-2033 (Long-term) |

| Talent Shortage in Skilled Semiconductor Engineering | -0.3% | North America, Europe, APAC | 2025-2033 (Long-term) |

Power Management IC Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Power Management IC (PMIC) market, covering historical data, current market dynamics, and future projections. It offers a detailed examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The report is designed to provide stakeholders with actionable insights into industry trends, competitive landscapes, and strategic recommendations to navigate the evolving market and capitalize on emerging opportunities within the power management semiconductor sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 28.5 billion |

| Market Forecast in 2033 | USD 56.5 billion |

| Growth Rate | 8.7% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Texas Instruments Inc., Analog Devices Inc., STMicroelectronics N.V., Renesas Electronics Corporation, Infineon Technologies AG, NXP Semiconductors N.V., ON Semiconductor Corporation, Rohm Co. Ltd., Microchip Technology Inc., Qualcomm Incorporated, Dialog Semiconductor PLC, Maxim Integrated (now part of Analog Devices), Broadcom Inc., Toshiba Corporation, Vicor Corporation, Semtech Corporation, Diodes Incorporated, Alpha and Omega Semiconductor Limited, Richtek Technology Corporation, Monolithic Power Systems Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Power Management IC (PMIC) market is segmented to provide a granular understanding of its diverse components and their respective contributions to overall market dynamics. This segmentation facilitates a comprehensive analysis of market performance across different product types, applications, and end-use industries, highlighting specific growth areas and technological preferences. Each segment is influenced by unique drivers and faces distinct challenges, reflecting the varied requirements of modern electronic systems.

The segmentation by product type is crucial as it differentiates between the core functionalities of PMICs, such as voltage regulation, battery management, and motor driving. Each product category serves distinct purposes within an electronic system, with innovations in one area often impacting others. For instance, advancements in battery management ICs are critical for the portable electronics and electric vehicle sectors, while sophisticated voltage regulators are indispensable for high-performance computing and telecommunications infrastructure. Understanding these specific product markets helps identify areas of high growth and technological advancement.

Application-based segmentation provides insights into the primary industries leveraging PMICs, including consumer electronics, automotive, industrial, and telecommunications. This breakdown reveals which sectors are driving demand and where future growth opportunities lie. For example, the automotive segment is witnessing a significant surge due to electrification and ADAS, whereas the consumer electronics segment continues to demand miniaturized and highly efficient solutions for smartphones and wearables. Analyzing these applications enables a targeted approach to market strategy and product development, aligning with specific industry needs and technological roadmaps.

- By Product Type:

- Voltage Regulators: Essential for stable power supply to various components.

- Integrated ASSP Power Management ICs: Application-specific standard products for optimized power management in complex systems.

- Battery Management ICs: Critical for charging, discharging, and monitoring battery health in portable and automotive applications.

- Motor Driver ICs: Used in a wide range of applications from industrial automation to consumer devices.

- Gate Driver ICs: Drive power MOSFETs and IGBTs in high-power switching applications.

- Others: Includes specialized PMICs like energy harvesting ICs, power factor correction (PFC) controllers, etc.

- By Application:

- Consumer Electronics: Smartphones, laptops, tablets, wearables, smart home devices.

- Automotive: EVs/HEVs, ADAS, infotainment systems, body electronics.

- Industrial: Automation, robotics, power tools, industrial IoT.

- Telecommunications: 5G infrastructure, network equipment, base stations.

- Healthcare: Medical devices, patient monitoring, portable diagnostic equipment.

- Energy & Power: Renewable energy systems, smart grids, power conversion.

- Others: Aerospace & Defense, data centers, enterprise computing.

Regional Highlights

- Asia Pacific (APAC): Dominates the Power Management IC market due to its robust manufacturing ecosystem for consumer electronics, automotive components, and telecommunications equipment. Countries like China, South Korea, Japan, and Taiwan are major hubs for semiconductor production and electronic device assembly. The rapid adoption of 5G, the expansion of IoT, and the accelerating growth of electric vehicle production further fuel demand in this region. Government initiatives supporting semiconductor manufacturing and digital infrastructure also contribute significantly to market expansion.

- North America: Represents a significant market share, driven by strong demand from data centers, high-performance computing (HPC), advanced automotive technologies (including ADAS and EVs), and aerospace and defense sectors. The presence of leading technology companies and extensive research and development activities contributes to the adoption of sophisticated and high-value PMICs. Focus on energy efficiency and technological innovation remains a key driver in this region.

- Europe: Exhibits steady growth, primarily fueled by its strong automotive industry (especially in Germany and France), industrial automation, and renewable energy initiatives. The region is a pioneer in developing smart factory solutions and advanced power grid infrastructure, which necessitates highly efficient and reliable PMICs. Strict energy efficiency regulations also promote the adoption of advanced power management solutions across various applications.

- Latin America: An emerging market for PMICs, driven by increasing industrialization, growing consumer electronics penetration, and investments in telecommunications infrastructure. While smaller than other regions, it offers considerable potential as economic development and technological adoption continue to advance across countries like Brazil and Mexico.

- Middle East and Africa (MEA): Shows promising growth, albeit from a smaller base, primarily due to investments in smart city projects, renewable energy, and telecommunications network expansion. The region's growing population and increasing disposable income also contribute to rising demand for consumer electronics, indirectly boosting the PMIC market.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Power Management IC Market.- Texas Instruments Inc.

- Analog Devices Inc.

- STMicroelectronics N.V.

- Renesas Electronics Corporation

- Infineon Technologies AG

- NXP Semiconductors N.V.

- ON Semiconductor Corporation

- Rohm Co. Ltd.

- Microchip Technology Inc.

- Qualcomm Incorporated

- Dialog Semiconductor PLC

- Broadcom Inc.

- Toshiba Corporation

- Vicor Corporation

- Semtech Corporation

- Diodes Incorporated

- Alpha and Omega Semiconductor Limited

- Richtek Technology Corporation

- Monolithic Power Systems Inc.

- Cypress Semiconductor (now part of Infineon)

Frequently Asked Questions

What is the projected growth rate of the Power Management IC market?

The Power Management IC (PMIC) market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033, reaching an estimated USD 56.5 billion by 2033.

What key trends are driving the Power Management IC market?

Key trends include miniaturization, increased power density, the adoption of Wide Band Gap (WBG) materials like GaN and SiC, integration of multiple functionalities into single-chip solutions, and the rising demand for intelligent power management in devices like electric vehicles, 5G infrastructure, and IoT.

How is AI impacting the Power Management IC market?

AI is significantly impacting the market by increasing demand for highly efficient PMICs to power AI-enabled devices. Additionally, AI and Machine Learning are being integrated into PMIC designs for dynamic power optimization, predictive management, and enhanced power integrity.

Which applications are the primary drivers for the Power Management IC market?

The primary applications driving the PMIC market include consumer electronics (smartphones, wearables), automotive (EVs, ADAS), industrial automation, telecommunications (5G), and data centers, all requiring sophisticated and efficient power solutions.

What are the main challenges facing the Power Management IC industry?

Major challenges include the complex technical demands of miniaturization with high power density, ensuring power integrity and mitigating electromagnetic interference (EMI), the rapid pace of technological obsolescence, and managing global supply chain disruptions for semiconductor components.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted