Polyurethane Market

Polyurethane Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708113 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

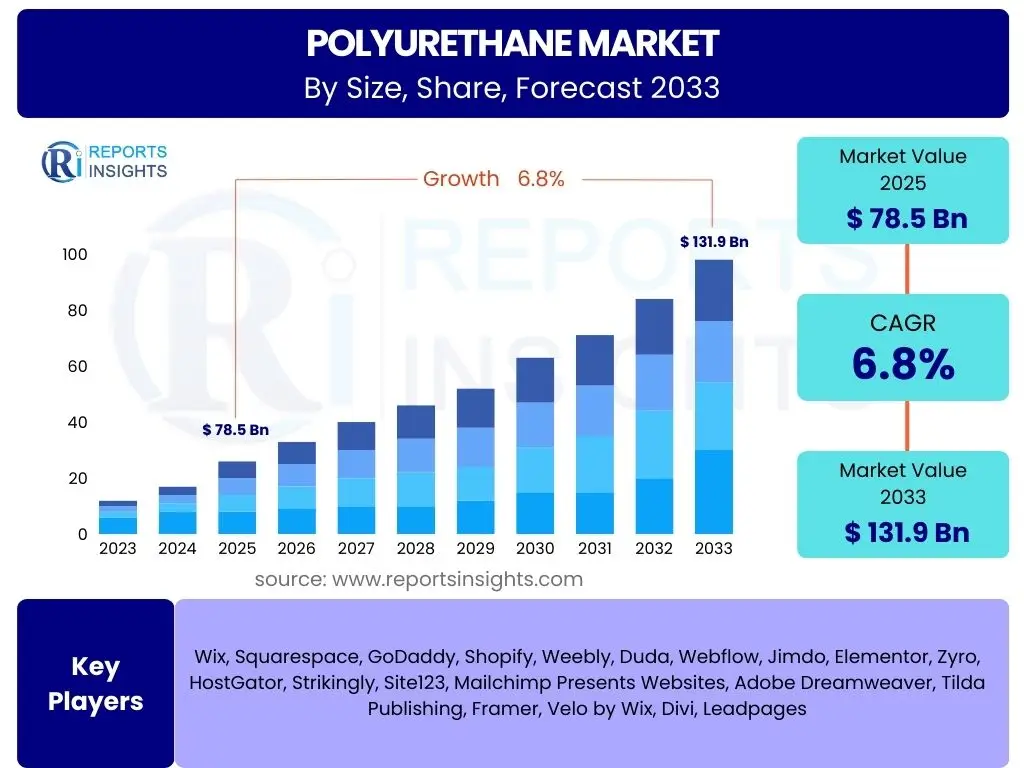

Polyurethane Market Size

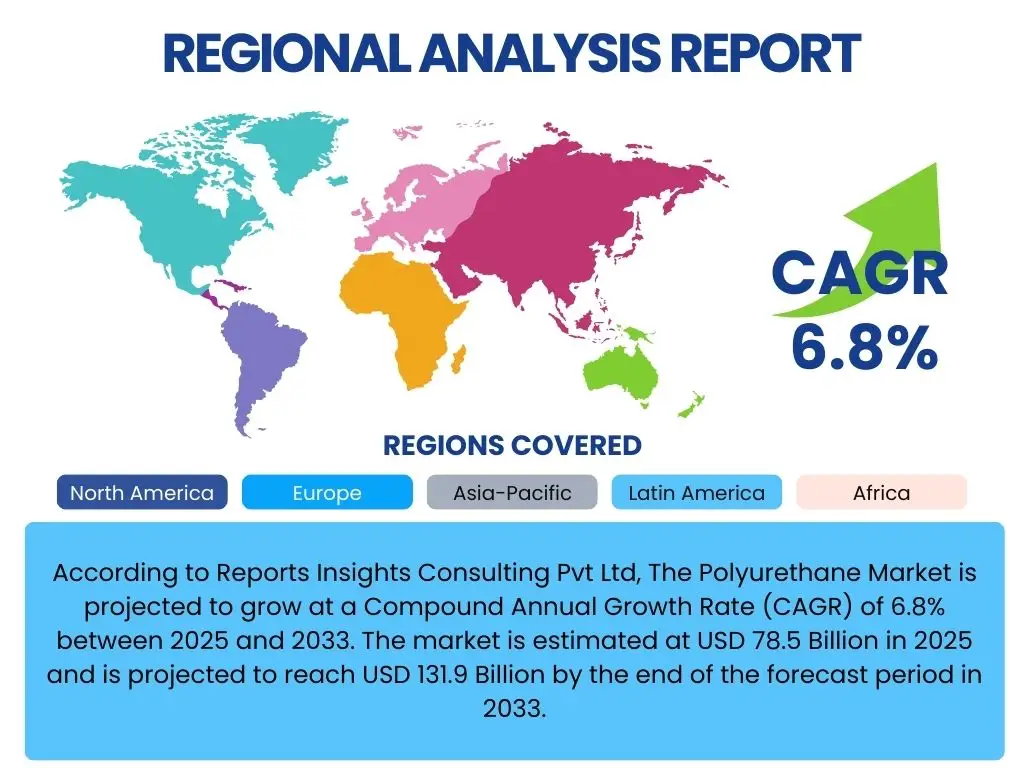

According to Reports Insights Consulting Pvt Ltd, The Polyurethane Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 78.5 Billion in 2025 and is projected to reach USD 131.9 Billion by the end of the forecast period in 2033.

Key Polyurethane Market Trends & Insights

The polyurethane market is currently undergoing significant transformation, driven by a confluence of technological advancements, evolving consumer demands, and increasing regulatory scrutiny. A major trend observed is the growing emphasis on sustainability, pushing manufacturers towards the development of bio-based and recycled polyurethane solutions. This shift is not only a response to environmental concerns but also a strategic move to secure raw material supply chains and appeal to environmentally conscious consumers and industries.

Another pivotal insight is the accelerated demand for high-performance polyurethanes across various end-use industries. In automotive, the focus on lightweighting and enhanced fuel efficiency is driving the adoption of advanced polyurethane composites. Similarly, the construction sector is increasingly utilizing rigid polyurethane foams for superior insulation properties, contributing to energy efficiency in buildings. The market is also witnessing innovation in specialized applications such as medical devices, footwear, and electronics, where polyurethanes offer unique combinations of flexibility, durability, and biocompatibility.

Furthermore, digitalization and automation in manufacturing processes are becoming more prevalent, improving production efficiency, consistency, and traceability. The integration of smart technologies in polyurethane production allows for better process control, reduced waste, and the ability to tailor material properties more precisely to specific application requirements. This trend ensures the market remains competitive and responsive to the intricate needs of its diverse clientele.

- Growing adoption of bio-based and recycled polyurethanes due to sustainability initiatives.

- Increasing demand for lightweight and high-performance polyurethane solutions in automotive and aerospace.

- Technological advancements in rigid polyurethane foams for enhanced thermal insulation in construction.

- Expansion of polyurethane applications in specialized fields like medical devices and smart textiles.

- Integration of digitalization and automation in manufacturing processes for improved efficiency and quality.

- Shift towards solvent-free and low-VOC polyurethane coatings and adhesives for environmental compliance.

- Development of durable and weather-resistant polyurethanes for infrastructure and marine applications.

AI Impact Analysis on Polyurethane

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is beginning to revolutionize various facets of the polyurethane industry, from raw material sourcing and process optimization to product development and quality control. Users frequently inquire about how AI can enhance efficiency, reduce costs, and accelerate innovation within this complex chemical sector. The primary focus is on leveraging AI for predictive analytics to anticipate market demands, manage supply chain fluctuations more effectively, and optimize manufacturing parameters to achieve desired material properties with greater precision.

AI's influence extends significantly to research and development, where algorithms can rapidly analyze vast datasets of chemical compositions and material performance characteristics. This capability enables quicker identification of novel polyurethane formulations with improved properties, such as enhanced durability, flexibility, or flame retardancy, thereby shortening development cycles and reducing experimental costs. Furthermore, AI-powered simulations allow for virtual prototyping and testing, predicting how new materials will behave under various conditions before physical synthesis, leading to more efficient material discovery.

In manufacturing, AI contributes to predictive maintenance of equipment, minimizing downtime and optimizing operational efficiency. It also plays a crucial role in real-time quality control, where machine vision systems and AI algorithms can detect defects or inconsistencies in polyurethane products during production, ensuring higher product quality and reducing waste. The overarching expectation is that AI will drive a paradigm shift towards more intelligent, sustainable, and responsive polyurethane manufacturing ecosystems.

- AI-driven optimization of polyurethane production processes, leading to enhanced efficiency and reduced energy consumption.

- Acceleration of new material discovery and formulation development through AI-powered predictive modeling and simulation.

- Implementation of AI for real-time quality control and defect detection, ensuring higher product consistency.

- Enhanced supply chain management and demand forecasting using AI algorithms to minimize disruptions and optimize inventory.

- Predictive maintenance of manufacturing equipment through AI analytics, extending machinery lifespan and reducing downtime.

- Customization of polyurethane properties for specific applications using AI to fine-tune chemical compositions.

- Development of autonomous or semi-autonomous polyurethane manufacturing facilities with AI at the core of operations.

Key Takeaways Polyurethane Market Size & Forecast

The polyurethane market is poised for robust and sustained growth over the forecast period, driven by its versatile applications across burgeoning end-use industries globally. A key takeaway for stakeholders is the consistent demand from the construction, automotive, and furniture sectors, which continue to be the primary consumers of polyurethane products. This foundational demand, coupled with emerging applications in specialized fields, underpins the market's positive outlook. The forecast suggests that despite potential headwinds from raw material volatility, the inherent benefits of polyurethanes—such as durability, insulation properties, and design flexibility—will maintain its upward trajectory.

Another significant insight derived from the market size and forecast is the increasing importance of innovation, particularly in sustainable solutions. The market will heavily reward companies that invest in bio-based alternatives, recycling technologies, and processes that reduce the environmental footprint of polyurethane production. This is not merely an ethical imperative but a strategic necessity, as regulatory pressures and consumer preferences increasingly favor eco-friendly materials. Manufacturers that adapt quickly to these sustainability trends are likely to gain a competitive edge and capture a larger market share in the coming years.

Furthermore, the regional dynamics highlight Asia Pacific as the dominant and fastest-growing market, largely due to rapid urbanization, industrialization, and infrastructure development in countries like China and India. While North America and Europe will continue to be significant markets, driven by technological innovation and specialized applications, the growth impetus will primarily emanate from emerging economies. Companies looking to capitalize on this growth must adopt a globally diversified strategy, focusing on localization and understanding regional market nuances to maximize their penetration and profitability.

- The polyurethane market exhibits a strong growth trajectory, projected to exceed USD 130 Billion by 2033.

- Consistent demand from construction, automotive, and furniture industries remains a core growth driver.

- Sustainability and circular economy principles are becoming critical for market competitiveness and innovation.

- Asia Pacific is anticipated to be the leading region for growth, fueled by rapid industrialization and infrastructure development.

- Technological advancements in material properties and processing efficiency will continue to drive new application areas.

- Volatility in raw material prices is a persistent challenge requiring strategic sourcing and supply chain resilience.

- Specialized and high-performance polyurethane formulations offer premium growth opportunities.

Polyurethane Market Drivers Analysis

The polyurethane market is significantly propelled by its extensive utility across a multitude of industries, where its unique blend of properties offers indispensable advantages. The accelerating pace of urbanization and industrial development globally, particularly in emerging economies, underpins a robust demand for construction materials, automotive components, and consumer goods that heavily rely on polyurethane. Furthermore, the imperative for energy efficiency and sustainable building practices is intensifying the adoption of rigid polyurethane foams for superior insulation, directly contributing to market expansion. The versatility of polyurethane, ranging from flexible foams in furniture to durable coatings and adhesives, ensures its continued relevance and integration into diverse product designs.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand from Construction Industry | +2.1% | Asia Pacific, North America, Europe | Short- to Mid-term (2025-2029) |

| Growth in Automotive Sector for Lightweighting & Interiors | +1.8% | North America, Europe, Asia Pacific (China, Japan) | Mid- to Long-term (2027-2033) |

| Rising Adoption in Furniture & Bedding for Comfort & Durability | +1.5% | Global, especially Asia Pacific, Latin America | Short- to Mid-term (2025-2030) |

| Focus on Energy Efficiency and Green Building Initiatives | +1.2% | Europe, North America, Developed Asia Pacific | Mid- to Long-term (2026-2033) |

Polyurethane Market Restraints Analysis

Despite its broad utility, the polyurethane market faces several significant restraints that could temper its growth trajectory. The most prominent challenge is the volatility and fluctuating prices of key raw materials, particularly isocyanates (MDI, TDI) and polyols, which are derived from crude oil. These price swings can directly impact manufacturing costs and profit margins, making long-term planning difficult for producers. Moreover, stringent environmental regulations regarding the use of certain chemicals in polyurethane production, as well as concerns over the disposal and recycling of polyurethane waste, present formidable hurdles. These regulatory pressures necessitate costly investments in cleaner production technologies and sustainable end-of-life solutions, which can restrain market expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices (Isocyanates, Polyols) | -1.5% | Global | Short- to Mid-term (2025-2028) |

| Stringent Environmental Regulations on Production and Disposal | -1.0% | Europe, North America | Mid- to Long-term (2026-2033) |

| Competition from Substitute Materials in Certain Applications | -0.8% | Global | Short- to Long-term (2025-2033) |

| Health and Safety Concerns Related to Isocyanate Exposure | -0.5% | Global, particularly manufacturing hubs | Long-term (2028-2033) |

Polyurethane Market Opportunities Analysis

The polyurethane market is rich with opportunities, particularly in the realm of sustainable and high-performance applications. The growing global consciousness regarding environmental impact is fostering significant demand for bio-based polyurethanes derived from renewable resources and advanced recycling technologies for post-consumer and post-industrial waste. This not only aligns with green initiatives but also offers a pathway to reduce reliance on petrochemicals. Additionally, the continuous innovation in material science is opening doors for polyurethane in niche, high-value applications, such as advanced medical devices, specialized coatings for harsh environments, and components for renewable energy infrastructure. The demand for lightweight materials in electric vehicles and aerospace further amplifies these opportunities, pushing the boundaries of polyurethane's potential.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and Adoption of Bio-based Polyurethanes | +1.7% | Europe, North America, Japan | Mid- to Long-term (2027-2033) |

| Advancements in Polyurethane Recycling Technologies | +1.4% | Europe, North America | Mid- to Long-term (2028-2033) |

| Increasing Demand for Polyurethane in Electric Vehicles (EVs) | +1.1% | Global, especially China, Europe, North America | Short- to Long-term (2025-2033) |

| Expansion into Niche Applications like Medical and Additive Manufacturing | +0.9% | North America, Europe, Developed Asia Pacific | Mid- to Long-term (2026-2033) |

Polyurethane Market Challenges Impact Analysis

The polyurethane market faces multifaceted challenges that require strategic responses from industry players. Beyond raw material price volatility, ensuring the resilience and stability of the global supply chain has become a paramount concern, especially given recent geopolitical events and logistical disruptions. Manufacturers must navigate complex international trade dynamics and potential shortages, which can severely impact production schedules and costs. Furthermore, the persistent pressure to reduce the environmental footprint of polyurethane products, from manufacturing emissions to end-of-life disposal, presents a significant innovation challenge. Meeting evolving sustainability mandates while maintaining cost-effectiveness and performance requires substantial investment in research and development and the adoption of new technologies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Supply Chain Disruptions and Logistics Issues | -1.2% | Global | Short- to Mid-term (2025-2027) |

| Achieving Cost-Effective Recycling at Scale | -0.9% | Global | Mid- to Long-term (2027-2033) |

| Developing Sustainable Alternatives to Fossil-Based Raw Materials | -0.7% | Global | Long-term (2028-2033) |

| Intensifying Competition from Advanced Thermoplastics and Composites | -0.6% | Global, particularly specialized applications | Short- to Long-term (2025-2033) |

Polyurethane Market - Updated Report Scope

This report provides an in-depth analysis of the global Polyurethane Market, offering a comprehensive overview of its current state, historical performance, and future growth prospects. It segments the market by product type, end-use industry, application, and raw material, delivering granular insights into each category. The study includes detailed market size estimations and forecasts, identifies key market drivers, restraints, opportunities, and challenges, and assesses their impact on the market's trajectory. Furthermore, the report features a competitive landscape analysis, profiling leading companies and their strategic initiatives, along with a thorough regional assessment to highlight growth hotspots and emerging market dynamics. This updated scope ensures a holistic understanding for strategic decision-making within the polyurethane ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 78.5 Billion |

| Market Forecast in 2033 | USD 131.9 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, Covestro AG, Dow Inc., Wanhua Chemical Group Co. Ltd., Huntsman Corporation, LyondellBasell Industries Holdings B.V., Mitsubishi Chemical Corporation, Mitsui Chemicals Inc., SEKISUI CHEMICAL CO., LTD., Repsol S.A., LANXESS AG, Kumho Mitsui Chemicals, Inc., Tosoh Corporation, Perstorp Holding AB, DIC Corporation, Stepan Company, Coim Group, Woodbridge Foam Corporation, The Lubrizol Corporation, Chemtura Corporation (now part of Lanxess) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The polyurethane market is comprehensively segmented to provide granular insights into its diverse components and application areas. This detailed categorization allows for a precise understanding of specific growth drivers, market dynamics, and competitive landscapes within each segment. The segmentation encompasses various product types, ranging from versatile foams to specialized coatings and adhesives, reflecting polyurethane's adaptable nature. Furthermore, the market is analyzed across a broad spectrum of end-use industries, highlighting its critical role in sectors such as construction, automotive, and consumer goods. This multi-dimensional segmentation is crucial for stakeholders to identify key investment areas and develop targeted strategies that cater to distinct market needs.

- By Product Type: Flexible Foams, Rigid Foams, Coatings, Adhesives & Sealants, Elastomers, Binders, Thermoplastic Polyurethane (TPU).

- By End-Use Industry: Construction, Automotive, Furniture & Bedding, Electronics & Appliances, Footwear, Packaging, Medical, Marine, Energy, Others.

- By Application: Insulation, Seating, Flooring, Interior Components, Adhesion, Encapsulation, Protective Layers, Sound Damping.

- By Raw Material: MDI, TDI, Polyether Polyols, Polyester Polyols, Other Raw Materials.

Regional Highlights

The global polyurethane market exhibits diverse growth patterns and regional dominance, significantly influenced by local economic conditions, industrial development, and regulatory frameworks.

- Asia Pacific (APAC): Emerges as the largest and fastest-growing market for polyurethane. This dominance is primarily driven by rapid urbanization, extensive infrastructure development projects, and the expanding manufacturing bases in countries like China, India, and Southeast Asian nations. The region's thriving automotive, construction, electronics, and footwear industries are substantial consumers of polyurethane, fueling robust demand for both flexible and rigid foams, as well as coatings and adhesives. The increasing disposable income and improving living standards in these economies further contribute to the demand for polyurethane-based consumer goods and home furnishings.

- Europe: Represents a mature yet innovative market, characterized by stringent environmental regulations and a strong emphasis on sustainability. The region is at the forefront of developing bio-based polyurethanes and advanced recycling technologies. Demand is robust from the automotive sector for lightweighting solutions, the construction industry for high-performance insulation, and the furniture sector. Germany, France, and the UK are key contributors, driven by a focus on energy efficiency and circular economy initiatives.

- North America: A significant market for polyurethane, driven by a well-established automotive industry, a resilient construction sector, and continuous innovation in specialized applications. The demand for lightweight vehicles, advanced insulation materials, and high-performance coatings is particularly strong. The presence of leading R&D facilities and a focus on advanced manufacturing techniques contribute to the region's market value. The United States accounts for the largest share, with Canada also contributing steadily.

- Latin America: Expected to witness steady growth, primarily fueled by increasing investments in infrastructure, a growing construction sector, and expanding automotive production, particularly in Brazil and Mexico. The rising middle-class population also contributes to the demand for polyurethane in furniture and consumer goods.

- Middle East and Africa (MEA): Projected to experience moderate growth, supported by large-scale construction projects, diversification of economies away from oil, and increasing manufacturing activities. Countries such as Saudi Arabia, UAE, and South Africa are leading the demand, particularly for rigid foams in insulation and coatings for industrial applications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Polyurethane Market.- BASF SE

- Covestro AG

- Dow Inc.

- Wanhua Chemical Group Co. Ltd.

- Huntsman Corporation

- LyondellBasell Industries Holdings B.V.

- Mitsubishi Chemical Corporation

- Mitsui Chemicals Inc.

- SEKISUI CHEMICAL CO., LTD.

- Repsol S.A.

- LANXESS AG

- Kumho Mitsui Chemicals, Inc.

- Tosoh Corporation

- Perstorp Holding AB

- DIC Corporation

- Stepan Company

- Coim Group

- Woodbridge Foam Corporation

- The Lubrizol Corporation

- Chemtura Corporation (now part of Lanxess)

Frequently Asked Questions

What is polyurethane and what are its primary uses?

Polyurethane is a versatile polymer composed of organic units joined by carbamate (urethane) links. It is used in a vast range of applications due to its customizable properties, including flexible and rigid foams (for furniture, bedding, insulation), coatings (for protective surfaces), adhesives & sealants (for bonding), and elastomers (for durable components in footwear and automotive).

What factors are driving the growth of the polyurethane market?

Key drivers include increasing demand from the construction industry for energy-efficient insulation, growth in the automotive sector for lightweighting and interior components, rising adoption in furniture and bedding for comfort and durability, and continuous advancements in sustainable and high-performance material formulations.

Which region currently holds the largest share in the polyurethane market, and why?

Asia Pacific holds the largest market share, driven primarily by rapid urbanization, extensive infrastructure development, and the booming manufacturing sectors (automotive, construction, electronics) in countries like China and India. Economic growth and increasing disposable incomes also contribute significantly to regional demand.

What are the main challenges facing the polyurethane market?

Major challenges include the volatility of raw material prices (isocyanates and polyols), stringent environmental regulations concerning production and disposal, complexities in establishing large-scale recycling solutions, and the need to develop more sustainable, bio-based alternatives to petrochemical-derived components.

How is sustainability impacting the future of polyurethane products?

Sustainability is profoundly impacting the polyurethane market by driving innovation towards bio-based raw materials, enhancing recycling technologies, and developing products with lower environmental footprints. Manufacturers are focusing on reducing VOC emissions, improving end-of-life solutions, and promoting the circular economy to meet regulatory demands and consumer preferences for eco-friendly materials.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted