Polysilicon Market

Polysilicon Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700460 | Last Updated : July 24, 2025 |

Format : ![]()

![]()

![]()

![]()

Polysilicon Market Size

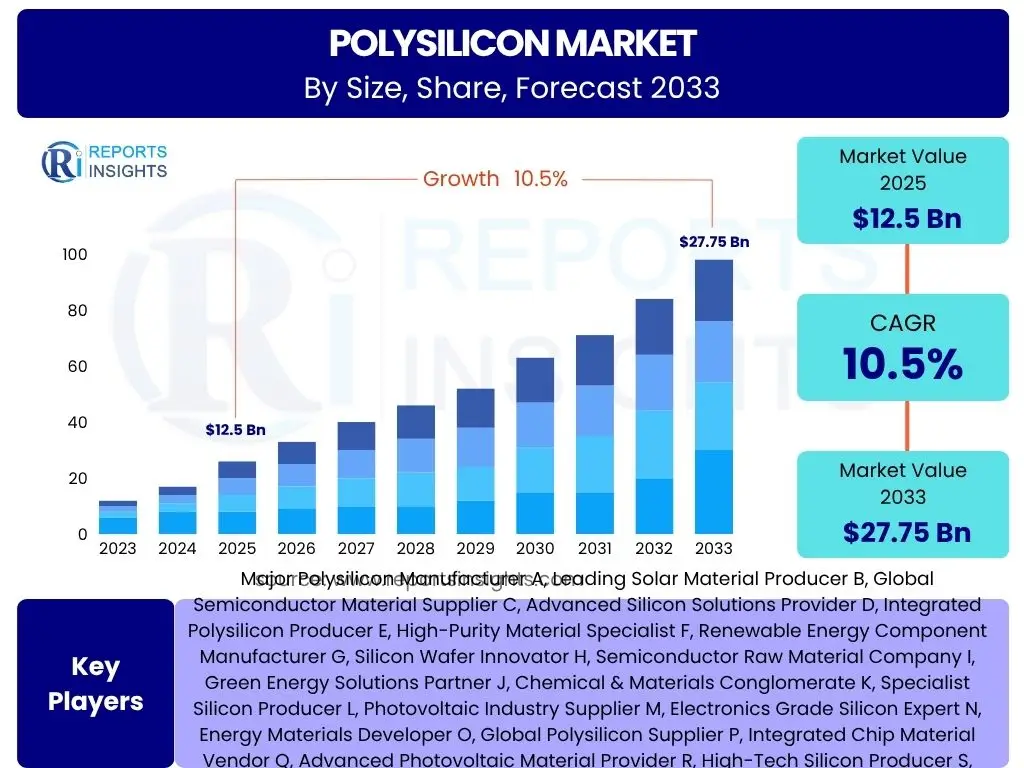

Polysilicon Market is projected to grow at a Compound annual growth rate (CAGR) of 10.5% between 2025 and 2033, valued at an estimated USD 12.5 Billion in 2025 and is projected to grow to USD 27.75 Billion by 2033, the end of the forecast period.

Key Polysilicon Market Trends & Insights

The polysilicon market is undergoing significant transformation driven by evolving energy landscapes and technological advancements. Key trends indicate a robust demand surge from renewable energy sectors, particularly solar photovoltaic (PV) manufacturing, alongside a consistent need from the burgeoning semiconductor industry. Innovations in production methodologies are also shaping the competitive landscape, influencing efficiency and cost structures across the value chain. Global efforts toward decarbonization are further accelerating the adoption of polysilicon-dependent technologies, cementing its crucial role in future energy and electronics infrastructure. These dynamics underscore a market poised for sustained expansion and strategic evolution.

- Increasing adoption of high-efficiency solar cells (PERC, TOPCon, HJT).

- Technological advancements in polysilicon production for purity and cost reduction.

- Growing demand from semiconductor industry for high-purity polysilicon.

- Shift towards sustainable and green manufacturing processes.

- Geopolitical influences impacting global supply chain resilience.

- Emergence of localized manufacturing hubs to reduce dependency.

AI Impact Analysis on Polysilicon

Artificial intelligence is increasingly influencing various stages of the polysilicon value chain, from raw material processing to final product quality control. AI-driven analytics can optimize production parameters, predict equipment failures, and enhance energy efficiency in highly intensive manufacturing processes. Furthermore, AI can aid in supply chain management by forecasting demand patterns more accurately and optimizing logistics, leading to reduced operational costs and improved resource allocation. Its application extends to research and development, accelerating the discovery of novel materials and optimizing existing polysilicon chemistries for enhanced performance. This integration signifies a crucial step towards more intelligent and resilient polysilicon production, fostering efficiency and innovation across the sector.

- Process optimization in polysilicon manufacturing for energy efficiency and yield improvement.

- Predictive maintenance for production equipment, reducing downtime and operational costs.

- Enhanced quality control through AI-driven defect detection and material analysis.

- Supply chain optimization and demand forecasting for better inventory management.

- Accelerated research and development of new polysilicon grades and applications.

- Automated monitoring and control systems for safety and environmental compliance.

Key Takeaways Polysilicon Market Size & Forecast

- The global polysilicon market is projected to achieve substantial growth from 2025 to 2033.

- Significant demand acceleration is anticipated from the solar photovoltaic industry, which remains the primary end-use sector.

- The semiconductor industry's continuous expansion contributes steadily to high-purity polysilicon demand.

- Technological innovations aimed at enhancing purity, reducing production costs, and improving energy efficiency will be critical growth enablers.

- Regional manufacturing capacities are diversifying, with emphasis on localized supply chains to mitigate geopolitical risks.

- The market's future trajectory is strongly linked to global renewable energy policies and semiconductor industry investments.

- New applications in niche electronic components and advanced materials are expected to provide additional growth avenues.

Polysilicon Market Drivers Analysis

The polysilicon market is significantly propelled by several robust drivers, primarily the escalating global demand for renewable energy and the expansion of the electronics industry. The accelerating deployment of solar photovoltaic (PV) installations worldwide, fueled by ambitious renewable energy targets and declining solar energy costs, creates a consistent and growing need for high-quality polysilicon. Simultaneously, the relentless innovation and growth in the semiconductor sector, driven by advancements in computing, artificial intelligence, and IoT devices, require a steady supply of ultra-high-purity polysilicon. These overarching trends, combined with supportive government policies and an increasing focus on energy security, collectively underpin the market's positive trajectory, fostering innovation and capacity expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Growth in Solar Photovoltaic Installations | +3.5% | Asia Pacific (China, India), Europe (Germany, Spain), North America (USA) | Long-term (2025-2033) |

| Increasing Demand from Semiconductor Industry | +2.8% | East Asia (Taiwan, South Korea, Japan), North America, Europe | Continuous (2025-2033) |

| Government Initiatives and Renewable Energy Policies | +2.2% | Global, particularly EU, China, USA, India | Medium to Long-term |

| Technological Advancements in Polysilicon Production | +1.5% | Major manufacturing hubs globally | Continuous |

| Energy Security Concerns and Decarbonization Goals | +0.5% | Global | Long-term |

Polysilicon Market Restraints Analysis

Despite significant growth drivers, the polysilicon market faces several notable restraints that could temper its expansion. High capital expenditure requirements for establishing new production facilities and the energy-intensive nature of polysilicon manufacturing contribute to elevated operational costs, potentially impacting profitability and market entry for new players. Volatility in raw material prices, particularly for metallurgical silicon, can introduce uncertainty into production costs. Furthermore, the market is susceptible to oversupply cycles, which can lead to price erosion and reduce profit margins for producers, making strategic planning and capacity management critical. Environmental regulations regarding emissions and waste disposal from polysilicon plants also impose additional compliance costs and operational constraints, requiring continuous investment in greener technologies.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure and Energy Intensity in Production | -1.8% | Global (all manufacturing regions) | Long-term |

| Volatility in Raw Material Prices (Metallurgical Silicon) | -1.2% | Global | Short to Medium-term |

| Risk of Oversupply and Price Erosion | -0.9% | Global, particularly major production regions | Cyclical, Short-term impact |

| Stringent Environmental Regulations | -0.7% | Europe, North America, East Asia | Medium to Long-term |

| Geopolitical Tensions Affecting Trade and Supply Chains | -0.5% | Global, especially sensitive trade routes | Sporadic, Short-term |

Polysilicon Market Opportunities Analysis

The polysilicon market is rich with opportunities stemming from the continuous drive for sustainable energy and advanced technology. The global push for net-zero emissions and increasing investments in green hydrogen production present new avenues for polysilicon, as it is integral to the solar energy infrastructure supporting these initiatives. Developments in ultra-high-purity polysilicon for next-generation semiconductors, including those used in quantum computing and advanced AI, offer significant high-value market expansion. Furthermore, the diversification of end-use applications beyond traditional solar and semiconductors, such as in specialized electronic components or emerging energy storage solutions, creates new demand streams. Strategic regional expansion into nascent solar markets and the development of localized supply chains also offer robust growth prospects, minimizing external dependencies and fostering regional self-sufficiency. These opportunities signal a dynamic future for polysilicon.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Green Hydrogen Production Initiatives | +2.0% | Europe, Middle East, Australia, North America | Long-term |

| Demand for Ultra-High Purity Polysilicon in Advanced Electronics | +1.8% | East Asia (South Korea, Japan, Taiwan), North America, Europe | Continuous |

| Technological Advancements in Solar Cell Efficiency (e.g., TOPCon, HJT) | +1.5% | Global | Medium to Long-term |

| Expansion into Emerging Solar Markets (e.g., Africa, Southeast Asia) | +1.0% | Developing economies globally | Long-term |

| Development of Localized Polysilicon Manufacturing Capacities | +0.7% | USA, India, Southeast Asia, Europe | Medium to Long-term |

Polysilicon Market Challenges Impact Analysis

The polysilicon market encounters several significant challenges that demand strategic responses from industry participants. Intense competition among manufacturers, often exacerbated by capacity expansions and fluctuating demand, leads to pricing pressures and can compress profit margins. The complex and energy-intensive manufacturing process necessitates substantial capital investment and sophisticated technical expertise, posing barriers to entry and expansion. Furthermore, the global supply chain for polysilicon and its raw materials is susceptible to geopolitical disruptions, trade disputes, and logistical bottlenecks, which can impact availability and cost. Meeting increasingly stringent environmental regulations, particularly concerning energy consumption and emissions, presents ongoing operational and compliance challenges, requiring continuous innovation in sustainable production methods. Successfully navigating these hurdles is crucial for long-term market stability and growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Pricing Pressures | -1.5% | Global, especially China | Continuous |

| High Energy Consumption and Operational Costs | -1.0% | All manufacturing regions | Long-term |

| Supply Chain Vulnerabilities and Geopolitical Risks | -0.8% | Global | Sporadic, but high impact |

| Technological Obsolescence and Need for Continuous R&D | -0.6% | Major technological hubs | Medium to Long-term |

| Waste Management and Disposal of By-products | -0.4% | Regions with strict environmental laws | Long-term |

Polysilicon Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global polysilicon market, offering critical insights into its current landscape, historical performance, and future projections. The report details market sizing, growth rates, key trends, and a thorough examination of the drivers, restraints, opportunities, and challenges shaping the industry. It covers extensive segmentation analysis by product type, application, and end-use, alongside a detailed regional outlook. Designed for business professionals and decision-makers, this report serves as an invaluable resource for strategic planning, investment decisions, and competitive intelligence in the dynamic polysilicon sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 27.75 Billion |

| Growth Rate | 10.5% (CAGR from 2025 to 2033) |

| Number of Pages | 257 |

| Key Trends | |

| Segments Covered | |

| Key Companies Covered | Major Polysilicon Manufacturer A, Leading Solar Material Producer B, Global Semiconductor Material Supplier C, Advanced Silicon Solutions Provider D, Integrated Polysilicon Producer E, High-Purity Material Specialist F, Renewable Energy Component Manufacturer G, Silicon Wafer Innovator H, Semiconductor Raw Material Company I, Green Energy Solutions Partner J, Chemical & Materials Conglomerate K, Specialist Silicon Producer L, Photovoltaic Industry Supplier M, Electronics Grade Silicon Expert N, Energy Materials Developer O, Global Polysilicon Supplier P, Integrated Chip Material Vendor Q, Advanced Photovoltaic Material Provider R, High-Tech Silicon Producer S, Clean Energy Material Company T |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global polysilicon market is meticulously segmented to provide a granular understanding of its diverse components and their respective market dynamics. These segmentations enable stakeholders to identify key growth areas, analyze competitive landscapes within specific categories, and tailor strategic approaches. The market is primarily bifurcated by product type, differentiating between solar-grade polysilicon for photovoltaic applications and electronic-grade polysilicon critical for the semiconductor industry, reflecting distinct purity requirements and market drivers. Further distinctions are made by form, acknowledging the various physical states in which polysilicon is supplied. Application and end-use industry segmentations provide deeper insights into the demand ecosystem, highlighting the crucial role of polysilicon across renewable energy, electronics, and other specialized sectors, allowing for precise market targeting and opportunity assessment.

- By Product Type: This segmentation distinguishes polysilicon based on its purity levels and intended application.

- Solar Grade Polysilicon: Characterized by lower purity levels compared to electronic grade, optimized for cost-effectiveness and efficiency in solar cell manufacturing. It is primarily used in photovoltaic modules and solar cells, serving the rapidly expanding renewable energy sector.

- Electronic Grade Polysilicon: Requires ultra-high purity (typically 9N to 11N) with minimal impurities, essential for the production of semiconductor wafers. It is a fundamental material for integrated circuits, discrete components, and advanced optoelectronic devices.

- By Form: Polysilicon is supplied in various physical forms to suit different manufacturing processes.

- Granular Polysilicon: Small, spherical particles, often preferred for their high packing density and ease of handling in Czochralski (CZ) crystal growth processes.

- Chunk Polysilicon: Irregularly shaped pieces, commonly used in crucible furnaces for melting and subsequent crystal growth.

- Rod Polysilicon: Cylindrical rods, typically produced via the Siemens process, often broken into smaller pieces for use.

- By Application: This outlines the primary industries and products where polysilicon is consumed.

- Solar Photovoltaics (PV Modules, Solar Cells): The largest application segment, driven by global solar energy deployment. It encompasses the raw material for solar cells that convert sunlight into electricity.

- Semiconductors (Integrated Circuits, Discrete Components, Optoelectronics): High-purity polysilicon is foundational for manufacturing silicon wafers used in microchips, transistors, diodes, and various optoelectronic devices.

- Other Applications: Includes niche uses in specialty alloys, chemical reagents, and other advanced material formulations where silicon's unique properties are leveraged.

- By End-Use Industry: This categorizes the ultimate industries benefiting from polysilicon products.

- Renewable Energy: Encompasses the entire solar power generation ecosystem, including utility-scale solar farms and distributed rooftop installations.

- Electronics & IT: Covers computing devices, telecommunications equipment, consumer electronics, and data centers, all reliant on semiconductor components.

- Automotive: Growing demand from electric vehicles (EVs) for power electronics and sensing technologies.

- Aerospace & Defense: Applications in specialized electronic components and lightweight, high-performance materials.

- Consumer Goods: Broad range of electronic gadgets and appliances.

Regional Highlights

The global polysilicon market exhibits significant regional disparities in terms of production capacity, demand, and growth dynamics. Asia Pacific stands as the undisputed leader, driven by its dominant manufacturing presence in both solar photovoltaics and semiconductors. Europe and North America are also critical regions, focusing on technological innovation, high-purity polysilicon production, and robust demand from advanced semiconductor and renewable energy projects. Latin America, the Middle East, and Africa are emerging as growth frontiers, propelled by increasing investments in solar energy infrastructure and growing industrialization.

- Asia Pacific (APAC):

- Dominates both polysilicon production and consumption, particularly China, which accounts for a substantial share of global output and demand for solar PV manufacturing.

- South Korea, Japan, and Taiwan are key players in electronic-grade polysilicon production and semiconductor manufacturing, driving high-purity demand.

- India and Southeast Asian countries (e.g., Vietnam, Malaysia) are emerging as significant solar markets with increasing installation capacities and developing manufacturing bases.

- The region benefits from economies of scale, integrated supply chains, and supportive government policies for renewable energy and electronics.

- Europe:

- A strong focus on renewable energy targets and decarbonization initiatives fuels demand for solar-grade polysilicon.

- Germany, Norway, and other European nations emphasize sustainable production methods and high-quality polysilicon for advanced applications.

- The region is actively investing in research and development for next-generation solar technologies and advanced semiconductor manufacturing, demanding high-purity material.

- Policy frameworks and incentives for solar energy deployment play a crucial role in market growth.

- North America:

- Robust demand from both the semiconductor industry and the rapidly expanding solar energy sector.

- The United States is a significant consumer of electronic-grade polysilicon due to its strong presence in advanced technology and chip manufacturing.

- Increasing domestic manufacturing initiatives for solar components and polysilicon aim to reduce reliance on foreign supply chains.

- Government support for clean energy projects and tax credits for solar installations further stimulate market expansion.

- Latin America:

- Emerging market for solar energy, particularly Brazil, Mexico, and Chile, driven by abundant solar resources and increasing energy demand.

- Investments in large-scale solar projects and distributed generation are creating new opportunities for polysilicon demand.

- The region's focus on diversifying energy sources contributes to steady growth in PV installations.

- Middle East and Africa (MEA):

- Significant potential for solar energy adoption due to high irradiation levels and growing electricity demand, especially in the Middle East.

- Large-scale solar power projects and ambitious renewable energy targets are driving polysilicon consumption.

- Africa is a nascent but high-potential market with increasing electrification efforts and development of solar infrastructure.

- Diversification of economies away from fossil fuels in the Middle East is accelerating solar investments.

Top Key Players:

The market research report covers the analysis of key stake holders of the Polysilicon Market. Some of the leading players profiled in the report include -- Major Polysilicon Manufacturer A

- Leading Solar Material Producer B

- Global Semiconductor Material Supplier C

- Advanced Silicon Solutions Provider D

- Integrated Polysilicon Producer E

- High-Purity Material Specialist F

- Renewable Energy Component Manufacturer G

- Silicon Wafer Innovator H

- Semiconductor Raw Material Company I

- Green Energy Solutions Partner J

- Chemical & Materials Conglomerate K

- Specialist Silicon Producer L

- Photovoltaic Industry Supplier M

- Electronics Grade Silicon Expert N

- Energy Materials Developer O

- Global Polysilicon Supplier P

- Integrated Chip Material Vendor Q

- Advanced Photovoltaic Material Provider R

- High-Tech Silicon Producer S

- Clean Energy Material Company T

Frequently Asked Questions:

What is polysilicon and its primary uses?

Polysilicon, or polycrystalline silicon, is a high-purity form of silicon that serves as the fundamental raw material for solar photovoltaic cells and most semiconductor devices. Its primary uses include manufacturing solar panels to generate electricity and producing silicon wafers for integrated circuits and other electronic components vital to computers, smartphones, and advanced electronics.How large is the global polysilicon market expected to be by 2033?

The global polysilicon market is projected to reach an estimated value of USD 27.75 Billion by 2033. This growth is primarily driven by the expanding solar energy sector and the continuous demand from the semiconductor industry for high-purity silicon materials.What are the main drivers of growth for the polysilicon market?

The primary drivers of growth for the polysilicon market include the rapid expansion of solar photovoltaic installations worldwide, increasing demand from the semiconductor industry for electronic-grade silicon, supportive government policies promoting renewable energy, and ongoing technological advancements in polysilicon production processes that enhance efficiency and reduce costs.What role does Asia Pacific play in the polysilicon market?

Asia Pacific plays a dominant role in the polysilicon market, serving as both the largest producer and consumer. Countries like China lead in solar-grade polysilicon manufacturing and solar panel production, while South Korea, Japan, and Taiwan are key hubs for electronic-grade polysilicon and semiconductor manufacturing, driving significant demand and innovation in the region.How does AI impact polysilicon production?

Artificial intelligence impacts polysilicon production by optimizing manufacturing processes for increased energy efficiency and yield, enabling predictive maintenance for equipment to minimize downtime, enhancing quality control through advanced defect detection, and improving supply chain management for better resource allocation and demand forecasting.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted