Polyol Ester Market

Polyol Ester Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708071 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Polyol Ester Market Size

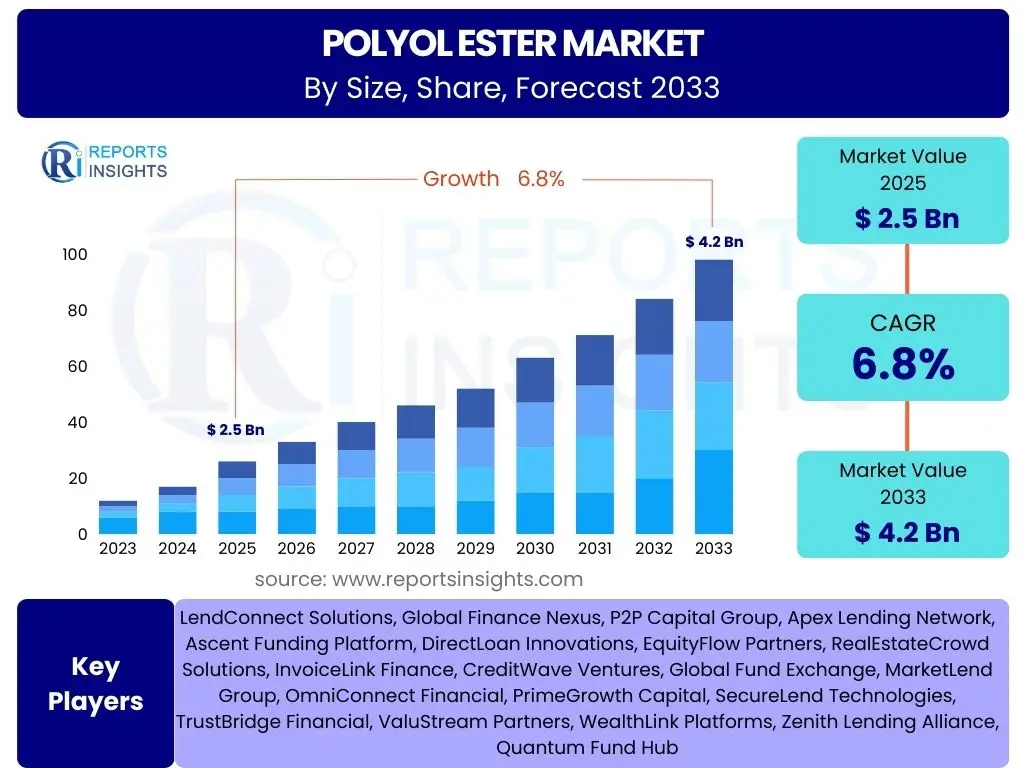

According to Reports Insights Consulting Pvt Ltd, The Polyol Ester Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 2.5 Billion in 2025 and is projected to reach USD 4.2 Billion by the end of the forecast period in 2033.

Key Polyol Ester Market Trends & Insights

Market trends for polyol esters are predominantly shaped by the increasing global demand for high-performance and environmentally sustainable industrial solutions. A significant shift towards synthetic lubricants and functional fluids in automotive, industrial, and aerospace sectors drives this growth, as polyol esters offer superior thermal stability, oxidative resistance, and lubricating properties compared to traditional mineral oils. Furthermore, evolving regulatory landscapes and a heightened focus on eco-friendly products are accelerating the adoption of bio-based polyol esters, influencing new product development and market penetration strategies.

The expansion of the HVAC&R (Heating, Ventilation, Air Conditioning, and Refrigeration) industry, particularly with the proliferation of HFO (hydrofluoroolefin) refrigerants, has created a robust demand for polyol ester-based refrigeration lubricants. These lubricants are crucial for the efficient and safe operation of modern refrigeration systems. Additionally, advancements in coating and adhesive technologies are leveraging polyol esters for enhanced durability, flexibility, and reduced volatile organic compound (VOC) emissions, aligning with current industry and consumer preferences for safer and more effective materials.

- Increasing demand for high-performance lubricants and functional fluids across industries.

- Growing adoption of environmentally friendly and bio-based polyol esters due to regulatory pressures and sustainability goals.

- Expansion of the HVAC&R sector driving the need for advanced refrigeration lubricants.

- Innovation in coating and adhesive formulations utilizing polyol esters for improved properties and reduced VOCs.

- Shifting industrial focus towards energy efficiency and extended equipment life, favoring synthetic lubricants.

- Technological advancements in polyol ester synthesis leading to tailored properties for niche applications.

AI Impact Analysis on Polyol Ester

Artificial Intelligence (AI) is poised to significantly transform various facets of the polyol ester market, from research and development to manufacturing and supply chain management. Users are particularly interested in how AI can accelerate the discovery and optimization of novel polyol ester formulations, predict material performance under diverse conditions, and streamline complex chemical synthesis processes. This technological integration is expected to reduce development cycles, cut costs, and enable the creation of highly customized polyol ester products that meet specific industry requirements with unprecedented precision.

Beyond R&D, AI’s influence extends to operational efficiencies within polyol ester production facilities. Predictive analytics, machine learning algorithms, and real-time data processing can optimize manufacturing parameters, enhance quality control, and minimize waste, thereby improving overall productivity and sustainability. Supply chain optimization, including demand forecasting, logistics management, and raw material sourcing, will also benefit immensely from AI, leading to more resilient and responsive supply networks that can adapt swiftly to market fluctuations and geopolitical challenges.

- Optimized research and development (R&D) for novel polyol ester formulations, accelerating discovery and reducing lead times.

- Predictive modeling for polyol ester performance, enabling more accurate material selection and application-specific tailoring.

- Enhanced process optimization and quality control in polyol ester manufacturing through AI-driven analytics.

- Streamlined supply chain management and demand forecasting, leading to improved efficiency and reduced inventory costs.

- Automated analysis of market trends and competitive intelligence, informing strategic business decisions.

- Facilitation of sustainable practices by optimizing resource utilization and minimizing waste in production.

Key Takeaways Polyol Ester Market Size & Forecast

The polyol ester market is poised for robust expansion, primarily driven by the escalating demand for high-performance and environmentally compliant industrial lubricants, functional fluids, and specialty chemicals. A significant takeaway is the strong Compound Annual Growth Rate (CAGR) projected through 2033, indicating a sustained upward trajectory. This growth is underpinned by the superior properties of polyol esters, which position them as critical components in advanced applications across diverse end-use industries, notably automotive, HVAC&R, and industrial manufacturing.

Furthermore, the market's future growth will be heavily influenced by advancements in sustainable chemistry and the increasing adoption of bio-based solutions. Companies that prioritize innovation in green polyol ester technologies and develop products that meet stringent environmental regulations are likely to gain a competitive edge. The market's expansion is not only volume-driven but also value-driven, with a focus on specialized, high-margin applications that leverage the unique performance characteristics of polyol esters, promising significant returns for stakeholders investing in strategic areas like R&D and market penetration.

- Significant market expansion anticipated at a CAGR of 6.8% from 2025 to 2033, reaching USD 4.2 Billion.

- Strong demand for polyol esters driven by their superior performance in high-temperature, high-stress applications.

- Increasing regulatory pressure and consumer preference for eco-friendly products are catalyzing the adoption of bio-based polyol esters.

- The automotive and HVAC&R sectors are key growth engines for polyol ester consumption, especially for synthetic lubricants.

- Technological innovation in formulation and application development will be crucial for sustained market leadership and differentiation.

Polyol Ester Market Drivers Analysis

The Polyol Ester market is experiencing significant growth propelled by several key drivers. A primary factor is the increasing global demand for high-performance synthetic lubricants and functional fluids across various industries. Polyol esters offer superior thermal stability, oxidative resistance, and low volatility compared to traditional mineral oils, making them ideal for demanding applications in automotive, industrial machinery, and aerospace sectors. As industries strive for enhanced equipment longevity, improved efficiency, and reduced maintenance costs, the adoption of advanced lubricants based on polyol esters becomes essential.

Another crucial driver is the rapid expansion of the Heating, Ventilation, Air Conditioning, and Refrigeration (HVAC&R) industry. With the phase-out of ozone-depleting refrigerants and the transition to more environmentally friendly HFO refrigerants, there is a burgeoning need for specialized refrigeration lubricants that are compatible and efficient. Polyol esters are the preferred lubricant type for these next-generation refrigerants, thus directly benefiting from the growth and technological advancements within the HVAC&R sector. Furthermore, stringent environmental regulations globally are pushing industries towards bio-based and biodegradable products, where polyol esters, particularly those derived from renewable resources, offer a compelling sustainable solution.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for high-performance synthetic lubricants | +1.5-2.0% | North America, Europe, Asia Pacific | Short to Mid-Term |

| Expansion of the HVAC&R industry and adoption of HFO refrigerants | +1.0-1.5% | Global, particularly China, India, Southeast Asia | Mid to Long-Term |

| Increasing adoption of polyol esters in automotive applications (e.g., EVs) | +0.8-1.2% | Europe, North America, Japan | Mid to Long-Term |

| Stringent environmental regulations favoring bio-based products | +0.7-1.0% | Europe, North America, Japan, Australia | Mid to Long-Term |

| Technological advancements in polyol ester synthesis and applications | +0.6-0.9% | Global | Short to Mid-Term |

Polyol Ester Market Restraints Analysis

Despite its significant growth prospects, the polyol ester market faces several notable restraints that could temper its expansion. One primary challenge is the volatility and fluctuating prices of raw materials, such as fatty acids and polyols, which are essential for polyol ester production. These price fluctuations, often influenced by agricultural output, petrochemical costs, and global supply chain disruptions, directly impact the manufacturing cost of polyol esters and can affect their competitiveness against alternative products.

Another significant restraint comes from the intense competition posed by alternative lubricant and fluid chemistries, including mineral oils, polyalphaolefins (PAOs), and other synthetic esters. While polyol esters offer superior performance in many applications, their generally higher production cost compared to conventional mineral oils can deter price-sensitive end-users. Furthermore, the market faces challenges related to the complexity of meeting diverse and evolving regulatory requirements across different regions, particularly concerning environmental and health standards, which can increase compliance costs and limit market access for certain formulations.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in raw material prices | -0.8 to -1.2% | Global | Short to Mid-Term |

| Competition from alternative lubricant chemistries | -0.7 to -1.0% | Global | Mid-Term |

| High production costs compared to mineral oils | -0.6 to -0.9% | Emerging Economies, developing markets | Short to Mid-Term |

| Stringent environmental regulations on specific chemicals | -0.5 to -0.8% | Europe, North America | Mid to Long-Term |

Polyol Ester Market Opportunities Analysis

The polyol ester market presents numerous opportunities for growth, primarily driven by the increasing global emphasis on sustainability and the continuous advancement of industrial technologies. A significant opportunity lies in the development and commercialization of sustainable and biodegradable polyol esters, particularly those derived from renewable resources. As industries worldwide commit to reducing their carbon footprint and adhering to stricter environmental mandates, the demand for eco-friendly chemical solutions is on a steep upward trajectory, opening new avenues for bio-based polyol esters in lubricants, functional fluids, and personal care products.

Emerging applications in electric vehicles (EVs) and advanced manufacturing also represent a substantial growth opportunity. EVs require specialized lubricants and coolants that can handle unique operating conditions, such as high electrical insulation properties and compatibility with new materials, areas where polyol esters excel. Furthermore, the expansion into new geographical markets, especially in rapidly industrializing economies of Asia Pacific and Latin America, offers immense potential. These regions are experiencing significant growth in manufacturing, automotive, and construction sectors, leading to increased demand for high-performance chemical inputs. Customization for niche applications and strategic collaborations with end-users to develop tailored solutions for specific performance requirements will further unlock market value.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of sustainable and biodegradable polyol esters | +1.2-1.8% | Global, particularly Europe, North America | Mid to Long-Term |

| Emerging applications in electric vehicles (EVs) and advanced manufacturing | +1.0-1.5% | North America, Europe, Asia Pacific (China, Japan) | Mid to Long-Term |

| Expansion into new geographical markets (e.g., developing economies) | +0.8-1.2% | Asia Pacific, Latin America, Middle East & Africa | Mid to Long-Term |

| Customization for niche, high-performance applications | +0.7-1.0% | Global | Short to Mid-Term |

Polyol Ester Market Challenges Impact Analysis

The polyol ester market faces several significant challenges that can influence its growth trajectory and operational complexities. One prominent challenge is managing the intricate and evolving regulatory landscapes across different countries and regions. Compliance with diverse environmental protection laws, chemical substance registrations (e.g., REACH, TSCA), and industry-specific certifications can be costly and time-consuming, requiring substantial investment in R&D and legal expertise. Non-compliance can lead to hefty fines, market exclusion, and reputational damage.

Another critical challenge involves balancing the superior performance requirements of polyol esters with their cost-effectiveness. While polyol esters offer unmatched properties for specific applications, their higher price point compared to conventional alternatives can be a deterrent, especially in price-sensitive markets. Manufacturers must continuously innovate to reduce production costs, improve synthesis efficiency, or clearly demonstrate the long-term value proposition (e.g., extended equipment life, energy savings) to justify the premium price. Furthermore, ensuring consistent quality and purity of raw materials, which are often sourced from diverse global suppliers, remains a logistical and quality control hurdle, directly impacting the final product's performance and market acceptance.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Managing complex regulatory landscapes | -0.6 to -1.0% | Europe, North America, Japan | Mid to Long-Term |

| Balancing performance requirements with cost-effectiveness | -0.5 to -0.8% | Global, particularly emerging markets | Short to Mid-Term |

| Ensuring consistent quality and purity of raw materials | -0.4 to -0.7% | Global | Short to Mid-Term |

| Educating end-users about long-term benefits | -0.3 to -0.6% | Global | Short to Mid-Term |

Polyol Ester Market - Updated Report Scope

This report provides a detailed and comprehensive analysis of the global Polyol Ester market, offering insights into its current size, historical trends, and future growth projections. It covers key market dynamics including drivers, restraints, opportunities, and challenges, along with a thorough examination of market segmentation by type, application, and end-use industry. The report also highlights regional market performance and profiles leading industry players, aiming to equip stakeholders with critical data for strategic decision-making and market positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.5 Billion |

| Market Forecast in 2033 | USD 4.2 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Lubricant Solutions Inc., Specialty Esters Corp., Advanced Chemical Synthesis, Green Lubrication Technologies, Performance Fluids Global, Industrial Chemical Producers, Coatings Innovations Ltd., Petrochemical Derivatives, Sustainable Materials Group, Global Ester Manufacturers, Synthetic Oil Formulations, Polymer Additive Solutions, Bio-Based Chemicals Co., Functional Ingredients, Precision Lubricants LLC, Chemical Blends Worldwide, Engineered Esters, High-Performance Synthetics, Chemical Innovations Hub, Apex Lubricant Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The polyol ester market is meticulously segmented to provide a granular understanding of its diverse applications and product types. This segmentation allows for precise market analysis, identifying key growth areas and niche opportunities within the broader industry landscape. Understanding these segments is crucial for stakeholders to tailor product development, marketing strategies, and investment decisions effectively across various end-use sectors.

The market is primarily segmented by type, differentiating between various polyol ester chemistries based on their foundational alcohol, which dictates their performance characteristics. Further segmentation by application highlights the diverse functional roles polyol esters play, ranging from high-performance lubricants to specialty ingredients in personal care. Finally, the end-use industry segmentation categorizes consumption across major sectors like automotive, HVAC&R, and industrial manufacturing, showcasing the broad industrial utility and demand drivers for these versatile compounds.

- By Type:

- Neopentyl Glycol (NPG) Esters

- Trimethylolpropane (TMP) Esters

- Pentaerythritol (PE) Esters

- Dipentaerythritol (Di-PE) Esters

- Complex Polyol Esters

- Others

- By Application:

- Lubricants

- Automotive Lubricants

- Industrial Lubricants

- Compressor Lubricants

- Aviation Lubricants

- Refrigeration Lubricants

- Functional Fluids

- Hydraulic Fluids

- Metalworking Fluids

- Coatings & Adhesives

- Cosmetics & Personal Care

- Food & Beverages

- Plastics & Polymers

- Textiles

- Others

- Lubricants

- By End-Use Industry:

- Automotive

- HVAC & Refrigeration

- Industrial Manufacturing

- Aerospace & Defense

- Consumer Goods

- Food Processing

- Marine

- Medical

- Electrical & Electronics

- Others

Regional Highlights

The global polyol ester market exhibits diverse growth patterns across different geographical regions, influenced by varying industrialization levels, regulatory frameworks, and technological adoption rates. Each region contributes uniquely to the market's overall dynamics, driven by specific economic and environmental factors. Understanding these regional distinctions is crucial for identifying key growth pockets and tailoring market strategies effectively.

Asia Pacific is expected to emerge as a dominant region, driven by rapid industrialization, burgeoning automotive and manufacturing sectors, and increasing infrastructure development in countries like China, India, and Southeast Asian nations. North America and Europe, characterized by stringent environmental regulations and a strong emphasis on high-performance and sustainable products, are seeing significant adoption of advanced polyol ester formulations, particularly in the HVAC&R, aerospace, and specialty chemical industries. Latin America, the Middle East, and Africa are also poised for growth, fueled by industrial expansion and increasing demand for sophisticated lubricants and functional fluids in emerging economies.

- North America: Strong demand from the automotive, aerospace, and HVAC&R sectors, coupled with a growing focus on bio-based lubricants.

- Europe: Driven by strict environmental regulations, innovation in sustainable chemistry, and demand for high-performance industrial and automotive lubricants.

- Asia Pacific (APAC): Fastest-growing region due to rapid industrialization, expanding manufacturing base, and increasing adoption in China, India, and Southeast Asian countries.

- Latin America: Emerging market with increasing industrial activity and demand for advanced lubricants in automotive and manufacturing sectors.

- Middle East & Africa (MEA): Growth attributed to industrial diversification, infrastructure development, and demand from the energy and automotive industries.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Polyol Ester Market.- Lubricant Solutions Inc.

- Specialty Esters Corp.

- Advanced Chemical Synthesis

- Green Lubrication Technologies

- Performance Fluids Global

- Industrial Chemical Producers

- Coatings Innovations Ltd.

- Petrochemical Derivatives

- Sustainable Materials Group

- Global Ester Manufacturers

- Synthetic Oil Formulations

- Polymer Additive Solutions

- Bio-Based Chemicals Co.

- Functional Ingredients

- Precision Lubricants LLC

- Chemical Blends Worldwide

- Engineered Esters

- High-Performance Synthetics

- Chemical Innovations Hub

- Apex Lubricant Systems

Frequently Asked Questions

What are polyol esters and their primary uses?

Polyol esters are synthetic lubricants and specialty chemicals formed by reacting a polyol (an alcohol with multiple hydroxyl groups) with one or more fatty acids. They are widely valued for their superior thermal stability, oxidative resistance, excellent lubricity, and biodegradability. Primary uses include high-performance lubricants for automotive, industrial, and refrigeration systems, functional fluids like hydraulic and metalworking fluids, and as components in cosmetics, coatings, and adhesives.

Why are polyol esters gaining traction in the market?

Polyol esters are gaining traction due to increasing demand for high-performance and environmentally friendly solutions across various industries. Their superior properties, such as high flash point, low volatility, and excellent lubricity, make them ideal for demanding applications. Additionally, their compatibility with next-generation refrigerants and their potential for biodegradability align with global sustainability trends and stringent environmental regulations.

What are the key types of polyol esters?

The key types of polyol esters are typically classified by their polyol component. Common types include Neopentyl Glycol (NPG) Esters, Trimethylolpropane (TMP) Esters, Pentaerythritol (PE) Esters, and Dipentaerythritol (Di-PE) Esters. Each type offers distinct performance characteristics, making them suitable for different applications, such as TMP esters for aviation lubricants and PE esters for refrigeration compressors.

How do polyol esters contribute to sustainability?

Polyol esters contribute to sustainability through several mechanisms. Many polyol esters can be synthesized from renewable bio-based raw materials, reducing reliance on petrochemicals. They often offer enhanced biodegradability compared to mineral oils. Their high performance leads to extended equipment life, reduced energy consumption, and less frequent lubricant changes, thereby minimizing waste and environmental impact in industrial operations.

Which industries are the largest consumers of polyol esters?

The largest consumers of polyol esters are the automotive industry, primarily for synthetic engine oils and transmission fluids; the HVAC & Refrigeration sector, for compressor lubricants compatible with modern refrigerants; and the Industrial Manufacturing sector, utilizing polyol ester-based industrial lubricants, hydraulic fluids, and metalworking fluids for various machinery and processes. The aerospace and defense industry also represents a significant high-value consumer.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted