Polylactic Acid Market

Polylactic Acid Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709553 | Last Updated : December 10, 2025 |

Format : ![]()

![]()

![]()

![]()

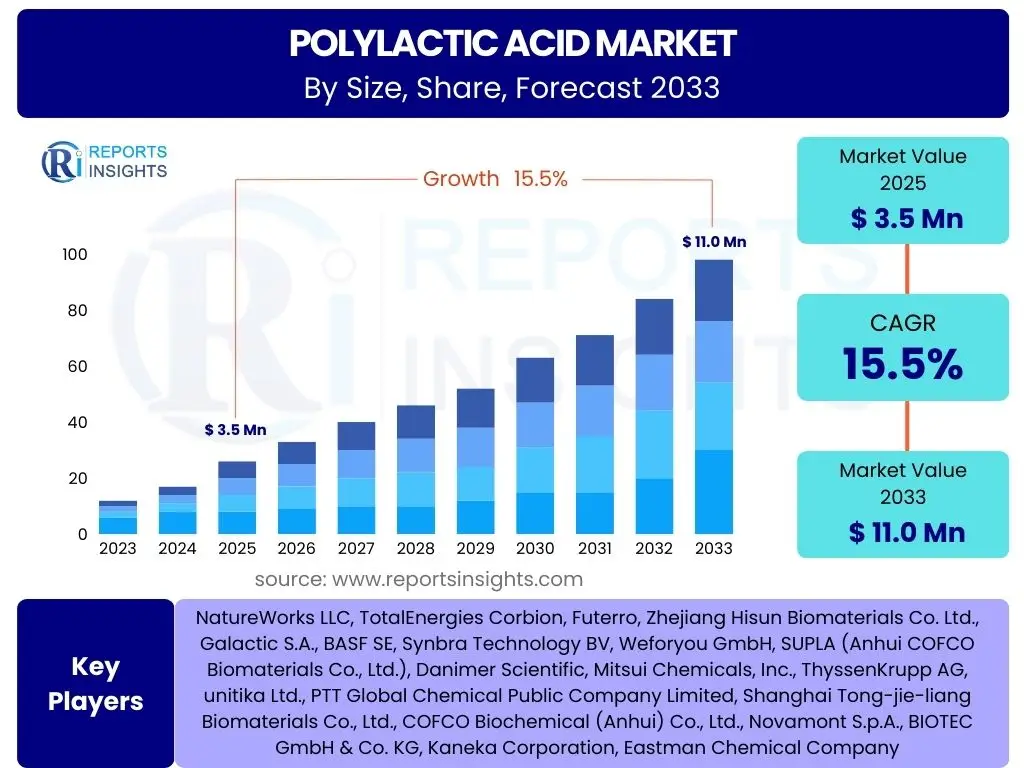

Polylactic Acid Market Size

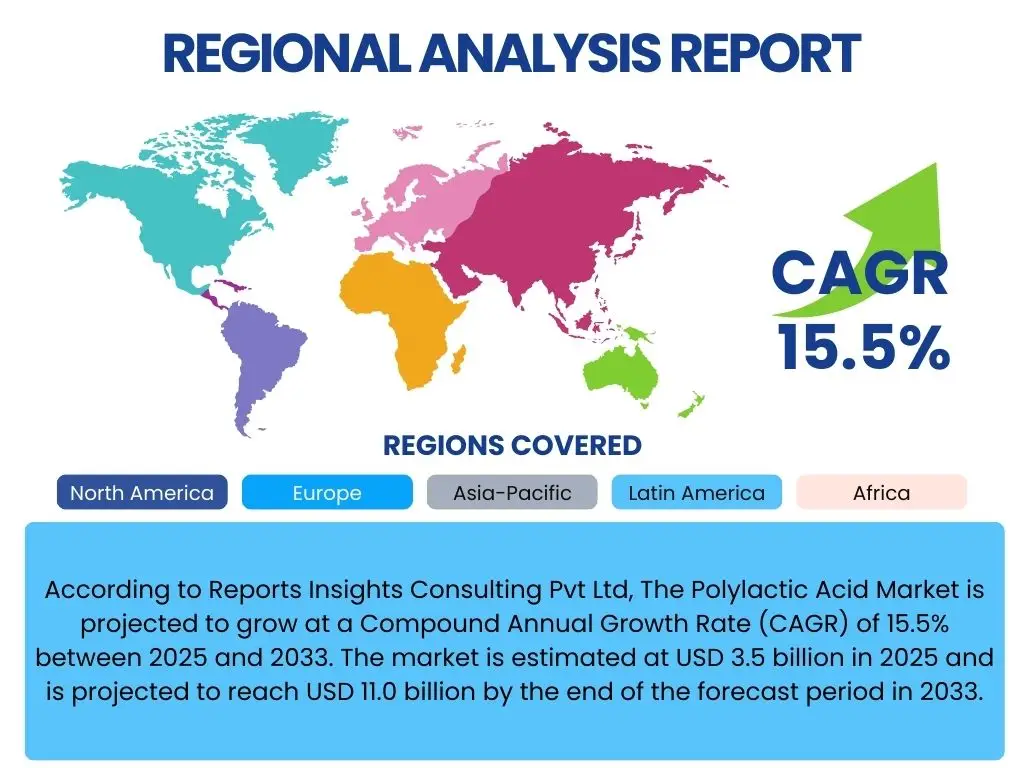

According to Reports Insights Consulting Pvt Ltd, The Polylactic Acid Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.5% between 2025 and 2033. The market is estimated at USD 3.5 billion in 2025 and is projected to reach USD 11.0 billion by the end of the forecast period in 2033.

The robust expansion of the Polylactic Acid (PLA) market is primarily driven by an accelerating global shift towards sustainable and bio-based plastics. Increasing consumer awareness regarding environmental degradation caused by traditional petrochemical-based plastics, coupled with stringent regulatory frameworks promoting biodegradability and compostability, fuels the demand for PLA. Industries across packaging, textiles, automotive, and medical sectors are actively seeking eco-friendly alternatives to reduce their carbon footprint and align with circular economy principles. This widespread adoption, supported by advancements in production technologies and cost-effectiveness, positions PLA as a pivotal material in the bio-plastics landscape.

Furthermore, continuous research and development efforts are expanding the application scope and performance characteristics of PLA, enhancing its competitiveness against conventional plastics. Innovations in PLA blends, composites, and processing techniques are addressing historical limitations such as heat resistance and impact strength, making it suitable for a broader range of high-performance applications. Government incentives and investments in green technologies globally also contribute significantly to the market's upward trajectory. As manufacturers scale up production capacities and supply chain efficiencies improve, the economic viability of PLA further strengthens, underpinning its substantial market growth forecast through 2033.

Key Polylactic Acid Market Trends & Insights

The Polylactic Acid (PLA) market is currently undergoing dynamic evolution, shaped by several influential trends that cater to a growing global demand for sustainable materials. Common inquiries from users often center on the driving forces behind PLA's increasing adoption, its expanding application areas, and the technological advancements that are enhancing its properties and reducing its cost. A significant trend is the relentless push for circular economy models, where PLA's biodegradability and compostability are highly valued, positioning it as a preferred alternative to conventional plastics in single-use items and packaging. This is further supported by rising consumer environmental consciousness and corporate sustainability initiatives aiming to mitigate plastic pollution.

Another prominent insight reveals a strong focus on innovation in PLA formulations and processing techniques. Researchers and manufacturers are actively developing new grades of PLA with improved mechanical properties, better heat resistance, and enhanced barrier functions, addressing the performance gaps that previously limited its use in certain applications. This includes the development of high-performance PLA blends and composites, which are critical for its penetration into more demanding sectors like automotive, electronics, and construction. Furthermore, the market is witnessing an emphasis on optimizing the entire lifecycle of PLA, from sustainable feedstock sourcing, such as non-food biomass, to efficient industrial composting and chemical recycling methods, ensuring a truly eco-friendly profile.

The geographic expansion of PLA production and consumption, particularly in emerging economies, represents a key trend, driven by industrialization and increasing environmental regulations in these regions. Strategic partnerships and collaborations across the value chain, involving raw material suppliers, PLA producers, converters, and end-users, are becoming more common to streamline innovation and market penetration. These collaborations aim to ensure a stable supply of high-quality PLA and accelerate its integration into diverse product lines, solidifying its position as a cornerstone of the bio-plastics industry.

- Growing adoption in sustainable packaging solutions

- Expansion into diverse end-use industries including textiles, automotive, and medical

- Technological advancements in PLA blends and composites for enhanced performance

- Increased focus on circular economy principles and advanced recycling methods for PLA

- Rising consumer awareness and demand for bio-based and compostable products

- Strategic collaborations across the PLA value chain to optimize production and application

AI Impact Analysis on Polylactic Acid

Artificial Intelligence (AI) is poised to significantly transform the Polylactic Acid (PLA) market, with user queries frequently exploring how AI can enhance efficiency, optimize material properties, and accelerate innovation in this sector. One key area of AI's impact is in the optimization of PLA production processes. AI-driven algorithms can analyze vast datasets from manufacturing plants, identifying patterns and correlations that human operators might miss, thereby enabling predictive maintenance, optimizing reaction conditions, and improving yield and energy efficiency. This leads to reduced operational costs and a more consistent product quality, making PLA more competitive against traditional plastics.

Furthermore, AI is instrumental in accelerating material innovation and discovery for PLA. Through machine learning models, researchers can predict the properties of novel PLA formulations and blends based on their chemical structures and processing parameters, drastically reducing the need for extensive physical experimentation. This capability allows for the rapid development of PLA grades with tailored properties, such as improved heat resistance, impact strength, or biodegradability rates, customized for specific applications. AI can also facilitate the design of more sustainable feedstock conversion processes, by optimizing enzymatic reactions or fermentation processes for lactic acid production from biomass.

Beyond production and material science, AI's influence extends to supply chain management and market analytics within the PLA industry. Predictive analytics can forecast demand fluctuations, optimize inventory levels, and streamline logistics, ensuring a more resilient and responsive supply chain for PLA manufacturers and consumers. Moreover, AI tools can analyze market trends, consumer preferences, and regulatory changes with greater accuracy, providing invaluable insights for strategic decision-making and identifying new market opportunities for PLA products. The integration of AI therefore promises to drive both operational excellence and groundbreaking advancements across the entire PLA value chain, fostering a more efficient and innovative bio-plastics sector.

- Optimization of PLA synthesis and polymerization processes for higher yield and purity

- Predictive modeling for accelerated development of novel PLA blends and composites with enhanced properties

- AI-driven quality control and process monitoring in manufacturing plants

- Enhanced supply chain management and demand forecasting for PLA raw materials and finished products

- Identification of sustainable feedstock sources and optimization of their conversion to lactic acid using AI algorithms

- Automated analysis of market trends and consumer preferences to inform product development and market strategy

Key Takeaways Polylactic Acid Market Size & Forecast

The analysis of common user questions regarding the Polylactic Acid (PLA) market size and forecast consistently reveals a strong interest in understanding the core drivers of its rapid growth, the sustainability imperative, and the long-term viability of PLA as a widespread plastic alternative. A primary takeaway is the undeniable momentum behind the market's expansion, driven by global environmental policies, increasing corporate commitments to sustainability, and evolving consumer preferences towards eco-friendly products. This robust growth trajectory, reflected in the double-digit CAGR, underscores PLA's critical role in the transition to a more circular economy and a less plastic-polluted world. The shift from fossil-based resources to bio-based and biodegradable materials is not merely a niche trend but a fundamental transformation shaping industrial practices and product development worldwide.

Another significant insight derived from market inquiries is the growing diversification of PLA applications, which is essential for sustaining its market growth. While packaging remains a dominant sector, the increasing integration of PLA into textiles, automotive components, medical devices, and 3D printing signifies its versatility and improving performance attributes. This broadening application base is supported by continuous research and development efforts aimed at enhancing PLA's mechanical strength, heat resistance, and durability, thereby overcoming previous limitations. These technological advancements are pivotal in enabling PLA to compete effectively with conventional plastics in higher-performance applications, unlocking new market segments and driving increased demand over the forecast period.

Finally, a crucial takeaway relates to the strategic importance of investment in production capacity and infrastructure. The projected market value by 2033 indicates a substantial increase in demand, necessitating significant scaling up of lactic acid fermentation and PLA polymerization facilities globally. This expansion will be supported by innovations in feedstock sourcing, including the utilization of non-food biomass, and advancements in efficient production technologies to ensure economic viability and reduce the environmental footprint of PLA manufacturing. The long-term forecast points to a future where PLA is not just a niche bioplastic but a mainstream material, integral to various industries seeking to achieve ambitious sustainability targets and meet evolving regulatory requirements.

- Significant market growth driven by global sustainability trends and regulatory support.

- PLA is increasingly viewed as a viable and preferred alternative to conventional plastics across multiple industries.

- Diversification of applications beyond packaging into textiles, automotive, and medical sectors fuels demand.

- Ongoing technological advancements are enhancing PLA's performance, expanding its utility.

- Increased investment in production capacity and sustainable feedstock development is crucial for meeting future demand.

- Consumer and corporate demand for bio-based and biodegradable materials is a foundational driver of market expansion.

Polylactic Acid Market Drivers Analysis

The Polylactic Acid (PLA) market is experiencing significant tailwinds from several powerful drivers, chief among them being the escalating global concern over plastic waste and its environmental impact. This concern has translated into increased pressure from governments, environmental organizations, and consumers for sustainable alternatives to traditional petrochemical-based plastics. Consequently, regulations promoting biodegradable and compostable packaging, coupled with bans on single-use plastics in various regions, are compelling industries to adopt materials like PLA. The favorable legislative landscape, particularly in Europe and North America, provides a strong impetus for market growth, creating a demand-pull for bio-based polymers.

Parallel to regulatory support, the growing consumer awareness regarding environmental issues plays a pivotal role. Consumers are increasingly willing to pay a premium for eco-friendly products, forcing brands to integrate sustainable packaging and materials into their product offerings. This shift in consumer preference is a powerful market driver, encouraging manufacturers across diverse sectors—from food and beverages to consumer goods—to invest in PLA. Furthermore, advancements in PLA production technologies have led to improved material properties, such as enhanced heat resistance and mechanical strength, broadening its applicability and making it a more viable option for performance-demanding applications, thereby stimulating further market penetration.

Moreover, the strategic initiatives by major corporations to achieve their sustainability goals are significantly impacting the PLA market. Many multinational companies have committed to reducing their reliance on fossil-based plastics and incorporating a higher percentage of recycled or bio-based materials into their products. This corporate responsibility trend translates into substantial procurement demand for PLA, often through direct partnerships with producers. The ongoing research and development in optimizing PLA manufacturing processes, including the use of non-food biomass as feedstock, further contributes to its cost-effectiveness and scalability, making it an attractive option for large-scale industrial adoption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing environmental regulations and plastic bans | +3.5% | Europe, North America, Asia Pacific (China, India) | Short to Mid-term (2025-2030) |

| Growing consumer preference for sustainable products | +2.8% | Global, particularly developed economies | Mid to Long-term (2026-2033) |

| Corporate sustainability initiatives and brand commitments | +2.3% | Global multinational corporations | Short to Mid-term (2025-2030) |

| Technological advancements improving PLA properties and processing | +2.0% | Global, R&D focused regions (EU, US, Japan) | Mid to Long-term (2027-2033) |

| Expansion of application areas (packaging, textiles, automotive) | +1.8% | Global, diverse industrial sectors | Short to Mid-term (2025-2030) |

| Rising cost and volatility of crude oil prices affecting traditional plastics | +1.5% | Global, especially import-dependent regions | Short-term (2025-2027) |

Polylactic Acid Market Restraints Analysis

Despite its promising growth trajectory, the Polylactic Acid (PLA) market faces several significant restraints that could impede its full potential. A primary challenge lies in the relatively higher production cost of PLA compared to conventional petrochemical-based plastics, such as polyethylene (PE) or polypropylene (PP). While economies of scale are improving and technologies are advancing, the initial capital expenditure for new PLA production facilities and the ongoing costs associated with feedstock sourcing and processing can make it less competitive on price points, especially for commodity applications where cost is a paramount factor. This cost disparity often deters manufacturers from fully transitioning to PLA, particularly in markets with tight margins.

Another notable restraint is the inherent performance limitations of standard PLA grades when compared to some conventional plastics. While advancements are continually being made, typical PLA can exhibit lower heat resistance, impact strength, and barrier properties, which restrict its use in high-temperature applications, durable goods, or products requiring extended shelf life without significant modification or blending. Addressing these performance gaps often requires additional processing steps, blending with other polymers, or the use of additives, which can further increase costs and complexity. This necessitates ongoing research and development to tailor PLA for specific, demanding applications without compromising its eco-friendly attributes.

Furthermore, the infrastructure for industrial composting and recycling of PLA is not yet universally established or widely accessible. For PLA to fulfill its promise as a truly circular material, robust collection, sorting, and composting facilities are essential. In many regions, the lack of adequate industrial composting infrastructure means that PLA products may end up in landfills or general recycling streams, where they cannot properly biodegrade, thus negating their environmental benefit and causing consumer confusion. This infrastructural deficit, coupled with consumer misunderstandings about proper disposal, represents a significant hurdle to broader market acceptance and the realization of PLA's sustainable potential.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher production cost compared to conventional plastics | -2.5% | Global, particularly cost-sensitive markets | Short to Mid-term (2025-2030) |

| Limited performance properties (e.g., heat resistance, impact strength) of standard grades | -1.8% | Global, specific high-performance applications | Mid-term (2026-2031) |

| Lack of widespread industrial composting infrastructure | -1.5% | Global, varying by region (more pronounced in developing regions) | Long-term (2028-2033) |

| Competition from other bio-based or recycled plastics | -1.2% | Global, across all end-use sectors | Short to Mid-term (2025-2030) |

| Dependence on agricultural feedstocks and potential food vs. fuel/materials debate | -1.0% | Global, particularly regions with food security concerns | Long-term (2029-2033) |

| Consumer confusion regarding proper disposal and recyclability | -0.8% | Global, affecting consumer perception | Short to Mid-term (2025-2029) |

Polylactic Acid Market Opportunities Analysis

The Polylactic Acid (PLA) market is ripe with numerous opportunities that promise to accelerate its growth and expand its footprint across various industries. A significant opportunity lies in the burgeoning demand for sustainable packaging, particularly in the food and beverage sector. As regulations intensify and consumer preferences shift towards eco-friendly options, PLA's biodegradability and compostability make it an ideal material for single-use packaging, rigid containers, flexible films, and food service ware. This segment presents a vast untapped potential, especially in emerging economies where packaging consumption is rising rapidly, and environmental awareness is gaining traction.

Another substantial opportunity stems from the continuous innovation in PLA material science. Developing advanced PLA grades with improved mechanical, thermal, and barrier properties will unlock new applications in more demanding sectors. For instance, high-heat resistant PLA can penetrate the automotive interior, electronic casing, and durable consumer goods markets, where conventional PLA previously faced limitations. Similarly, enhanced barrier properties could make PLA a more viable option for sensitive food packaging, extending shelf life and reducing food waste. Investment in R&D to create specialized PLA formulations, including blends with other bio-based polymers, offers a pathway to differentiate products and capture premium market segments.

Furthermore, the growth of the 3D printing and additive manufacturing industry presents a unique and expanding opportunity for PLA. PLA is already a popular filament choice due to its ease of printing, biodegradability, and minimal warping. As 3D printing expands from prototyping to end-use part production in various industries like aerospace, medical, and consumer goods, the demand for high-performance PLA filaments is expected to surge. Leveraging this trend by developing specialized PLA filaments with enhanced strength, flexibility, or specific functionalities can provide a competitive edge. Additionally, the increasing focus on the circular economy and bioplastics recycling initiatives creates opportunities for chemical recycling of PLA, which can recover lactic acid monomers, enabling a truly closed-loop system and further enhancing its sustainability credentials.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expanding demand for sustainable packaging in F&B and consumer goods | +3.0% | Global, particularly Asia Pacific & Europe | Short to Mid-term (2025-2030) |

| Technological breakthroughs creating high-performance PLA grades | +2.5% | Global, R&D intensive regions (North America, Europe, Japan) | Mid to Long-term (2027-2033) |

| Growth in 3D printing and additive manufacturing applications | +2.0% | Global, tech-forward industries | Short to Mid-term (2025-2030) |

| Development of advanced chemical recycling and composting infrastructure | +1.7% | Europe, North America, pioneering regions | Long-term (2028-2033) |

| Strategic collaborations with major brands for product integration | +1.5% | Global, large multinational corporations | Short-term (2025-2028) |

| Utilization of non-food biomass as sustainable feedstock for lactic acid production | +1.2% | Global, agricultural regions | Mid to Long-term (2027-2033) |

Polylactic Acid Market Challenges Impact Analysis

The Polylactic Acid (PLA) market, while promising, contends with several significant challenges that could hinder its growth and broader adoption. One primary challenge is the volatility and availability of sustainable feedstock, primarily agricultural crops like corn and sugarcane, for lactic acid production. Fluctuations in crop yields due to climate change, competition with food and feed production, and geopolitical factors can lead to price instability and supply disruptions for lactic acid monomers. This dependence raises concerns about land use, food security, and the overall environmental footprint, urging the industry to explore alternative non-food biomass sources, which themselves come with complex processing and cost challenges.

Another substantial challenge is the perception and reality of PLA's end-of-life management. While PLA is biodegradable and compostable, it often requires specific industrial composting conditions (high temperatures and humidity) to fully break down. This distinction is often misunderstood by consumers, who may incorrectly assume it degrades in home composts or natural environments, leading to improper disposal. The lack of standardized labeling and inadequate widespread industrial composting infrastructure in many regions means that PLA can end up in landfills, where it degrades slowly and contributes to methane emissions, or contaminates traditional plastic recycling streams, reducing the quality of recycled products. This issue severely impacts PLA's circularity and its environmental credibility.

Furthermore, competition from other bio-based polymers and recycled plastics poses a continuous challenge to PLA's market share. While PLA is a leading bioplastic, other bio-based alternatives like Polyhydroxyalkanoates (PHAs), Bio-polyethylene (Bio-PE), or recycled content plastics offer different property profiles and sustainability claims. PHA, for instance, boasts better marine biodegradability, while Bio-PE offers direct drop-in replacement for conventional PE. Manufacturers and brands considering sustainable options have a growing array of choices, and PLA must continually demonstrate its superior combination of performance, cost-effectiveness, and environmental benefits to maintain its competitive edge. This requires ongoing investment in R&D and clear communication of its unique value proposition.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility and availability of sustainable feedstock | -1.5% | Global, particularly in regions dependent on specific crops | Short to Mid-term (2025-2030) |

| Inadequate industrial composting infrastructure and consumer confusion | -1.8% | Global, varying by region, affecting end-of-life management | Mid to Long-term (2027-2033) |

| Competition from other bio-based and recycled plastic alternatives | -1.2% | Global, impacting market share in various applications | Short to Mid-term (2025-2030) |

| Need for further performance improvements to match conventional plastics | -1.0% | Global, affecting penetration into high-performance markets | Mid-term (2026-2031) |

| Standardization and certification for biodegradability and compostability | -0.8% | Global, impacting regulatory acceptance and consumer trust | Short to Mid-term (2025-2029) |

| Scalability of production to meet rapidly increasing demand | -0.7% | Global, particularly in expanding markets | Short-term (2025-2028) |

Polylactic Acid Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Polylactic Acid (PLA) market, covering historical data from 2019 to 2023 and offering detailed forecasts up to 2033. The report delves into key market dynamics, including drivers, restraints, opportunities, and challenges, along with a thorough examination of market trends, segmentation, and regional landscapes. It aims to offer strategic insights for stakeholders to make informed business decisions, supported by quantitative market size estimations and growth projections.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.5 billion |

| Market Forecast in 2033 | USD 11.0 billion |

| Growth Rate | 15.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | NatureWorks LLC, TotalEnergies Corbion, Futerro, Zhejiang Hisun Biomaterials Co. Ltd., Galactic S.A., BASF SE, Synbra Technology BV, Weforyou GmbH, SUPLA (Anhui COFCO Biomaterials Co., Ltd.), Danimer Scientific, Mitsui Chemicals, Inc., ThyssenKrupp AG, unitika Ltd., PTT Global Chemical Public Company Limited, Shanghai Tong-jie-liang Biomaterials Co., Ltd., COFCO Biochemical (Anhui) Co., Ltd., Novamont S.p.A., BIOTEC GmbH & Co. KG, Kaneka Corporation, Eastman Chemical Company |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Polylactic Acid (PLA) market is intricately segmented to provide a granular understanding of its diverse applications, end-use industries, and material forms. This segmentation analysis helps in identifying key growth pockets, understanding demand patterns across different sectors, and formulating targeted market strategies. The market is primarily segmented based on its application in various industries, the end-use sectors consuming PLA products, the specific types of PLA polymers, and the physical forms in which PLA is supplied.

- By Application:

- Packaging (Flexible Packaging, Rigid Packaging, Food Service Ware)

- Textile

- Agriculture (Mulch Films, Crop Protection)

- Medical (Sutures, Implants, Drug Delivery)

- Automotive

- Electronics

- 3D Printing

- Others

- By End-Use Industry:

- Food & Beverage

- Healthcare

- Consumer Goods

- Automotive

- Textile

- Agriculture

- Building & Construction

- Electronics

- Others

- By Type:

- PLLA (Poly-L-Lactide)

- PDLA (Poly-D-Lactide)

- PDLLA (Poly-DL-Lactide)

- By Form:

- Films & Sheets

- Fibers

- Bottles

- Injection Molding

- Coatings

- Other

Regional Highlights

- North America: This region is a significant market for Polylactic Acid, driven by increasing consumer awareness regarding environmental issues and stringent regulations promoting sustainable packaging. The presence of key market players and a robust R&D infrastructure further support market growth. The food and beverage sector, along with advancements in medical applications, are key contributors to PLA demand.

- Europe: Europe stands as a pioneering region in the adoption of bioplastics, with a strong regulatory framework, including the European Green Deal and single-use plastic directives, heavily favoring PLA. Countries like Germany, France, and Italy are at the forefront of implementing circular economy principles, leading to high demand for compostable and biodegradable materials in packaging, agriculture, and consumer goods. Continuous innovation and government incentives for sustainable industries are also propelling growth.

- Asia Pacific (APAC): The Asia Pacific region is projected to be the fastest-growing market for PLA, primarily due to rapid industrialization, increasing environmental concerns, and a growing middle-class population demanding sustainable products. Countries such as China, India, and Japan are witnessing substantial investments in bio-based materials and production capacities. The expanding packaging, textile, and automotive industries in this region are expected to drive significant demand for PLA in the coming years, balancing economic growth with environmental responsibility.

- Latin America: This region shows emerging potential for the PLA market, with increasing awareness about environmental protection and a gradual shift towards sustainable practices. Brazil and Mexico are leading the adoption of bioplastics, especially in packaging and agricultural applications, driven by local initiatives and evolving regulatory landscapes. While smaller than other regions, its growth trajectory is expected to accelerate.

- Middle East and Africa (MEA): The MEA region is at an nascent stage but is gradually recognizing the benefits of sustainable materials. Government initiatives aimed at diversifying economies and reducing reliance on petrochemicals, coupled with growing environmental concerns, are slowly paving the way for PLA adoption, particularly in packaging and agricultural sectors. Investments in sustainable technologies are anticipated to drive future growth in select countries.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Polylactic Acid Market.- NatureWorks LLC

- TotalEnergies Corbion

- Futerro

- Zhejiang Hisun Biomaterials Co. Ltd.

- Galactic S.A.

- BASF SE

- Synbra Technology BV

- Weforyou GmbH

- SUPLA (Anhui COFCO Biomaterials Co., Ltd.)

- Danimer Scientific

- Mitsui Chemicals, Inc.

- ThyssenKrupp AG

- Unitika Ltd.

- PTT Global Chemical Public Company Limited

- Shanghai Tong-jie-liang Biomaterials Co., Ltd.

- COFCO Biochemical (Anhui) Co., Ltd.

- Novamont S.p.A.

- BIOTEC GmbH & Co. KG

- Kaneka Corporation

- Eastman Chemical Company

Frequently Asked Questions

What is Polylactic Acid (PLA) and why is it important?

Polylactic Acid (PLA) is a biodegradable and compostable thermoplastic derived from renewable resources like corn starch or sugarcane. It is crucial for its role as a sustainable alternative to conventional fossil-based plastics, helping to reduce plastic pollution and carbon footprint across various industries.

What are the primary applications of PLA?

PLA finds primary applications in packaging (flexible, rigid, and food service ware), textiles, agriculture (mulch films), medical devices (sutures, implants), automotive interiors, and 3D printing filaments due to its versatility and eco-friendly properties.

How does PLA compare to traditional plastics in terms of performance?

Standard PLA offers good transparency, stiffness, and processability. While some grades may have lower heat resistance and impact strength than certain traditional plastics, ongoing advancements in PLA blends and composites are continuously improving its performance to match or exceed conventional materials for specific applications.

Is PLA truly biodegradable and compostable?

Yes, PLA is both biodegradable and compostable, but it typically requires specific conditions found in industrial composting facilities (high temperatures, humidity, and microbial activity) to fully break down into natural components like water, carbon dioxide, and biomass. It does not readily degrade in natural environments or home composts.

What are the key market drivers for PLA growth?

Key drivers include increasing global environmental regulations and bans on single-use plastics, growing consumer demand for sustainable and eco-friendly products, corporate sustainability initiatives, and continuous technological advancements improving PLA's properties and expanding its application range.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted