Polyethylene Terephthalate Glycol Market

Polyethylene Terephthalate Glycol Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709959 | Last Updated : December 24, 2025 |

Format : ![]()

![]()

![]()

![]()

Polyethylene Terephthalate Glycol Market Size

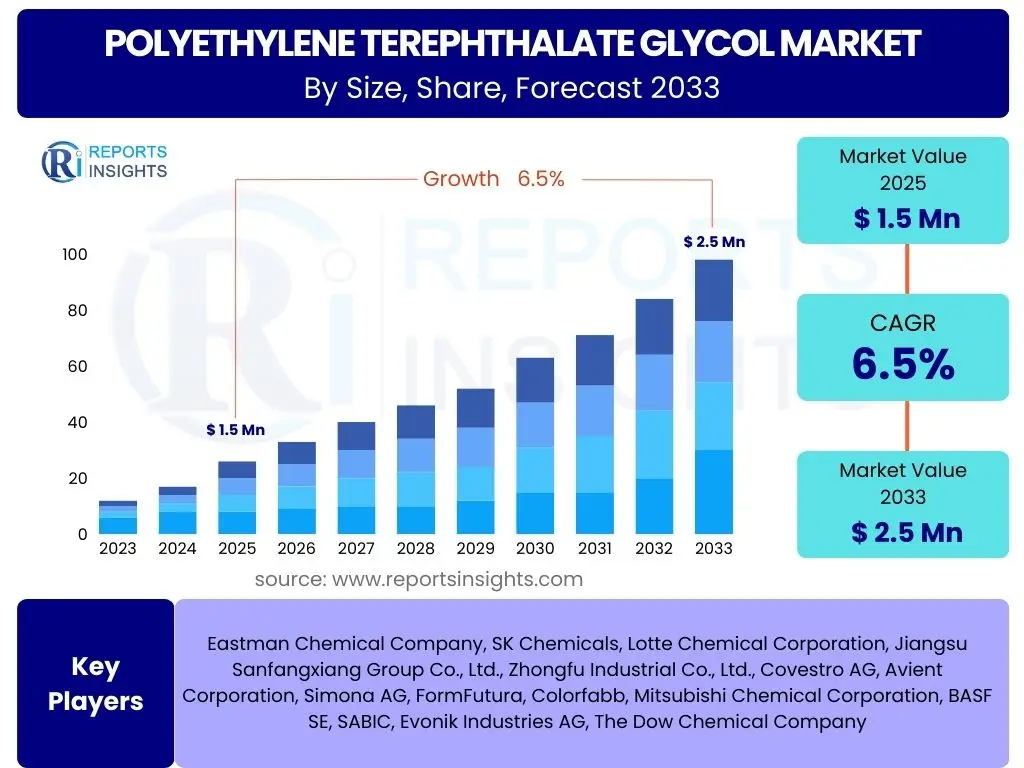

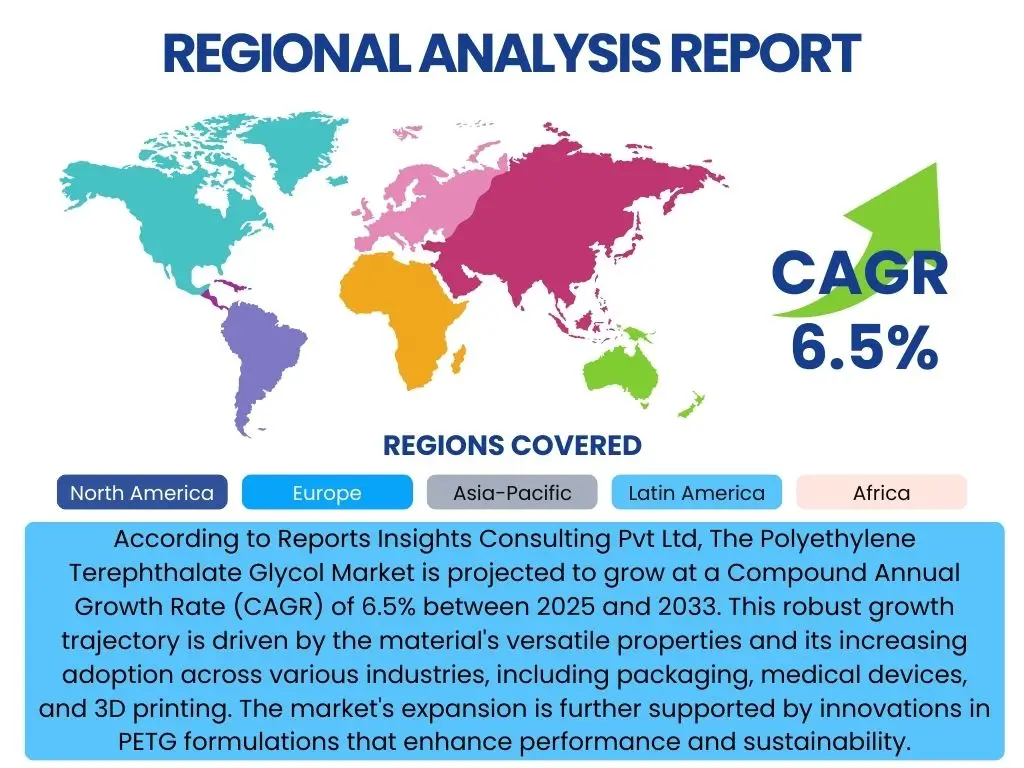

According to Reports Insights Consulting Pvt Ltd, The Polyethylene Terephthalate Glycol Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. This robust growth trajectory is driven by the material's versatile properties and its increasing adoption across various industries, including packaging, medical devices, and 3D printing. The market's expansion is further supported by innovations in PETG formulations that enhance performance and sustainability.

The market is estimated at USD 1.5 Billion in 2025, reflecting a significant base fueled by consistent demand from established and emerging applications. As industries increasingly seek materials that offer a superior balance of clarity, toughness, and chemical resistance, PETG continues to gain traction as a preferred choice over conventional polymers. This solid foundation positions the market for sustained expansion.

The Polyethylene Terephthalate Glycol market is projected to reach USD 2.5 Billion by the end of the forecast period in 2033. This forecast indicates a substantial increase in market valuation, underpinned by continuous technological advancements, expanding end-use applications, and a growing emphasis on high-performance, recyclable plastic solutions globally. The projected growth underscores the material's strategic importance in various manufacturing sectors.

Key Polyethylene Terephthalate Glycol Market Trends & Insights

Users frequently inquire about the principal shifts and evolving dynamics within the Polyethylene Terephthalate Glycol (PETG) market. Analysis reveals that key user questions often center on how sustainability initiatives are influencing material selection, the impact of technological advancements, and the expanding scope of PETG applications. There is a strong interest in understanding the material's role in cutting-edge industries and its competitive positioning against alternative polymers. Users are particularly keen on identifying trends related to production innovations, supply chain resilience, and the overall market's response to global economic and environmental pressures.

The market is currently undergoing transformative shifts, largely driven by the increasing global emphasis on sustainable packaging solutions. Consumers and regulators alike are pushing for materials that offer improved recyclability and a reduced environmental footprint, positioning PETG as an attractive option due to its favorable properties in these areas. Additionally, the rapid expansion of additive manufacturing (3D printing) is opening new avenues for PETG, particularly given its excellent printability, dimensional stability, and material strength, leading to diverse prototyping and production applications.

Another significant trend is the growing demand from the medical and pharmaceutical sectors, where PETG’s clarity, chemical resistance, and sterilization capabilities make it ideal for various medical devices, diagnostic components, and pharmaceutical packaging. This trend is further supported by the need for robust, safe, and easily processable materials in a highly regulated environment. Concurrently, advancements in specialized PETG grades, offering enhanced barrier properties or increased impact resistance, are catering to niche applications and expanding the material's overall utility and market reach.

- Growing adoption in sustainable packaging solutions across food, beverage, and personal care sectors.

- Increased demand from the medical and pharmaceutical industries for device components and sterile packaging.

- Expansion of 3D printing and additive manufacturing applications, utilizing PETG for its versatility and ease of use.

- Shift towards specialized PETG grades offering enhanced performance characteristics like improved barrier properties or UV resistance.

- Focus on circular economy initiatives, driving demand for PETG’s recyclability and compatibility with existing recycling streams.

- Development of bio-based or partially bio-based PETG formulations to meet evolving environmental standards.

AI Impact Analysis on Polyethylene Terephthalate Glycol

User queries regarding the impact of Artificial Intelligence (AI) on the Polyethylene Terephthalate Glycol (PETG) market often revolve around efficiency gains in manufacturing, optimization of supply chains, and the potential for accelerated material innovation. Users are keen to understand how AI can enhance predictive analytics for market demand, improve quality control in production processes, and streamline research and development efforts for new PETG formulations. There is also interest in AI's role in achieving sustainability goals, such as optimizing energy consumption during PETG production and managing waste streams more effectively. The overarching theme is how AI can drive operational excellence and foster competitive advantages within the PETG industry.

The integration of AI technologies is poised to revolutionize various facets of the PETG industry, from raw material sourcing to end-product manufacturing and distribution. In production, AI-powered systems can optimize process parameters, predict equipment failures, and ensure consistent product quality, thereby reducing waste and improving operational efficiency. Predictive maintenance, enabled by AI algorithms analyzing sensor data from machinery, can significantly minimize downtime and extend the lifespan of manufacturing assets, leading to cost savings and increased output of PETG resins.

Furthermore, AI is instrumental in accelerating material innovation and R&D for PETG. Machine learning algorithms can analyze vast datasets of polymer properties, synthesis methods, and application performance, helping researchers identify novel formulations with enhanced characteristics more rapidly. This data-driven approach can lead to the development of new PETG grades tailored for specific, high-value applications or improved sustainability profiles. Additionally, AI's application in supply chain management can optimize logistics, predict demand fluctuations with greater accuracy, and enhance inventory management, ensuring a more resilient and responsive supply of PETG to global markets.

- Optimization of PETG manufacturing processes through AI-driven predictive analytics, enhancing efficiency and reducing waste.

- Acceleration of research and development for new PETG formulations and grades using machine learning for material property prediction.

- Enhanced supply chain management and logistics for PETG, improving demand forecasting and inventory optimization.

- Improved quality control and defect detection in PETG production via AI-powered vision systems and real-time monitoring.

- Development of sustainable PETG solutions by optimizing energy consumption during synthesis and predicting end-of-life material behavior.

Key Takeaways Polyethylene Terephthalate Glycol Market Size & Forecast

Common user questions about the Polyethylene Terephthalate Glycol (PETG) market size and forecast frequently center on the primary growth drivers, the longevity of its demand, and its resilience against market fluctuations. Users seek clear insights into which sectors are most heavily influencing market expansion, the projected valuation over the forecast period, and the underlying factors contributing to its sustained Compound Annual Growth Rate (CAGR). They are particularly interested in understanding the strategic implications of these forecasts for investment decisions, supply chain planning, and future product development within the PETG industry. The emphasis is on identifying the core elements that will define the market's trajectory through 2033.

The Polyethylene Terephthalate Glycol market is poised for significant expansion, driven by its versatile properties and increasing utility across a spectrum of industries. The forecast period anticipates robust growth, largely fueled by a global shift towards sustainable and high-performance packaging solutions, where PETG offers an advantageous balance of clarity, toughness, and recyclability. The material's adaptability to advanced manufacturing techniques, such as 3D printing, further cements its position as a material of choice for innovation-driven applications, contributing significantly to its projected market size. This upward trend indicates a healthy and expanding market landscape for PETG, underpinned by consistent demand from key end-use sectors.

A critical takeaway from the market forecast is the substantial valuation increase expected by 2033, moving from USD 1.5 Billion in 2025 to USD 2.5 Billion. This growth signifies not only rising volume consumption but also potential premiumization for specialized PETG grades that cater to stringent industry requirements, particularly in the medical and electronics sectors. The consistent CAGR of 6.5% underscores a stable and predictable growth pattern, suggesting that PETG's core value propositions—durability, clarity, and ease of processing—will continue to resonate strongly with manufacturers and consumers. This sustained growth trajectory positions PETG as a key material in the evolving plastics landscape, crucial for companies focused on future-proof material strategies.

- The PETG market is projected for substantial growth, reaching USD 2.5 Billion by 2033 from USD 1.5 Billion in 2025, at a CAGR of 6.5%.

- Strong demand from packaging, medical, and 3D printing industries is a primary growth engine for the market.

- Sustainability initiatives are increasingly favoring PETG due to its recyclability and performance, driving market adoption.

- Innovations in specialized PETG formulations are expanding application areas and enhancing market value.

- The market demonstrates resilience and consistent expansion, making PETG a strategically important material for various industries.

Polyethylene Terephthalate Glycol Market Drivers Analysis

The Polyethylene Terephthalate Glycol (PETG) market is primarily propelled by a confluence of factors, each contributing significantly to its sustained growth. A major driver is the increasing demand for high-performance and aesthetically pleasing plastics across various consumer and industrial applications. PETG's inherent properties, such as excellent clarity, toughness, and chemical resistance, make it a preferred material over traditional plastics like PVC or even some grades of PET, particularly where a combination of these attributes is critical. This versatility allows PETG to penetrate diverse markets, from sophisticated medical devices to everyday consumer packaging, expanding its utility and market share.

Another pivotal driver is the accelerating expansion of the medical and pharmaceutical sectors, which increasingly rely on PETG for its bio-compatibility, ease of sterilization, and strong barrier properties. The material is widely used in medical device housings, laboratory ware, and pharmaceutical packaging, where safety and reliability are paramount. Furthermore, the burgeoning 3D printing industry has adopted PETG as a filament of choice due to its excellent printability, minimal warping, and good layer adhesion, catering to the growing demand for rapid prototyping and custom manufacturing across various industries. These sector-specific demands create a robust and consistent pull for PETG materials.

Lastly, the global shift towards more sustainable and recyclable packaging solutions significantly bolsters the PETG market. As environmental regulations tighten and consumer preferences lean towards eco-friendlier options, PETG offers an attractive alternative due to its recyclability and lower environmental impact compared to certain other plastics. Its ability to be thermoformed and processed efficiently also contributes to reduced energy consumption during manufacturing, aligning with broader sustainability goals. This combination of superior material properties, expanding application bases, and environmental advantages collectively drives the PETG market forward.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Sustainable Packaging | +1.5% | North America, Europe, Asia Pacific | 2025-2033 |

| Expansion of Medical & Pharmaceutical Sector | +1.2% | Global, particularly North America, Europe | 2025-2033 |

| Rising Adoption in 3D Printing & Additive Manufacturing | +1.0% | Global, particularly developed economies | 2025-2033 |

| Preference for High-Clarity and Durable Materials | +0.8% | Global | 2025-2033 |

| Technological Advancements in PETG Formulations | +0.5% | Global | 2027-2033 |

Polyethylene Terephthalate Glycol Market Restraints Analysis

Despite its robust growth potential, the Polyethylene Terephthalate Glycol (PETG) market faces several restraints that could temper its expansion. One of the primary concerns is the volatility in raw material prices. PETG is derived from monomers such as terephthalic acid (PTA) and ethylene glycol (EG), whose prices are often influenced by crude oil fluctuations, global supply-demand dynamics, and geopolitical events. Such price instability can directly impact production costs, squeezing profit margins for manufacturers and potentially leading to higher end-product prices, which may deter some price-sensitive buyers or encourage the search for more cost-effective alternatives.

Another significant restraint is the intense competition from alternative polymers. The plastics market is highly competitive, with a wide array of materials offering similar or complementary properties. Polymers such as Polycarbonate (PC), Polymethyl Methacrylate (PMMA), and even standard Polyethylene Terephthalate (PET) pose a competitive challenge to PETG in various applications. While PETG offers unique advantages, particularly its balance of clarity and toughness, other materials might be favored based on specific cost, performance, or regulatory requirements, thereby limiting PETG’s market penetration in certain segments. This constant competition necessitates continuous innovation and cost-efficiency from PETG producers.

Furthermore, the environmental perception and regulatory landscape, despite PETG’s relatively favorable profile compared to some plastics, can act as a restraint. While PETG is recyclable, the infrastructure for its recycling is not as widespread or developed as for commodity plastics like PET. Concerns over plastic waste and microplastics globally can lead to stricter regulations on plastic usage, production, or disposal, which might indirectly affect the growth trajectory of PETG if not properly managed or if more robust recycling solutions are not universally adopted. The ongoing debate around single-use plastics also presents a challenge, pushing industries to explore even more sustainable or reusable material alternatives.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Raw Material Prices | -0.8% | Global | 2025-2033 |

| Competition from Alternative Polymers | -0.7% | Global | 2025-2033 |

| Limited Recycling Infrastructure for PETG | -0.5% | Emerging Economies, parts of North America | 2025-2030 |

| Strict Environmental Regulations on Plastics | -0.4% | Europe, parts of North America | 2027-2033 |

Polyethylene Terephthalate Glycol Market Opportunities Analysis

The Polyethylene Terephthalate Glycol (PETG) market is ripe with opportunities that can significantly accelerate its growth trajectory. One notable avenue lies in the continuous innovation of bio-based PETG formulations. As global pressure mounts to reduce reliance on fossil fuels and mitigate carbon emissions, the development and commercialization of PETG partly or wholly derived from renewable resources present a massive opportunity. Such advancements would not only align with stringent environmental regulations but also cater to a growing consumer base actively seeking sustainable products, thereby opening new markets and enhancing brand appeal for PETG-based applications.

Furthermore, the expansion into emerging economies represents a substantial growth opportunity. Countries in Asia Pacific, Latin America, and the Middle East and Africa are experiencing rapid industrialization, urbanization, and increasing disposable incomes. This leads to higher demand for packaged goods, medical supplies, and consumer products where PETG excels. As these regions develop their manufacturing capabilities and adopt more sophisticated materials, PETG producers can capitalize on these burgeoning markets by establishing local production facilities, forging strategic partnerships, and tailoring products to regional needs. The untapped potential in these regions offers long-term growth prospects.

Another key opportunity lies in the development of specialized PETG grades for high-end and niche applications. This includes enhancing properties such as chemical resistance for harsh industrial environments, improving UV stability for outdoor applications, or optimizing barrier properties for sensitive food and pharmaceutical packaging. By offering tailor-made solutions, manufacturers can command premium prices and establish strong positions in specific market segments where standard PETG might not fully meet the requirements. This strategic focus on differentiation and value-added products ensures PETG remains competitive and relevant in an evolving material science landscape.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bio-based PETG Formulations | +1.3% | Global, particularly Europe, North America | 2026-2033 |

| Expansion into Emerging Economies | +1.1% | Asia Pacific, Latin America, MEA | 2025-2033 |

| Innovation in High-Performance & Specialized Grades | +0.9% | Global | 2025-2033 |

| Increasing Demand for Custom Manufacturing (3D Printing) | +0.7% | Developed Economies | 2025-2033 |

| Circular Economy Initiatives and Enhanced Recycling | +0.6% | Europe, North America | 2028-2033 |

Polyethylene Terephthalate Glycol Market Challenges Impact Analysis

The Polyethylene Terephthalate Glycol (PETG) market, while promising, is not without its challenges that require strategic navigation. A significant challenge lies in managing the supply chain volatility for key raw materials. Geopolitical tensions, trade disputes, natural disasters, or unexpected shutdowns of major production facilities can disrupt the supply of terephthalic acid and ethylene glycol, leading to price spikes and shortages. Such disruptions can severely impact production schedules, increase operational costs, and force manufacturers to seek alternative, potentially less efficient, sourcing channels, thus undermining market stability and profitability for PETG producers.

Another considerable challenge is the intense competition from a diverse range of existing and emerging plastic materials. The market for transparent and durable plastics is crowded, with materials like polycarbonate, acrylic, and even specialized grades of PET continuously evolving and vying for market share. While PETG offers a unique balance of properties, manufacturers must constantly innovate and differentiate their products to justify its cost and performance advantages. The pressure to remain competitive in terms of both price and performance against these alternatives necessitates continuous investment in research and development, which can be a financial strain, particularly for smaller market players.

Furthermore, evolving environmental regulations and consumer perceptions regarding plastic waste present a multifaceted challenge. Despite PETG's recyclability, the broader public and regulatory focus on reducing plastic consumption and improving recycling rates for all plastics can negatively impact demand if not adequately addressed. The industry faces the challenge of educating consumers and policymakers about PETG's specific environmental benefits and ensuring robust recycling infrastructure is in place. Failure to effectively communicate these aspects or adapt to stricter regulations could lead to market access restrictions or reduced adoption, particularly in regions with strong anti-plastic sentiments or highly developed circular economy policies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions & Raw Material Volatility | -0.9% | Global | 2025-2029 |

| Intense Competition from Alternative Plastics | -0.7% | Global | 2025-2033 |

| Evolving Environmental Regulations & Public Perception | -0.6% | Europe, North America | 2026-2033 |

| High Initial Investment for Production & Processing | -0.4% | Emerging Economies | 2025-2030 |

Polyethylene Terephthalate Glycol Market - Updated Report Scope

This comprehensive market report delves into the intricate dynamics of the Polyethylene Terephthalate Glycol (PETG) market, providing a detailed analysis of its size, growth drivers, restraints, opportunities, and challenges across various segments and geographic regions. The report offers an updated perspective on market trends, competitive landscape, and the impact of technological advancements, including Artificial Intelligence, shaping the industry's future. It aims to equip stakeholders with critical insights to make informed strategic decisions and capitalize on emerging market prospects, ensuring a thorough understanding of PETG's evolving role in diverse end-use applications.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.5 Billion |

| Market Forecast in 2033 | USD 2.5 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Eastman Chemical Company, SK Chemicals, Lotte Chemical Corporation, Jiangsu Sanfangxiang Group Co., Ltd., Zhongfu Industrial Co., Ltd., Covestro AG, Avient Corporation, Simona AG, FormFutura, Colorfabb, Mitsubishi Chemical Corporation, BASF SE, SABIC, Evonik Industries AG, The Dow Chemical Company |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Polyethylene Terephthalate Glycol (PETG) market is comprehensively segmented to provide granular insights into its diverse applications and material types. This segmentation allows for a detailed understanding of market dynamics within specific product categories and end-use industries, enabling stakeholders to identify high-growth areas and tailor their strategies accordingly. The primary segmentation criteria typically include the type of PETG resin, its various applications across different sectors, and the specific end-use industries that leverage PETG for their products, reflecting the material's broad utility and adaptability.

Segmentation by type often distinguishes between extrusion grade, injection molding grade, and film grade PETG, each optimized for different processing methods and final product characteristics. This distinction is crucial as it highlights the specialized requirements of various manufacturing processes. For instance, extrusion grades are critical for sheets and films, while injection molding grades are preferred for intricate parts and components, showcasing the engineering versatility of PETG. Understanding these distinctions is vital for both producers in formulating the right product and consumers in selecting the optimal material.

Further, application-based segmentation provides clarity on how PETG is utilized across sectors such as packaging (food, medical, cosmetics), consumer goods, and the rapidly expanding 3D printing industry. Each application leverages specific properties of PETG, such as its clarity and toughness in packaging or its printability in additive manufacturing. Concurrently, end-use industry segmentation, encompassing healthcare, automotive, and electronics, offers an overview of the broader industrial ecosystems where PETG plays a crucial role. This multi-layered segmentation is instrumental for a thorough market analysis, revealing specific demand patterns and future growth opportunities within the PETG landscape.

- By Type: Extrusion Grade, Injection Molding Grade, Film Grade, Others

- By Application: Packaging (Food & Beverage, Medical & Pharmaceutical, Cosmetics & Personal Care, Industrial), Consumer Goods, Medical & Healthcare, Electronics, Automotive, Building & Construction, 3D Printing Filaments, Others

- By End-Use Industry: Healthcare, Food & Beverage, Consumer Durables, Automotive, Construction, Electronics, 3D Printing, Others

Regional Highlights

- North America: This region represents a mature yet continually growing market for Polyethylene Terephthalate Glycol, driven by strong demand from the medical, pharmaceutical, and consumer goods packaging sectors. The presence of key market players, advanced manufacturing capabilities, and a focus on high-performance plastics contribute to its significant market share. Innovations in sustainable packaging and the robust growth of 3D printing applications also propel PETG adoption.

- Europe: Characterized by stringent environmental regulations and a strong emphasis on the circular economy, Europe is a pivotal market for PETG, especially due to its recyclability and low-VOC properties. The region sees high demand from the food and beverage packaging industry, as well as the medical and automotive sectors, where clarity, chemical resistance, and durability are highly valued.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region for the PETG market, fueled by rapid industrialization, increasing disposable incomes, and the expansion of manufacturing bases in countries like China, India, Japan, and South Korea. The escalating demand for consumer electronics, packaged food, and healthcare products, coupled with significant investments in infrastructure development, drives the adoption of PETG across diverse applications.

- Latin America: The market in Latin America is witnessing steady growth, primarily driven by the expanding packaging industry and increasing investments in healthcare infrastructure. Countries like Brazil and Mexico are leading the adoption of PETG due to growing consumer awareness of product quality and rising demand for safe and durable materials in various sectors.

- Middle East and Africa (MEA): This region is an emerging market for PETG, with growth attributed to economic diversification efforts, increasing construction activities, and the nascent but expanding packaging industry. Investments in healthcare and consumer goods manufacturing are creating new opportunities for PETG, though market penetration is still in its early stages compared to more developed regions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Polyethylene Terephthalate Glycol Market.- Eastman Chemical Company

- SK Chemicals

- Lotte Chemical Corporation

- Jiangsu Sanfangxiang Group Co., Ltd.

- Zhongfu Industrial Co., Ltd.

- Covestro AG

- Avient Corporation

- Simona AG

- FormFutura

- Colorfabb

- Mitsubishi Chemical Corporation

- BASF SE

- SABIC

- Evonik Industries AG

- The Dow Chemical Company

Frequently Asked Questions

What is Polyethylene Terephthalate Glycol (PETG)?

Polyethylene Terephthalate Glycol (PETG) is a thermoplastic polyester that offers an excellent balance of properties, including clarity, toughness, chemical resistance, and ease of thermoforming. It is a modified version of polyethylene terephthalate (PET), where glycol is added to prevent crystallization and make the material amorphous, enhancing its clarity and making it easier to work with.

What are the primary applications of PETG?

PETG is widely used across various industries due to its versatility. Primary applications include packaging (food & beverage, medical, cosmetics), medical device components, consumer goods, point-of-purchase displays, signage, and increasingly, as a filament for 3D printing and additive manufacturing due to its excellent printability and durability.

How does PETG compare to PET and PC?

PETG offers a unique blend of properties distinct from PET and Polycarbonate (PC). Compared to PET, PETG is typically more impact-resistant, less brittle, and easier to thermoform. Compared to PC, PETG provides similar toughness and clarity but is generally easier to process, has better chemical resistance, and is often a more cost-effective alternative for certain applications, while also being more widely recyclable than PC.

Is PETG considered a sustainable material?

PETG is considered a relatively sustainable material within the plastics family. It is 100% recyclable, often compatible with existing PET recycling streams, and does not contain BPA or other hazardous chemicals. Furthermore, innovations are leading to the development of bio-based PETG formulations, further enhancing its environmental profile and aligning with circular economy principles.

What are the future growth prospects for the PETG market?

The PETG market is projected for robust future growth, driven by expanding applications in sustainable packaging, increased demand from the healthcare and 3D printing sectors, and continuous advancements in material science. Its favorable properties, coupled with efforts towards bio-based formulations and improved recycling infrastructure, are expected to ensure sustained market expansion through 2033 and beyond.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted