Polyacrylonitrile Market

Polyacrylonitrile Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706515 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

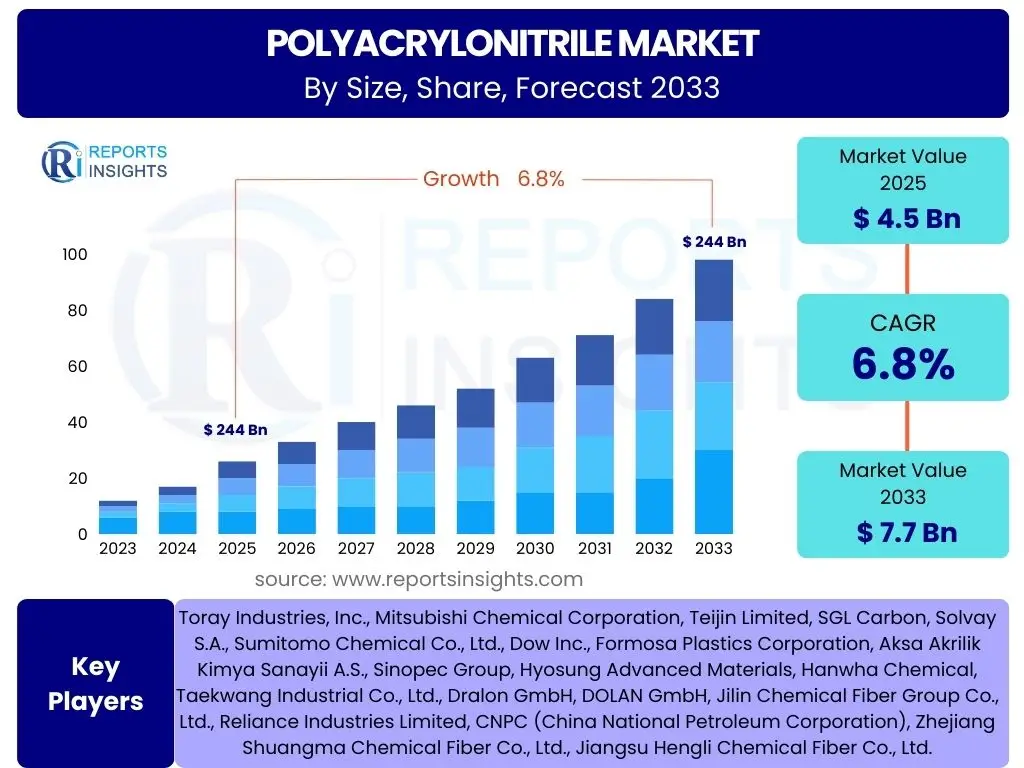

Polyacrylonitrile Market Size

According to Reports Insights Consulting Pvt Ltd, The Polyacrylonitrile Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 4.5 billion in 2025 and is projected to reach USD 7.7 billion by the end of the forecast period in 2033.

Key Polyacrylonitrile Market Trends & Insights

The Polyacrylonitrile (PAN) market is witnessing a significant transformation driven by evolving industrial demands and technological advancements. A primary trend is the escalating demand for PAN as a precursor in carbon fiber manufacturing, which is crucial for lightweighting in aerospace, automotive, and renewable energy sectors. This application is shifting the market focus from traditional textile uses to high-performance composite materials, requiring PAN with superior mechanical properties and purity.

Another key insight involves the growing emphasis on sustainability and circular economy principles within the PAN industry. There is increasing investment in research and development for bio-based PAN production, which aims to reduce reliance on fossil resources and lower the carbon footprint of PAN manufacturing. Furthermore, advancements in recycling technologies for carbon fiber and other PAN-based materials are gaining traction, addressing environmental concerns and promoting resource efficiency across the value chain.

Emerging applications in advanced filtration systems, medical devices, and energy storage solutions are also shaping market dynamics. The unique properties of PAN, such as its chemical resistance, thermal stability, and membrane-forming capabilities, make it ideal for these specialized uses. Innovation in polymerization techniques and fiber spinning processes is leading to new forms of PAN with enhanced functionalities, further broadening its application spectrum and driving market growth in niche segments globally.

- Increasing demand for carbon fiber precursors across aerospace, automotive, and wind energy sectors.

- Growing focus on sustainable and bio-based Polyacrylonitrile production methods.

- Technological advancements in filtration and membrane applications.

- Expansion into specialized textile markets requiring high-performance fibers.

- Rising adoption of Polyacrylonitrile in energy storage devices and medical applications.

- Development of advanced recycling technologies for Polyacrylonitrile-based products.

- Shift towards lightweight and high-strength materials in industrial applications.

AI Impact Analysis on Polyacrylonitrile

Artificial Intelligence (AI) is set to significantly revolutionize the Polyacrylonitrile (PAN) industry by optimizing complex manufacturing processes and enhancing material properties. AI-driven predictive modeling can fine-tune polymerization conditions, such as temperature, pressure, and catalyst concentrations, to achieve desired molecular weights and distributions, leading to improved fiber quality, reduced waste, and increased production yields. This optimization translates into substantial cost savings and operational efficiency for PAN manufacturers.

Furthermore, AI accelerates research and development efforts in discovering novel PAN derivatives and advanced composite materials. Machine learning algorithms can analyze vast datasets of material properties, experimental results, and molecular structures to predict the performance of new PAN formulations without extensive physical testing. This capability shortens development cycles, fostering innovation in applications such as advanced filtration membranes, high-performance textiles, and next-generation carbon fibers.

In terms of supply chain and operational management, AI implementation offers predictive maintenance solutions for machinery, minimizing downtime and extending equipment lifespan. AI-powered analytics can also optimize raw material procurement, inventory management, and logistics, ensuring a more resilient and efficient supply chain. The integration of AI tools promises to drive productivity, enhance product quality, and open new avenues for application and market expansion within the Polyacrylonitrile sector.

- Process optimization and yield enhancement in Polyacrylonitrile polymerization.

- Predictive maintenance for manufacturing equipment, reducing downtime.

- Accelerated research and development for new Polyacrylonitrile derivatives and applications.

- Improved quality control and consistency of Polyacrylonitrile fibers and resins.

- Enhanced supply chain management and logistics efficiency.

- Data-driven insights for market analysis and strategic decision-making.

- Development of smart materials incorporating Polyacrylonitrile.

Key Takeaways Polyacrylonitrile Market Size & Forecast

The Polyacrylonitrile (PAN) market is projected for robust growth, primarily driven by its indispensable role as a precursor for carbon fiber. This expansion is intrinsically linked to the increasing global demand for lightweight, high-strength materials across critical sectors such as aerospace, automotive, and wind energy. The inherent properties of carbon fibers derived from PAN offer significant performance advantages, positioning PAN as a cornerstone material for future industrial advancements and sustainable solutions.

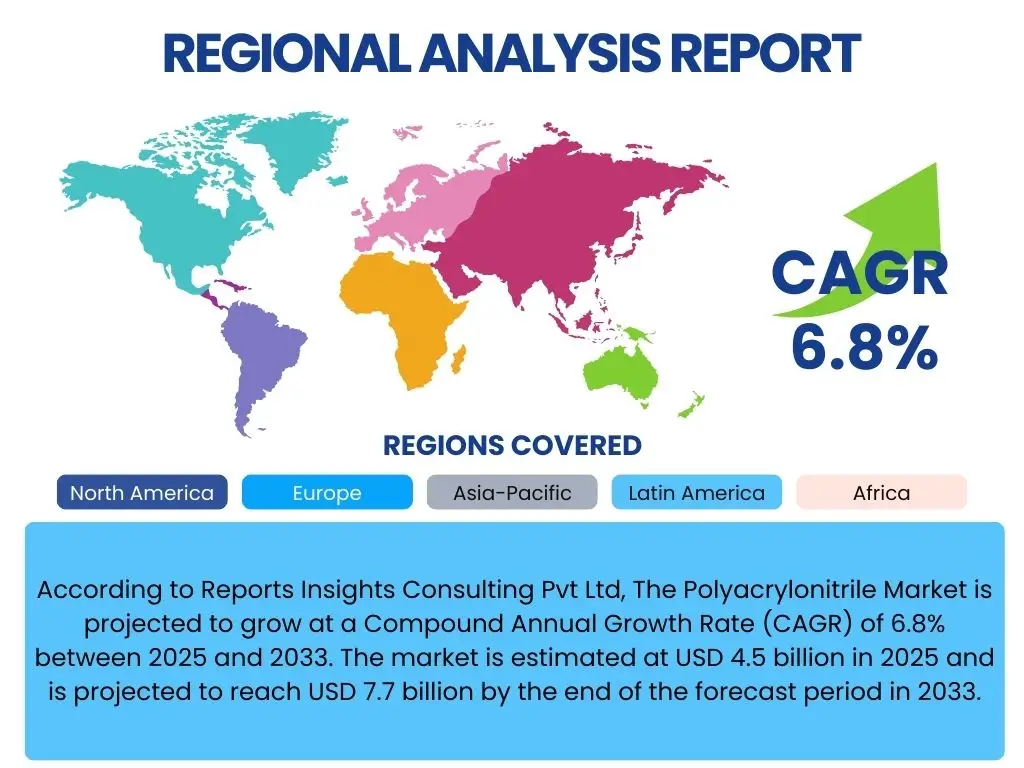

Geographically, the Asia Pacific region is expected to maintain its dominance and exhibit the fastest growth, fueled by rapid industrialization, expanding manufacturing capacities, and substantial infrastructure development. Countries like China, India, and Japan are at the forefront of adopting advanced materials in their burgeoning automotive and construction sectors, as well as investing heavily in renewable energy projects, all of which contribute significantly to PAN demand. This regional leadership is also supported by a strong presence of key PAN manufacturers and downstream processing industries.

Looking ahead, diversification into new high-value applications beyond traditional textiles will be crucial for sustaining market momentum. Opportunities in advanced filtration, medical devices, and innovative energy storage solutions are emerging as significant growth avenues. Furthermore, a growing emphasis on sustainability, including the development of bio-based PAN and advanced recycling technologies, is becoming a key differentiator, influencing investment decisions and shaping long-term market trends in the global Polyacrylonitrile industry.

- Significant Compound Annual Growth Rate (CAGR) driven by carbon fiber demand.

- Polyacrylonitrile is a critical precursor for lightweight materials in aerospace and automotive.

- Asia Pacific region leads in market share and growth due to industrial expansion.

- Increasing strategic focus on sustainability and bio-based Polyacrylonitrile alternatives.

- Emerging applications in water treatment, medical, and energy storage provide new growth avenues.

- Technological advancements are enhancing Polyacrylonitrile performance and processing efficiency.

Polyacrylonitrile Market Drivers Analysis

The Polyacrylonitrile (PAN) market is propelled by a confluence of factors, with the surging demand for carbon fiber precursors standing out as a primary catalyst. Carbon fiber’s exceptional strength-to-weight ratio and rigidity make it indispensable in industries striving for fuel efficiency and performance enhancement. As aerospace, automotive, and wind energy sectors continue to expand and innovate, their reliance on carbon fiber directly translates into increased demand for high-quality PAN.

Beyond carbon fiber, the growing global focus on environmental protection and resource efficiency is driving the adoption of PAN in water treatment and filtration applications. PAN-based membranes offer superior filtration capabilities, addressing the increasing need for clean water and industrial wastewater treatment across various regions. This environmental imperative, coupled with rapid urbanization and industrial growth, particularly in developing economies, is fueling market expansion.

Furthermore, advancements in specialized textile manufacturing and the continuous pursuit of high-performance materials in diverse end-use industries contribute significantly to market growth. From outdoor apparel requiring lightweight and durable fibers to advanced composites for infrastructure, the versatility and performance characteristics of PAN fibers position them favorably against traditional materials, ensuring sustained demand and opening new market segments.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for carbon fiber precursors in aerospace, automotive, and wind energy sectors. | +2.5% | Global, particularly North America, Europe, Asia Pacific (China, Japan) | Mid to Long-term (2025-2033) |

| Expansion of water treatment and industrial filtration industries globally. | +1.8% | Asia Pacific, Latin America, Middle East & Africa | Short to Mid-term (2025-2029) |

| Increasing adoption in specialized textiles and high-performance apparel. | +1.2% | Europe, North America, Asia Pacific (South Korea, Japan) | Mid-term (2027-2033) |

| Rising investments in research and development for new Polyacrylonitrile applications (e.g., energy storage, medical). | +1.0% | Global, primarily developed economies (US, Germany, Japan) | Long-term (2030-2033) |

Polyacrylonitrile Market Restraints Analysis

Despite its significant growth prospects, the Polyacrylonitrile (PAN) market faces several restraints that could impede its expansion. A primary concern is the volatility in the prices of acrylonitrile monomer, the key raw material for PAN production. Acrylonitrile prices are often influenced by the fluctuating costs of crude oil and natural gas, as well as supply-demand imbalances in the petrochemical industry. Such price instability directly impacts the production costs of PAN, potentially eroding profit margins for manufacturers and affecting the overall market stability.

Furthermore, stringent environmental regulations and growing concerns regarding the environmental footprint of chemical production pose significant challenges. The manufacturing process of PAN can be energy-intensive and may involve the use of hazardous chemicals. Increasing regulatory scrutiny, particularly in regions like Europe and North America, necessitates significant investments in cleaner production technologies and waste management systems, which can add to operational costs and limit market entry for new players.

Competition from alternative materials also acts as a restraint. While PAN is uniquely positioned for carbon fiber precursors, other materials like aramid fibers, glass fibers, and advanced polymers offer competitive performance in specific applications. Continuous innovation in these substitute materials could divert demand from PAN-based products, especially in cost-sensitive segments. Additionally, the high initial capital investment required for establishing new PAN production facilities can be a barrier, particularly in emerging markets, slowing down capacity expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in acrylonitrile monomer prices and raw material supply chain disruptions. | -1.5% | Global, with acute impact on regions dependent on imports (e.g., Europe, Asia Pacific). | Ongoing, Short to Mid-term (2025-2028) |

| Strict environmental regulations and concerns over the ecological impact of production. | -1.0% | Europe, North America, increasingly Asia Pacific. | Mid to Long-term (2026-2033) |

| Competition from alternative high-performance fibers and composite materials. | -0.8% | Global, particularly in industrial and automotive applications. | Ongoing |

| High initial capital investment required for establishing Polyacrylonitrile manufacturing facilities. | -0.7% | Developing regions, new market entrants. | Short to Mid-term (2025-2029) |

Polyacrylonitrile Market Opportunities Analysis

The Polyacrylonitrile (PAN) market is poised for significant growth through various emerging opportunities. A substantial opportunity lies in the development and commercialization of bio-based and sustainable PAN. As global industries increasingly prioritize eco-friendly solutions, research into renewable feedstocks for acrylonitrile and greener polymerization processes for PAN offers a pathway to reduce environmental impact and meet evolving regulatory and consumer demands, potentially unlocking new market segments and attracting environmentally conscious investors.

Furthermore, the rapid expansion of energy storage solutions, particularly in the realm of batteries and supercapacitors, presents a promising avenue for PAN. PAN-based materials are being explored for their potential as binders, separators, and even as active materials in advanced battery technologies due to their thermal stability and electrochemical properties. This application area aligns with the global shift towards electric vehicles and renewable energy integration, offering a substantial long-term growth trajectory for the PAN market.

Advancements in recycling technologies for PAN and PAN-derived products, especially carbon fibers, represent another critical opportunity. Developing efficient and economically viable methods to reclaim valuable PAN from waste streams or end-of-life products can not only reduce waste and environmental pollution but also create a circular economy model, enhancing resource security and cost-effectiveness for manufacturers. Additionally, the exploration of PAN in medical and pharmaceutical applications, such as specialized membranes for dialysis or drug delivery systems, highlights its potential in high-value, niche markets that demand high purity and biocompatibility.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and commercialization of bio-based and sustainable Polyacrylonitrile. | +2.0% | Europe, North America, Asia Pacific (Japan, South Korea) | Mid to Long-term (2027-2033) |

| Growing demand for Polyacrylonitrile in energy storage solutions (batteries, supercapacitors). | +1.5% | Asia Pacific (China, South Korea), North America, Europe | Mid to Long-term (2026-2033) |

| Advancements in Polyacrylonitrile and carbon fiber recycling technologies. | +1.0% | Europe, North America, Japan | Long-term (2029-2033) |

| Expansion into high-value medical and pharmaceutical applications. | +0.8% | Global, particularly developed healthcare markets. | Mid-term (2027-2032) |

Polyacrylonitrile Market Challenges Impact Analysis

The Polyacrylonitrile (PAN) market encounters several significant challenges that necessitate strategic navigation for sustained growth. One primary challenge is the inherent complexity and energy-intensive nature of PAN manufacturing processes. The polymerization of acrylonitrile and subsequent spinning of fibers require precise control over numerous parameters and consume substantial energy, leading to high operational costs. This can particularly impact profitability and competitiveness, especially for manufacturers operating in regions with high energy prices.

Another hurdle is the increasingly stringent regulatory landscape governing chemical production and environmental emissions. PAN manufacturers must comply with evolving environmental protection laws related to air and water pollution, waste disposal, and the handling of hazardous substances. Meeting these regulations often requires significant capital investment in advanced abatement technologies and continuous monitoring, which adds to the cost burden and can slow down capacity expansions or the introduction of new products.

Furthermore, the market faces challenges related to intellectual property (IP) and patent disputes. The specialized nature of PAN production, particularly for carbon fiber precursors, often involves proprietary technologies and processes. This can lead to complex and costly legal battles over patent infringement, restricting market entry for new players and creating uncertainty for existing ones. Additionally, maintaining a resilient and secure supply chain for acrylonitrile monomer, which can be vulnerable to geopolitical tensions or natural disasters, poses an ongoing operational challenge that could impact production stability and pricing across the global PAN market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex and energy-intensive manufacturing processes. | -1.2% | Global, impacts all major production hubs. | Ongoing |

| Stringent regulatory landscape for chemical production and environmental compliance. | -0.9% | Europe, North America, increasingly Asia Pacific. | Ongoing |

| Intellectual property and patent disputes related to Polyacrylonitrile technology. | -0.6% | Global, particularly in high-tech carbon fiber markets. | Ongoing |

| Supply chain disruptions and geopolitical risks affecting raw material availability. | -0.5% | Global, with varied regional impact based on import reliance. | Short-term (2025-2027) |

Polyacrylonitrile Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Polyacrylonitrile market, encompassing historical data, current market dynamics, and future growth projections. It offers a detailed examination of market size, trends, drivers, restraints, opportunities, and challenges affecting the industry. The report segments the market by form, application, and end-use industry, providing granular insights into key segments. Furthermore, it includes a thorough regional analysis and profiles of leading market participants, delivering strategic insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.5 billion |

| Market Forecast in 2033 | USD 7.7 billion |

| Growth Rate | 6.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Toray Industries, Inc., Mitsubishi Chemical Corporation, Teijin Limited, SGL Carbon, Solvay S.A., Sumitomo Chemical Co., Ltd., Dow Inc., Formosa Plastics Corporation, Aksa Akrilik Kimya Sanayii A.S., Sinopec Group, Hyosung Advanced Materials, Hanwha Chemical, Taekwang Industrial Co., Ltd., Dralon GmbH, DOLAN GmbH, Jilin Chemical Fiber Group Co., Ltd., Reliance Industries Limited, CNPC (China National Petroleum Corporation), Zhejiang Shuangma Chemical Fiber Co., Ltd., Jiangsu Hengli Chemical Fiber Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Polyacrylonitrile (PAN) market is extensively segmented to provide a detailed understanding of its diverse applications and forms. This segmentation allows for granular analysis of market dynamics, identifying specific growth drivers and opportunities within each category. The market is primarily bifurcated by its physical form, its various end-use applications, and the industries it serves, reflecting the versatility and adaptability of PAN across a wide range of sectors.

Segmentation by form typically includes fiber, powder, and solution, each catering to distinct manufacturing processes and product requirements. For instance, PAN fiber is predominantly used as a carbon fiber precursor, while PAN powder might find applications in specialized additives or coatings. The application-based segmentation delves into specific end-products or functions, such as textiles, filtration media, and carbon fiber precursors, highlighting the core functionalities PAN provides.

Further, segmenting by end-use industry, such as aerospace & defense, automotive, energy, and water treatment, reveals how different economic sectors leverage PAN for their unique material needs. This comprehensive segmentation provides a holistic view of the market landscape, enabling stakeholders to identify high-growth areas, understand competitive dynamics, and formulate targeted business strategies to capitalize on emerging trends.

- By Form:

- Fiber

- Powder

- Solution

- By Application:

- Carbon Fiber Precursors

- Textiles (Acrylic Fibers)

- Filtration Media (e.g., hot gas filtration, water treatment)

- Outdoor and Apparel

- Medical Devices (e.g., membranes for dialysis)

- Other Applications (e.g., energy storage, concrete reinforcement)

- By End-use Industry:

- Aerospace & Defense

- Automotive

- Energy (Wind Turbines, Fuel Cells, Solar)

- Construction

- General Industrial

- Water Treatment & Purification

- Medical & Healthcare

- Sports & Leisure

Regional Highlights

- Asia Pacific: The largest and fastest-growing market for Polyacrylonitrile, primarily driven by robust industrialization, expanding manufacturing base, and increasing investments in infrastructure and renewable energy sectors, particularly in China, India, Japan, and South Korea. The region's dominance is also supported by a significant automotive industry and a strong focus on carbon fiber production for various applications.

- North America: A mature market characterized by significant demand from the aerospace and defense sectors, advanced automotive manufacturing, and a strong emphasis on research and development for high-performance materials. Investments in lightweight vehicle technologies and sustainable solutions are key drivers in this region.

- Europe: Exhibits steady growth fueled by stringent environmental regulations driving demand for filtration solutions and a strong focus on advanced materials for the automotive, aerospace, and renewable energy industries. Innovation in sustainable and recycled Polyacrylonitrile also plays a crucial role in the European market.

- Latin America: An emerging market with potential growth stemming from developing industrial sectors, increasing infrastructure projects, and a growing textile industry. Brazil and Mexico are key contributors to the region's Polyacrylonitrile demand.

- Middle East and Africa (MEA): Shows promising growth due to ongoing industrialization, diversification of economies away from oil, and increasing investments in water treatment facilities and infrastructure development. The textile industry in some parts of Africa also contributes to market demand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Polyacrylonitrile Market.

- Toray Industries, Inc.

- Mitsubishi Chemical Corporation

- Teijin Limited

- SGL Carbon

- Solvay S.A.

- Sumitomo Chemical Co., Ltd.

- Dow Inc.

- Formosa Plastics Corporation

- Aksa Akrilik Kimya Sanayii A.S.

- Sinopec Group

- Hyosung Advanced Materials

- Hanwha Chemical

- Taekwang Industrial Co., Ltd.

- Dralon GmbH

- DOLAN GmbH

- Jilin Chemical Fiber Group Co., Ltd.

- Reliance Industries Limited

- CNPC (China National Petroleum Corporation)

- Zhejiang Shuangma Chemical Fiber Co., Ltd.

- Jiangsu Hengli Chemical Fiber Co., Ltd.

Frequently Asked Questions

What is Polyacrylonitrile (PAN)?

Polyacrylonitrile (PAN) is a synthetic, semi-crystalline organic polymer resin predominantly used as a precursor to carbon fiber. It is a versatile polymer known for its high strength, rigidity, thermal stability, and chemical resistance. Besides carbon fiber production, it is also utilized in various forms such as textiles (acrylic fibers), filtration media, and specialized materials.

What are the primary applications of Polyacrylonitrile?

The primary application of Polyacrylonitrile is as a precursor for carbon fiber, which is extensively used in aerospace, automotive, and wind energy sectors due to its lightweight and high-strength properties. Other significant applications include acrylic fibers for textiles and apparel, filtration media for industrial and water treatment, and increasingly, in emerging fields like energy storage solutions and medical devices for membranes and specialized components.

What is the projected growth of the Polyacrylonitrile market?

The Polyacrylonitrile market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. It is estimated to reach USD 7.7 billion by the end of 2033, up from USD 4.5 billion in 2025. This growth is primarily fueled by the surging global demand for carbon fiber and expanding applications in high-performance materials across diverse industries.

Which factors are driving the Polyacrylonitrile market?

Key drivers for the Polyacrylonitrile market include the rapidly increasing demand for carbon fiber precursors from the aerospace, automotive, and wind energy industries, driven by the need for lightweight and strong materials. Additionally, growth in water treatment and filtration applications, expanding use in specialized textiles, and rising investments in research for new applications like energy storage significantly contribute to market expansion.

What are the key challenges facing the Polyacrylonitrile industry?

The Polyacrylonitrile industry faces several challenges, including the volatility of acrylonitrile monomer prices, which directly impacts production costs. Stringent environmental regulations and the energy-intensive nature of PAN manufacturing processes pose compliance and operational cost challenges. Furthermore, competition from alternative materials and potential intellectual property disputes in advanced applications also represent significant hurdles for market players.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted