Plastic to Fuel Technology Market

Plastic to Fuel Technology Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701209 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

Plastic to Fuel Technology Market Size

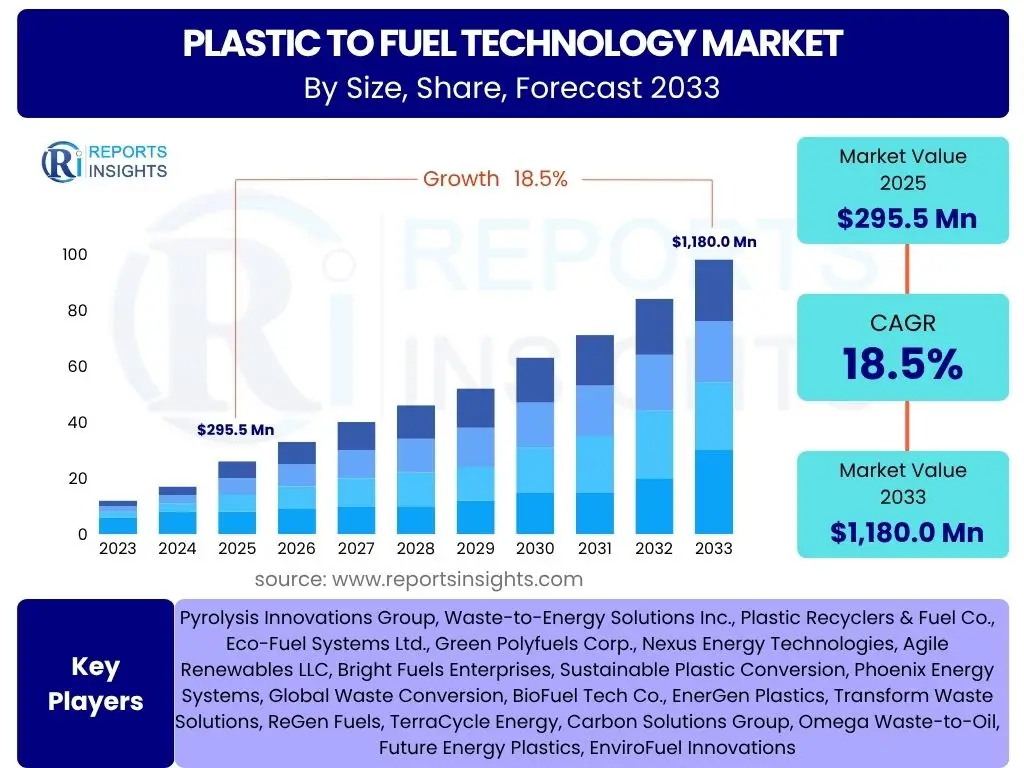

According to Reports Insights Consulting Pvt Ltd, The Plastic to Fuel Technology Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 295.5 Million in 2025 and is projected to reach USD 1,180.0 Million by the end of the forecast period in 2033.

Key Plastic to Fuel Technology Market Trends & Insights

The Plastic to Fuel Technology market is witnessing a profound transformation driven by global imperatives for sustainable waste management and energy security. A primary trend involves the increasing adoption of advanced pyrolysis and gasification technologies, which offer higher conversion efficiencies and produce more refined fuel products. These technological advancements are pivotal in addressing the historical challenges of yield and quality, making the process more economically viable and environmentally sound. Furthermore, there is a growing emphasis on modular and decentralized plastic-to-fuel plants, enabling local waste processing and reducing transportation costs, which is particularly attractive for municipalities and remote industrial sites aiming to manage plastic waste streams effectively.

Another significant insight points to the burgeoning integration of plastic-to-fuel solutions within the broader circular economy framework. Rather than solely viewing plastic waste as a disposal problem, industries are increasingly recognizing its value as a renewable feedstock. This paradigm shift is encouraging collaborations between waste management companies, technology providers, and end-users of the derived fuels, fostering a closed-loop system where plastic waste is diverted from landfills and oceans to create valuable energy resources. Policy support, including regulations promoting waste reduction and renewable energy adoption, is further accelerating these trends, creating a conducive environment for market expansion and innovation in diverse geographical regions.

- Technological advancements in pyrolysis and gasification increasing conversion efficiency and fuel quality.

- Development and deployment of modular, scalable, and decentralized plastic-to-fuel units.

- Growing integration of plastic-to-fuel processes into circular economy models.

- Increasing strategic partnerships across the waste management and energy sectors.

- Rising investment in research and development to optimize catalysts and refine fuel products.

- Shifting focus towards processing difficult-to-recycle and mixed plastic waste streams.

- Emergence of carbon capture and utilization technologies alongside plastic-to-fuel processes.

AI Impact Analysis on Plastic to Fuel Technology

Artificial Intelligence (AI) is poised to revolutionize the Plastic to Fuel Technology sector by enhancing operational efficiency, optimizing processes, and improving overall economic viability. Users frequently inquire about AI's potential to fine-tune reaction parameters, predict equipment failures, and manage feedstock variability. AI-driven systems can analyze vast datasets from plant operations, including temperature, pressure, and feedstock composition, to dynamically adjust parameters for maximum fuel yield and quality. This predictive capability minimizes downtime, reduces energy consumption, and ensures consistent product output, addressing key concerns regarding the scalability and profitability of these technologies.

Furthermore, AI is expected to play a critical role in the intelligent sorting and pre-treatment of plastic waste, a bottleneck often cited in feedstock preparation. Machine learning algorithms can identify and classify different types of plastics with high accuracy, optimizing the input stream for the conversion process and preventing contamination that can degrade fuel quality or damage equipment. Additionally, AI-powered predictive maintenance models can monitor machinery health in real-time, forecasting potential malfunctions before they occur. This proactive approach leads to significant reductions in maintenance costs and operational disruptions, ensuring continuous and efficient production. The integration of AI tools will therefore be instrumental in making plastic-to-fuel operations more robust, sustainable, and economically competitive.

- Intelligent Process Optimization: AI algorithms can analyze real-time operational data to dynamically adjust reaction parameters (e.g., temperature, pressure, catalyst dosage) for maximum fuel yield and quality, leading to higher efficiency and reduced waste.

- Predictive Maintenance: AI-powered sensors and machine learning models can monitor equipment health, predict potential failures, and schedule maintenance proactively, minimizing downtime and reducing operational costs.

- Feedstock Classification and Sorting: Computer vision and AI can accurately identify and sort different types of plastic waste, ensuring consistent and optimal feedstock for the conversion process, which improves fuel quality and prevents equipment damage.

- Supply Chain Optimization: AI can optimize the logistics of plastic waste collection and delivery to processing plants, reducing transportation costs and ensuring a steady supply of feedstock.

- Quality Control and Assurance: AI can monitor the quality of the produced fuel in real-time, identifying deviations from specifications and enabling immediate corrective actions, ensuring consistent high-quality output.

- Market Demand Forecasting: AI can analyze market trends and predict demand for various fuel products, allowing producers to adjust their output strategies and maximize revenue.

Key Takeaways Plastic to Fuel Technology Market Size & Forecast

The Plastic to Fuel Technology market is poised for substantial growth, driven by an urgent global need for effective plastic waste management and the escalating demand for sustainable energy alternatives. Users are particularly interested in the long-term viability and potential returns on investment within this sector. The forecast indicates a robust expansion, signaling increasing confidence from investors and policymakers in the technological maturity and economic feasibility of converting plastic waste into valuable fuels. This growth trajectory is underpinned by continuous innovation aimed at improving conversion efficiencies, broadening feedstock compatibility, and enhancing the quality of derived products, addressing previous barriers to widespread adoption.

Furthermore, the market's positive outlook is significantly influenced by a confluence of environmental regulations, governmental incentives, and a growing corporate commitment to circular economy principles. These factors are creating a fertile ground for new plant constructions, capacity expansions, and strategic collaborations across the value chain. The economic advantages, coupled with profound ecological benefits of reducing landfill burden and greenhouse gas emissions, firmly establish plastic-to-fuel technology as a pivotal solution in the transition towards a more sustainable and resource-efficient global economy, making it a compelling area for future investment and development.

- The Plastic to Fuel Technology market is projected for significant growth, driven by environmental mandates and energy demands.

- Technological advancements are consistently improving process efficiency and fuel quality, enhancing commercial viability.

- Increasing policy support and government incentives are accelerating market adoption and investment.

- The technology offers a dual benefit of sustainable waste management and alternative energy production.

- Strategic partnerships and collaborations are fostering a robust ecosystem for market expansion.

- The market presents substantial opportunities for innovation, investment, and sustainable development.

Plastic to Fuel Technology Market Drivers Analysis

The Plastic to Fuel Technology market is fundamentally driven by the escalating global plastic waste crisis, which presents an overwhelming environmental challenge. As landfills overflow and plastic pollution pervades oceans and ecosystems, governments and industries are compelled to seek innovative and sustainable waste management solutions. Plastic to fuel conversion offers a promising alternative, transforming a significant environmental liability into a valuable energy resource, thereby alleviating pollution and reducing reliance on virgin fossil fuels. This imperative for effective waste management serves as a powerful catalyst for market growth, pushing for greater adoption of conversion technologies worldwide.

Concurrently, the rising demand for alternative and renewable energy sources contributes significantly to the market's momentum. With volatile crude oil prices and increasing concerns over climate change, countries are actively seeking ways to diversify their energy mix and reduce carbon emissions. Fuels derived from plastic waste offer a lower-carbon alternative to conventional fossil fuels, supporting energy security objectives while contributing to decarbonization efforts. This dual benefit of waste remediation and energy generation positions plastic to fuel technology as a strategically important solution in the global transition towards a more sustainable and resilient energy landscape.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Plastic Waste Management Crisis | +5.0% | Global, particularly Asia Pacific (China, India, Southeast Asia) and Europe | Short to Long-term (2025-2033) |

| Increasing Demand for Alternative Fuels | +4.5% | North America, Europe, Middle East | Short to Mid-term (2025-2029) |

| Supportive Government Policies & Regulations | +4.0% | Europe (EU Directives), North America (US EPA), Asia Pacific (India, Japan) | Mid-term (2026-2031) |

| Technological Advancements in Conversion Efficiency | +3.5% | Global, especially developed economies with strong R&D (US, Germany, Japan) | Mid to Long-term (2027-2033) |

| Rising Public and Corporate Environmental Awareness | +1.5% | Global, consumer-driven markets | Long-term (2028-2033) |

Plastic to Fuel Technology Market Restraints Analysis

Despite its significant potential, the Plastic to Fuel Technology market faces several substantial restraints that could impede its growth. One of the primary concerns is the high initial capital investment required for establishing plastic-to-fuel conversion plants. The sophisticated machinery, complex infrastructure, and land acquisition costs can be prohibitive for many potential investors, particularly small and medium-sized enterprises. This high entry barrier limits the widespread adoption of the technology, especially in developing regions where access to large-scale funding and financial incentives may be more restricted, thereby slowing the market's overall expansion.

Another significant restraint involves the regulatory and permitting complexities associated with waste processing and fuel production. Operating a plastic-to-fuel plant often requires navigating intricate environmental regulations, waste management permits, and energy production licenses, which can be time-consuming and costly. Furthermore, the variability in the quality and consistency of the derived fuel products, compared to conventional fossil fuels, poses a challenge for market acceptance and integration into existing fuel supply chains. Issues such as sulfur content, viscosity, and heating value can fluctuate depending on feedstock and process parameters, demanding further refining or blending, which adds to the operational cost and technical complexity.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment and Operational Costs | -4.5% | Global, more pronounced in developing economies | Short to Mid-term (2025-2029) |

| Regulatory Hurdles and Permitting Complexities | -3.0% | Europe, North America (strict environmental regulations) | Short to Mid-term (2025-2028) |

| Competition from Established Fossil Fuel Markets | -2.5% | Global, particularly regions with abundant oil/gas reserves | Mid to Long-term (2026-2033) |

| Quality Inconsistency of Derived Fuels | -2.0% | Global, impacts end-user adoption | Short to Mid-term (2025-2030) |

| Challenges in Feedstock Collection and Sorting | -1.5% | Global, especially regions with underdeveloped waste infrastructure | Short-term (2025-2027) |

Plastic to Fuel Technology Market Opportunities Analysis

The Plastic to Fuel Technology market is rich with emerging opportunities that promise to accelerate its growth and impact. One significant avenue lies in the advancement and commercialization of modular and scalable conversion units. These smaller, decentralized systems can be deployed closer to waste generation sources, reducing transportation costs and enabling localized waste management solutions. This scalability makes the technology more accessible to a wider range of municipalities, industrial facilities, and even remote communities, opening up new markets that were previously uneconomical for large-scale plants. The flexibility offered by modular units can significantly enhance market penetration and accelerate adoption.

Another substantial opportunity is the diversification of derived products beyond mere fuel. While fuel oil is a primary output, ongoing research and development are exploring the production of higher-value chemicals, waxes, and specialized lubricants from plastic waste. This diversification can significantly improve the economic returns of plastic-to-fuel operations, making them more attractive to investors and enabling market players to tap into broader industrial applications. Furthermore, the integration of plastic-to-fuel facilities with existing waste management infrastructure, such as recycling centers or energy-from-waste plants, offers synergistic benefits, optimizing resource utilization and creating more comprehensive circular economy solutions. The rising global push for sustainable industrial practices further amplifies these opportunities, fostering innovation and investment in advanced waste conversion technologies.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Modular and Scalable Units | +4.0% | Global, particularly emerging economies and remote areas | Mid-term (2026-2031) |

| Production of Higher-Value Chemicals and Waxes | +3.5% | North America, Europe, East Asia (strong chemical industries) | Long-term (2028-2033) |

| Expansion into New Geographical Markets | +3.0% | Asia Pacific, Latin America, Middle East & Africa (rapid urbanization, waste issues) | Mid to Long-term (2027-2033) |

| Strategic Partnerships & Collaborative Ventures | +2.5% | Global, cross-industry collaborations | Short to Mid-term (2025-2030) |

| Integration with Existing Waste Management Infrastructure | +2.0% | Europe, North America (developed waste management systems) | Mid-term (2026-2031) |

Plastic to Fuel Technology Market Challenges Impact Analysis

The Plastic to Fuel Technology market, while promising, faces significant challenges that could hinder its widespread adoption and commercial viability. A paramount challenge is ensuring a consistent and high-quality feedstock supply. Plastic waste is highly diverse in composition, often mixed with contaminants and different polymer types, which can complicate the conversion process and affect the quality of the derived fuel. Sorting and pre-treatment of this heterogeneous waste stream require substantial investment in infrastructure and technology, and any inconsistencies can lead to inefficiencies, reduced yield, and increased operational costs, thereby impacting profitability.

Another critical challenge lies in achieving economic viability and competitiveness against established fossil fuel markets. Despite the environmental benefits, the production costs of plastic-derived fuels must be comparable or lower than conventional fuels to gain significant market traction without heavy subsidies. Scaling up the technology from pilot projects to commercial-scale operations also presents engineering and economic hurdles, including optimizing reactor designs, managing energy consumption, and ensuring long-term operational stability. Addressing these technical and economic challenges is crucial for the sustainable growth and widespread acceptance of plastic to fuel technology as a mainstream solution.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Feedstock Consistency and Contamination | -4.0% | Global, prevalent in regions with mixed waste streams | Short to Mid-term (2025-2030) |

| Economic Viability vs. Conventional Fuels | -3.5% | Global, impacts market adoption without policy support | Mid to Long-term (2026-2033) |

| Scaling Up Technology to Commercial Levels | -3.0% | Global, particularly for new entrants | Mid-term (2027-2032) |

| Environmental Emissions from Conversion Process | -2.0% | Europe, North America (strict environmental regulations) | Short to Mid-term (2025-2029) |

| Public Perception and Acceptance | -1.0% | Global, varies by region based on awareness | Long-term (2028-2033) |

Plastic to Fuel Technology Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Plastic to Fuel Technology market, encompassing historical data, current market dynamics, and future projections. It delivers critical insights into market size, growth drivers, restraints, opportunities, and challenges, leveraging robust methodologies and extensive primary and secondary research. The report aims to equip stakeholders with actionable intelligence for strategic decision-making, offering a detailed segmentation analysis, regional breakdown, and competitive landscape assessment to navigate this evolving industry effectively.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 295.5 Million |

| Market Forecast in 2033 | USD 1,180.0 Million |

| Growth Rate | 18.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Pyrolysis Innovations Group, Waste-to-Energy Solutions Inc., Plastic Recyclers & Fuel Co., Eco-Fuel Systems Ltd., Green Polyfuels Corp., Nexus Energy Technologies, Agile Renewables LLC, Bright Fuels Enterprises, Sustainable Plastic Conversion, Phoenix Energy Systems, Global Waste Conversion, BioFuel Tech Co., EnerGen Plastics, Transform Waste Solutions, ReGen Fuels, TerraCycle Energy, Carbon Solutions Group, Omega Waste-to-Oil, Future Energy Plastics, EnviroFuel Innovations |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Plastic to Fuel Technology market is extensively segmented to provide a granular understanding of its diverse facets and varying dynamics across different parameters. This comprehensive segmentation allows for a detailed analysis of market performance based on the specific technologies employed, the types of products generated, the variety of plastic feedstocks utilized, and the ultimate end-use applications of the derived fuels. Such a structured breakdown is crucial for identifying key growth areas, understanding competitive landscapes within niches, and formulating targeted strategies for market penetration and expansion.

Understanding these segments helps stakeholders pinpoint the most promising technological advancements, identify high-potential feedstock streams, and cater to specific industrial demands for alternative fuels. For instance, the market for converting mixed plastics presents different challenges and opportunities compared to processing a single type of polymer. Similarly, the demand for fuel oil in industrial applications differs from the need for synthetic gas in power generation. This detailed segmentation thus serves as a foundational tool for market participants to make informed investment decisions, optimize their operational models, and adapt to evolving market needs effectively.

- By Technology: This segment includes the various conversion processes used to transform plastic waste into fuel.

- Pyrolysis: A thermochemical decomposition of organic material at elevated temperatures in the absence of oxygen.

- Gasification: A process that converts organic or fossil-based carbonaceous materials into carbon monoxide, hydrogen, and carbon dioxide.

- Hydrothermal Liquefaction: A thermochemical process that converts biomass into liquid products under moderate temperatures and high pressures in the presence of water.

- Catalytic Conversion: Processes that use catalysts to enhance the cracking of plastic polymers into smaller hydrocarbon molecules at lower temperatures.

- By Product: This segment categorizes the different types of fuels or materials produced from plastic waste.

- Fuel Oil: Typically similar to diesel or naphtha, used in industrial burners or as transportation fuel.

- Synthetic Gas (Syngas): A mixture primarily of hydrogen and carbon monoxide, used for power generation or chemical synthesis.

- Solid Residue/Char: A carbonaceous byproduct that can have various applications, including activated carbon or soil amendment.

- By Feedstock: This segment focuses on the types of plastic waste utilized for conversion.

- Polyethylene (PE): High-density (HDPE) and low-density (LDPE) polyethylene, commonly found in packaging.

- Polypropylene (PP): Used in containers, automotive parts, and textiles.

- Polystyrene (PS): Found in disposable cups, insulation, and packaging peanuts.

- Polyvinyl Chloride (PVC): Used in pipes, window frames, and flooring.

- Mixed Plastics: Heterogeneous plastic waste streams often collected from municipal solid waste, requiring advanced sorting.

- By End-Use: This segment identifies the primary sectors or applications where the derived fuels are consumed.

- Industrial: Use in furnaces, boilers, and other industrial heating applications.

- Transportation: Blending with conventional fuels for use in vehicles.

- Power Generation: Utilization in gas turbines or engines for electricity production.

- Chemical Feedstock: Conversion into monomers or other chemical building blocks for new plastic production or other chemical processes.

Regional Highlights

- North America: The region is characterized by significant research and development investments in advanced conversion technologies, coupled with increasing regulatory pressures for sustainable waste management. The United States and Canada are leading in adopting innovative solutions, driven by environmental consciousness and the search for energy independence. Strong industrial infrastructure supports the scaling up of plastic-to-fuel plants.

- Europe: Europe is a frontrunner in circular economy initiatives and stringent waste directives, making it a pivotal market for plastic to fuel technology. Countries like Germany, the UK, and France are heavily investing in pyrolysis and gasification plants to meet ambitious recycling targets and reduce reliance on landfilling. The region benefits from robust regulatory frameworks and public support for eco-friendly solutions.

- Asia Pacific (APAC): APAC represents the largest and fastest-growing market due to its immense plastic waste generation, rapid industrialization, and burgeoning energy demand. Countries such as China, India, Japan, and South Korea are increasingly exploring plastic-to-fuel solutions to address their severe waste management challenges and enhance energy security. Government initiatives and foreign investments are fueling the growth in this region.

- Latin America: This region is an emerging market for plastic to fuel technology, driven by growing environmental awareness, increasing plastic consumption, and the need for improved waste infrastructure. Countries like Brazil and Mexico are witnessing nascent developments and pilot projects, with potential for significant growth as economic conditions and regulatory frameworks become more conducive to large-scale waste conversion.

- Middle East and Africa (MEA): The MEA region faces substantial challenges in waste management, coupled with a high demand for energy. Plastic to fuel technology offers a viable solution to both issues. GCC countries, with their focus on diversification from oil and gas and investment in sustainable technologies, are showing increasing interest. South Africa and other African nations are also exploring these technologies to manage urban waste and provide decentralized energy solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Plastic to Fuel Technology Market.- Pyrolysis Innovations Group

- Waste-to-Energy Solutions Inc.

- Plastic Recyclers & Fuel Co.

- Eco-Fuel Systems Ltd.

- Green Polyfuels Corp.

- Nexus Energy Technologies

- Agile Renewables LLC

- Bright Fuels Enterprises

- Sustainable Plastic Conversion

- Phoenix Energy Systems

- Global Waste Conversion

- BioFuel Tech Co.

- EnerGen Plastics

- Transform Waste Solutions

- ReGen Fuels

- TerraCycle Energy

- Carbon Solutions Group

- Omega Waste-to-Oil

- Future Energy Plastics

- EnviroFuel Innovations

Frequently Asked Questions

What is Plastic to Fuel Technology?

Plastic to Fuel Technology refers to a range of processes, primarily thermochemical methods like pyrolysis and gasification, that convert plastic waste into valuable liquid fuels (such as fuel oil, diesel, or naphtha) or synthetic gas. It offers a solution for managing non-recyclable plastic waste by transforming it into an energy resource.

Is Plastic to Fuel Technology environmentally friendly?

Yes, when properly implemented, Plastic to Fuel Technology can be environmentally beneficial. It diverts plastic waste from landfills and incineration, reducing land and ocean pollution. It also provides an alternative to fossil fuels, potentially lowering greenhouse gas emissions, especially when combined with advanced emission control and carbon capture technologies.

What types of plastics can be converted into fuel?

The technology is capable of processing various types of plastics, including Polyethylene (PE), Polypropylene (PP), Polystyrene (PS), and even some mixed plastics. The efficiency and quality of the derived fuel can vary depending on the plastic type and the specific conversion technology used, with some systems optimized for particular waste streams.

What are the primary products of Plastic to Fuel conversion?

The main products typically include fuel oil, which can be used as an industrial fuel or further refined into diesel or gasoline components; synthetic gas (syngas), suitable for power generation; and solid residues (char) that may have various industrial applications or require further disposal. Some advanced processes also yield waxes or chemical feedstocks.

What are the main challenges facing the Plastic to Fuel market?

Key challenges include high initial capital investment costs for plants, ensuring a consistent and uncontaminated supply of plastic feedstock, achieving consistent quality of the derived fuels to meet market specifications, and navigating complex regulatory landscapes. Economic competitiveness against established fossil fuel markets without subsidies also remains a significant hurdle.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted