Plastic Food Storage Container Market

Plastic Food Storage Container Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706891 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

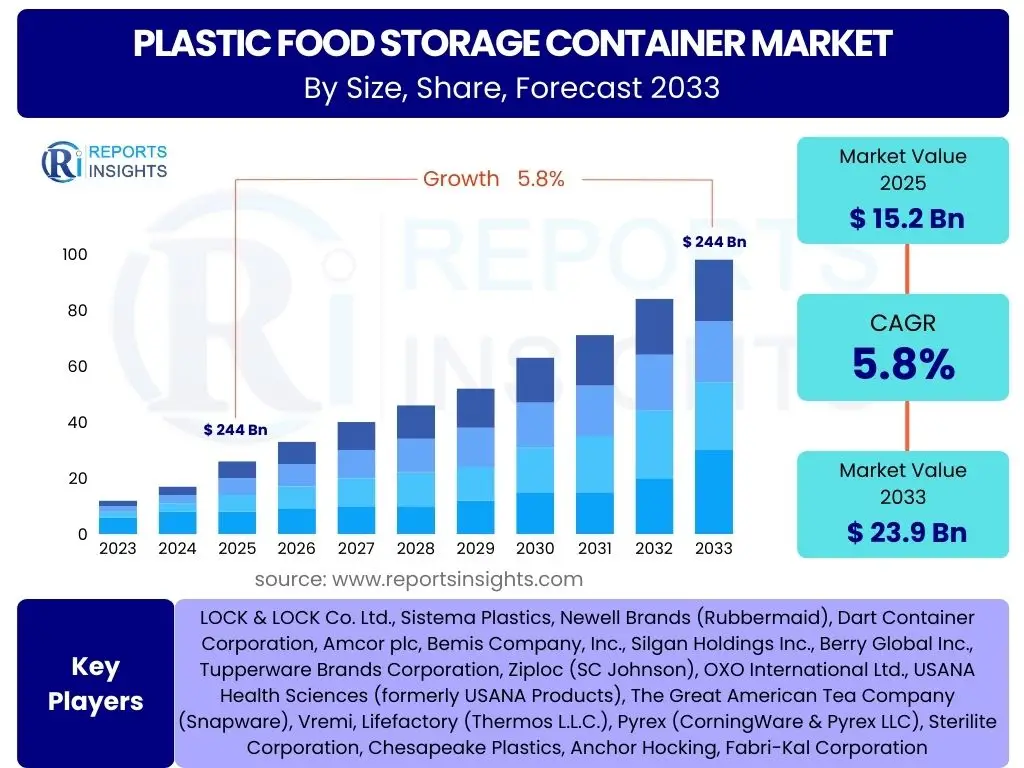

Plastic Food Storage Container Market Size

According to Reports Insights Consulting Pvt Ltd, The Plastic Food Storage Container Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 23.9 Billion by the end of the forecast period in 2033.

Key Plastic Food Storage Container Market Trends & Insights

User inquiries frequently highlight evolving consumer preferences for convenience, sustainability, and product innovation within the plastic food storage container market. A prominent trend is the increasing demand for eco-friendly and reusable options, driven by growing environmental awareness and regulatory pressures. Consumers are also seeking versatile, multi-functional containers that cater to diverse needs such as meal prepping, on-the-go consumption, and organized pantry storage.

Furthermore, the market is witnessing a shift towards aesthetic and customizable designs, moving beyond mere utility to integrate with modern kitchen aesthetics. The rise of e-commerce platforms has also significantly influenced distribution channels, making a wider variety of products accessible to a global consumer base. Innovation in material science, focusing on enhanced durability, reduced weight, and improved sealing mechanisms, remains a crucial area of development.

- Growing demand for sustainable and recyclable plastic materials, including recycled content and bio-based plastics.

- Increased focus on multi-functional and modular designs to optimize space and cater to diverse food storage needs.

- Expansion of e-commerce as a primary distribution channel, offering wider product accessibility and consumer choice.

- Integration of smart features, such as QR codes for content tracking or freshness indicators, in premium offerings.

- Emphasis on aesthetic appeal and customizable designs to align with modern home decor trends.

- Rising adoption of meal prepping and on-the-go food consumption habits.

AI Impact Analysis on Plastic Food Storage Container

Common user questions regarding AI's impact on the plastic food storage container sector revolve around how it can enhance manufacturing efficiency, optimize supply chains, and contribute to sustainability efforts. Users are interested in AI's potential to streamline production processes, reduce waste, and improve product quality control. There is also curiosity about AI's role in personalized consumer experiences and demand forecasting.

AI's influence extends to various facets, from predictive maintenance in manufacturing facilities to intelligent inventory management, significantly reducing operational costs and improving responsiveness to market changes. Moreover, AI can play a crucial role in waste management and recycling processes, identifying and sorting different plastic types more efficiently, thereby closing the loop on plastic usage. It also has potential in personalized marketing and product development, analyzing consumer data to inform design and feature enhancements.

- Optimizing manufacturing processes through predictive analytics for equipment maintenance and operational efficiency.

- Enhancing supply chain management by predicting demand, optimizing logistics, and reducing lead times.

- Improving quality control and defect detection during the production of plastic containers.

- Facilitating personalized product recommendations and marketing strategies based on consumer purchasing patterns.

- Assisting in the advanced sorting and recycling of plastic materials, contributing to a circular economy.

Key Takeaways Plastic Food Storage Container Market Size & Forecast

Analysis of user questions regarding market size and forecast highlights strong interest in understanding the primary growth catalysts, particularly the role of consumer behavior shifts and innovation. Key takeaways indicate a robust growth trajectory for the plastic food storage container market, primarily propelled by the increasing global emphasis on convenience, food waste reduction, and organized living. The market's resilience is further supported by continuous product innovation, addressing both functional and aesthetic consumer demands.

The forecast suggests that while traditional uses remain significant, emerging applications such as meal kit delivery services and a heightened focus on hygiene will fuel demand. Companies that prioritize sustainable material development, smart design features, and strong e-commerce presence are poised for significant market capture. Regional economic growth, particularly in developing nations, will also serve as a crucial accelerator for market expansion over the forecast period.

- The market is set for sustained growth, driven by lifestyle changes such as increased meal prepping and on-the-go consumption.

- Sustainability initiatives, including the adoption of recycled and bio-based plastics, are critical for future market acceptance and growth.

- Product innovation focusing on modularity, airtight seals, and aesthetic design will be key differentiators.

- E-commerce channels are becoming increasingly vital for market reach and consumer engagement.

- Growth in developing economies, fueled by urbanization and rising disposable incomes, will significantly contribute to market expansion.

Plastic Food Storage Container Market Drivers Analysis

The rising global emphasis on food preservation and waste reduction is a primary driver for the plastic food storage container market. Consumers are increasingly aware of the economic and environmental benefits of minimizing food spoilage, leading to higher adoption rates of effective storage solutions. This growing consciousness, combined with busy lifestyles, necessitates practical and reliable containers for leftovers, meal prepping, and packed lunches, directly stimulating market demand.

Furthermore, the proliferation of online food delivery services and the increasing popularity of meal kit subscriptions have created a significant demand for convenient, durable, and leak-proof food packaging, much of which relies on plastic containers. These services often provide pre-portioned ingredients or cooked meals in plastic containers designed for easy transport and storage. The ongoing product innovation, including features like improved sealing mechanisms, stackable designs, and microwave-safe materials, continuously enhances user convenience and broadens application areas, thereby driving market expansion.

The overall growth in disposable income in emerging economies and the expanding urban populations globally also contribute to market growth. As more individuals adopt modern dietary habits and require efficient solutions for daily food management, the demand for versatile and affordable plastic food storage containers naturally increases. This demographic shift, coupled with an escalating need for household organization, underpins the consistent market trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for convenience and on-the-go food consumption | +1.5% | Global | Short to Mid-term |

| Increasing awareness regarding food waste reduction and preservation | +1.2% | Developed Economies | Mid-term |

| Expansion of online food delivery and meal prep services | +1.0% | Urban Areas, Globally | Short-term |

| Product innovation enhancing functionality and design | +0.8% | Global | Mid to Long-term |

Plastic Food Storage Container Market Restraints Analysis

Significant environmental concerns surrounding plastic pollution represent a major restraint on the market. Public awareness about single-use plastics, ocean plastic accumulation, and the slow degradation rate of conventional plastics has led to negative consumer perception and increased pressure on manufacturers. This shift in public sentiment encourages consumers to seek alternatives, such as glass, stainless steel, or silicone, which are perceived as more environmentally friendly or sustainable.

Furthermore, stringent governmental regulations and bans on certain types of plastics or specific plastic products, particularly within regions like the European Union, are directly impacting the market. These regulations aim to reduce plastic waste and promote a circular economy, often leading to increased production costs for manufacturers or a forced transition to more expensive, sustainable materials, thereby slowing market growth for conventional plastics. The complexity of recycling various plastic types also acts as a restraint, as inadequate recycling infrastructure can undermine sustainability efforts and public trust.

Health concerns associated with certain chemical compounds found in plastics, such as BPA (Bisphenol A) and phthalates, also continue to be a restraint. Despite industry efforts to develop BPA-free products, lingering consumer apprehension about potential chemical leaching into food influences purchasing decisions. This contributes to a preference for non-plastic alternatives or requires manufacturers to invest heavily in research and development for safer plastic formulations, which can increase product costs and reduce competitive edge.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Environmental concerns regarding plastic pollution and waste | -1.8% | Developed Economies | Long-term |

| Stringent governmental regulations and bans on single-use plastics | -1.5% | Europe, North America | Short to Mid-term |

| Competition from alternative materials like glass, stainless steel, and silicone | -1.0% | North America, Europe | Mid-term |

| Consumer health concerns related to chemical leaching from plastics | -0.9% | Global | Long-term |

Plastic Food Storage Container Market Opportunities Analysis

The growing emphasis on sustainability presents a significant opportunity for the plastic food storage container market, particularly through the development and adoption of bio-based, biodegradable, and recycled content plastics. Innovation in these areas allows manufacturers to address environmental concerns while retaining the functional benefits of plastic, such as lightness and durability. Investing in research and development for advanced sustainable polymers and robust recycling technologies can unlock new market segments and appeal to an eco-conscious consumer base.

The integration of smart technologies offers another lucrative opportunity. Incorporating features like integrated sensors for freshness monitoring, QR codes for inventory management, or temperature indicators can differentiate products and add significant value. While still nascent, these intelligent solutions cater to a technologically savvy consumer base seeking enhanced convenience and efficiency in food management, opening avenues for premium product lines and partnerships with smart home ecosystems.

Furthermore, the expansion into emerging markets, particularly in Asia Pacific and Latin America, presents substantial growth opportunities. These regions are experiencing rapid urbanization, rising disposable incomes, and a shift towards modern retail formats, leading to increased demand for convenient and hygienic food storage solutions. Tailoring product offerings to meet the specific cultural preferences and economic conditions of these markets can drive significant volume growth and establish new revenue streams for market players. Additionally, the increasing global focus on food safety and hygiene, accelerated by recent global health events, reinforces the need for reliable and safe food storage, presenting a continuous opportunity for compliant and innovative products.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and adoption of sustainable and bio-based plastic materials | +1.7% | Global | Mid to Long-term |

| Integration of smart technologies for enhanced functionality and food safety | +1.3% | Developed Economies | Long-term |

| Expansion into untapped and emerging markets with growing middle-class populations | +1.1% | Asia Pacific, Latin America, MEA | Long-term |

| Growing demand for multi-functional, modular, and customizable storage solutions | +0.9% | Global | Mid-term |

Plastic Food Storage Container Market Challenges Impact Analysis

The plastic food storage container market faces significant challenges, notably the volatility in raw material prices, primarily crude oil derivatives. Fluctuations in petroleum prices directly impact the cost of plastic resins, leading to unpredictable production expenses for manufacturers. This unpredictability can squeeze profit margins, complicate pricing strategies, and hinder long-term investment in product development, especially for smaller market players who have less leverage with suppliers.

Another critical challenge is the persistent negative public perception of plastics due to environmental and health concerns. Despite advancements in material science and the introduction of safer, more sustainable plastics, general consumer sentiment often views plastic as inherently harmful or non-eco-friendly. This perception can lead to a consumer shift towards alternative materials, eroding market share for plastic containers and forcing manufacturers to invest heavily in marketing and education to dispel misconceptions.

Furthermore, building and maintaining a robust and accessible recycling infrastructure for diverse plastic types remains a significant hurdle. While many plastic containers are technically recyclable, the lack of widespread and efficient collection, sorting, and processing facilities globally means a substantial portion still ends up in landfills or the environment. This infrastructure gap not only undermines sustainability efforts but also makes it difficult for manufacturers to source sufficient recycled content, hindering their ability to meet growing demand for circular economy products and comply with regulatory requirements.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in raw material prices (e.g., petroleum derivatives) | -1.2% | Global | Short to Mid-term |

| Maintaining product safety standards and addressing health concerns | -0.8% | Global | Ongoing |

| Inadequate global recycling infrastructure for plastic waste | -0.7% | Developing Economies | Long-term |

| Shifting consumer preferences and negative perception towards plastics | -0.6% | Developed Economies | Mid-term |

Plastic Food Storage Container Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global plastic food storage container market, covering historical data from 2019 to 2023, base year 2024, and forecasts through 2033. It examines market size, growth drivers, restraints, opportunities, and challenges influencing the industry landscape. The report includes detailed segmentation analysis by material, type, application, capacity, and distribution channel, offering granular insights into key market dynamics. Additionally, it provides regional breakdowns, highlights prominent market trends, and profiles leading companies to offer a holistic view of the competitive environment.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2033 | USD 23.9 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | LOCK & LOCK Co. Ltd., Sistema Plastics, Newell Brands (Rubbermaid), Dart Container Corporation, Amcor plc, Bemis Company, Inc., Silgan Holdings Inc., Berry Global Inc., Tupperware Brands Corporation, Ziploc (SC Johnson), OXO International Ltd., USANA Health Sciences (formerly USANA Products), The Great American Tea Company (Snapware), Vremi, Lifefactory (Thermos L.L.C.), Pyrex (CorningWare & Pyrex LLC), Sterilite Corporation, Chesapeake Plastics, Anchor Hocking, Fabri-Kal Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The plastic food storage container market is highly segmented, reflecting the diverse needs of consumers and commercial entities across various applications and preferences. Understanding these segments is crucial for manufacturers to tailor their product offerings, marketing strategies, and distribution channels effectively. The segmentation by material highlights the prevalence and evolution of different plastic types based on properties like durability, heat resistance, and recyclability, with polypropylene (PP) and polyethylene (PE) being dominant due to their versatility and cost-effectiveness.

Further segmentation by container type, such as airtight, vacuum seal, stackable, and modular, addresses specific consumer demands for food preservation, space optimization, and convenience. The application segment differentiates between residential, commercial, and industrial uses, each with unique requirements for capacity, durability, and compliance. Lastly, the distribution channel analysis provides insights into consumer purchasing habits, emphasizing the growing importance of online retail alongside traditional brick-and-mortar stores, enabling companies to optimize their market reach.

- By Material: Includes Polypropylene (PP), Polyethylene (PE), Polyethylene Terephthalate (PET), and Other Plastics (e.g., Polystyrene, Polycarbonate). PP and PE remain prevalent due to their excellent barrier properties and chemical resistance.

- By Type: Comprises Airtight containers for extended freshness, Vacuum Seal for superior preservation, Stackable and Collapsible designs for space efficiency, and Modular systems for organizational needs.

- By Application: Categorized into Residential use for household storage, Commercial use encompassing restaurants, catering, and food service industries, and Industrial applications for large-scale food processing and packaging.

- By Capacity: Segments include Below 500 ml for small portions or snacks, 500 ml - 1500 ml for standard meal prep and leftovers, and Above 1500 ml for bulk storage or large family use.

- By Distribution Channel: Covers Online Retail, Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, and other direct sales channels, reflecting diverse consumer purchasing preferences.

Regional Highlights

- North America: This region is characterized by a mature market with high consumer awareness regarding food safety and convenience. The demand for multi-functional and sustainable plastic storage solutions is strong, driven by busy lifestyles and a growing meal-prepping culture. Innovation in design and the adoption of smart features are key trends here.

- Europe: Europe is at the forefront of sustainability, with stringent regulations on plastic use driving the demand for recycled, recyclable, and bio-based plastic food containers. Consumers are increasingly eco-conscious, influencing manufacturers to invest heavily in green solutions and circular economy principles.

- Asia Pacific (APAC): APAC represents the fastest-growing market, fueled by rapid urbanization, rising disposable incomes, and changing dietary habits. The burgeoning e-commerce sector and the increasing adoption of modern retail formats are significant growth accelerators. Both residential and commercial applications contribute substantially to market expansion.

- Latin America: This region is experiencing steady growth due to improving economic conditions, expanding middle-class populations, and the increasing adoption of packaged food. The demand for affordable and practical storage solutions for everyday use is a key driver.

- Middle East and Africa (MEA): The MEA market is gradually expanding, driven by population growth, urbanization, and a developing retail infrastructure. While still nascent in some areas, increasing health consciousness and demand for hygienic food storage are contributing to market development.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Plastic Food Storage Container Market.- LOCK & LOCK Co. Ltd.

- Sistema Plastics

- Newell Brands (Rubbermaid)

- Dart Container Corporation

- Amcor plc

- Bemis Company, Inc.

- Silgan Holdings Inc.

- Berry Global Inc.

- Tupperware Brands Corporation

- Ziploc (SC Johnson)

- OXO International Ltd.

- USANA Health Sciences

- The Great American Tea Company (Snapware)

- Vremi

- Lifefactory (Thermos L.L.C.)

- Pyrex (CorningWare & Pyrex LLC)

- Sterilite Corporation

- Chesapeake Plastics

- Anchor Hocking

- Fabri-Kal Corporation

Frequently Asked Questions

What is the projected growth rate of the plastic food storage container market?

The plastic food storage container market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, reaching an estimated USD 23.9 Billion by 2033.

What are the key drivers for market growth?

Key drivers include the rising demand for convenience and on-the-go food consumption, increasing awareness of food waste reduction, the expansion of online food delivery services, and continuous product innovation focusing on functionality and design.

How do sustainability concerns impact this market?

Sustainability concerns act as a significant restraint, driving demand for eco-friendly alternatives like glass or stainless steel. However, they also present an opportunity for manufacturers developing sustainable plastic solutions such as bio-based, recycled, or biodegradable materials to meet evolving consumer and regulatory demands.

What role does e-commerce play in distribution?

E-commerce is an increasingly vital distribution channel, offering consumers wider product accessibility, diverse choices, and competitive pricing. Its growth is significantly contributing to market reach and sales volume for plastic food storage containers globally.

Which regions are expected to show significant growth?

The Asia Pacific (APAC) region is expected to show the most significant growth due to rapid urbanization, rising disposable incomes, and the expansion of modern retail and e-commerce infrastructure.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted