Plastic Dielectric Film in Electronic Market

Plastic Dielectric Film in Electronic Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709168 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Plastic Dielectric Film in Electronic Market Size

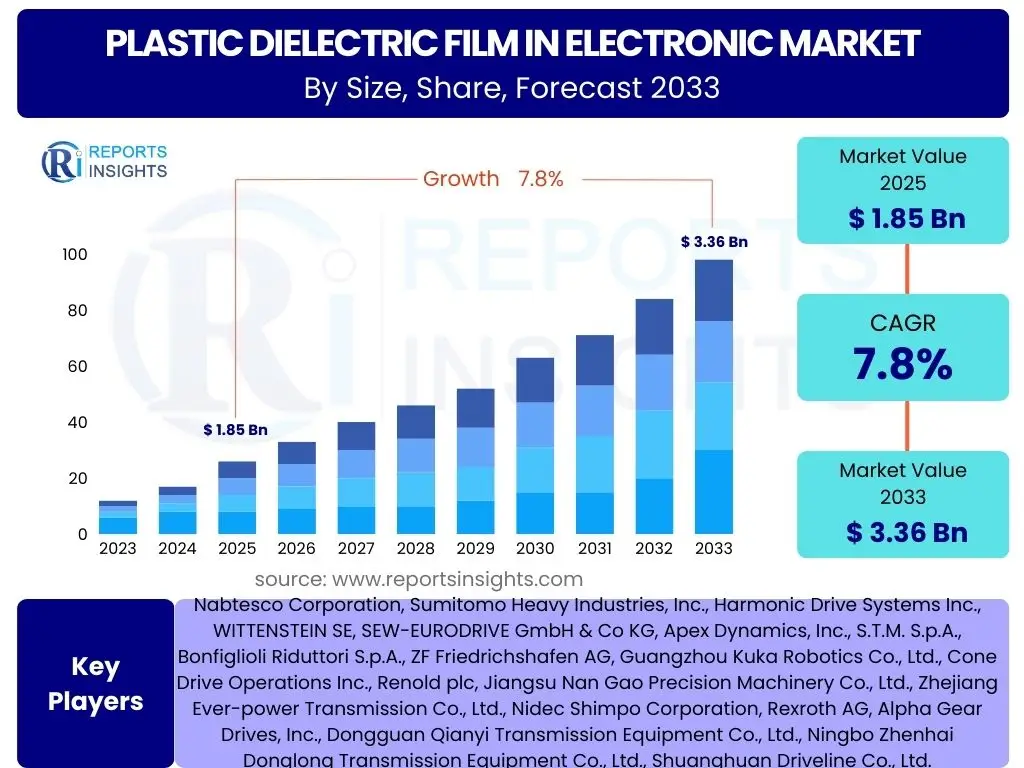

According to Reports Insights Consulting Pvt Ltd, The Plastic Dielectric Film in Electronic Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 1.85 billion in 2025 and is projected to reach USD 3.36 billion by the end of the forecast period in 2033.

Key Plastic Dielectric Film in Electronic Market Trends & Insights

The Plastic Dielectric Film in Electronic market is experiencing significant evolution driven by the relentless demand for higher performance and smaller electronic components across various industries. Current user interest predominantly revolves around the adoption of advanced materials capable of withstanding extreme conditions, the integration of these films into cutting-edge applications like flexible electronics and electric vehicles, and the overarching push for sustainable and eco-friendly manufacturing processes. Industry stakeholders are keenly observing how material innovations and application diversification will shape market dynamics and competitive landscapes over the coming decade.

The drive towards miniaturization and increased energy efficiency in consumer electronics continues to be a primary catalyst for innovation in plastic dielectric films. Manufacturers are under constant pressure to develop films with superior dielectric strength, lower loss tangents, and enhanced thermal stability to support the next generation of smartphones, wearables, and computing devices. Furthermore, the proliferation of 5G technology and the Internet of Things (IoT) demands components that can operate reliably at higher frequencies and temperatures, directly influencing material science advancements in this domain. This has led to a focus on films that can offer robust performance without compromising on form factor or environmental impact.

- Miniaturization and High-Density Integration: Growing demand for compact electronic devices drives the need for ultra-thin films with high dielectric constant and breakdown strength, enabling smaller components.

- Electric Vehicle (EV) and Renewable Energy Adoption: Increasing demand for high-performance capacitors in power electronics for EVs, hybrid vehicles, and renewable energy inverters (solar, wind) necessitates films with excellent thermal and electrical properties.

- 5G and IoT Expansion: The rollout of 5G infrastructure and proliferation of IoT devices requires dielectric films capable of operating reliably at higher frequencies and temperatures, with low signal loss characteristics.

- Advanced Material Development: Continuous research and development in novel polymer formulations and composite materials for enhanced performance, including higher temperature resistance, improved mechanical flexibility, and better insulation properties.

- Sustainability and Green Manufacturing: Growing emphasis on environmentally friendly materials, recyclable films, and energy-efficient production processes to meet regulatory requirements and consumer demand for sustainable products.

- Flexible and Wearable Electronics: Emergence of flexible displays, bendable circuits, and wearable health monitors creates new applications for highly flexible and durable dielectric films.

- Increased Performance in Power Electronics: Demand for films that can handle higher voltages and currents with improved efficiency and reliability for industrial power supplies and grid applications.

AI Impact Analysis on Plastic Dielectric Film in Electronic

The impact of Artificial Intelligence (AI) on the Plastic Dielectric Film in Electronic market is a topic of increasing scrutiny, with users frequently querying its role in accelerating material discovery, optimizing manufacturing processes, and enhancing product performance. Key concerns revolve around the potential for AI to revolutionize research and development by reducing experimental cycles, predicting material properties, and designing novel film structures. Users are also interested in how AI can improve efficiency and yield in complex film production, potentially leading to cost reductions and higher quality output, thereby addressing the challenges associated with advanced material fabrication.

Furthermore, AI's influence extends to predictive maintenance and quality control within manufacturing facilities, allowing for real-time adjustments and early detection of anomalies that could compromise film integrity. This proactive approach ensures consistent product quality and minimizes waste, which is crucial in the high-precision world of electronic components. The integration of AI in design tools and simulation platforms also empowers engineers to model the behavior of dielectric films under various operational conditions, accelerating the development of application-specific solutions and shortening time-to-market for innovative electronic devices.

- Accelerated Material Discovery: AI algorithms can analyze vast datasets of material properties, predict performance characteristics, and suggest novel polymer formulations for dielectric films, significantly shortening R&D cycles.

- Optimized Manufacturing Processes: AI-driven systems can monitor and control film extrusion, coating, and lamination processes in real-time, optimizing parameters for thickness uniformity, defect reduction, and improved yield.

- Predictive Quality Control: Machine learning models can analyze sensor data from production lines to predict potential defects or deviations in film quality, enabling proactive adjustments and minimizing waste.

- Enhanced Product Design and Simulation: AI assists engineers in simulating the electrical, thermal, and mechanical behavior of dielectric films under various operating conditions, leading to more robust and efficient designs for electronic components.

- Supply Chain Optimization: AI can be used to forecast demand, optimize inventory management for raw materials, and identify potential supply chain disruptions, ensuring smoother production of dielectric films.

- Personalized Material Solutions: AI could enable the rapid development of customized dielectric films tailored to specific electronic applications, meeting unique performance requirements.

Key Takeaways Plastic Dielectric Film in Electronic Market Size & Forecast

Common user inquiries regarding the Plastic Dielectric Film in Electronic market size and forecast often center on the long-term growth prospects, the primary drivers fueling this expansion, and the most promising application areas. The market's consistent growth trajectory is largely underpinned by the insatiable global demand for advanced electronic devices, coupled with significant investments in next-generation technologies like electric vehicles and 5G infrastructure. Stakeholders are keen to understand which segments will offer the highest returns and where strategic investments should be directed over the forecast period to capitalize on these trends effectively.

The projected increase in market valuation from USD 1.85 billion in 2025 to USD 3.36 billion by 2033, at a CAGR of 7.8%, highlights a robust and expanding sector. This growth is not uniform across all segments; rather, it is concentrated in areas requiring high-performance, compact, and energy-efficient dielectric solutions. Understanding the nuanced interplay between technological advancements, regulatory pressures, and evolving consumer preferences is critical for market participants looking to maintain a competitive edge. The forecast emphasizes the resilience and adaptability of the market to meet the ever-increasing demands of the electronic industry, positioning plastic dielectric films as indispensable components.

- Robust Market Expansion: The market is projected to grow substantially from USD 1.85 billion in 2025 to USD 3.36 billion by 2033, indicating a healthy and consistent growth trajectory.

- CAGR Reflects Strong Demand: A Compound Annual Growth Rate (CAGR) of 7.8% signifies sustained demand driven by advancements in electronics and emerging high-growth applications.

- Key Growth Catalysts: Miniaturization in consumer electronics, the electrification of vehicles, and the build-out of 5G and IoT networks are primary drivers.

- Investment Opportunities: High-performance films for power electronics, flexible electronics, and advanced materials for high-temperature applications represent significant investment opportunities.

- Regional Variances: Asia Pacific is expected to remain a dominant region due to its strong manufacturing base and high adoption of electronic components.

- Sustainability Imperative: Future market success will increasingly depend on the development and adoption of environmentally friendly and recyclable dielectric film solutions.

Plastic Dielectric Film in Electronic Market Drivers Analysis

The Plastic Dielectric Film in Electronic market is significantly propelled by several key factors that underscore its indispensable role in modern technology. A primary driver is the pervasive trend of miniaturization and increasing functionality in consumer electronics, which necessitates dielectric films capable of providing superior insulation in increasingly compact spaces. This demand is further amplified by the global surge in electric vehicle (EV) adoption, where high-performance capacitors relying on these films are critical for power management and energy storage systems. The need for films with enhanced thermal stability and dielectric strength is paramount in these high-power applications.

Another substantial driver is the rapid expansion of 5G infrastructure and the Internet of Things (IoT). These technologies demand electronic components that can operate reliably at higher frequencies and temperatures, often in complex and constrained environments. Plastic dielectric films, with their customizable properties, are crucial for achieving the necessary performance in these advanced communication and sensing devices. Furthermore, the growing focus on renewable energy systems, such as solar inverters and wind turbines, also drives demand for robust and efficient power electronics, directly impacting the market for specialized dielectric films that can withstand demanding operational conditions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Consumer Electronics Miniaturization | +2.1% | Global (APAC, North America, Europe) | Short to Mid-term (2025-2030) |

| Rapid Growth in Electric Vehicles (EVs) and Hybrid Electric Vehicles (HEVs) | +1.8% | Global (China, Europe, North America) | Mid to Long-term (2026-2033) |

| Expansion of 5G Infrastructure and IoT Devices | +1.6% | Global (APAC, North America, Europe) | Short to Mid-term (2025-2030) |

| Rising Adoption of Renewable Energy Systems | +1.3% | Global (Europe, North America, APAC) | Mid to Long-term (2027-2033) |

| Advancements in Flexible and Wearable Electronics | +1.0% | Global (APAC, North America) | Mid to Long-term (2028-2033) |

Plastic Dielectric Film in Electronic Market Restraints Analysis

Despite its robust growth, the Plastic Dielectric Film in Electronic market faces several significant restraints that could temper its expansion. One prominent restraint is the volatility of raw material prices, particularly for petrochemical-derived polymers like polypropylene and polyethylene terephthalate. Fluctuations in crude oil prices and supply chain disruptions can directly impact manufacturing costs, subsequently affecting product pricing and profit margins for film producers. This instability makes long-term planning and investment more challenging for market participants.

Another crucial restraint involves the stringent environmental regulations and the increasing pressure for sustainable materials. The disposal of conventional plastic films poses environmental challenges, leading to regulatory scrutiny and consumer preference for eco-friendly alternatives. Developing biodegradable or easily recyclable dielectric films that still meet the demanding performance specifications for electronic applications is a complex and costly endeavor. Furthermore, intense competition from alternative dielectric materials, such as ceramics or advanced composites, especially in high-temperature or high-frequency applications, poses a threat to the market share of plastic films, requiring continuous innovation to maintain competitive relevance.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -1.5% | Global | Short to Mid-term (2025-2030) |

| Stringent Environmental Regulations and Sustainability Concerns | -1.2% | Europe, North America, APAC | Mid to Long-term (2027-2033) |

| Competition from Alternative Dielectric Materials (e.g., Ceramics) | -1.0% | Global | Mid to Long-term (2026-2033) |

| Complex Manufacturing Processes and High Capital Expenditure | -0.8% | Global | Short to Mid-term (2025-2030) |

| Performance Limitations in Extreme Temperature/Voltage Applications | -0.7% | Global | Mid to Long-term (2028-2033) |

Plastic Dielectric Film in Electronic Market Opportunities Analysis

Despite existing restraints, the Plastic Dielectric Film in Electronic market is rich with opportunities that promise to drive future growth and innovation. A significant opportunity lies in the burgeoning field of flexible and wearable electronics. The demand for bendable displays, flexible printed circuit boards (FPCBs), and smart textiles necessitates dielectric films with exceptional mechanical flexibility, durability, and stable electrical properties under deformation. Developing ultra-thin, highly flexible films that maintain performance under repeated stress represents a lucrative niche for manufacturers to explore.

Another compelling opportunity emerges from the continuous advancements in material science, particularly the development of high-performance polymers and composite materials. Innovations leading to films with superior thermal conductivity, higher breakdown strength, and lower dielectric loss at elevated temperatures can unlock new applications in high-power electronics, aerospace, and defense sectors. Furthermore, the increasing global awareness and regulatory push for sustainability create an opportunity for producers to invest in and market biodegradable, recyclable, or bio-based dielectric films, differentiating themselves in an increasingly eco-conscious market. Strategic partnerships with electronic component manufacturers and end-use industries can also accelerate the adoption of these novel film solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced High-Performance Films | +1.9% | Global | Mid to Long-term (2026-2033) |

| Emergence of Flexible and Wearable Electronic Devices | +1.7% | APAC, North America, Europe | Mid to Long-term (2027-2033) |

| Growing Demand for Sustainable and Eco-Friendly Films | +1.4% | Europe, North America | Mid to Long-term (2028-2033) |

| Expansion into Untapped Emerging Markets | +1.1% | Latin America, MEA, Southeast Asia | Long-term (2029-2033) |

| Technological Integration with AI and IoT for Smart Materials | +0.9% | Global | Long-term (2030-2033) |

Plastic Dielectric Film in Electronic Market Challenges Impact Analysis

The Plastic Dielectric Film in Electronic market faces a distinct set of challenges that require innovative solutions and strategic foresight to overcome. One significant challenge is the ongoing need to achieve ultra-thin films while simultaneously enhancing dielectric strength and maintaining mechanical integrity. As electronic devices become more compact and powerful, the demand for thinner films with superior insulating properties intensifies, pushing the boundaries of current material science and manufacturing capabilities. This often involves complex multi-layer structures and precise control over film uniformity, which can be difficult to achieve consistently at scale.

Another critical challenge revolves around managing the thermal properties of dielectric films, especially in high-power and high-frequency applications. Heat dissipation is a major concern in modern electronics, and films must be able to withstand elevated operating temperatures without degradation of their electrical performance. Developing materials that offer both excellent insulation and improved thermal conductivity, or robust thermal stability, is crucial. Additionally, ensuring the long-term reliability and operational stability of these films in harsh environmental conditions, such as high humidity, extreme temperatures, or exposure to chemicals, presents ongoing hurdles for manufacturers, impacting the overall lifespan and performance of electronic devices.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Ultra-Thin Films with High Breakdown Strength | -1.3% | Global | Short to Mid-term (2025-2030) |

| Managing Thermal Properties and Heat Dissipation | -1.1% | Global | Mid to Long-term (2026-2033) |

| Ensuring Long-Term Reliability in Harsh Environments | -0.9% | Global | Mid to Long-term (2027-2033) |

| High Research and Development Costs for Novel Materials | -0.7% | Global | Short to Mid-term (2025-2030) |

| Supply Chain Vulnerability and Geopolitical Risks | -0.6% | Global | Short-term (2025-2027) |

Plastic Dielectric Film in Electronic Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Plastic Dielectric Film in Electronic market, covering historical data from 2019 to 2023, with a detailed forecast extending from 2025 to 2033. The scope includes an assessment of market size, growth drivers, restraints, opportunities, and challenges across various segments and regions. It also incorporates an AI impact analysis and key market trends, offering strategic insights for stakeholders. The report aims to assist industry players in making informed decisions by presenting a holistic view of the market's current state and future potential, emphasizing critical factors influencing its trajectory and competitive landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 3.36 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | DuPont de Nemours, Inc., Toray Industries, Inc., Teijin Limited, Sumitomo Electric Industries, Ltd., Shin-Etsu Chemical Co., Ltd., SKC Co., Ltd., Denka Company Limited, Mitsubishi Chemical Corporation, Kaneka Corporation, UBE Corporation, Celanese Corporation, Arkema S.A., 3M Company, Nitto Denko Corporation, Wipak Group, Avery Dennison Corporation, Coveme SpA, Polyplex Corporation Limited, Treofan Group, Jindal Poly Films Limited |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Plastic Dielectric Film in Electronic market is meticulously segmented to provide a granular understanding of its diverse components and growth avenues. This segmentation allows for a detailed analysis of market dynamics across various material types, application areas, and end-use industries. Such a breakdown is critical for identifying specific market niches, understanding competitive landscapes, and formulating targeted business strategies. Each segment's performance is influenced by unique technological requirements, regulatory frameworks, and market adoption rates, highlighting the complexity and diversity within the broader market.

Analyzing these segments individually and in conjunction provides a holistic view of the market's structure and potential. For instance, the demand for specific film materials like polyimide or polypropylene varies significantly based on the application's thermal, electrical, and mechanical requirements. Similarly, the growth trajectory of applications in electric vehicles differs from that in consumer electronics, driven by distinct innovation cycles and market forces. This comprehensive segmentation analysis is fundamental for understanding the market's current state and forecasting its future evolution.

- By Material: Polypropylene (PP), Polyethylene Terephthalate (PET), Polycarbonate (PC), Polyphenylsulfone (PPS), Polyimide (PI), Polyethylene Naphthalate (PEN), Polytetrafluoroethylene (PTFE), Others

- By Application: Film Capacitors (AC Film Capacitors, DC Film Capacitors), Power Capacitors, Flexible Printed Circuit Boards (FPCBs), Flexible Displays, Touch Panels, Cable Insulation, Insulating Tapes, Sensors, Wearable Devices, Integrated Circuits (IC) Packaging, Others

- By End-use Industry: Consumer Electronics (Smartphones, Laptops, Tablets, TVs), Automotive (EV/HEV, Infotainment, ADAS), Industrial (Power Supplies, Motor Drives), Energy (Renewable Energy Inverters, Grid Systems), Telecommunications (5G Infrastructure, Base Stations), Aerospace & Defense, Medical Devices, Home Appliances, Others

Regional Highlights

- Asia Pacific (APAC): Expected to remain the largest and fastest-growing market due to the presence of a robust electronics manufacturing base, high consumer electronics adoption, and significant investments in electric vehicles and 5G infrastructure, particularly in countries like China, Japan, South Korea, and India.

- North America: Driven by technological advancements, strong R&D activities, demand from the automotive (EV), aerospace, and telecommunications sectors, and increasing adoption of advanced power electronics.

- Europe: Characterized by stringent environmental regulations, a strong focus on sustainable materials, significant investments in renewable energy, and a growing electric vehicle market, particularly in Germany, France, and the UK.

- Latin America: Emerging market with increasing industrialization and growing demand for consumer electronics, presenting long-term growth opportunities as manufacturing capabilities expand.

- Middle East and Africa (MEA): Growing infrastructure development and increasing adoption of digital technologies are expected to drive demand for electronic components, leading to gradual market expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Plastic Dielectric Film in Electronic Market.- DuPont de Nemours, Inc.

- Toray Industries, Inc.

- Teijin Limited

- Sumitomo Electric Industries, Ltd.

- Shin-Etsu Chemical Co., Ltd.

- SKC Co., Ltd.

- Denka Company Limited

- Mitsubishi Chemical Corporation

- Kaneka Corporation

- UBE Corporation

- Celanese Corporation

- Arkema S.A.

- 3M Company

- Nitto Denko Corporation

- Wipak Group

- Avery Dennison Corporation

- Coveme SpA

- Polyplex Corporation Limited

- Treofan Group

- Jindal Poly Films Limited

Frequently Asked Questions

Analyze common user questions about the Plastic Dielectric Film in Electronic market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a plastic dielectric film in electronics?

A plastic dielectric film is a thin, insulating polymer layer used in electronic components like capacitors, printed circuit boards, and flexible electronics. It prevents electrical current flow between conductors while storing electrical energy or providing isolation, crucial for component functionality.

What are the primary applications of plastic dielectric films?

The main applications include film capacitors (for power electronics, automotive, and consumer devices), flexible printed circuit boards, flexible displays, cable insulation, and various insulating tapes in a wide range of electronic devices and systems.

Which factors are driving the growth of this market?

Key drivers include the miniaturization of consumer electronics, the rapid expansion of electric vehicles and renewable energy systems, the rollout of 5G infrastructure, and continuous advancements in flexible and wearable electronic technologies.

What challenges does the market face?

Challenges include the need to produce ultra-thin films with high dielectric strength, effectively manage thermal properties in high-power applications, ensure long-term reliability in harsh operating environments, and navigate volatile raw material prices.

How is AI impacting the plastic dielectric film market?

AI is accelerating material discovery, optimizing manufacturing processes for improved efficiency and quality, enhancing product design through advanced simulations, and aiding in predictive maintenance and supply chain management for film production.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted