Plastic Container Market

Plastic Container Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710286 | Last Updated : January 02, 2026 |

Format : ![]()

![]()

![]()

![]()

Plastic Container Market Size

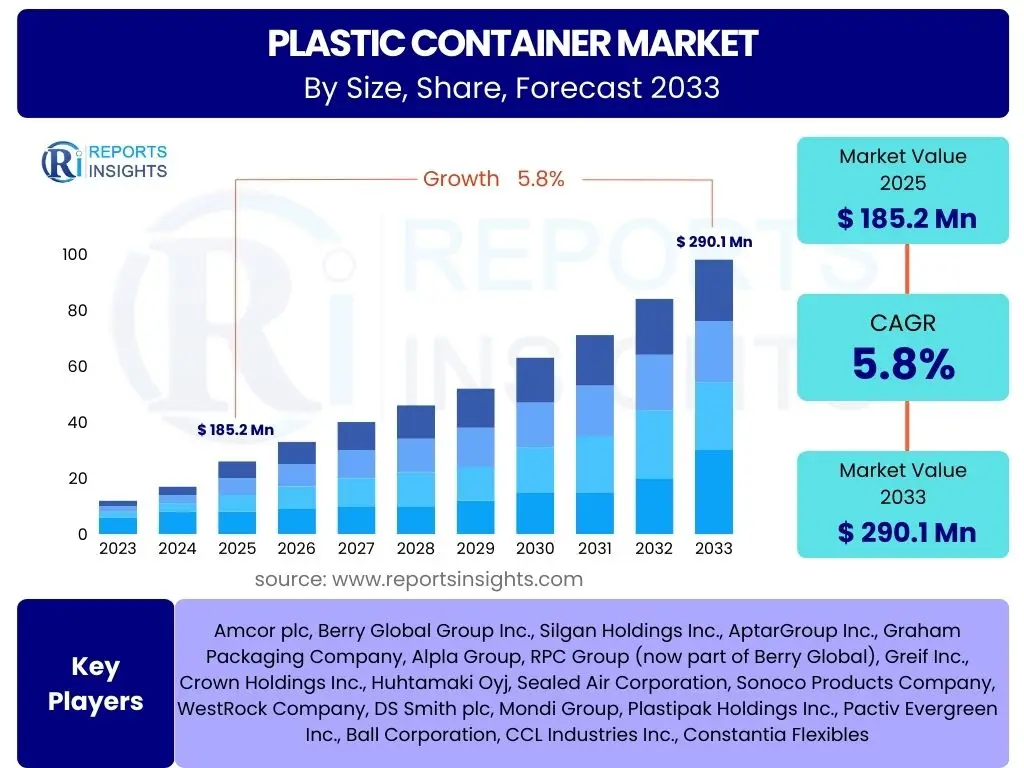

According to Reports Insights Consulting Pvt Ltd, The Plastic Container Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 185.2 billion in 2025 and is projected to reach USD 290.1 billion by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by increasing demand from diverse end-use industries, including food and beverage, healthcare, personal care, and consumer goods, coupled with the inherent advantages of plastic containers such as their lightweight nature, durability, and cost-effectiveness.

The market expansion is further bolstered by global urbanization trends, rising disposable incomes in emerging economies, and the burgeoning e-commerce sector, which necessitates efficient and secure packaging solutions for product delivery. Innovations in material science, focusing on enhanced barrier properties, recyclability, and the integration of recycled content, are also significant contributors to market growth. These advancements address both performance requirements and growing environmental concerns, thereby sustaining the market's long-term viability.

Key Plastic Container Market Trends & Insights

Users frequently inquire about the evolving landscape of the plastic container market, seeking to understand the most impactful trends shaping its future. Common questions revolve around shifts in consumer preferences, technological advancements in manufacturing, the increasing focus on sustainability, and the influence of global economic factors. The market is currently experiencing significant transformations driven by a collective push towards more environmentally responsible solutions, the acceleration of digital commerce, and continuous innovation in material science and production processes.

A predominant trend is the relentless pursuit of sustainability, which encompasses the use of recycled materials (PCR plastics), the development of bio-based and biodegradable plastics, and designs that facilitate easier recycling. Consumers are increasingly favoring brands that demonstrate a commitment to eco-friendly practices, prompting manufacturers to innovate. Furthermore, the expansion of e-commerce has led to a demand for robust, lightweight, and tamper-evident packaging that can withstand the rigors of shipping while minimizing costs. This has spurred innovations in container design and material optimization. Digitalization and automation in manufacturing processes are also gaining traction, enhancing efficiency, reducing waste, and enabling greater customization capabilities within the plastic container industry.

- Increased adoption of Post-Consumer Recycled (PCR) content in packaging.

- Growing demand for lightweight plastic containers to reduce transportation costs and carbon footprint.

- Shift towards flexible packaging solutions, including pouches and films, offering material reduction and convenience.

- Development of bio-based and compostable plastics as alternatives to traditional fossil-based polymers.

- Expansion of smart packaging features, such as QR codes for traceability and NFC tags for consumer engagement.

- Focus on circular economy principles, promoting design for recyclability and reuse systems.

- Customization and personalization of packaging to enhance brand appeal and consumer experience.

AI Impact Analysis on Plastic Container

Users frequently seek to understand the transformative potential of Artificial Intelligence (AI) across various industries, and the plastic container sector is no exception. Common inquiries include how AI can optimize manufacturing processes, enhance supply chain efficiency, aid in sustainable material development, and contribute to the overall competitiveness of the industry. There is significant interest in AI's role in addressing complex challenges, such as waste reduction, predictive maintenance, and creating more resilient operational frameworks.

The integration of AI in the plastic container industry is poised to revolutionize several operational facets. In manufacturing, AI-powered systems can optimize production parameters, predict equipment failures, and ensure consistent quality, leading to reduced downtime and waste. For supply chain management, AI algorithms can forecast demand more accurately, optimize logistics routes, and manage inventory levels efficiently, thereby lowering operational costs and improving delivery times. Furthermore, AI is increasingly being applied in research and development to accelerate the discovery of new, sustainable plastic materials and to design containers with improved functional properties and enhanced recyclability. This analytical capability of AI offers the potential for significant advancements in efficiency, sustainability, and innovation throughout the plastic container value chain.

- AI-driven optimization of injection molding and blow molding processes for improved efficiency and reduced material waste.

- Predictive maintenance programs leveraging AI to minimize equipment downtime and extend machinery lifespan.

- Enhanced supply chain visibility and demand forecasting through AI algorithms, leading to optimized inventory management.

- AI-powered quality control systems for real-time defect detection and improved product consistency.

- Accelerated research and development of sustainable plastic materials and recyclable container designs using AI simulation.

- Personalized packaging design and production facilitated by AI for mass customization.

- Robotics and automation, often AI-driven, improving handling, sorting, and packing efficiency in facilities.

Key Takeaways Plastic Container Market Size & Forecast

Stakeholders frequently ask for a concise summary of the most critical insights derived from the plastic container market size and forecast data. They want to know the primary drivers of growth, the segments offering the most promising opportunities, and the overarching factors that will dictate market evolution over the forecast period. The focus is on understanding the actionable intelligence that can inform strategic decision-making and investment planning within the dynamic market landscape.

The plastic container market is set for sustained growth, primarily fueled by robust demand from essential end-use industries and the expanding reach of e-commerce. A crucial takeaway is the pervasive influence of sustainability, which is transforming product development, manufacturing processes, and consumer choices. Companies prioritizing eco-friendly materials and circular economy principles are likely to gain significant competitive advantages. Regional market dynamics also play a vital role, with emerging economies in Asia Pacific and Latin America demonstrating particularly high growth potential due to urbanization and increasing consumption. Navigating regulatory landscapes and investing in technological advancements, including AI for operational efficiency and material innovation, will be paramount for long-term success in this evolving market.

- The market is poised for significant expansion, driven by strong fundamentals in key end-use sectors and global economic development.

- Sustainability initiatives, including PCR adoption and bio-based plastics, are not just trends but essential drivers shaping future market dynamics.

- E-commerce growth continues to be a powerful catalyst, increasing demand for protective, lightweight, and cost-effective plastic packaging.

- Technological innovation in manufacturing processes and material science is critical for maintaining competitiveness and addressing environmental challenges.

- Emerging economies present substantial growth opportunities, necessitating localized strategies for market penetration.

- Regulatory pressures concerning plastic waste management will intensify, requiring proactive industry adaptation and collaboration.

- Investment in automation and AI will be key to enhancing operational efficiency, quality, and supply chain resilience.

Plastic Container Market Drivers Analysis

The plastic container market is propelled by a confluence of factors that underscore the material's versatility, economic viability, and functional attributes. A primary driver is the pervasive demand from the food and beverage industry, where plastic containers offer excellent barrier properties, lightweight design, and shatter resistance, crucial for product preservation and safe transportation. The convenience offered by plastic packaging, such as ease of opening, resealability, and portability, aligns well with modern consumer lifestyles characterized by busy schedules and on-the-go consumption.

Furthermore, the rapid expansion of the e-commerce sector globally significantly boosts the demand for plastic containers. These containers provide the necessary protection during shipping, reduce weight for freight cost optimization, and often allow for clear product visibility. Urbanization trends, particularly in developing regions, lead to increased consumption of packaged goods, directly stimulating the plastic container market. Innovations in plastic resins, including the development of high-performance polymers with enhanced barrier properties and lighter weight, continually expand the applications and appeal of plastic packaging across various sectors, ensuring its sustained market relevance.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand from Food & Beverage Industry | +2.8% | Global, particularly APAC & Latin America | Long-term (2025-2033) |

| Increasing E-commerce Penetration | +2.5% | North America, Europe, APAC | Mid to Long-term (2025-2033) |

| Lightweighting and Cost-Effectiveness Benefits | +1.9% | Global | Long-term (2025-2033) |

| Urbanization and Rising Disposable Incomes | +1.5% | APAC, MEA, Latin America | Long-term (2025-2033) |

| Innovations in Material Science (e.g., barrier properties) | +1.2% | Global | Mid-term (2025-2030) |

Plastic Container Market Restraints Analysis

Despite its significant growth, the plastic container market faces several formidable restraints that could impede its trajectory. Foremost among these are the escalating environmental concerns surrounding plastic waste and pollution. Public awareness and pressure from environmental advocacy groups have intensified, leading to a negative perception of plastics and calls for reduced usage. This scrutiny has translated into stringent governmental regulations targeting single-use plastics, imposing bans, taxes, and extended producer responsibility (EPR) schemes in numerous countries, which directly impacts market growth, particularly in mature economies.

Another significant restraint is the volatility in raw material prices, primarily crude oil and natural gas, which are key feedstocks for plastic production. Fluctuations in these commodity prices introduce uncertainty into manufacturing costs, affecting profitability and investment decisions across the value chain. Furthermore, the increasing availability and adoption of alternative packaging materials, such as glass, metal, paper, and compostable solutions, pose a competitive threat. As consumers and industries seek more sustainable or perception-friendly options, these alternatives can divert market share away from traditional plastic containers. The challenge of developing cost-effective and truly scalable recycling infrastructure also remains a substantial hurdle, limiting the market's ability to fully embrace circular economy principles.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Environmental Concerns and Negative Perception of Plastics | -2.1% | Global, particularly Europe & North America | Long-term (2025-2033) |

| Stringent Government Regulations and Bans on Single-Use Plastics | -1.8% | Europe, North America, parts of APAC | Mid to Long-term (2025-2033) |

| Volatility in Raw Material Prices (e.g., crude oil) | -1.5% | Global | Short to Mid-term (2025-2028) |

| Competition from Alternative Packaging Materials | -1.0% | Global | Long-term (2025-2033) |

| Challenges in Recycling Infrastructure and Cost-Effectiveness | -0.8% | Global | Long-term (2025-2033) |

Plastic Container Market Opportunities Analysis

Amidst the challenges, the plastic container market presents numerous opportunities for growth and innovation. A significant avenue lies in the relentless pursuit of sustainable packaging solutions. This includes the widespread adoption of recycled plastics, especially Post-Consumer Recycled (PCR) content, which helps to mitigate environmental impact and meet regulatory requirements. The development and commercialization of bio-based and biodegradable plastics, offering alternatives to traditional fossil-derived materials, represent another burgeoning opportunity. As technology advances and production costs decrease, these materials are expected to gain greater market traction.

The increasing demand for customized and personalized packaging offers a robust growth opportunity for manufacturers. Brands are seeking unique designs and specialized features to differentiate products and enhance consumer engagement, which plastic containers are well-suited to provide due to their design flexibility. Furthermore, the expansion into emerging markets, particularly in Asia Pacific, Latin America, and the Middle East & Africa, where consumer demand for packaged goods is rapidly rising alongside economic development and urbanization, provides fertile ground for market expansion. Strategic investments in these regions, coupled with localized product offerings, can unlock substantial market share. Lastly, the integration of smart packaging technologies, such as IoT sensors for freshness monitoring or QR codes for enhanced traceability and consumer interaction, can add significant value and open new revenue streams.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and Adoption of Sustainable Packaging Solutions (PCR, Bio-based) | +3.5% | Global, particularly Europe & North America | Long-term (2025-2033) |

| Growth in Emerging Economies and Untapped Markets | +3.0% | APAC, Latin America, MEA | Long-term (2025-2033) |

| Increasing Demand for Customized and Smart Packaging | +2.2% | North America, Europe, parts of APAC | Mid to Long-term (2025-2033) |

| Technological Advancements in Manufacturing Processes | +1.8% | Global | Mid-term (2025-2030) |

| Application Expansion in Healthcare and Pharmaceutical Sector | +1.5% | Global | Long-term (2025-2033) |

Plastic Container Market Challenges Impact Analysis

The plastic container market is navigating a complex landscape marked by significant challenges that demand strategic responses from industry players. One of the most pressing issues is the public perception of plastics, which is heavily influenced by concerns about environmental pollution and the inadequacy of waste management systems globally. This negative perception directly impacts consumer choices and brand reputation, compelling companies to invest heavily in sustainable alternatives and communication strategies to reassure stakeholders. The sheer volume of plastic waste generated annually, coupled with insufficient recycling infrastructure in many regions, exacerbates these concerns and creates a bottleneck for circular economy initiatives.

Another critical challenge is the evolving and increasingly stringent regulatory environment. Governments worldwide are implementing stricter policies on plastic production, usage, and disposal, including bans on certain single-use plastics, mandatory recycled content targets, and extended producer responsibility (EPR) schemes. These regulations necessitate significant investments in research and development for new materials, redesign of existing products, and adaptation of manufacturing processes, adding to operational complexities and costs. Furthermore, competition from established and emerging sustainable alternative materials, such as glass, aluminum, paperboard, and innovative compostable solutions, continues to intensify, requiring plastic container manufacturers to continuously innovate and demonstrate the value proposition of their products. Navigating these challenges effectively will require a proactive approach to sustainability, regulatory compliance, and technological differentiation.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Public Perception and Environmental Scrutiny | -1.8% | Global | Long-term (2025-2033) |

| Complexity of Global Waste Management and Recycling Systems | -1.5% | Global | Long-term (2025-2033) |

| Navigating Evolving Regulatory Landscape and Policy Changes | -1.2% | Europe, North America, parts of APAC | Mid to Long-term (2025-2033) |

| High Investment Required for Sustainable Innovations and Infrastructure | -0.9% | Global | Mid to Long-term (2025-2033) |

| Cost and Scalability of Bio-based and Degradable Alternatives | -0.7% | Global | Short to Mid-term (2025-2029) |

Plastic Container Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the plastic container market, offering a detailed segmentation, competitive landscape assessment, and regional insights from 2019 to 2033. It covers critical market dynamics, including drivers, restraints, opportunities, and challenges, alongside the significant impact of emerging technologies like Artificial Intelligence. The scope encompasses detailed market sizing, forecasting, and trend analysis to equip stakeholders with actionable intelligence for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 185.2 billion |

| Market Forecast in 2033 | USD 290.1 billion |

| Growth Rate | 5.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amcor plc, Berry Global Group Inc., Silgan Holdings Inc., AptarGroup Inc., Graham Packaging Company, Alpla Group, RPC Group (now part of Berry Global), Greif Inc., Crown Holdings Inc., Huhtamaki Oyj, Sealed Air Corporation, Sonoco Products Company, WestRock Company, DS Smith plc, Mondi Group, Plastipak Holdings Inc., Pactiv Evergreen Inc., Ball Corporation, CCL Industries Inc., Constantia Flexibles |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) | Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The plastic container market is extensively segmented to provide a granular understanding of its diverse components and dynamics. This segmentation facilitates a detailed analysis of various material types, container forms, application industries, and manufacturing processes, enabling stakeholders to identify specific growth areas and market niches. Each segment reacts differently to market drivers, restraints, and opportunities, influenced by technological advancements, regulatory changes, and evolving consumer preferences.

Understanding these segments is crucial for strategic planning, product development, and market entry strategies. For instance, the material segmentation highlights the dominance and growth of PET and PP due to their versatility and recyclability, while the end-use industry analysis points to the sustained demand from the food & beverage and healthcare sectors. The diverse array of container types reflects the wide range of packaging needs across various product categories, emphasizing the importance of design flexibility and functional performance in the market.

- By Material:

- Polyethylene Terephthalate (PET)

- Polypropylene (PP)

- High-Density Polyethylene (HDPE)

- Low-Density Polyethylene (LDPE)

- Polyvinyl Chloride (PVC)

- Polystyrene (PS)

- Others (e.g., Polycarbonate, Nylon)

- By Type:

- Bottles (Beverage, Personal Care, Household)

- Jars (Food, Cosmetics)

- Tubs (Dairy, Spreads)

- Cups (Beverage, Yogurt)

- Boxes & Crates (Industrial, Agriculture)

- Trays (Food, Retail)

- Bags & Pouches (Snacks, Liquid, Flexible Packaging)

- Films & Wraps (Food Wrapping, Industrial)

- Others

- By End-Use Industry:

- Food & Beverage (Packaged Food, Dairy, Beverages, Confectionery)

- Healthcare (Pharmaceuticals, Medical Devices, Nutraceuticals)

- Personal Care & Cosmetics (Skincare, Haircare, Makeup)

- Industrial Packaging (Chemicals, Automotive, Agriculture)

- Consumer Goods (Household Cleaning, Electronics, Toys)

- Others (e.g., Building & Construction, Textiles)

- By Process:

- Injection Molding

- Blow Molding (Extrusion Blow Molding, Injection Blow Molding)

- Thermoforming

- Extrusion

- Others (e.g., Rotational Molding, Compression Molding)

Regional Highlights

- North America: This region is characterized by high consumption of packaged goods and a robust e-commerce sector. Strict regulations regarding recycled content and sustainability are driving innovation towards eco-friendly plastic container solutions. Demand from the food & beverage, pharmaceutical, and personal care industries remains consistently strong.

- Europe: Europe is at the forefront of the circular economy transition, with stringent environmental regulations and ambitious recycling targets heavily influencing the plastic container market. There is a strong emphasis on PCR content, design for recyclability, and the exploration of bio-based alternatives, particularly in countries like Germany, France, and the UK.

- Asia Pacific (APAC): APAC represents the largest and fastest-growing market for plastic containers, fueled by rapid urbanization, rising disposable incomes, and the expansion of the middle-class population. Countries like China, India, and Southeast Asian nations are experiencing significant growth in packaged food, beverages, and personal care products, driving substantial demand.

- Latin America: This region shows significant growth potential due to increasing consumer spending, developing retail infrastructure, and expanding manufacturing sectors. Brazil and Mexico are key markets, with rising demand for convenient and affordable plastic packaging solutions across various end-use industries.

- Middle East and Africa (MEA): The MEA region is witnessing steady growth in the plastic container market, driven by infrastructure development, increasing population, and growing consumer demand for packaged goods. Investments in food processing and manufacturing capabilities are contributing to the regional market expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Plastic Container Market.- Amcor plc

- Berry Global Group Inc.

- Silgan Holdings Inc.

- AptarGroup Inc.

- Graham Packaging Company

- Alpla Group

- Greif Inc.

- Huhtamaki Oyj

- Sealed Air Corporation

- Sonoco Products Company

- WestRock Company

- DS Smith plc

- Mondi Group

- Plastipak Holdings Inc.

- Pactiv Evergreen Inc.

- Ball Corporation

- CCL Industries Inc.

- Constantia Flexibles

- Tekni-Plex, Inc.

- Resilux NV

Frequently Asked Questions

What is the projected growth rate of the plastic container market?

The plastic container market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, reaching an estimated USD 290.1 billion by 2033.

What are the primary drivers of growth in the plastic container market?

Key growth drivers include increasing demand from the food and beverage industry, the expansion of e-commerce, the benefits of lightweight and cost-effective packaging, urbanization, and continuous innovations in material science.

How is sustainability impacting the plastic container market?

Sustainability is a major trend, driving the adoption of Post-Consumer Recycled (PCR) content, the development of bio-based plastics, and designs focused on recyclability to meet evolving consumer preferences and stringent environmental regulations.

Which regions offer the most significant growth opportunities?

The Asia Pacific region, particularly countries like China and India, alongside Latin America and the Middle East & Africa, offer significant growth opportunities due to rapid urbanization, rising disposable incomes, and expanding consumer markets.

What challenges does the plastic container market face?

Major challenges include negative public perception due to environmental concerns, stringent government regulations on plastic use, volatility in raw material prices, and increasing competition from alternative packaging materials.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted