Plastic and Competitive Pipe Market

Plastic and Competitive Pipe Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709707 | Last Updated : December 12, 2025 |

Format : ![]()

![]()

![]()

![]()

Plastic and Competitive Pipe Market Size

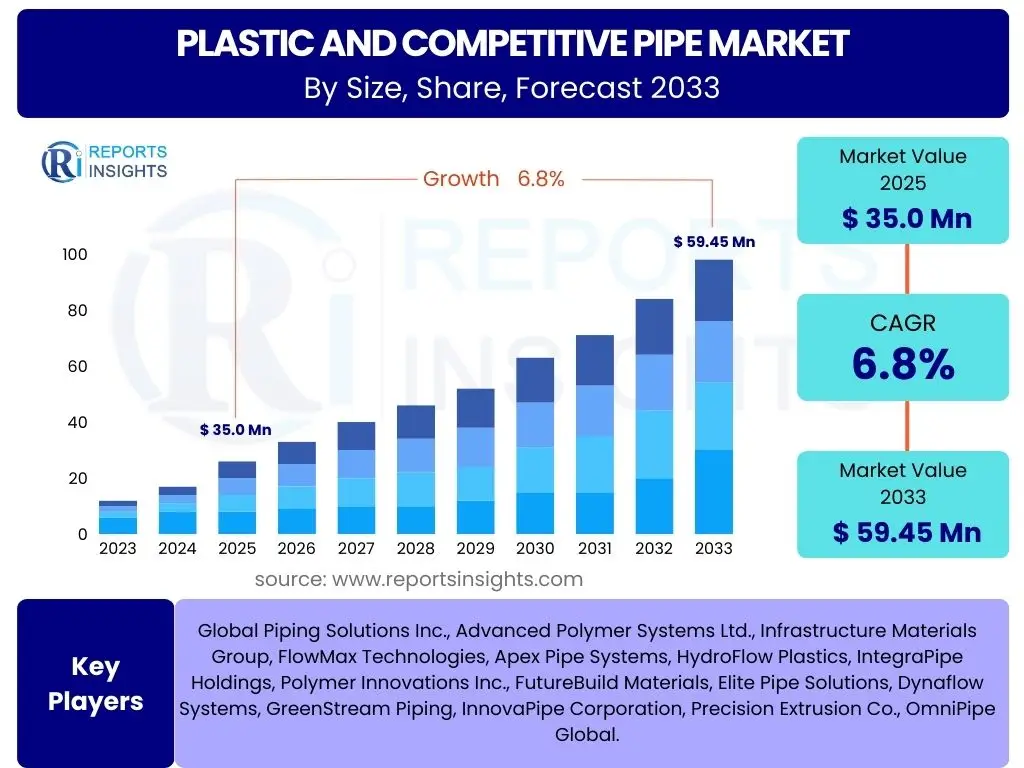

According to Reports Insights Consulting Pvt Ltd, The Plastic and Competitive Pipe Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. This robust growth trajectory is underpinned by increasing global infrastructure development, urbanization trends, and the inherent advantages offered by plastic piping solutions over traditional materials. The market's expansion is further fueled by continuous advancements in material science and manufacturing processes, leading to the development of more durable, efficient, and cost-effective pipe systems.

The market is estimated at USD 35.0 Billion in 2025 and is projected to reach USD 59.45 Billion by the end of the forecast period in 2033. This substantial increase reflects a growing preference for plastic and composite pipe materials across various end-use sectors, including water and wastewater management, oil and gas, agriculture, and chemical processing. The long-term forecast indicates sustained demand driven by both new construction projects and the replacement of aging infrastructure, highlighting the critical role these piping solutions play in modern societal and industrial frameworks.

Key Plastic and Competitive Pipe Market Trends & Insights

User inquiries frequently center on the evolving landscape of materials, sustainability initiatives, and technological advancements within the plastic and competitive pipe market. A prominent theme is the shift towards higher performance and more environmentally friendly materials, alongside the integration of smart technologies. There is significant interest in how manufacturers are addressing issues such as pipe longevity, installation efficiency, and the overall carbon footprint of their products, reflecting a market driven by both economic and ecological considerations.

Another crucial area of user focus involves the competitive dynamics between different pipe materials, particularly the ongoing innovation in plastic composites that aim to challenge traditional materials like steel and concrete. Questions also arise regarding the adoption of trenchless technologies and modular construction methods, which streamline installation and reduce project timelines. The emphasis on resource efficiency and compliance with stricter environmental regulations is clearly shaping the strategic directions of companies operating within this dynamic market.

- Increased adoption of trenchless installation technologies, reducing disruption and costs.

- Growing demand for multi-layer composite pipes offering enhanced performance and durability.

- Focus on sustainable and recycled plastic content in pipe manufacturing to reduce environmental impact.

- Integration of smart sensing capabilities for leak detection and predictive maintenance in piping networks.

- Expansion of specialized pipe applications in district heating/cooling and renewable energy infrastructure.

- Regional shifts in manufacturing and supply chain optimization to cater to localized demand and reduce logistics costs.

AI Impact Analysis on Plastic and Competitive Pipe

Common user questions regarding AI's impact on the plastic and competitive pipe sector highlight curiosity about efficiency gains, cost reductions, and enhanced product quality. Users are keen to understand how AI can optimize manufacturing processes, predict material failures, and improve supply chain logistics. The primary expectation is that AI will automate complex tasks, provide data-driven insights for better decision-making, and ultimately lead to more resilient and intelligent piping systems capable of long-term, reliable performance with minimal human intervention.

Furthermore, there is considerable interest in AI's role in product design and development, particularly in simulating material properties and performance under various stress conditions to accelerate innovation. Concerns often revolve around the initial investment costs, the need for specialized skills, and data privacy issues associated with AI implementation. However, the overall sentiment points towards AI as a transformative force capable of revolutionizing not just the production but also the operational and maintenance aspects of piping infrastructure, driving significant advancements across the value chain.

- AI-driven optimization of manufacturing processes for reduced waste and improved efficiency.

- Predictive maintenance analytics for pipe networks, minimizing downtime and extending asset life.

- Enhanced quality control through AI-powered visual inspection systems detecting microscopic defects.

- Supply chain optimization using AI algorithms for inventory management and logistics routing.

- AI-assisted material science research for developing advanced pipe composites and polymers.

- Automated design and simulation tools accelerating new product development and customization.

Key Takeaways Plastic and Competitive Pipe Market Size & Forecast

Analysis of user questions regarding market size and forecast consistently reveals a focus on the underlying drivers of growth, particularly global infrastructure investments and the shift towards modern piping solutions. Users seek clarity on which regions are experiencing the most significant expansion and the specific product types that are expected to dominate the market. The overarching insight is that the market's trajectory is strongly linked to sustainable urban development and industrial modernization, emphasizing efficiency and durability.

Another key area of interest is the impact of evolving regulatory landscapes and environmental considerations on market demand. The market is clearly poised for substantial growth, driven by both replacement demand in mature economies and new infrastructure development in emerging regions. Stakeholders are keen to understand the long-term viability and competitive advantages of plastic and composite pipes, indicating a strategic shift from traditional materials towards advanced polymer solutions that offer superior performance and a reduced total cost of ownership over their lifecycle.

- Significant market expansion driven by global urbanization and infrastructure spending.

- Strong preference for plastic and composite pipes due to their durability, corrosion resistance, and cost-effectiveness.

- Emerging economies present substantial growth opportunities due to rapid industrialization and construction activities.

- Technological advancements in pipe materials and manufacturing are critical for sustained competitive advantage.

- Emphasis on sustainable practices and circular economy principles is increasingly influencing market dynamics and product development.

Plastic and Competitive Pipe Market Drivers Analysis

The plastic and competitive pipe market is fundamentally propelled by a confluence of macroeconomic and technological factors. Rapid urbanization globally necessitates extensive infrastructure development, particularly in water, wastewater, and gas distribution systems, where the advantages of plastic pipes are increasingly recognized. Government initiatives worldwide focusing on improving civic amenities and industrial capabilities further bolster demand. The inherent characteristics of plastic pipes, such as corrosion resistance, light weight, and ease of installation, offer significant long-term operational and cost benefits compared to traditional materials, making them a preferred choice across numerous applications.

Furthermore, the escalating demand for efficient and resilient infrastructure in critical sectors like agriculture and energy transmission underscores the market's robust growth. Innovations in polymer science continually enhance pipe performance, enabling their use in more demanding environments and specialized applications. As resource scarcity, particularly water, becomes a global concern, the need for leak-proof and durable piping systems drives the adoption of advanced plastic solutions. This broad appeal, coupled with economic efficiencies, establishes a strong foundation for continued market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Urbanization and Infrastructure Development | +1.5% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2025-2033) |

| Superior Properties (Corrosion Resistance, Longevity, Lightweight) | +1.2% | North America, Europe (Replacement Markets) | Medium to Long-term (2025-2033) |

| Increasing Demand for Water and Wastewater Management | +1.0% | Global, particularly water-stressed regions | Long-term (2025-2033) |

| Cost-Effectiveness and Ease of Installation | +0.8% | All Regions, especially cost-sensitive markets | Short to Medium-term (2025-2029) |

| Advancements in Polymer Technology | +0.6% | Developed Economies (Innovation Hubs) | Medium to Long-term (2026-2033) |

Plastic and Competitive Pipe Market Restraints Analysis

Despite significant growth prospects, the plastic and competitive pipe market faces several considerable restraints that could temper its expansion. One primary challenge is the volatility in raw material prices, particularly for petrochemical derivatives used in plastic production. Fluctuations in crude oil prices directly impact manufacturing costs, potentially compressing profit margins and leading to price instability for end-users. This unpredictability can make long-term project planning difficult for construction and infrastructure companies, occasionally leading to delays or a reevaluation of material choices.

Another significant restraint stems from environmental concerns and increasing regulatory scrutiny surrounding plastic waste and its impact on ecosystems. Public perception regarding plastics, especially single-use plastics, can indirectly affect the pipe market, even though durable pipe systems represent a different category of plastic usage. Competition from traditional pipe materials like ductile iron, concrete, and steel, which continue to evolve with new coatings and manufacturing techniques, also poses a competitive challenge. Additionally, certain niche applications may still require the structural rigidity or high-temperature resistance predominantly offered by non-plastic alternatives, limiting plastic pipe penetration in those specific segments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility (Petrochemicals) | -0.8% | Global | Short to Medium-term (2025-2029) |

| Environmental Concerns and Regulations on Plastics | -0.7% | Europe, North America, Developing Economies (Emerging Regulations) | Medium to Long-term (2026-2033) |

| Competition from Traditional Pipe Materials | -0.5% | Global (Specific applications) | Medium to Long-term (2025-2033) |

| Limited Use in Extreme High-Temperature/Pressure Applications | -0.3% | Industrial Sector | Long-term (2025-2033) |

| Perception Issues (Durability vs. Sustainability) | -0.2% | Developed Markets | Medium-term (2025-2030) |

Plastic and Competitive Pipe Market Opportunities Analysis

The plastic and competitive pipe market is ripe with opportunities, primarily driven by the global imperative for sustainable development and technological innovation. The increasing focus on smart cities and resilient infrastructure creates a demand for advanced piping systems equipped with monitoring capabilities and enhanced longevity. This trend presents a significant avenue for manufacturers to integrate sensors and IoT devices into pipes, offering solutions for real-time leak detection, pressure monitoring, and predictive maintenance, thereby extending the service life of water and gas networks and minimizing waste.

Furthermore, the growing emphasis on circular economy principles and recycling initiatives opens doors for innovation in pipe manufacturing. Companies that invest in developing pipes from recycled plastics or create easily recyclable pipe systems can gain a substantial competitive advantage and appeal to environmentally conscious consumers and governments. The expansion of specialized applications, such as pipes for geothermal energy systems, district cooling, and advanced agricultural irrigation, also represents untapped potential. These niche markets often require specific material properties and design flexibility, areas where plastic pipes excel, thus offering robust growth prospects beyond conventional applications.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of Smart Technologies (IoT, Sensors) | +1.0% | Developed Economies, Smart City Initiatives | Medium to Long-term (2026-2033) |

| Growth in Sustainable & Recycled Content Pipes | +0.9% | Europe, North America, ESG-focused markets | Medium to Long-term (2026-2033) |

| Expansion into Specialized Applications (Geothermal, Agri-Tech) | +0.7% | Global, particularly regions with specific resource needs | Medium to Long-term (2026-2033) |

| Modernization of Aging Infrastructure (Replacement Demand) | +0.6% | North America, Europe, Japan | Long-term (2025-2033) |

| Developing Markets' Infrastructure Catch-up | +0.5% | Asia Pacific, Africa, Latin America | Long-term (2025-2033) |

Plastic and Competitive Pipe Market Challenges Impact Analysis

The plastic and competitive pipe market faces several inherent challenges that demand strategic responses from manufacturers and stakeholders. A significant hurdle is the public and regulatory scrutiny regarding the environmental impact of plastic materials. While plastic pipes offer long service lives, concerns about microplastic pollution, end-of-life management, and recycling infrastructure gaps can influence market acceptance and drive stringent regulations. This necessitates continuous innovation in sustainable materials and robust recycling programs to ensure the industry's long-term viability and public trust.

Another challenge is the intense competition from well-established traditional pipe materials, which, despite some drawbacks, continue to hold a strong market share in certain applications due to historical precedence, existing infrastructure, or perceived robustness. Overcoming this requires sustained efforts in demonstrating the superior performance, lower total cost of ownership, and environmental benefits of plastic and composite pipes. Furthermore, a shortage of skilled labor for advanced pipe installation and maintenance, particularly for complex systems, can hinder project execution and market expansion in certain regions. Addressing these multifaceted challenges is crucial for the industry to maintain its growth trajectory and fully capitalize on emerging opportunities.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Regulatory and Public Pressure on Plastic Usage | -0.6% | Global, especially Western Europe | Medium to Long-term (2025-2033) |

| Competition and Market Acceptance of New Materials | -0.5% | All Regions, particularly in conservative markets | Long-term (2025-2033) |

| Complexity of Recycling and End-of-Life Management | -0.4% | Developed Economies | Medium to Long-term (2026-2033) |

| Skilled Labor Shortage for Installation | -0.3% | North America, Europe | Short to Medium-term (2025-2030) |

| Initial Capital Investment for Advanced Manufacturing | -0.2% | Developing Economies | Short-term (2025-2028) |

Plastic and Competitive Pipe Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Plastic and Competitive Pipe Market, encompassing its historical performance, current dynamics, and future projections. The scope meticulously details market sizing, segmentation across various types, applications, and end-uses, along with a thorough regional breakdown. It also offers a detailed examination of key market trends, drivers, restraints, opportunities, and challenges, providing a holistic view for strategic decision-making. The report identifies and profiles leading industry players, offering insights into their competitive strategies and market positioning to equip stakeholders with actionable intelligence for navigating this evolving landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 35.0 Billion |

| Market Forecast in 2033 | USD 59.45 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Piping Solutions Inc., Advanced Polymer Systems Ltd., Infrastructure Materials Group, FlowMax Technologies, Apex Pipe Systems, HydroFlow Plastics, IntegraPipe Holdings, Polymer Innovations Inc., FutureBuild Materials, Elite Pipe Solutions, Dynaflow Systems, GreenStream Piping, InnovaPipe Corporation, Precision Extrusion Co., OmniPipe Global. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The plastic and competitive pipe market is extensively segmented to reflect the diverse applications and material preferences across various industries and geographies. This segmentation is crucial for understanding specific market dynamics, identifying growth pockets, and tailoring product development to meet specialized requirements. The primary segmentation categories encompass pipe type, application, and end-use industry, each characterized by distinct performance criteria, material compositions, and installation methods. The dominance of certain plastic types like PVC and PE in volume terms highlights their versatility and cost-effectiveness, while specialized polymers and composites cater to more demanding environments.

The application-based segmentation further delineates market demand, with water supply and wastewater management representing significant traditional strongholds for plastic pipes due to their corrosion resistance and leak-proof properties. Emerging applications in energy transmission, telecommunications, and advanced agricultural irrigation are driving innovation in material science and pipe design. The end-use industry analysis, covering residential, commercial, industrial, municipal, and agricultural sectors, provides insights into the varying procurement processes, regulatory compliance, and project scales, underscoring the fragmented yet expansive nature of the plastic and competitive pipe market.

- By Type: Polyvinyl Chloride (PVC) Pipes, Polyethylene (PE) Pipes, Polypropylene (PP) Pipes, Acrylonitrile Butadiene Styrene (ABS) Pipes, Fiberglass Reinforced Plastic (FRP) Pipes, and Other Plastic Pipes. PVC and PE remain foundational due to their cost-efficiency and versatility, while FRP and specialized polymers address high-performance needs.

- By Application: Water Supply & Distribution, Wastewater & Drainage, Oil & Gas, Agriculture & Irrigation, HVAC & Radiant Heating/Cooling, Chemical & Industrial Processes, Power & Telecommunications, Mining, and Building & Construction. Infrastructure development and resource management are key drivers across these segments.

- By End-Use Industry: Residential, Commercial, Industrial, Municipal, and Agricultural. Each industry presents unique demands regarding pipe durability, regulatory compliance, and installation scalability.

Regional Highlights

- North America: Characterized by significant investment in replacing aging water and wastewater infrastructure. The demand for durable, corrosion-resistant plastic pipes is high, driven by municipal projects and residential construction. Innovations in trenchless technologies and smart piping solutions are gaining traction.

- Europe: A mature market with strong emphasis on sustainability, energy efficiency, and regulatory compliance. Adoption of recycled plastic content in pipes and advanced materials for district heating and cooling systems is prevalent. Germany, the UK, and France are key contributors to market value.

- Asia Pacific (APAC): The fastest-growing region, fueled by rapid urbanization, industrialization, and massive infrastructure development projects, particularly in China, India, and Southeast Asian countries. High demand for water supply, irrigation, and building construction applications. Government initiatives like "Smart Cities" further accelerate growth.

- Latin America: Experiencing consistent growth due to expanding construction activities and improving access to potable water and sanitation. Brazil and Mexico are leading markets, with increasing adoption of plastic pipes for both municipal and agricultural purposes. Economic stability and foreign investment are crucial for market expansion.

- Middle East & Africa (MEA): Marked by substantial investments in oil and gas infrastructure, water desalination projects, and urban development, especially in the GCC countries. Demand for large-diameter pipes for water transmission and irrigation is high. Infrastructure reconstruction in certain African nations also contributes to market growth.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Plastic and Competitive Pipe Market.- Global Piping Solutions Inc.

- Advanced Polymer Systems Ltd.

- Infrastructure Materials Group

- FlowMax Technologies

- Apex Pipe Systems

- HydroFlow Plastics

- IntegraPipe Holdings

- Polymer Innovations Inc.

- FutureBuild Materials

- Elite Pipe Solutions

- Dynaflow Systems

- GreenStream Piping

- InnovaPipe Corporation

- Precision Extrusion Co.

- OmniPipe Global

- Resourceful Tubes Inc.

- Unified Pipe Networks

- Vanguard Polymer Products

- Waterfront Pipe Co.

- Zenix Flow Solutions

Frequently Asked Questions

Analyze common user questions about the Plastic and Competitive Pipe market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are the primary growth drivers for the Plastic and Competitive Pipe Market?

The market is primarily driven by global urbanization, extensive infrastructure development in emerging economies, increasing demand for efficient water and wastewater management systems, and the superior performance properties of plastic pipes such as corrosion resistance and longevity compared to traditional materials. Ease of installation and cost-effectiveness also contribute significantly.

Which types of plastic pipes are most commonly used and for what applications?

Polyvinyl Chloride (PVC) and Polyethylene (PE) pipes are the most common types. PVC pipes are widely used for water supply, drainage, and sewage systems due to their rigidity and chemical resistance. PE pipes, particularly HDPE, are favored for gas distribution, water main lines, and agricultural irrigation because of their flexibility, durability, and resistance to extreme temperatures.

How do environmental concerns impact the Plastic Pipe Market?

Environmental concerns drive innovation towards sustainable solutions, including pipes made from recycled plastics and those designed for long service life to reduce waste. Regulations aimed at reducing plastic waste and promoting circular economy principles influence manufacturing processes and product development, pushing companies to adopt more eco-friendly practices and materials.

What role does technology play in the future of the Plastic and Competitive Pipe Market?

Technology plays a crucial role through advancements in material science for improved pipe performance, manufacturing automation for efficiency, and the integration of smart technologies like IoT sensors for real-time monitoring and predictive maintenance. AI is increasingly used for optimizing design, production, and supply chain management, leading to more resilient and intelligent piping networks.

Which regions offer the most significant growth opportunities for plastic pipes?

The Asia Pacific region, particularly countries like China and India, offers the most significant growth opportunities due to rapid urbanization, industrialization, and substantial infrastructure development projects. Additionally, emerging economies in Latin America, the Middle East, and Africa present considerable potential as they modernize their public utilities and industrial infrastructure.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted