Plant based Water Market

Plant based Water Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700120 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

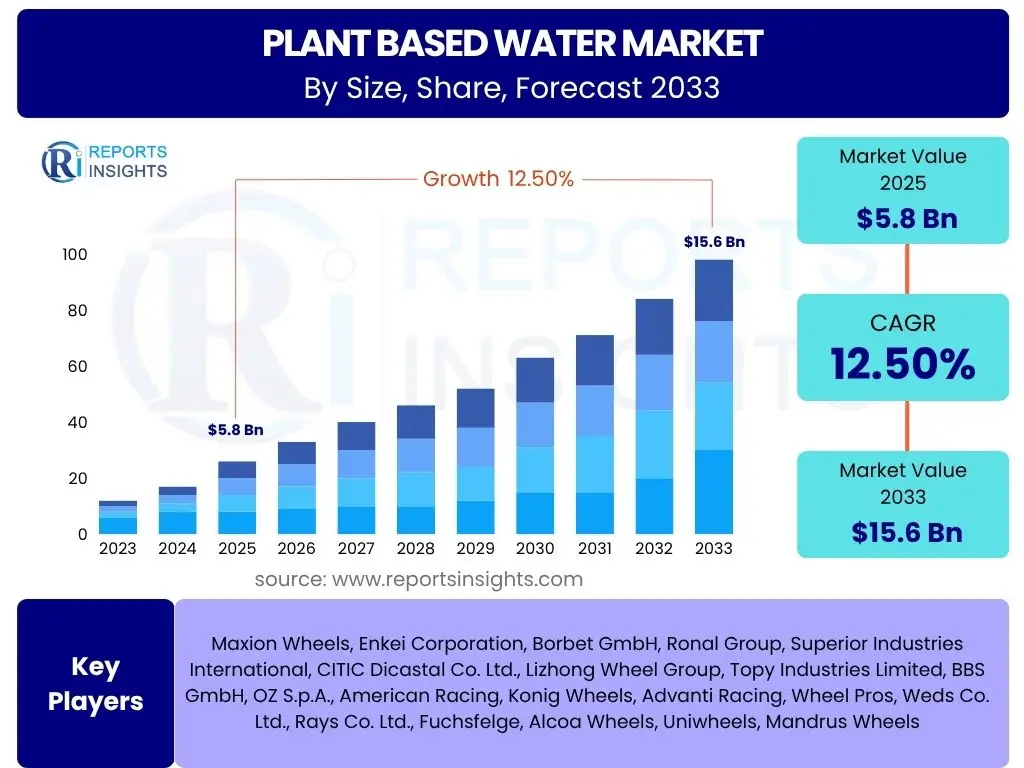

Plant based Water Market is projected to grow at a Compound annual growth rate (CAGR) of 12.5% between 2025 and 2033, reaching an estimated USD 5.8 billion in 2025 and is projected to grow significantly to USD 15.6 billion by 2033 the end of the forecast period.

Key Plant based Water Market Trends & Insights

The plant-based water market is currently experiencing dynamic growth, driven by evolving consumer preferences towards healthier, more natural, and sustainable hydration options. A prominent trend is the increasing consumer awareness regarding the health benefits associated with plant-derived ingredients, such as electrolytes, antioxidants, and essential minerals, leading to a shift away from artificially sweetened beverages. This health-centric approach is further amplified by a growing emphasis on natural ingredients and minimal processing, making plant-based waters an attractive alternative to conventional drinks. Furthermore, environmental consciousness is playing a crucial role, with consumers actively seeking products that align with sustainable practices, including responsibly sourced ingredients and eco-friendly packaging, which many plant-based water brands are proactively adopting. This convergence of health, naturalness, and sustainability is reshaping the beverage landscape and driving innovation within the sector.- Rising consumer preference for natural, healthy, and functional beverages.

- Increasing demand for sustainable and ethically sourced products.

- Innovation in flavor profiles and source variety (e.g., cactus, artichoke, bamboo).

- Expansion of distribution channels, particularly online retail and specialty stores.

- Focus on clean label ingredients and transparent sourcing.

- Integration of fortified vitamins and minerals for added health benefits.

AI Impact Analysis on Plant based Water

The integration of Artificial Intelligence (AI) across the plant-based water market is poised to revolutionize various aspects, from product development and supply chain management to consumer engagement and market forecasting. AI-driven analytics can process vast amounts of data related to consumer preferences, nutritional trends, and ingredient performance, enabling manufacturers to identify emerging demands and formulate innovative plant-based water products with precision. This allows for the rapid development of new flavors, functional additives, and plant sources that resonate with target demographics, significantly reducing the time and resources traditionally required for R&D. Furthermore, AI can optimize supply chain efficiencies by predicting demand fluctuations, managing inventory levels, and streamlining logistics for fresh, plant-based ingredients, thereby minimizing waste and ensuring product freshness. In terms of marketing and consumer interaction, AI tools facilitate highly personalized marketing campaigns, allowing brands to deliver tailored messages to specific consumer segments based on their purchasing habits, lifestyle, and dietary preferences. Chatbots and virtual assistants powered by AI can enhance customer service, providing instant answers to queries about product ingredients, health benefits, and sustainability efforts, thereby building stronger brand loyalty. Predictive analytics can also offer invaluable insights into market dynamics, helping businesses anticipate competitive moves, identify new market opportunities, and strategically position their offerings for optimal growth. The strategic adoption of AI is therefore not just an operational enhancement but a fundamental shift towards a more intelligent, responsive, and consumer-centric approach within the plant-based water sector.- AI-driven consumer insights for personalized product development and marketing strategies.

- Optimization of supply chain and logistics for fresh, plant-based ingredients using predictive analytics.

- Enhanced quality control and freshness monitoring through AI-powered sensors.

- Automated customer service and personalized recommendations via AI chatbots.

- Predictive market forecasting for trend identification and strategic business planning.

Key Takeaways Plant based Water Market Size & Forecast

- The plant-based water market is set for robust expansion, projected to achieve a Compound Annual Growth Rate (CAGR) of 12.5% from 2025 to 2033.

- Market valuation is estimated to reach USD 5.8 billion in 2025, reflecting significant current consumer interest and adoption.

- By 2033, the market is forecast to surge to USD 15.6 billion, indicating strong sustained growth and increasing market penetration.

- This growth underscores a fundamental shift in consumer preferences towards natural, healthier, and sustainably sourced hydration options globally.

- The market's upward trajectory is propelled by innovations in diverse plant sources, functional benefits, and evolving distribution strategies.

Plant based Water Market Drivers Analysis

The plant-based water market is experiencing significant tailwinds from several key drivers, primarily stemming from a global paradigm shift in consumer health consciousness and environmental awareness. A paramount driver is the escalating consumer demand for healthier beverage alternatives that offer natural hydration and functional benefits without artificial additives or excessive sugars. As consumers become more informed about nutrition and ingredients, there is a clear preference for beverages derived directly from nature, such as coconut, maple, or birch sap, which are inherently rich in electrolytes, vitamins, and minerals. This desire for 'clean label' products, free from synthetic components, positions plant-based waters as an ideal choice, aligning perfectly with evolving dietary trends and wellness goals. Beyond individual health, environmental concerns are profoundly influencing purchasing decisions, serving as another potent driver for this market. Consumers are increasingly seeking products that align with sustainability principles, including responsible sourcing, minimal ecological footprint, and recyclable packaging. Plant-based water brands often highlight their eco-friendly cultivation methods and commitment to environmental stewardship, appealing to a growing segment of environmentally conscious consumers. Furthermore, aggressive marketing campaigns and celebrity endorsements, coupled with expanding distribution channels that make these products more accessible in mainstream retail and online platforms, are significantly contributing to the market's growth by enhancing visibility and driving trial among a broader consumer base. These combined factors create a fertile ground for sustained market expansion, as plant-based waters increasingly move from niche offerings to mainstream staples in the beverage industry.| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Consumer Health Consciousness: Growing awareness of wellness and natural ingredients drives demand for low-sugar, nutrient-rich beverages, making plant-based waters attractive alternatives to conventional sugary drinks. | +3.5% | North America, Europe, Asia Pacific (particularly developed economies) | Short to Mid-term (Ongoing) |

| Rising Demand for Natural and Functional Beverages: Consumers are actively seeking beverages that offer hydration along with added health benefits like electrolytes, vitamins, and antioxidants naturally present in plant saps and fruit waters. | +3.0% | Global, with strong traction in urban centers and health-conscious demographics | Short to Mid-term (Ongoing) |

| Growing Preference for Sustainable and Eco-friendly Products: Environmental concerns are pushing consumers towards brands that emphasize sustainable sourcing, ethical production, and recyclable or biodegradable packaging. | +2.5% | Europe, North America, Australia, parts of Asia Pacific (e.g., Japan, South Korea) | Mid to Long-term (Increasingly significant) |

| Expansion of Distribution Channels and Marketing Efforts: Increased availability in mainstream retail, online platforms, and focused marketing campaigns are enhancing product visibility and consumer accessibility. | +2.0% | Emerging markets, developing economies, e-commerce platforms globally | Short to Mid-term (Immediate impact) |

| Product Innovation and Diversification: The introduction of new plant sources (e.g., cactus, artichoke, bamboo), unique flavor combinations, and fortified versions is continually attracting new consumers and expanding the market appeal. | +1.5% | Developed markets, innovation hubs (e.g., California, Western Europe) | Mid to Long-term (Sustained growth factor) |

Plant based Water Market Restraints Analysis

Despite its promising growth trajectory, the plant-based water market faces several significant restraints that could potentially temper its expansion. One of the primary challenges is the relatively high production cost and resulting premium pricing associated with many plant-based water products, especially when compared to conventional bottled water or even some fruit juices. The specialized harvesting methods for saps, the careful processing to preserve natural nutrients, and often complex supply chain logistics contribute to a higher cost of goods, which can deter price-sensitive consumers and limit widespread adoption, particularly in emerging markets where disposable income may be lower. This premium positioning can confine the market to a niche segment of affluent or highly health-conscious consumers. Furthermore, a considerable restraint is the limited consumer awareness and understanding of the specific health benefits and unique properties of various plant-based waters in certain regions. Unlike mainstream beverages, many consumers are still unfamiliar with the distinct advantages of birch water over coconut water, or the hydrating qualities of cactus water, leading to skepticism or a lack of perceived value. This knowledge gap necessitates significant investment in consumer education and marketing, which can be a substantial financial burden for market players. Additionally, the market faces intense competition not only from established conventional beverage giants but also from other segments within the plant-based category, such as plant-based milk and functional juices. This crowded landscape demands continuous innovation and differentiation, making it challenging for newer or smaller brands to carve out a sustainable market share. Issues such as the inherently shorter shelf-life of some natural plant saps without extensive processing and potential taste variances that may not appeal to all palates further add to these complexities, collectively acting as brakes on the market's full potential.| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Production Cost and Premium Pricing: The specialized harvesting and processing of plant saps and waters often lead to higher manufacturing costs, resulting in premium pricing that can deter price-sensitive consumers. | -2.0% | Global, particularly in price-sensitive emerging markets and mass-market segments | Short to Mid-term (Immediate barrier) |

| Limited Consumer Awareness and Education: Many consumers are still unfamiliar with the specific health benefits, taste profiles, and value proposition of diverse plant-based waters compared to traditional beverages. | -1.8% | Developing regions, general population outside of health-conscious demographics | Mid-term (Requires sustained marketing) |

| Intense Competition from Traditional and Other Plant-Based Beverages: The market faces strong competition from established bottled water brands, sugary drinks, juices, and other popular plant-based alternatives like plant milks. | -1.5% | Highly saturated beverage markets (e.g., North America, Western Europe) | Short to Mid-term (Constant pressure) |

| Shelf-Life and Storage Challenges for Natural Varieties: Some minimally processed plant-based waters have a shorter shelf-life or require specific refrigeration, posing logistical challenges for distribution and retail display. | -1.0% | Regions with less developed cold chain infrastructure, long-distance supply routes | Short to Mid-term (Operational constraint) |

| Taste Preferences and Palatability Variances: The distinct natural flavors of certain plant-based waters may not appeal to all consumer palates, leading to a narrower consumer base for some product types. | -0.7% | Culturally diverse markets, regions with strong traditional beverage preferences | Long-term (Requires flavor innovation) |

Plant based Water Market Opportunities Analysis

The plant-based water market is ripe with opportunities that can propel its growth beyond current projections, largely driven by ongoing innovation, market expansion, and evolving consumer values. A significant opportunity lies in the continuous product innovation, particularly through the exploration of novel plant sources and the integration of functional ingredients. Developing waters from new plant saps, such as bamboo or even certain tree barks, can introduce unique flavor profiles and distinct health benefits, captivating adventurous consumers and diversifying the market beyond established offerings like coconut or maple water. Furthermore, fortifying these waters with beneficial additives like adaptogens, probiotics, or specialized vitamins can transform them into highly functional beverages that cater to specific health needs, such as stress reduction, gut health, or immune support, opening up new premium segments. Geographical expansion into emerging markets represents another substantial opportunity. As health and wellness trends gain traction in developing economies, coupled with rising disposable incomes, these regions present an untapped consumer base eager for natural and functional hydration options. Strategic partnerships with local distributors and tailored marketing approaches can facilitate successful market entry and rapid penetration. Moreover, the increasing consumer focus on environmental sustainability provides a compelling opportunity for brands to differentiate themselves through eco-friendly packaging solutions, such as fully recyclable materials, plant-based plastics, or even refillable models. Emphasizing a transparent and ethical supply chain, from sourcing to production, can significantly enhance brand appeal and resonate deeply with conscientious consumers. These strategic initiatives, coupled with targeted marketing that educates consumers on the unique value proposition of plant-based waters, can unlock substantial growth avenues and solidify the market's position in the global beverage landscape.| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Product Innovation with Novel Plant Sources and Functional Additives: Exploring new plant saps (e.g., bamboo, specific tree barks) and incorporating adaptogens, probiotics, or enhanced vitamins to create highly functional beverages. | +3.0% | Developed markets (North America, Europe) seeking novelty and advanced wellness benefits | Mid to Long-term (Continuous evolution) |

| Expansion into Emerging Markets: Untapped potential in developing economies where health and wellness trends are nascent but growing, coupled with increasing disposable incomes. | +2.5% | Asia Pacific (China, India, Southeast Asia), Latin America, Middle East & Africa | Mid to Long-term (Significant market expansion) |

| Development of Eco-Friendly and Sustainable Packaging Solutions: Innovating with fully recyclable, biodegradable, or plant-based packaging materials to appeal to environmentally conscious consumers and reduce ecological footprint. | +2.0% | Global, especially strong in Europe and North America due to regulatory and consumer pressure | Short to Mid-term (Growing consumer demand) |

| Strategic Partnerships and Collaborations: Collaborating with health and fitness influencers, nutritionists, food service providers, and complementary beverage brands to expand reach and consumer trust. | +1.5% | Global, leveraging digital marketing and niche communities | Short to Mid-term (Enhanced market penetration) |

| Targeted Marketing and Consumer Education on Health Benefits: Developing focused campaigns to educate specific demographics (e.g., athletes, wellness enthusiasts, children) about the unique hydration and nutritional advantages. | +1.0% | Markets with evolving dietary habits and increasing health literacy | Short to Mid-term (Conversion and adoption) |

Plant based Water Market Challenges Impact Analysis

The plant-based water market, while flourishing, is not immune to a distinct set of challenges that could impede its sustained growth and profitability. One significant challenge is the inherent volatility and sustainability of the supply chain for natural plant-based ingredients. Relying on seasonal harvesting of tree saps or specific plant sources means that factors like climate change, adverse weather conditions, and regional environmental regulations can severely impact raw material availability and quality. This can lead to price fluctuations, inconsistent supply, and difficulties in scaling production to meet rising demand, ultimately affecting product consistency and brand reliability. Managing this agricultural dependency requires robust risk mitigation strategies and diversified sourcing. Furthermore, the market faces considerable regulatory hurdles and complexities, particularly concerning labeling and health claims. Different regions and countries have varying regulations on what constitutes a "natural" product, how specific health benefits can be communicated, and the permissible levels of processing. Navigating this intricate web of compliance can be costly and time-consuming for manufacturers, potentially slowing down market entry for new products or innovations and increasing operational expenses. Maintaining consistent product quality and taste across different batches and geographic locations also presents a formidable challenge, especially for products derived directly from natural sources where natural variations are common. This requires stringent quality control measures and advanced processing techniques to ensure a uniform consumer experience, which is crucial for building and retaining customer loyalty. Lastly, intense market competition from both traditional beverage giants entering the plant-based space and a proliferation of smaller, innovative brands means that differentiation, market share acquisition, and sustainable profitability remain significant hurdles requiring continuous investment in brand building and competitive strategy.| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Volatility and Raw Material Sourcing: Dependence on seasonal and geographically specific plant sources makes the supply chain vulnerable to climate change, environmental factors, and harvesting limitations. | -1.5% | Global, especially for geographically concentrated sources (e.g., Canadian maple, Northern European birch) | Short to Mid-term (Operational disruption) |

| Regulatory Hurdles and Labeling Complexities: Varying national and international regulations regarding "natural" claims, health benefits, and ingredient lists can create compliance challenges and hinder market expansion. | -1.2% | Markets with stringent food and beverage regulations (e.g., EU, US, Japan) | Mid-term (Market entry barrier) |

| Maintaining Consistent Product Quality and Taste: Natural variations in plant sources can lead to inconsistencies in flavor, color, and nutritional profile, requiring advanced processing and quality control to ensure uniformity. | -1.0% | Global, affects brand perception and consumer loyalty | Short to Mid-term (Reputation risk) |

| Intense Market Competition and Saturation in Key Segments: The growing popularity attracts numerous players, leading to price wars, commoditization, and increased pressure on profit margins. | -0.8% | Developed markets (North America, Western Europe) where the segment is more mature | Short to Mid-term (Profitability pressure) |

| Educating Consumers on Value Proposition vs. Cost: Overcoming the perception of plant-based water as a premium product and effectively communicating its unique health and sustainability benefits to justify its higher price point. | -0.7% | All markets, particularly crucial for mass-market adoption | Long-term (Requires continuous marketing investment) |

Plant based Water Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global plant-based water market, offering a detailed understanding of its current landscape, key dynamics, and future growth projections. It covers a broad spectrum of market aspects, from historical performance and current market size to future trends and the impact of influential factors such as drivers, restraints, opportunities, and challenges. The report is meticulously designed to equip stakeholders with actionable insights, enabling informed decision-making for strategic planning, investment prioritization, and market expansion initiatives within this rapidly evolving beverage sector.| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.8 Billion |

| Market Forecast in 2033 | USD 15.6 Billion |

| Growth Rate | 12.5% CAGR from 2025 to 2033 |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Nature's Pure Hydration, Botanical Refreshments Inc., PlantEssence Beverages, Organic Hydrate Co., Verdant Waters Global, GreenLeaf Drinks, EcoThirst Solutions, PurePlant Hydration, AquaVita Botanicals, Natural Dew Corp., Herbal H2O, Zenith Plant Waters, HydroBotanix, Rooted Hydration, FloraFlow Drinks, Bio-Hydrate Solutions, VitalSap Water, Earth's Nectar Beverages, OmniPlant Hydration, PureHarvest Drinks |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

: The plant-based water market is comprehensively segmented to provide a granular view of its diverse components, enabling a precise understanding of consumer preferences and market dynamics across various categories. These segments highlight how different aspects of product origin, taste, packaging, and sales channels contribute to the overall market structure and growth. Understanding these segmentations is crucial for businesses aiming to tailor their product offerings and market strategies effectively to meet specific consumer demands and penetrate niche markets. The detailed breakdown by source, flavor, packaging, and distribution channel offers a multi-dimensional perspective on where growth opportunities lie and how market shares are distributed, allowing for targeted resource allocation and strategic positioning within this burgeoning industry.- By Source: This segment categorizes plant-based waters based on their botanical origin, reflecting the unique nutritional profiles and taste characteristics each source offers.

- Maple Water: Derived from maple tree sap, known for natural electrolytes and minerals.

- Coconut Water: Sourced from young green coconuts, widely recognized for hydration and potassium.

- Birch Water: Harvested from birch trees, valued for its detoxifying properties and subtle sweetness.

- Aloe Water: Made from the inner leaf gel of the aloe vera plant, often sought for digestive benefits.

- Cactus Water: Extracted from prickly pear cacti, noted for electrolytes and antioxidants.

- Artichoke Water: Infused with artichoke leaf extract, offering unique digestive support.

- Others: Includes emerging sources like Bamboo Water, Olive Water, and various other tree saps.

- By Flavor: This segmentation differentiates products by their taste profile, catering to diverse consumer preferences for unadulterated or enhanced flavors.

- Unflavored: Pure, natural taste of the plant source, appealing to consumers seeking authenticity.

- Flavored: Products with added natural flavorings to enhance palatability and appeal.

- Fruit Flavors: Popular additions like Berry (e.g., strawberry, blueberry), Citrus (e.g., lemon, lime, orange), and Tropical Fruits (e.g., pineapple, mango).

- Botanical Flavors: Incorporating natural essences such as Ginger, Mint, Cucumber, or Rose for refreshing and sophisticated tastes.

- Other Flavors: Includes innovative and experimental flavor combinations designed to broaden market appeal.

- By Packaging Type: This segment focuses on the material and format of product packaging, reflecting trends in convenience, sustainability, and consumer preference.

- Bottles:

- PET (Polyethylene Terephthalate): Lightweight, widely recyclable, and cost-effective.

- Glass: Premium feel, preserves taste, and highly recyclable.

- Cartons: Eco-friendly options, often made from renewable resources, suitable for aseptic packaging.

- Cans: Durable, lightweight, and highly recyclable, growing in popularity for convenience beverages.

- Pouches: Flexible, portable, and often resealable, gaining traction for on-the-go consumption.

- Bottles:

- By Distribution Channel: This segmentation outlines the primary avenues through which plant-based water products reach consumers, indicating market accessibility and retail strategies.

- Supermarkets/Hypermarkets: Large retail formats offering wide product selection and competitive pricing, forming a significant sales channel.

- Convenience Stores: Readily accessible outlets for quick purchases, catering to immediate consumption needs.

- Online Retail: E-commerce platforms providing extensive reach, convenience, and direct-to-consumer options, experiencing rapid growth.

- Specialty Stores: Health food stores, organic markets, and gourmet shops catering to specific dietary or lifestyle preferences.

- Foodservice (HORECA): Includes hotels, restaurants, and cafes, where plant-based waters are offered as premium beverage options.

Regional Highlights

The plant-based water market exhibits distinct growth patterns and consumer preferences across different geographical regions, with certain areas emerging as key drivers and others presenting significant untapped potential. Understanding these regional nuances is critical for market players to develop localized strategies and optimize their distribution networks. Each region brings its unique set of factors, including cultural dietary habits, environmental awareness levels, regulatory frameworks, and economic conditions, all of which influence the adoption and growth of plant-based water products. North America stands out as a dominant market, largely driven by a well-established health and wellness industry, high consumer awareness regarding natural and functional foods, and a strong disposable income. The United States and Canada are leading the adoption, characterized by robust marketing efforts, extensive distribution across retail channels, and a consumer base actively seeking alternatives to sugary drinks. Europe is another significant region, particularly Western European countries like Germany, the UK, and France, where there is a strong emphasis on organic products, sustainability, and clean labels. Scandinavian countries also show high adoption rates, especially for birch and maple waters, due to cultural familiarity and local sourcing. The regulatory environment in Europe, while sometimes complex, also drives innovation in natural and additive-free formulations. Asia Pacific is rapidly emerging as a high-growth region, propelled by increasing health consciousness among its burgeoning middle-class population, urbanization, and a rising interest in Western health trends. Countries such as China, India, Japan, and Australia are witnessing a surge in demand, although consumer education remains a key focus to differentiate plant-based waters from traditional beverages. Latin America, particularly Brazil and Mexico, also presents substantial opportunities, driven by a growing awareness of natural health benefits and a cultural affinity for tropical fruit-based beverages, making coconut water a particularly strong segment. Finally, the Middle East and Africa, while smaller in market share currently, are showing nascent growth driven by an increasing focus on healthy lifestyles and the introduction of global beverage trends, particularly in urban centers and among expatriate populations. Each region, therefore, offers unique avenues for market penetration and expansion, contingent on tailored product offerings and strategic market entry approaches.

Top Key Players:

The market research report covers the analysis of key stake holders of the Plant based Water Market. Some of the leading players profiled in the report include -- Nature's Pure Hydration

- Botanical Refreshments Inc.

- PlantEssence Beverages

- Organic Hydrate Co.

- Verdant Waters Global

- GreenLeaf Drinks

- EcoThirst Solutions

- PurePlant Hydration

- AquaVita Botanicals

- Natural Dew Corp.

- Herbal H2O

- Zenith Plant Waters

- HydroBotanix

- Rooted Hydration

- FloraFlow Drinks

- Bio-Hydrate Solutions

- VitalSap Water

- Earth's Nectar Beverages

- OmniPlant Hydration

- PureHarvest Drinks

Frequently Asked Questions:

What is plant-based water?

Plant-based water refers to beverages naturally sourced from plants, distinct from regular tap or bottled water. These include waters derived from tree saps like coconut water, maple water, and birch water, or infusions from plants such as aloe and cactus. They are typically valued for their natural electrolytes, minerals, and other beneficial compounds inherent to their botanical source, offering a healthier, often functional, hydration alternative to traditional beverages.

What are the main benefits of consuming plant-based water?

The primary benefits of plant-based water include natural hydration, essential electrolytes (like potassium, magnesium, and calcium), vitamins, and antioxidants. Many varieties are naturally low in sugar, free from artificial additives, and support specific health aspects such as improved digestion, detoxification, or enhanced athletic recovery. They also align with clean-label and plant-forward dietary preferences, appealing to health-conscious consumers seeking natural wellness solutions.

How large is the plant-based water market expected to grow by 2033?

The global plant-based water market is projected to reach an estimated USD 15.6 billion by 2033. This significant growth forecast reflects a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2033, driven by increasing consumer awareness of health benefits, growing demand for natural and sustainable products, and continuous innovation in product offerings and distribution channels worldwide.

Which are the key types of plant-based water available in the market?

The market features several key types of plant-based water, each with unique characteristics. Prominent varieties include coconut water, known for its natural electrolytes; maple water, sourced from maple tree sap; and birch water, recognized for its natural minerals and subtly sweet flavor. Other emerging types include aloe water, cactus water, and artichoke water, all offering distinct nutritional profiles and appealing to diverse consumer tastes and health objectives.

What factors are driving the growth of the plant-based water market?

The growth of the plant-based water market is primarily driven by rising consumer health consciousness, leading to a demand for natural, low-sugar, and functional beverages. An increasing global focus on sustainability and eco-friendly products also plays a significant role. Furthermore, continuous product innovation, expanding distribution channels, and effective marketing strategies that highlight the unique benefits and natural origins of these waters are crucial growth enablers.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted