Physical Vapor Deposition Coating System Market

Physical Vapor Deposition Coating System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703034 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Physical Vapor Deposition Coating System Market Size

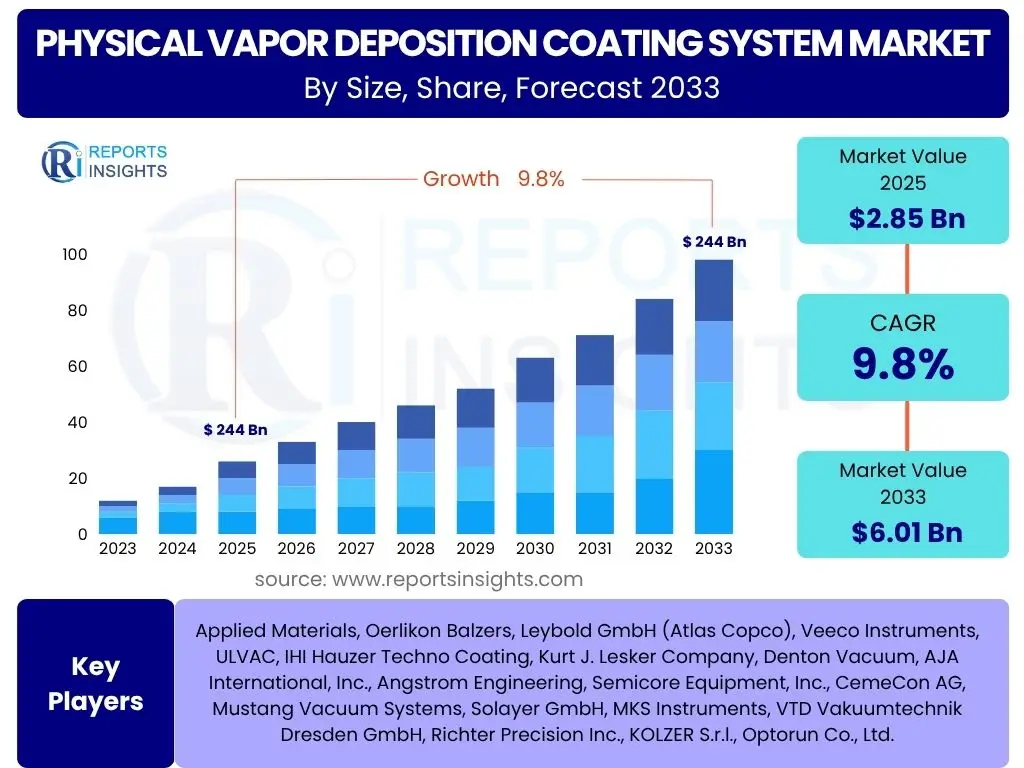

According to Reports Insights Consulting Pvt Ltd, The Physical Vapor Deposition Coating System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 2.85 Billion in 2025 and is projected to reach USD 6.01 Billion by the end of the forecast period in 2033.

Key Physical Vapor Deposition Coating System Market Trends & Insights

The Physical Vapor Deposition (PVD) Coating System market is experiencing dynamic shifts driven by technological innovation and evolving application demands. Common inquiries from users often center around advancements in coating performance, the integration of smart manufacturing principles, and the push for sustainable practices. Key insights reveal a strong emphasis on achieving higher coating uniformity, improved adhesion, and enhanced material properties for specialized applications, alongside a growing interest in reducing operational costs and environmental footprint. The market is increasingly characterized by a demand for customized solutions and greater precision in deposition processes.

Furthermore, there is a clear trend towards multi-layer and nanocomposite coatings, which offer superior performance characteristics, such as enhanced hardness, wear resistance, and corrosion protection. This is particularly relevant in industries like automotive, aerospace, and medical devices where component longevity and reliability are paramount. The miniaturization of electronic components and the advent of flexible electronics are also significantly shaping the demand for advanced PVD techniques, pushing the boundaries of thin-film deposition capabilities. Manufacturers are focusing on developing more efficient and versatile PVD systems capable of handling complex geometries and a wider range of substrate materials, contributing to the market's robust growth trajectory.

- Advancements in multi-layer and nanocomposite coating technologies.

- Increasing demand for customized PVD solutions across diverse industries.

- Emphasis on enhancing coating uniformity, adhesion, and material properties.

- Integration of sustainable and energy-efficient PVD processes.

- Growing adoption in emerging applications such as flexible electronics and advanced optics.

- Development of hybrid coating systems combining PVD with other deposition techniques.

- Focus on reducing operational costs and improving throughput for large-scale production.

AI Impact Analysis on Physical Vapor Deposition Coating System

User queries regarding the impact of Artificial Intelligence (AI) on Physical Vapor Deposition Coating Systems often revolve around process optimization, predictive maintenance, quality control, and the potential for autonomous operation. Users are keen to understand how AI can enhance the precision and efficiency of PVD processes, minimize material waste, and reduce human error. There is significant expectation that AI will lead to more intelligent systems capable of self-correction and adaptive learning, ultimately improving coating consistency and yield rates.

The integration of AI algorithms into PVD systems is expected to revolutionize various aspects of operation, from real-time monitoring and anomaly detection to advanced process control. AI-driven predictive models can anticipate equipment failures, thereby reducing downtime and maintenance costs. Furthermore, machine learning techniques can analyze vast amounts of process data to identify optimal deposition parameters for specific materials and applications, accelerating R&D cycles and improving overall product quality. This shift towards AI-enabled PVD solutions is poised to create highly efficient, resilient, and adaptive manufacturing environments, pushing the boundaries of what is achievable in thin-film technology.

- AI-driven optimization of deposition parameters for improved coating quality and efficiency.

- Predictive maintenance analytics reducing downtime and operational costs.

- Enhanced real-time quality control and defect detection through machine vision and AI algorithms.

- Development of autonomous or semi-autonomous PVD systems for reduced human intervention.

- Accelerated material discovery and process development through AI-powered simulations.

Key Takeaways Physical Vapor Deposition Coating System Market Size & Forecast

Common user questions about the Physical Vapor Deposition Coating System market size and forecast highlight interest in understanding the primary growth drivers, the most promising application areas, and the key regions contributing to market expansion. Insights indicate that the market's robust growth is largely fueled by escalating demand from high-growth sectors such as electronics, automotive, and medical devices, all of which increasingly rely on advanced material coatings for performance and durability. The forecast emphasizes a steady upward trajectory, driven by continuous innovation in PVD technology and its expanding utility across new and existing industrial applications.

A significant takeaway is the pivotal role of thin-film technology in enabling next-generation products, from advanced semiconductor components to resilient automotive parts and biocompatible medical implants. The market's resilience is also attributed to its capacity for customization, allowing PVD systems to be tailored for specific industrial needs. Geographically, Asia Pacific is expected to remain a dominant force, owing to its robust manufacturing base and significant investments in electronics and automotive industries. Overall, the PVD market is poised for sustained expansion, propelled by technological advancements and the critical need for high-performance coatings in modern industrial ecosystems.

- Consistent high growth projected, driven by increasing adoption in diversified industries.

- Electronics and semiconductor sectors remain key demand generators for PVD systems.

- Emerging applications in advanced materials and green technologies present significant growth avenues.

- Asia Pacific is expected to maintain its leading position in market share.

- Technological advancements in coating precision and efficiency are central to market expansion.

Physical Vapor Deposition Coating System Market Drivers Analysis

The Physical Vapor Deposition Coating System market is primarily driven by the escalating demand for high-performance, durable, and functional coatings across a multitude of industries. The inherent advantages of PVD coatings, such as superior hardness, wear resistance, corrosion protection, and biocompatibility, make them indispensable for enhancing product longevity and performance. This demand is particularly pronounced in sectors undergoing rapid technological advancements and stringent quality requirements, necessitating precise and reliable coating solutions.

Furthermore, the continuous innovation in PVD technology, including the development of advanced sputtering, evaporation, and arc ion plating techniques, contributes significantly to market growth. These innovations enable the deposition of complex multi-layer coatings and novel materials, opening up new application possibilities and expanding the scope of PVD technology. The global shift towards sustainable manufacturing practices also plays a role, as PVD is often considered a more environmentally friendly coating method compared to traditional electroplating, due to its minimal waste generation and absence of harmful chemical byproducts.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand from semiconductor and electronics industries | +2.5% | Asia Pacific (China, South Korea, Taiwan), North America, Europe | 2025-2033 |

| Increasing adoption in automotive for durability and aesthetic coatings | +1.8% | Europe (Germany), Asia Pacific (Japan, China), North America | 2025-2033 |

| Expansion of medical device manufacturing requiring biocompatible coatings | +1.5% | North America (USA), Europe (Germany, Switzerland), Asia Pacific (Japan) | 2026-2033 |

| Technological advancements leading to enhanced coating properties and efficiency | +1.2% | Global | 2025-2033 |

| Focus on sustainable and environmentally friendly coating solutions | +0.8% | Europe, North America | 2027-2033 |

Physical Vapor Deposition Coating System Market Restraints Analysis

Despite its robust growth, the Physical Vapor Deposition Coating System market faces several restraints that could potentially impede its expansion. One significant challenge is the high initial capital investment required for purchasing and installing PVD equipment. This substantial upfront cost can be a barrier for small and medium-sized enterprises (SMEs) or new entrants, limiting broader adoption, particularly in developing regions where access to capital may be more restricted. The complexity of operating and maintaining PVD systems also necessitates specialized technical expertise, leading to additional operational costs related to training and skilled labor.

Furthermore, the technical intricacies of PVD processes, including strict vacuum requirements and precise parameter control, can make it challenging to achieve consistent results for all applications and materials. This complexity can lead to higher production costs and a steeper learning curve for new operators. While PVD offers numerous advantages, the market also experiences competition from alternative coating technologies such as Chemical Vapor Deposition (CVD), plasma spraying, and electroplating, which may be more cost-effective or suitable for specific niche applications. These factors collectively contribute to a cautious outlook for certain segments of the market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial capital investment for PVD equipment | -1.0% | Global, particularly emerging economies | 2025-2030 |

| Technical complexity and need for skilled labor | -0.7% | Global | 2025-2033 |

| Competition from alternative coating technologies (e.g., CVD) | -0.5% | Global | 2025-2033 |

| Limitations on substrate size and geometry for certain PVD techniques | -0.3% | Specific industrial applications | 2027-2033 |

Physical Vapor Deposition Coating System Market Opportunities Analysis

The Physical Vapor Deposition Coating System market presents significant opportunities driven by emerging technological advancements and expanding application frontiers. One key opportunity lies in the burgeoning field of advanced materials, particularly in nanotechnology and smart coatings. As industries increasingly demand materials with tailored properties for specific functions, PVD offers unparalleled precision in creating thin films and multi-layer structures for applications such as augmented reality devices, flexible electronics, and high-efficiency solar cells. This pushes the boundaries of material science and opens new revenue streams for PVD system manufacturers.

Furthermore, the growing emphasis on sustainable and circular economy principles provides an avenue for growth. PVD is inherently a cleaner technology compared to many wet chemical processes, producing minimal waste and utilizing less hazardous materials. The development of more energy-efficient PVD systems and the ability to reclaim and reuse target materials can further enhance its environmental appeal, attracting industries seeking to reduce their carbon footprint. The customization and scalability of PVD solutions also represent a substantial opportunity, allowing manufacturers to cater to diverse industry needs, from large-scale industrial production to highly specialized niche applications, ensuring sustained market relevance and expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of new applications in advanced optics and flexible electronics | +1.7% | Global, particularly Asia Pacific and North America | 2026-2033 |

| Increasing adoption in renewable energy sector (e.g., thin-film solar cells) | +1.4% | Asia Pacific (China), Europe (Germany), North America (USA) | 2027-2033 |

| Demand for ultra-thin and precision coatings for miniaturized components | +1.1% | Global, especially in semiconductor hubs | 2025-2033 |

| Growing focus on sustainable and environmentally friendly coating technologies | +0.9% | Europe, North America, Japan | 2028-2033 |

Physical Vapor Deposition Coating System Market Challenges Impact Analysis

The Physical Vapor Deposition Coating System market faces several challenges that can impact its growth trajectory. One significant hurdle is the inherent complexity of PVD processes, which often require precise control over numerous parameters such as vacuum levels, temperature, gas flow, and power settings. Achieving consistent and high-quality coatings, especially for complex geometries or novel materials, demands highly specialized knowledge and experience, leading to a shortage of skilled technicians and engineers. This talent gap can hinder operational efficiency and limit the pace of technological adoption, particularly for new and advanced PVD applications.

Another challenge stems from the high research and development (R&D) investments required to innovate and improve PVD technologies. The constant need for enhanced coating performance, greater efficiency, and broader material compatibility necessitates substantial financial commitment to R&D. Furthermore, the scalability of PVD processes for high-volume manufacturing can be challenging, as maintaining uniformity and cost-effectiveness across large substrates or multiple batches remains an ongoing technical and economic concern. These complexities and investment requirements pose considerable barriers to market penetration and expansion, necessitating strategic responses from industry players to sustain growth and competitiveness.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Shortage of skilled labor and technical expertise | -0.9% | Global | 2025-2033 |

| High R&D costs for continuous innovation and material development | -0.6% | Global | 2025-2033 |

| Challenges in achieving uniform coatings on complex geometries and large surfaces | -0.4% | Specific industrial applications | 2026-2033 |

| Stringent quality control and process validation requirements | -0.3% | Highly regulated industries (Medical, Aerospace) | 2025-2033 |

Physical Vapor Deposition Coating System Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Physical Vapor Deposition Coating System market, offering detailed insights into market size, growth drivers, restraints, opportunities, and challenges. The scope encompasses a thorough examination of various PVD technologies, their applications across diverse industries, and regional market dynamics. It aims to equip stakeholders with critical intelligence for strategic decision-making and understanding the evolving landscape of thin-film deposition technologies.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.85 Billion |

| Market Forecast in 2033 | USD 6.01 Billion |

| Growth Rate | 9.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Applied Materials, Oerlikon Balzers, Leybold GmbH (Atlas Copco), Veeco Instruments, ULVAC, IHI Hauzer Techno Coating, Kurt J. Lesker Company, Denton Vacuum, AJA International, Inc., Angstrom Engineering, Semicore Equipment, Inc., CemeCon AG, Mustang Vacuum Systems, Solayer GmbH, MKS Instruments, VTD Vakuumtechnik Dresden GmbH, Richter Precision Inc., KOLZER S.r.l., Optorun Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Physical Vapor Deposition Coating System market is extensively segmented based on type, application, material, and end-use industry, reflecting the diverse range of technological approaches and industrial demands. This segmentation provides a granular view of the market, highlighting the specific areas driving growth and innovation within the PVD landscape. Each segment represents distinct technological requirements, material science considerations, and performance criteria, catering to the specialized needs of various manufacturing processes and product functionalities.

Understanding these segmentations is crucial for identifying precise market opportunities and developing targeted strategies. For instance, the semiconductor industry's demand for ultra-thin and highly uniform films drives advancements in sputtering and evaporation techniques, while the automotive sector's need for wear-resistant and decorative coatings boosts the adoption of arc ion plating. The material segmentation underscores the versatility of PVD, capable of depositing a wide array of metals, ceramics, and advanced compounds, directly influencing product performance across diverse applications. This detailed breakdown provides a roadmap for stakeholders to navigate the complexities and capitalize on the high-growth potential within the PVD market.

- By Type:

- Sputtering PVD

- DC Sputtering

- RF Sputtering

- Magnetron Sputtering

- Reactive Sputtering

- Evaporation PVD

- Thermal Evaporation

- E-beam Evaporation

- Flash Evaporation

- Arc Ion Plating

- Pulsed Laser Deposition (PLD)

- Ion Beam Assisted Deposition (IBAD)

- Sputtering PVD

- By Application:

- Micro-electronics

- Semiconductors

- Integrated Circuits (ICs)

- Displays (LCD, OLED, etc.)

- MEMS/NEMS

- Sensors

- Cutting Tools & Wear Parts

- Automotive Components

- Medical Devices

- Aerospace & Defense

- Optical Coatings

- Solar Energy

- Industrial & Others

- Architectural Glass

- Packaging

- Decorative Coatings

- Corrosion Protection

- Micro-electronics

- By Material:

- Metals

- Ceramics

- Polymers

- Carbon-based materials (DLC)

- Oxides

- Nitrides

- By End-Use Industry:

- Electronics and Semiconductor

- Industrial Manufacturing

- Automotive

- Medical and Healthcare

- Aerospace

- Energy

- Optics

- Consumer Goods

- Research and Development

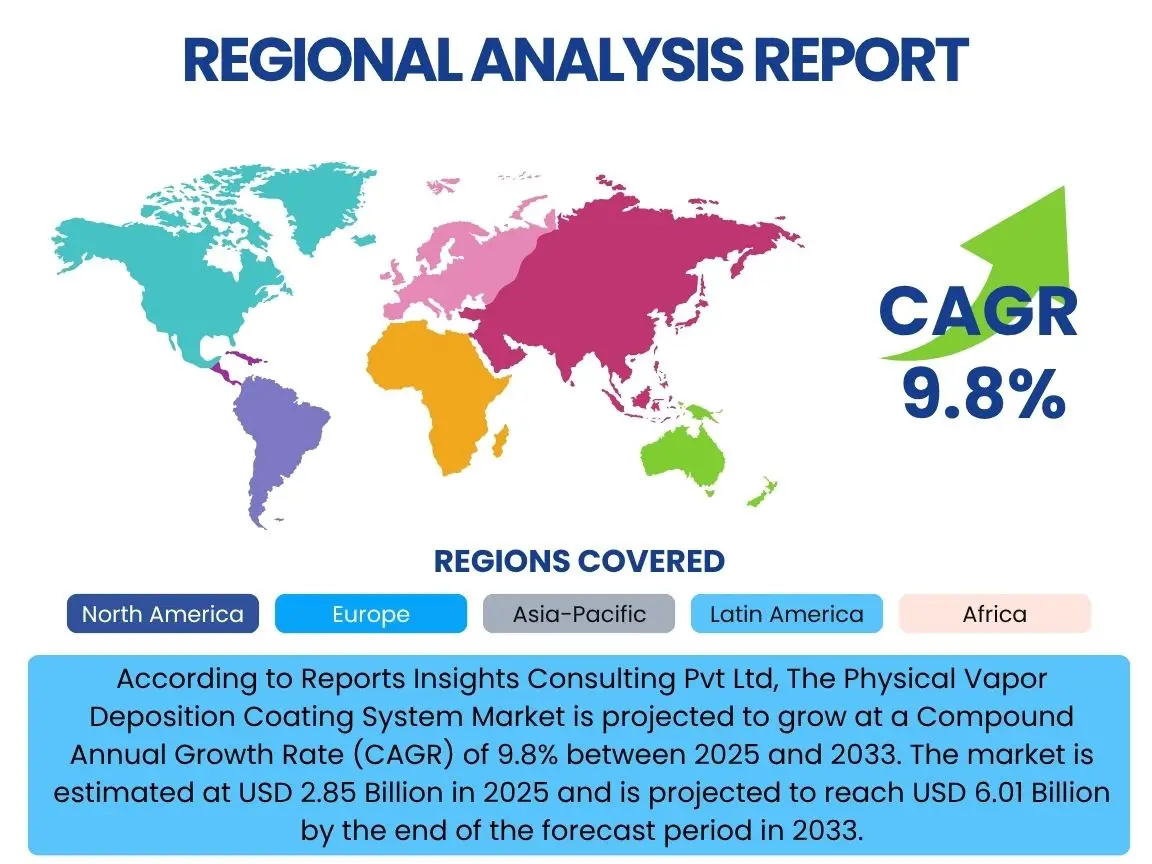

Regional Highlights

The global Physical Vapor Deposition Coating System market exhibits distinct regional dynamics, influenced by varying levels of industrialization, technological adoption, and investment in key end-use sectors. Asia Pacific is poised to remain the dominant region, primarily due to its robust manufacturing base, particularly in electronics, semiconductors, and automotive industries. Countries like China, South Korea, Taiwan, and Japan are at the forefront of technological innovation and have significant production capacities, driving substantial demand for advanced PVD systems. The region benefits from lower manufacturing costs and government initiatives supporting high-tech industries, making it a pivotal hub for PVD market growth.

North America and Europe also hold significant shares in the PVD market, driven by strong R&D activities, the presence of major PVD system manufacturers, and high demand from aerospace, medical devices, and precision engineering sectors. These regions emphasize high-performance coatings for critical applications, pushing the boundaries of PVD technology. Latin America, the Middle East, and Africa are emerging markets, showing gradual growth driven by increasing industrialization and diversification of their economies. While smaller in market share, these regions present future growth opportunities as manufacturing capabilities expand and awareness of PVD benefits increases across various industries.

- Asia Pacific: Expected to dominate the market due to robust electronics, semiconductor, and automotive manufacturing, particularly in China, South Korea, Taiwan, and Japan. Significant investments in high-tech infrastructure and lower production costs contribute to its leading position.

- North America: A significant market driven by strong demand from aerospace, defense, medical devices, and advanced manufacturing sectors. High R&D investments and adoption of cutting-edge PVD technologies characterize this region.

- Europe: A mature market with strong demand from automotive, industrial tools, and precision engineering. Germany, France, and Switzerland are key contributors, focusing on high-quality and sustainable coating solutions.

- Latin America: An emerging market with growing industrialization, particularly in Brazil and Mexico, driven by increasing adoption in automotive and general manufacturing sectors.

- Middle East and Africa (MEA): Demonstrating nascent growth in PVD adoption, primarily in oil & gas, automotive, and emerging manufacturing industries, with potential for future expansion as economic diversification continues.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Physical Vapor Deposition Coating System Market.- Applied Materials

- Oerlikon Balzers

- Leybold GmbH (Atlas Copco)

- Veeco Instruments

- ULVAC

- IHI Hauzer Techno Coating

- Kurt J. Lesker Company

- Denton Vacuum

- AJA International, Inc.

- Angstrom Engineering

- Semicore Equipment, Inc.

- CemeCon AG

- Mustang Vacuum Systems

- Solayer GmbH

- MKS Instruments

- VTD Vakuumtechnik Dresden GmbH

- Richter Precision Inc.

- KOLZER S.r.l.

- Optorun Co., Ltd.

- Plasma Process Group

Frequently Asked Questions

Analyze common user questions about the Physical Vapor Deposition Coating System market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Physical Vapor Deposition (PVD) and its primary applications?

Physical Vapor Deposition (PVD) is a vacuum deposition method used to produce thin films and coatings by condensing a vaporized material onto a substrate. Its primary applications include enhancing the hardness, wear resistance, and corrosion protection of cutting tools, medical devices, automotive components, and micro-electronic parts like semiconductors and displays.

What are the key types of PVD coating systems available in the market?

The key types of PVD coating systems include Sputtering (DC, RF, Magnetron, Reactive), Evaporation (Thermal, E-beam), Arc Ion Plating, Pulsed Laser Deposition (PLD), and Ion Beam Assisted Deposition (IBAD). Each type offers distinct advantages in terms of material compatibility, deposition rate, film quality, and application suitability.

Which industries are the major drivers for the PVD coating system market?

The major industries driving the PVD coating system market include Electronics and Semiconductor, Automotive, Medical and Healthcare, Cutting Tools and Wear Parts, and Aerospace and Defense. These sectors require advanced material properties such as enhanced durability, specific electrical conductivity, or biocompatibility, which PVD coatings effectively provide.

How do PVD coating systems contribute to sustainability?

PVD coating systems contribute to sustainability by being an environmentally friendly coating process. Unlike traditional wet chemical processes, PVD operates in a vacuum, minimizing waste generation, eliminating hazardous chemical byproducts, and often reducing energy consumption compared to conventional coating methods, thereby aligning with green manufacturing initiatives.

What are the future trends and opportunities in the PVD coating system market?

Future trends in the PVD coating system market include the integration of AI for process optimization and predictive maintenance, the development of multi-layer and nanocomposite coatings for enhanced performance, and expansion into emerging applications like flexible electronics, advanced optics, and renewable energy. Opportunities also arise from the increasing demand for customized solutions and sustainable manufacturing practices.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted