Photovoltaic Inverter Market

Photovoltaic Inverter Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707960 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Photovoltaic Inverter Market Size

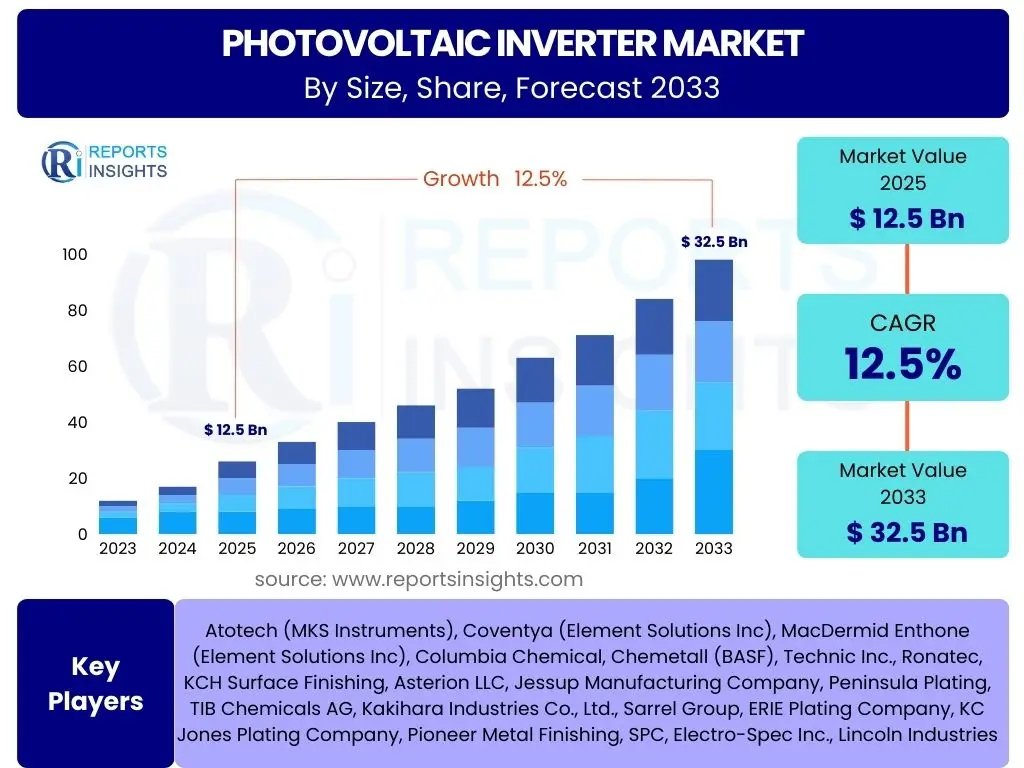

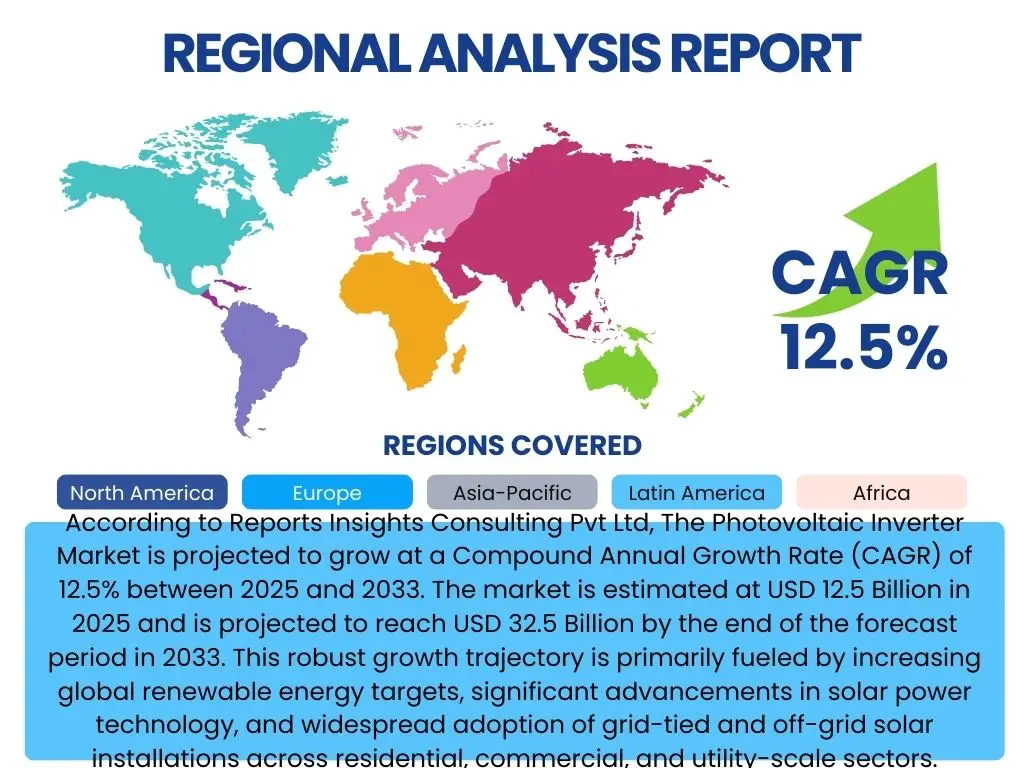

According to Reports Insights Consulting Pvt Ltd, The Photovoltaic Inverter Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2033. The market is estimated at USD 12.5 Billion in 2025 and is projected to reach USD 32.5 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily fueled by increasing global renewable energy targets, significant advancements in solar power technology, and widespread adoption of grid-tied and off-grid solar installations across residential, commercial, and utility-scale sectors.

The expansion is further supported by declining solar module costs, which make solar energy more competitive with traditional power sources, thereby boosting demand for efficient and reliable photovoltaic inverters. Moreover, the integration of energy storage systems with solar installations is creating new opportunities for advanced inverter technologies capable of managing complex power flows and ensuring grid stability. Developed economies are witnessing substantial investment in smart grid infrastructure, necessitating intelligent inverter solutions for optimal energy management and enhanced reliability.

Key Photovoltaic Inverter Market Trends & Insights

The Photovoltaic Inverter market is experiencing dynamic shifts, characterized by several pivotal trends aimed at enhancing efficiency, reliability, and grid integration. Users frequently seek information on the technological evolution driving the market, the increasing demand for smarter solutions, and the shift towards decentralized power generation. A key insight reveals a strong emphasis on smart inverters that offer advanced grid support functionalities, including reactive power control, fault ride-through capabilities, and seamless communication with grid operators. This trend is crucial for maintaining grid stability as renewable energy penetration increases.

Another significant trend involves the growing adoption of microinverters and string inverters, particularly in residential and commercial sectors. These smaller, modular units offer advantages such as improved module-level power optimization, enhanced safety, and greater design flexibility, which are highly valued by system installers and end-users. Furthermore, the market is seeing a surge in hybrid inverters capable of managing both solar power generation and battery storage, a critical development for the burgeoning energy storage market and for ensuring energy independence. The integration of advanced monitoring and control systems, often leveraging cloud-based platforms, is also gaining traction, providing users with real-time performance data and remote diagnostic capabilities.

- Growing adoption of smart inverters with advanced grid functionalities.

- Increased demand for microinverters and string inverters in distributed generation.

- Integration of photovoltaic inverters with battery energy storage systems (BESS) via hybrid inverters.

- Emphasis on higher power density, efficiency, and reliability for reduced balance-of-system costs.

- Development of cloud-based monitoring and predictive maintenance platforms.

- Focus on cybersecurity features to protect grid-connected inverter systems.

- Modular and flexible inverter designs to cater to diverse application requirements.

AI Impact Analysis on Photovoltaic Inverter

The integration of Artificial Intelligence (AI) is profoundly transforming the Photovoltaic Inverter market, with stakeholders keenly interested in how AI can optimize performance, predict failures, and enhance overall system intelligence. AI-driven algorithms are enabling inverters to learn and adapt to dynamic environmental conditions and grid requirements, leading to more efficient energy conversion and improved system reliability. Users are particularly focused on AI's ability to provide proactive solutions, moving beyond traditional reactive maintenance strategies. This intelligence is crucial for complex grid scenarios, where a high penetration of renewables demands sophisticated control and forecasting capabilities.

Specifically, AI is being leveraged for predictive maintenance, allowing inverter systems to anticipate potential failures based on historical data and real-time performance analytics, thereby minimizing downtime and operational costs. It also plays a critical role in optimizing energy yield by fine-tuning inverter operation based on weather forecasts, load patterns, and energy prices, ensuring maximum energy harvest and financial returns. Furthermore, AI enhances grid stability by enabling intelligent dispatch and load balancing, allowing inverters to respond dynamically to grid signals and contribute to a more resilient and efficient power infrastructure. The application of machine learning also aids in rapid fault detection and diagnosis, significantly reducing troubleshooting time and improving system safety.

- Predictive maintenance capabilities to forecast inverter failures, reducing downtime and operational expenditure.

- Optimized energy yield management through intelligent algorithms adapting to environmental and grid conditions.

- Enhanced grid stability and integration via smart control for reactive power compensation and frequency regulation.

- Advanced fault detection and diagnostics, enabling quicker identification and resolution of system anomalies.

- Intelligent demand-side management and load forecasting for optimal energy dispatch.

- Improved cybersecurity postures through AI-driven anomaly detection and threat response.

- Self-learning inverters adapting to variable irradiance, temperature, and grid characteristics for peak performance.

Key Takeaways Photovoltaic Inverter Market Size & Forecast

The Photovoltaic Inverter market is poised for significant expansion, driven by a confluence of global energy trends and technological innovation. Users seeking core insights into the market's trajectory will find that its growth is intrinsically linked to worldwide commitments to renewable energy and the decreasing costs associated with solar power generation. The forecast highlights a robust compound annual growth rate, underscoring the critical role inverters play in the broader energy transition. This expansion is not merely quantitative but also qualitative, reflecting a continuous evolution in inverter capabilities towards greater intelligence, efficiency, and integration.

A key takeaway from the market analysis is the increasing sophistication of inverter technology, moving beyond simple DC-to-AC conversion to encompass advanced grid services, energy storage management, and smart home integration. This evolution is vital for accommodating the rising share of intermittent renewable energy sources on the grid and enhancing overall system resilience. Furthermore, competitive pressures are driving continuous innovation in product design, manufacturing processes, and cost reduction strategies, making advanced inverter solutions more accessible. Regional disparities in growth rates and technology adoption remain significant, influenced by diverse regulatory landscapes, policy incentives, and varying levels of grid development.

- The market exhibits substantial growth potential, driven by global renewable energy policies and cost competitiveness of solar PV.

- Technological advancements, particularly in smart and hybrid inverters, are central to future market expansion and adoption.

- Increasing integration with battery energy storage systems (BESS) is a primary catalyst for innovation and demand.

- Regulatory frameworks and government incentives play a crucial role in shaping regional market dynamics and investment.

- A shift towards distributed generation and grid modernization is propelling the demand for sophisticated, intelligent inverter solutions.

- The competitive landscape necessitates continuous product differentiation, efficiency improvements, and cost optimization from manufacturers.

Photovoltaic Inverter Market Drivers Analysis

The Photovoltaic Inverter market's robust growth is propelled by several fundamental drivers that collectively create a fertile environment for innovation and expansion. Government policies and incentives globally are among the most significant accelerators, providing financial support and regulatory frameworks that encourage solar PV installations. These policies, such as feed-in tariffs, tax credits, and net metering, reduce the initial investment barrier for consumers and businesses, directly increasing the demand for photovoltaic inverters.

Furthermore, the steady decline in the Levelized Cost of Electricity (LCOE) for solar power has made it increasingly competitive with conventional energy sources, prompting a wider adoption of solar PV systems across various scales. This economic viability directly translates into a higher demand for high-efficiency and cost-effective inverters. The global imperative to address climate change and reduce carbon emissions also acts as a powerful driver, pushing countries towards renewable energy targets and sustainable power generation, with solar PV at the forefront. Coupled with the rising global electricity demand, especially in rapidly industrializing economies, these factors create a persistent need for scalable and reliable energy solutions, where PV inverters are indispensable.

Technological advancements in inverter design and functionality also play a crucial role. Innovations leading to higher efficiency, greater power density, and enhanced grid integration capabilities ensure that inverters can meet evolving utility requirements and consumer expectations. The growing synergy between solar PV and battery energy storage systems further boosts demand for advanced hybrid inverters capable of optimizing energy flow, managing grid stability, and ensuring energy security.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Favorable Government Policies & Incentives | +3.5% | Global, particularly Europe, North America, APAC | Short to Medium Term |

| Declining Levelized Cost of Electricity (LCOE) for Solar PV | +2.8% | Global | Medium to Long Term |

| Rising Global Electricity Demand | +2.0% | APAC, Middle East, Africa | Long Term |

| Increasing Integration with Energy Storage Systems | +2.2% | North America, Europe, Australia | Medium Term |

| Technological Advancements & Efficiency Improvements | +1.5% | Global | Continuous |

| Growing Environmental Concerns and Decarbonization Goals | +1.0% | Global | Long Term |

Photovoltaic Inverter Market Restraints Analysis

Despite significant growth prospects, the Photovoltaic Inverter market faces several notable restraints that could temper its expansion. One primary concern is the existing grid infrastructure limitations, particularly in developing regions, which may not be adequately equipped to handle the increasing influx of intermittent renewable energy sources. This lack of grid modernization can lead to curtailment of solar power and challenges in connecting new PV installations, thereby limiting the demand for inverters capable of advanced grid interaction.

Another significant restraint is the initial high investment cost associated with advanced inverter technologies, especially those with integrated AI capabilities or robust grid-support features. While solar panel costs have decreased, the cost of sophisticated inverters and accompanying installation can still represent a substantial upfront expenditure for consumers and smaller businesses, particularly in emerging markets with limited access to financing. This financial barrier can slow down adoption rates, despite the long-term benefits of efficiency and reliability.

Furthermore, supply chain disruptions, as experienced recently with global events, pose a constant threat to the market. Dependencies on specific raw materials and manufacturing hubs can lead to price volatility and delays in product delivery, impacting project timelines and increasing overall costs. Policy uncertainties and sudden changes in regulatory frameworks in certain countries can also create an unpredictable investment climate, deterring developers and manufacturers from making long-term commitments, thereby affecting market stability and growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Grid Infrastructure Limitations & Modernization Challenges | -1.8% | Developing Regions (APAC, Africa, Latin America) | Medium Term |

| High Initial Investment Costs for Advanced Inverters | -1.2% | Emerging Markets, Residential Sector | Short Term |

| Supply Chain Disruptions and Raw Material Price Volatility | -0.9% | Global | Short to Medium Term |

| Regulatory & Policy Uncertainties | -0.7% | Specific Countries/Regions | Medium Term |

Photovoltaic Inverter Market Opportunities Analysis

The Photovoltaic Inverter market is rich with emerging opportunities that promise to drive future growth and innovation. The increasing penetration of solar energy in emerging markets, particularly across Asia Pacific, Africa, and Latin America, represents a vast untapped potential. These regions often have abundant solar resources, rapidly growing electricity demand, and nascent grid infrastructure, creating a strong impetus for off-grid and hybrid solar solutions that rely heavily on advanced inverters. Local governments in these areas are increasingly prioritizing renewable energy, opening doors for market entry and expansion.

Another significant opportunity lies in the ongoing development of smart grids and the broader integration of IoT technologies. As grids become more digitized and interconnected, the demand for intelligent inverters capable of real-time communication, data analytics, and autonomous operation will surge. These smart inverters can contribute significantly to grid stability, demand response, and efficient energy management, positioning them as critical components in modern energy ecosystems. Investment in grid modernization efforts globally will directly translate into demand for such sophisticated inverter solutions.

Furthermore, the rise of electric vehicles (EVs) and the growing need for EV charging infrastructure present a novel opportunity. Integrating EV charging stations with solar PV systems, managed by specialized inverters, can create sustainable and cost-effective charging solutions. Hybrid inverters capable of bidirectional power flow and optimized energy management between solar, storage, grid, and EV charging points will be particularly vital. This convergence of solar energy with e-mobility creates a substantial market for innovative inverter applications. Additionally, advancements in energy storage technologies continue to drive demand for hybrid inverters, which can seamlessly manage the charging and discharging of batteries, maximizing self-consumption and grid independence for prosumers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Markets & Rural Electrification | +2.5% | APAC, Africa, Latin America | Long Term |

| Integration with Smart Grid and Internet of Things (IoT) Platforms | +2.0% | Developed Regions, rapidly modernizing grids | Medium Term |

| Development of Hybrid Inverters for Off-grid and Microgrid Solutions | +1.8% | Remote Areas, Island Nations, Developing Regions | Long Term |

| Integration with Electric Vehicle (EV) Charging Infrastructure | +1.5% | Europe, North America, China | Medium Term |

Photovoltaic Inverter Market Challenges Impact Analysis

The Photovoltaic Inverter market, while experiencing rapid growth, must navigate several significant challenges that could impede its progress. Cybersecurity risks represent a growing concern as inverters become more connected and intelligent. As critical components in smart grids, inverters are increasingly vulnerable to cyberattacks that could compromise grid stability, data integrity, or even operational control. Protecting these devices from malicious actors requires continuous investment in robust security protocols and ongoing software updates, posing a significant operational and financial challenge for manufacturers and operators.

Another key challenge involves the ongoing issue of standardization across the industry. The lack of universal standards for inverter communication protocols, grid codes, and safety requirements can create interoperability issues between different manufacturers' equipment and complicate grid integration. This fragmentation can lead to higher installation costs, reduced system flexibility, and slower market adoption of new technologies, particularly in cross-border projects. Establishing global standards is a complex undertaking that requires significant collaboration among industry stakeholders and regulatory bodies.

Furthermore, managing the intermittency of renewable energy sources, such as solar power, remains a core technical challenge. While inverters are designed to handle variable power input, the large-scale integration of solar PV into the grid necessitates advanced inverter functionalities to mitigate voltage fluctuations, frequency deviations, and other power quality issues. Developing sophisticated control algorithms and ensuring grid resilience against these variabilities requires continuous research and development. Additionally, a persistent shortage of skilled labor for installation, maintenance, and advanced system design in the solar sector poses a bottleneck, particularly in regions with rapidly expanding solar markets. This scarcity can lead to project delays and compromise the quality of installations, ultimately affecting system performance and reliability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cybersecurity Risks for Connected Inverter Systems | -1.0% | Global | Continuous |

| Lack of Standardization & Interoperability Issues | -0.8% | Global | Medium Term |

| Managing Intermittency & Grid Stability of Renewables | -1.2% | Global, particularly high penetration regions | Long Term |

| Shortage of Skilled Labor for Installation & Maintenance | -0.7% | Developed Regions, Rapidly Expanding Markets | Medium Term |

Photovoltaic Inverter Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Photovoltaic Inverter market, covering market sizing, growth forecasts, key trends, and competitive landscape. It delves into the impact of emerging technologies like AI, identifies critical market drivers, restraints, opportunities, and challenges. The scope encompasses detailed segmentation analysis by inverter type, power rating, phase, and end-use application across major geographical regions, offering a holistic view of market dynamics and strategic insights for stakeholders. The report aims to furnish actionable intelligence for business planning, investment decisions, and market positioning within the rapidly evolving renewable energy sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 32.5 Billion |

| Growth Rate | 12.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Huawei Technologies Co., Ltd., Sungrow Power Supply Co., Ltd., SMA Solar Technology AG, Enphase Energy, Inc., SolarEdge Technologies, Inc., Fronius International GmbH, ABB Ltd., GoodWe Technologies Co., Ltd., Ingeteam S.A., KSTAR New Energy Co., Ltd., Delta Electronics, Inc., TBEA Xi'an Electric Technology Co., Ltd., Siemens AG, Ginlong Technologies (Solis Inverters), KACO new energy GmbH, Schneider Electric SE, Hitachi Hi-Rel Power Electronics Pvt. Ltd., Chint Power Systems (CPS) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Photovoltaic Inverter market is extensively segmented to provide a detailed understanding of its diverse applications and technological nuances. These segmentations are critical for identifying specific market opportunities, competitive landscapes, and strategic entry points for manufacturers and service providers. The primary segmentation categories include inverter type, phase, power rating, and end-use application, each reflecting distinct operational characteristics and market demands. Understanding these segments helps stakeholders tailor product development and marketing strategies to specific customer needs and technical requirements, from small residential installations to large-scale utility projects.

For instance, the By Type segment differentiates between micro inverters, string inverters, central inverters, and hybrid inverters, each optimized for different system sizes and functionalities, with microinverters often preferred for residential setups due to module-level optimization and safety, while central inverters dominate utility-scale projects due to their cost-effectiveness per watt. The By Power Rating segment further categorizes inverters based on their capacity, directly correlating with the scale of the solar PV installation. Similarly, the By End-Use Application segment distinguishes between residential, commercial, utility-scale, and off-grid applications, highlighting varied requirements concerning efficiency, grid interaction, and robust design. This comprehensive segmentation allows for a granular analysis of market trends and forecasts, enabling more precise strategic planning.

- By Type:

- Micro Inverter

- String Inverter

- Central Inverter

- Hybrid Inverter

- By Phase:

- Single-Phase

- Three-Phase

- By Power Rating:

- Less than 10 kW

- 10-50 kW

- Greater than 50 kW

- By End-Use Application:

- Residential

- Commercial

- Utility-Scale

- Off-Grid

Regional Highlights

The global Photovoltaic Inverter market exhibits significant regional disparities in growth, adoption, and technological advancements, driven by varied policy landscapes, economic development, and energy demands. Asia Pacific (APAC) currently stands as the largest and fastest-growing market, primarily fueled by massive solar deployment initiatives in countries like China, India, and Australia. Favorable government policies, rapid industrialization, and increasing electricity consumption are key drivers in this region, particularly for utility-scale and commercial applications. The ongoing expansion of manufacturing capabilities also positions APAC as a hub for inverter production and innovation.

Europe demonstrates a mature but steadily growing market, propelled by ambitious renewable energy targets, a strong focus on energy independence, and advanced grid modernization efforts. Countries such as Germany, Spain, and Italy are leading the adoption of smart and hybrid inverters, driven by high penetration of distributed generation and a growing emphasis on energy storage integration. North America, particularly the United States, represents a significant market with strong growth in both utility-scale and residential solar installations, supported by federal and state incentives. The region is also at the forefront of integrating solar PV with battery storage and advanced grid services, demanding sophisticated inverter solutions.

Latin America and the Middle East & Africa (MEA) are emerging as high-potential markets, characterized by abundant solar resources and rapidly developing energy sectors. Countries like Brazil, Chile, and South Africa are witnessing substantial investment in large-scale solar projects, driving demand for robust and cost-effective central inverters. These regions also present considerable opportunities for off-grid and microgrid solutions, catering to rural electrification and energy access challenges. The unique environmental conditions in MEA, with high temperatures and dust, also drive demand for rugged and highly reliable inverter designs.

- Asia Pacific (APAC): Dominant market share and fastest growth, led by China, India, Japan, and Australia, driven by government policies, falling costs, and massive utility-scale projects.

- Europe: Mature market with steady growth, focused on distributed generation, energy independence, smart grid integration, and high adoption of hybrid inverters in countries like Germany, Italy, and Spain.

- North America: Significant market with strong residential and utility-scale solar growth, particularly in the United States, emphasis on energy storage integration and advanced grid services.

- Latin America: Emerging market with substantial growth potential due to abundant solar resources and rising energy demand in countries such as Brazil, Mexico, and Chile.

- Middle East & Africa (MEA): High growth potential, driven by large-scale solar projects, diversification from fossil fuels, and rural electrification initiatives across the region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Photovoltaic Inverter Market.- Huawei Technologies Co., Ltd.

- Sungrow Power Supply Co., Ltd.

- SMA Solar Technology AG

- Enphase Energy, Inc.

- SolarEdge Technologies, Inc.

- Fronius International GmbH

- ABB Ltd.

- GoodWe Technologies Co., Ltd.

- Ingeteam S.A.

- KSTAR New Energy Co., Ltd.

- Delta Electronics, Inc.

- TBEA Xi'an Electric Technology Co., Ltd.

- Siemens AG

- Ginlong Technologies (Solis Inverters)

- KACO new energy GmbH

- Schneider Electric SE

- Hitachi Hi-Rel Power Electronics Pvt. Ltd.

- Chint Power Systems (CPS)

Frequently Asked Questions

What is a photovoltaic inverter and why is it important?

A photovoltaic (PV) inverter is a crucial component in any solar power system, responsible for converting the direct current (DC) electricity generated by solar panels into alternating current (AC) electricity that can be used by homes, businesses, or fed into the electrical grid. Its importance stems from its role in enabling the use of solar energy, optimizing system performance, and ensuring seamless integration with the existing electrical infrastructure.

What are the main types of PV inverters available today?

The primary types of PV inverters include micro inverters, string inverters, central inverters, and hybrid inverters. Micro inverters are installed at each solar panel for module-level optimization. String inverters connect multiple panels in a series. Central inverters are large units used for utility-scale projects. Hybrid inverters combine solar conversion with battery storage management, offering versatility for grid-tied and off-grid applications.

How do government policies influence the PV inverter market?

Government policies significantly influence the PV inverter market through mechanisms like feed-in tariffs, tax credits, subsidies, and renewable energy mandates. These policies reduce the financial burden of solar installations, making them more attractive and directly stimulating demand for PV inverters. Regulatory frameworks also dictate grid connection standards and safety requirements, pushing innovation in inverter technology.

What role does AI play in modern PV inverter technology?

AI is increasingly integral to modern PV inverter technology, enhancing performance through predictive maintenance, optimizing energy yield by adapting to varying conditions, and improving grid stability with intelligent control algorithms. AI-driven systems also facilitate advanced fault detection and diagnosis, contributing to higher reliability, lower operational costs, and smarter energy management across the solar ecosystem.

What are the future growth prospects for the global PV inverter market?

The global PV inverter market is projected for robust future growth, driven by continued decline in solar costs, ambitious global renewable energy targets, and the increasing integration of energy storage systems. Technological advancements, particularly in smart and hybrid inverters, along with expansion into emerging markets, are expected to sustain a strong growth trajectory throughout the forecast period.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted