Photocuring Agent Market

Photocuring Agent Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709904 | Last Updated : December 22, 2025 |

Format : ![]()

![]()

![]()

![]()

Photocuring Agent Market Size

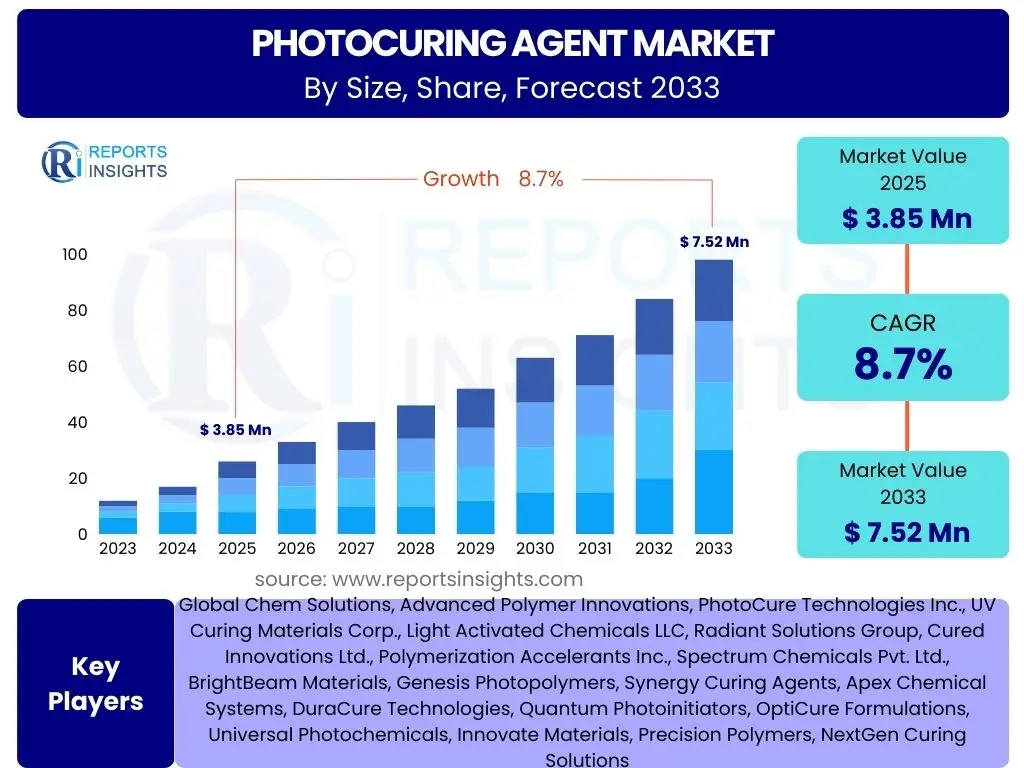

According to Reports Insights Consulting Pvt Ltd, The Photocuring Agent Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. The market is estimated at USD 3.85 Billion in 2025 and is projected to reach USD 7.52 Billion by the end of the forecast period in 2033.

Key Photocuring Agent Market Trends & Insights

The photocuring agent market is undergoing significant transformation driven by advancements in material science and increasing demand for sustainable and efficient manufacturing processes. Users frequently inquire about the latest technological breakthroughs that enhance curing speed, reduce energy consumption, and expand application versatility. There is a strong interest in understanding how regulatory shifts concerning VOC emissions and hazardous chemicals are shaping product development, pushing manufacturers towards greener, more compliant solutions. Furthermore, the market is experiencing a shift towards specialized formulations tailored for high-performance applications in burgeoning sectors like 3D printing and advanced electronics, where precision and rapid processing are paramount.

Another prominent area of user interest revolves around the adoption of multi-functional photoinitiators and the integration of smart materials into photocuring systems. These innovations promise enhanced performance characteristics such as improved adhesion, flexibility, and durability, while also enabling novel functionalities like self-healing or responsive surfaces. The increasing demand for customized solutions, particularly in the medical and dental fields, is fostering research into biocompatible and highly specific photocuring agents. This trend underscores a broader market movement towards value-added products that offer superior performance and cater to niche, high-growth applications, thereby expanding the overall market footprint for photocuring technologies.

- Shift towards low-migration and low-VOC photoinitiators for enhanced environmental compliance.

- Growing adoption of LED-curable systems driving demand for specific photoinitiators.

- Expansion of 3D printing applications, requiring advanced and specialized photocuring agents.

- Development of multi-functional photoinitiators offering improved performance and versatility.

- Integration of smart materials and responsive photocuring systems for advanced applications.

AI Impact Analysis on Photocuring Agent

Common user questions regarding AI's impact on photocuring agents frequently center on how artificial intelligence can optimize material discovery, accelerate product development cycles, and enhance manufacturing efficiency. There is significant interest in AI's potential to predict the performance of new photoinitiator formulations, thereby reducing the extensive experimental testing traditionally required. Users are keen to understand if AI can help identify novel chemical structures that exhibit superior curing properties, improved shelf life, or enhanced environmental profiles, streamlining the R&D process and bringing innovative products to market faster. The analytical power of AI is seen as a key enabler for unlocking complex relationships between molecular structure, formulation, and final cured material properties.

Beyond research and development, inquiries often touch upon AI's role in optimizing photocuring processes on the production line. This includes questions about using machine learning for real-time process control, predicting equipment maintenance needs, and ensuring consistent product quality across various batches. Users are interested in how AI can integrate with existing manufacturing systems to automate adjustments based on sensor data, leading to reduced waste, lower energy consumption, and increased throughput. The ability of AI to analyze vast datasets, from raw material specifications to finished product performance, presents a transformative opportunity for the photocuring agent industry to achieve unprecedented levels of efficiency, precision, and sustainability in its operations.

- AI-driven acceleration of R&D for novel photoinitiator design and discovery.

- Optimization of photocuring formulations through predictive modeling and simulation.

- Enhanced quality control and process automation in manufacturing using machine learning.

- Data-driven insights for understanding material performance and failure mechanisms.

- Supply chain optimization and demand forecasting for raw materials and finished products.

Key Takeaways Photocuring Agent Market Size & Forecast

Key takeaways from the photocuring agent market size and forecast consistently highlight the robust growth trajectory driven by expanding applications across diverse industries. Users are primarily interested in understanding the core factors contributing to this growth, such as the increasing adoption of UV/EB curing technologies due to their environmental benefits and efficiency. The market's significant projected CAGR and market value underscore a sustained demand for innovative photocuring solutions, especially those that offer faster processing, lower energy consumption, and improved material performance. The shift towards sustainable practices is a critical undercurrent, pushing the market towards greener formulations and more energy-efficient curing methods.

Furthermore, the forecast indicates a strategic pivot by industry players towards high-value, specialized segments. This includes the development of tailored agents for advanced manufacturing techniques like additive manufacturing (3D printing) and next-generation electronic components, where precision and rapid prototyping are crucial. The market's future expansion is also heavily reliant on overcoming current challenges related to raw material volatility and regulatory complexities, which will necessitate continuous innovation and strategic partnerships. Overall, the market is poised for considerable expansion, with a clear emphasis on technological advancement, application diversification, and sustainable development as central themes for long-term success.

- Significant market expansion anticipated, reaching USD 7.52 Billion by 2033.

- Strong CAGR of 8.7% driven by industrial adoption and technological advancements.

- Sustainability and regulatory compliance are key forces shaping future product development.

- Growth concentrated in high-performance applications such as 3D printing and advanced electronics.

- Continuous innovation in photoinitiator chemistry essential for market competitiveness.

Photocuring Agent Market Drivers Analysis

The increasing demand for environmentally friendly and efficient curing technologies stands as a primary driver for the photocuring agent market. UV/EB curing processes eliminate the need for solvents, significantly reducing Volatile Organic Compound (VOC) emissions, which aligns with stringent environmental regulations worldwide. Industries are increasingly adopting these technologies to improve air quality, enhance worker safety, and reduce their carbon footprint. This shift away from traditional thermal or solvent-based curing methods towards greener alternatives is a fundamental force propelling market expansion, especially in developed economies with robust environmental policies.

Moreover, the rapid growth in end-use industries such as 3D printing, advanced electronics, and automotive coatings further fuels market demand. In 3D printing, photocuring agents are integral to producing complex geometries with high precision and speed. The electronics sector relies on these agents for manufacturing printed circuit boards, display coatings, and encapsulants due to their rapid cure rates and excellent protective properties. The automotive industry utilizes UV-curable coatings for scratch resistance, aesthetics, and faster production cycles. These expanding high-growth applications, combined with continuous advancements in photopolymer chemistry that yield improved performance characteristics, are critical in sustaining the market's upward trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for eco-friendly UV/EB curing technologies | +2.1% | Global, particularly Europe & North America | 2025-2033 |

| Expansion of 3D printing and additive manufacturing applications | +1.8% | North America, APAC, Europe | 2025-2033 |

| Increasing use in advanced electronics and display manufacturing | +1.5% | APAC (China, South Korea, Japan), North America | 2025-2033 |

| Technological advancements in photoinitiator chemistry | +1.3% | Global | 2025-2033 |

| Rising adoption in high-performance coatings and adhesives | +1.0% | Global | 2025-2033 |

Photocuring Agent Market Restraints Analysis

Despite its significant growth prospects, the photocuring agent market faces several restraints, most notably the high initial investment required for UV/EB curing equipment. Implementing these advanced systems often involves substantial capital expenditure for UV lamps, electron beam accelerators, and specialized processing lines. This cost barrier can deter smaller manufacturers or those in developing regions from adopting the technology, thus limiting market penetration. The complexity of integrating these new systems into existing production infrastructures also poses a challenge, requiring specialized technical expertise and potential downtime during installation and calibration.

Another significant restraint is the volatility in raw material prices, particularly for key chemical intermediates used in the synthesis of photoinitiators. Fluctuations in crude oil prices, supply chain disruptions, and geopolitical events can directly impact the cost of these raw materials, leading to increased production costs and potential price instability for finished photocuring agents. Furthermore, the limited penetration of UV/EB curing in certain traditional industrial applications, where thermal or solvent-based systems are deeply entrenched and perceived as more cost-effective for large-volume, low-margin products, presents an ongoing hurdle for market expansion. Addressing these cost and adoption barriers will be crucial for sustained market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial capital investment for UV/EB curing equipment | -1.5% | Emerging Economies, SMBs Globally | 2025-2030 |

| Volatility in raw material prices | -1.2% | Global | 2025-2033 |

| Limited penetration in certain traditional applications | -0.9% | Global, particularly Industrial sectors | 2025-2033 |

| Technical challenges in formulating for specific substrates | -0.7% | Global, R&D focused regions | 2025-2028 |

| Stringent regulatory approvals for novel chemicals | -0.5% | Europe, North America | 2025-2033 |

Photocuring Agent Market Opportunities Analysis

Significant opportunities in the photocuring agent market stem from the rapid growth of emerging economies and the expanding manufacturing bases in regions like Asia Pacific and Latin America. As industrialization and consumer spending increase in these areas, there is a rising demand for advanced coatings, inks, and adhesives across various sectors, including packaging, automotive, and electronics. These regions often prioritize efficient and sustainable manufacturing practices to keep pace with global standards, creating a fertile ground for the adoption of UV/EB curing technologies. Local governments' support for advanced manufacturing and environmental initiatives further enhances the market's potential in these developing regions, offering new avenues for market players to expand their global footprint and diversify their customer base.

Furthermore, continuous research and development in sustainable and bio-based photocuring agents present a compelling opportunity for market innovation. With increasing consumer and regulatory pressure for greener products, developing photoinitiators derived from renewable resources or with improved biodegradability can open up new markets and significantly differentiate products. Niche applications in biomedical devices, microelectronics, and aerospace, which require highly specialized and high-performance curing solutions, also represent lucrative growth areas. These segments demand tailor-made formulations that can achieve extreme precision, durability, and biocompatibility, pushing the boundaries of existing photocuring technology and driving demand for advanced, high-value agents. Strategic collaborations between material scientists, chemical companies, and end-use manufacturers will be key to capitalizing on these emerging opportunities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into emerging markets and developing economies | +1.9% | APAC, Latin America, MEA | 2025-2033 |

| Development of sustainable and bio-based photocuring agents | +1.6% | Global, particularly Europe & North America | 2027-2033 |

| Growth in niche, high-value applications (e.g., biomedical, microelectronics) | +1.4% | North America, Europe, Japan | 2025-2033 |

| Advancements in LED curing technology and corresponding photoinitiators | +1.1% | Global | 2025-2033 |

| Strategic partnerships and collaborations for product innovation | +0.8% | Global | 2025-2033 |

Photocuring Agent Market Challenges Impact Analysis

The photocuring agent market faces notable challenges related to the need for continuous performance optimization across a diverse range of substrates and application conditions. Achieving consistent, high-quality curing on various materials, from plastics and metals to paper and composites, demands highly versatile and often specialized formulations. This complexity is compounded by the increasing demand for ultra-fast curing speeds without compromising adhesion, durability, or optical properties. Developing agents that offer broad spectral absorption, minimal yellowing, and excellent depth of cure for thick films remains a significant hurdle. These technical demands often necessitate extensive R&D and specialized synthesis, pushing development costs higher and extending time-to-market for new products, particularly for niche applications.

Another critical challenge involves navigating the evolving regulatory landscape surrounding chemical safety and environmental impact. With increasing scrutiny on potentially harmful chemicals, manufacturers of photocuring agents must constantly adapt their product portfolios to comply with new regulations, such as those related to REACH in Europe or various national chemical inventories. This often requires significant investment in toxicological testing, regulatory documentation, and potentially reformulating established products. Furthermore, maintaining a stable supply chain for specialized raw materials, which can be subject to geopolitical disruptions, trade restrictions, or limited global availability, poses a continuous operational challenge that can impact production schedules and profitability. Addressing these multifaceted challenges requires a combination of robust R&D, proactive regulatory engagement, and resilient supply chain management strategies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Performance optimization for diverse substrates and applications | -1.4% | Global | 2025-2033 |

| Evolving and stringent environmental and health regulations | -1.1% | Europe, North America | 2025-2033 |

| Ensuring supply chain stability for key raw materials | -0.9% | Global | 2025-2033 |

| High R&D costs and long development cycles for novel agents | -0.8% | Global | 2025-2030 |

| Addressing specific limitations (e.g., oxygen inhibition, through-cure) | -0.6% | Global, R&D focused regions | 2025-2033 |

Photocuring Agent Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global photocuring agent market, offering detailed insights into market size, growth drivers, restraints, opportunities, and challenges. It covers a forecast period from 2025 to 2033, examining historical data to provide a robust foundation for future projections. The report segments the market by product type, application, and end-use industry across major global regions, offering a holistic view of the market's dynamics and competitive landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.85 Billion |

| Market Forecast in 2033 | USD 7.52 Billion |

| Growth Rate | 8.7% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Chem Solutions, Advanced Polymer Innovations, PhotoCure Technologies Inc., UV Curing Materials Corp., Light Activated Chemicals LLC, Radiant Solutions Group, Cured Innovations Ltd., Polymerization Accelerants Inc., Spectrum Chemicals Pvt. Ltd., BrightBeam Materials, Genesis Photopolymers, Synergy Curing Agents, Apex Chemical Systems, DuraCure Technologies, Quantum Photoinitiators, OptiCure Formulations, Universal Photochemicals, Innovate Materials, Precision Polymers, NextGen Curing Solutions |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The photocuring agent market is broadly segmented by type, application, and end-use industry, providing a granular view of its diverse landscape. This segmentation helps in understanding the specific demands and growth drivers within each category, enabling targeted market strategies and product development. The distinct properties and performance requirements across these segments dictate the type of photocuring agents utilized, influencing innovation and market share distribution. Each segment contributes uniquely to the overall market growth, with some exhibiting higher growth rates due to technological advancements or expanding end-use applications.

- By Type

- Free Radical Photoinitiators (Benzophenones, Acetophenones, Thioxanthones, Phosphine Oxides, Others)

- Cationic Photoinitiators (Sulfonium Salts, Iodonium Salts, Others)

- Photosensitizers

- By Application

- Coatings (Wood, Plastic, Paper & Film, Metal, Optical Fiber, Others)

- Inks (Packaging, Graphic Arts, Digital, Others)

- Adhesives (Medical, Industrial, Electronics, Others)

- 3D Printing

- Electronics

- Dental

- Others

- By End-Use Industry

- Automotive

- Packaging

- Printing & Graphic Arts

- Electronics

- Medical & Dental

- Wood & Furniture

- Industrial

- Others

Regional Highlights

- North America: Expected to maintain a significant market share due to robust R&D activities, high adoption of advanced manufacturing technologies, and stringent environmental regulations promoting UV/EB curing. The presence of key industry players and strong demand from automotive, electronics, and medical sectors contribute to its growth.

- Europe: A mature market characterized by strict environmental policies, pushing innovation towards sustainable and low-VOC photocuring solutions. Germany, France, and the UK are key contributors, driven by the packaging, automotive, and graphic arts industries.

- Asia Pacific (APAC): Projected to be the fastest-growing region, fueled by rapid industrialization, expanding manufacturing base (especially in China, India, Japan, and South Korea), increasing demand for electronics, automotive, and packaging, and growing adoption of 3D printing technology.

- Latin America: Emerging market with increasing industrial investments, particularly in Brazil and Mexico, leading to a rise in demand for advanced coatings and adhesives in automotive and construction sectors.

- Middle East and Africa (MEA): Growing infrastructure development and diversification of economies in countries like UAE and Saudi Arabia are creating new opportunities for photocuring agents in industrial coatings and construction materials.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Photocuring Agent Market.- Global Chem Solutions

- Advanced Polymer Innovations

- PhotoCure Technologies Inc.

- UV Curing Materials Corp.

- Light Activated Chemicals LLC

- Radiant Solutions Group

- Cured Innovations Ltd.

- Polymerization Accelerants Inc.

- Spectrum Chemicals Pvt. Ltd.

- BrightBeam Materials

- Genesis Photopolymers

- Synergy Curing Agents

- Apex Chemical Systems

- DuraCure Technologies

- Quantum Photoinitiators

- OptiCure Formulations

- Universal Photochemicals

- Innovate Materials

- Precision Polymers

- NextGen Curing Solutions

Frequently Asked Questions

What is a photocuring agent and how does it work?

A photocuring agent, often a photoinitiator, is a chemical compound that, upon exposure to light (typically UV or visible light), initiates a chemical reaction to cure or harden a resin, coating, or adhesive. It absorbs light energy to form reactive species (like free radicals or cations) that then trigger the polymerization of monomers and oligomers, transforming a liquid formulation into a solid. This process is rapid and solvent-free.

Which industries are the primary consumers of photocuring agents?

Photocuring agents are predominantly utilized in industries requiring rapid and efficient curing processes, minimal VOC emissions, and high-performance material properties. Key sectors include coatings (wood, plastic, metal), printing inks (packaging, graphic arts, digital), adhesives (medical, industrial, electronics), 3D printing and additive manufacturing, and electronics (for circuit boards and displays).

What are the environmental benefits of using photocuring agents?

The primary environmental benefits of photocuring agents stem from their use in UV/EB curing technologies, which are solvent-free. This significantly reduces Volatile Organic Compound (VOC) emissions, contributing to cleaner air and a safer working environment. Additionally, these processes are energy-efficient, often requiring less energy and curing faster than traditional thermal methods, further reducing environmental impact.

How does 3D printing impact the demand for photocuring agents?

3D printing, particularly stereolithography (SLA) and digital light processing (DLP), heavily relies on photopolymerization, directly increasing the demand for specialized photocuring agents. These agents enable the rapid solidification of liquid resins layer by layer to create intricate 3D objects. The growth of additive manufacturing across various industries drives the need for high-performance, tailored photocuring agents that offer precision, speed, and specific material properties.

What challenges does the photocuring agent market currently face?

The photocuring agent market faces challenges such as high initial investment costs for UV/EB curing equipment, volatility in raw material prices, and the need for continuous performance optimization across diverse substrates. Additionally, stringent and evolving environmental regulations require constant innovation and reformulation to ensure product compliance and safety, while technical limitations like oxygen inhibition and achieving through-cure in thick films also pose hurdles.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted