Phosphate Fertilizer Market

Phosphate Fertilizer Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710100 | Last Updated : December 29, 2025 |

Format : ![]()

![]()

![]()

![]()

Phosphate Fertilizer Market Size

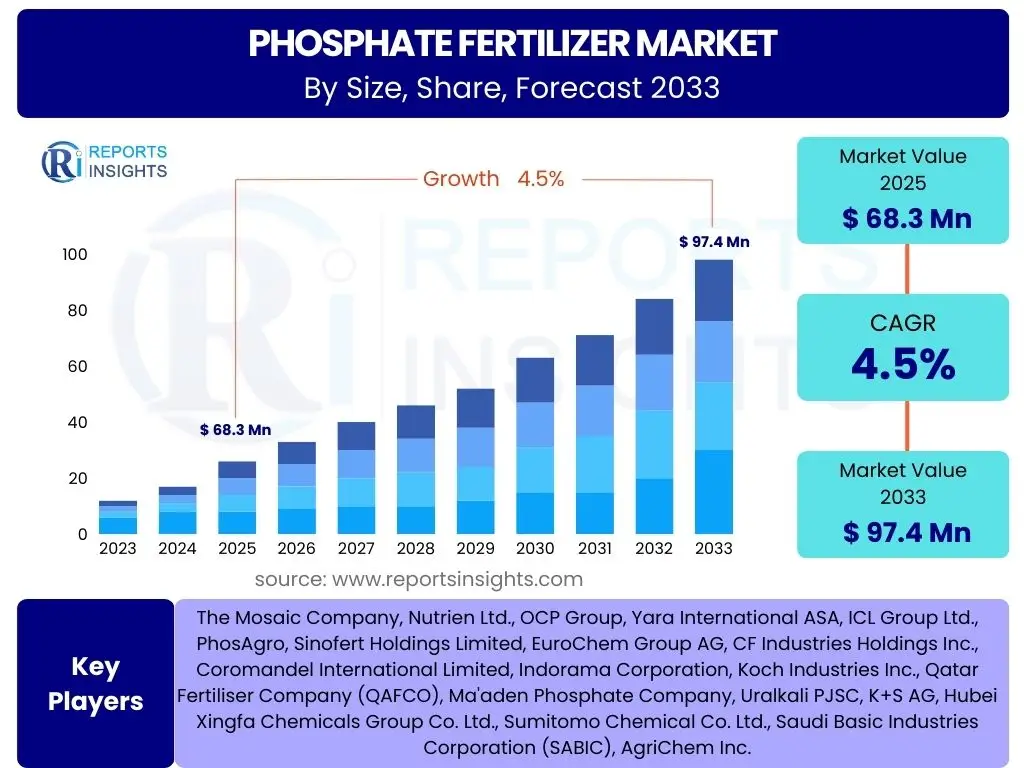

According to Reports Insights Consulting Pvt Ltd, The Phosphate Fertilizer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033. The market is estimated at USD 68.3 billion in 2025 and is projected to reach USD 97.4 billion by the end of the forecast period in 2033.

Key Phosphate Fertilizer Market Trends & Insights

User queries regarding market trends in the phosphate fertilizer sector frequently center on sustainability, demand drivers from evolving agricultural practices, and the influence of geopolitical factors on supply chains. There is significant interest in how technological advancements are reshaping the industry, alongside concerns about environmental impacts and the shift towards more efficient and environmentally friendly fertilizer solutions. The analysis indicates a strong focus on balancing agricultural productivity with ecological responsibility, driving innovation in product formulation and application methods.

Furthermore, an increasing number of questions pertain to regional demand shifts, particularly in emerging economies, and the impact of fluctuating raw material prices on overall market stability. Stakeholders are also keen on understanding the adoption rates of precision agriculture techniques and how these methods are influencing the demand for specific types of phosphate fertilizers. The overarching theme from user inquiries highlights a market in transition, adapting to both global food security imperatives and stringent environmental regulations.

- Growing adoption of precision agriculture techniques optimizing fertilizer use.

- Increasing focus on enhanced efficiency fertilizers (EEFs) to reduce environmental impact.

- Shift towards sustainable and eco-friendly agricultural practices.

- Volatile raw material prices and geopolitical tensions impacting supply chains.

- Rising demand for high-yield crops driven by global population growth.

AI Impact Analysis on Phosphate Fertilizer

Common user questions regarding AI's impact on the phosphate fertilizer market reveal an interest in how artificial intelligence can enhance efficiency, optimize resource allocation, and foster sustainability. Users frequently inquire about AI's role in precision farming, including data-driven recommendations for fertilizer application, predictive analytics for crop yield, and automated monitoring of soil health. There is also a keen focus on how AI can streamline supply chain logistics, from raw material sourcing to distribution, thereby reducing waste and improving operational performance across the value chain.

Furthermore, inquiries often extend to AI's potential in developing novel fertilizer formulations, particularly in identifying optimal nutrient combinations and predicting their efficacy under varying environmental conditions. Concerns are also raised regarding the accessibility and implementation costs of AI technologies for smaller agricultural enterprises, along with the need for robust data infrastructure and skilled personnel. Despite these challenges, the prevailing expectation is that AI will play a transformative role, leading to more sustainable, productive, and cost-effective agricultural practices within the phosphate fertilizer domain.

- Precision application of phosphate fertilizers via AI-driven analytics, reducing waste.

- Optimized supply chain management and logistics through AI-powered predictive modeling.

- Enhanced R&D for novel fertilizer formulations using AI to analyze nutrient efficacy.

- Real-time soil and crop health monitoring to recommend specific phosphate needs.

- Improved production efficiency and quality control in manufacturing processes.

Key Takeaways Phosphate Fertilizer Market Size & Forecast

Analysis of common user questions regarding key takeaways from the phosphate fertilizer market size and forecast emphasizes a strong interest in the primary drivers of growth, particularly global food demand and agricultural intensification. Users seek concise summaries of what will most significantly influence market expansion, including the increasing adoption of modern farming techniques and the critical role of developing economies. Insights are frequently requested on the segments expected to exhibit the most robust growth and the underlying reasons for their anticipated performance.

Furthermore, stakeholders are keen to understand the prevailing challenges that could impede market growth, such as environmental regulations and supply chain vulnerabilities, and how these factors are integrated into long-term forecasts. The synthesis of user inquiries highlights a demand for clear, actionable insights that not only quantify market potential but also contextualize it within the broader agricultural and economic landscape. This includes a focus on the evolving competitive dynamics and the potential for innovation to mitigate risks and unlock new opportunities.

- Global food demand and declining arable land remain primary growth catalysts.

- Asia Pacific region is projected to be the fastest-growing market due to agricultural expansion.

- Enhanced efficiency and specialty phosphate fertilizers are gaining traction due to environmental concerns.

- Fluctuations in raw material prices and geopolitical events present persistent market volatility.

- Sustainability initiatives and regulatory pressures are reshaping product development and market strategies.

Phosphate Fertilizer Market Drivers Analysis

The phosphate fertilizer market is propelled by a confluence of factors primarily centered on the escalating global demand for food, driven by a continually expanding human population. As urbanization encroaches on arable land, the imperative to maximize yields from existing agricultural areas becomes critical, directly increasing the need for effective crop nutrition. This demographic pressure, coupled with evolving dietary patterns that favor protein-rich foods requiring more intensive cultivation, significantly underpins the market's growth trajectory.

Technological advancements in agriculture, such as precision farming and protected cultivation, further amplify the demand for phosphate fertilizers by enabling more efficient and targeted application, thereby optimizing crop productivity. Government policies and subsidies in many regions, aimed at bolstering food security and supporting agricultural output, also play a crucial role in encouraging fertilizer use. The intersection of these demographic, technological, and policy-driven forces creates a robust environment for sustained market expansion, despite potential environmental or economic headwinds.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Population Growth and Food Demand | +1.5% | Globally, particularly Asia Pacific & Africa | Long-term (2025-2033) |

| Declining Arable Land & Agricultural Intensification | +1.2% | Globally, acute in densely populated regions | Mid to Long-term (2025-2033) |

| Increasing Adoption of Precision Agriculture | +0.8% | North America, Europe, parts of Asia Pacific | Mid-term (2026-2030) |

| Government Support & Subsidies for Farmers | +0.5% | India, China, EU, USA | Short to Mid-term (2025-2029) |

| Growth in Biofuel Production | +0.3% | North America, Latin America, Europe | Mid-term (2027-2031) |

Phosphate Fertilizer Market Restraints Analysis

The phosphate fertilizer market faces several significant restraints that could temper its projected growth. Environmental concerns represent a major impediment, with issues such as water pollution from nutrient runoff (eutrophication) and the carbon footprint associated with fertilizer production leading to increased scrutiny and stricter regulations. This pushes producers towards more costly, environmentally compliant manufacturing processes and farmers towards cautious application, potentially limiting market expansion. The long-term sustainability of phosphorus resources, a finite element, also poses a fundamental constraint as reserves become more challenging and expensive to extract.

Furthermore, the inherent volatility of raw material prices, particularly for phosphate rock and sulfur, creates significant cost uncertainty for manufacturers, which can then be passed on to farmers, impacting demand. Geopolitical instability and trade disputes can disrupt supply chains, affecting the availability and cost of these critical inputs. Economic factors such as fluctuating crop prices and farmers' purchasing power also play a role, as lower agricultural incomes can lead to reduced fertilizer expenditure, particularly in price-sensitive developing markets, thus acting as a brake on overall market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Environmental Regulations & Eutrophication Concerns | -1.0% | Europe, North America, increasingly Asia Pacific | Long-term (2025-2033) |

| Volatile Raw Material Prices (Phosphate Rock, Sulfur) | -0.7% | Globally, impacting import-dependent regions | Short to Mid-term (2025-2029) |

| Geopolitical Instability & Supply Chain Disruptions | -0.6% | Globally, affecting major producers & consumers | Short-term (2025-2027) |

| High Initial Investment & Operating Costs | -0.4% | Developing countries, small-scale farmers | Mid to Long-term (2025-2033) |

| Development of Alternative Crop Nutrient Sources | -0.2% | Globally, niche markets currently | Long-term (2030-2033) |

Phosphate Fertilizer Market Opportunities Analysis

Significant opportunities in the phosphate fertilizer market are emerging from the growing emphasis on sustainable agricultural practices and the demand for higher efficiency products. The development and adoption of enhanced efficiency fertilizers (EEFs), including slow-release and controlled-release variants, present a strong growth avenue. These products reduce nutrient loss, optimize uptake, and minimize environmental impact, aligning with both regulatory pressures and farmer preferences for greater economic and ecological efficiency. Investment in research and development for bio-based or organic phosphate alternatives also represents a nascent but potentially impactful opportunity, especially in markets driven by organic food consumption trends.

Furthermore, the expansion of agricultural land and intensification of farming in developing economies, particularly in Africa and parts of Asia, offer substantial untapped market potential. As these regions strive for food self-sufficiency and improved crop yields, the demand for foundational agricultural inputs like phosphate fertilizers is set to surge. Strategic partnerships and investments in local production facilities within these regions could significantly capture this growth. The integration of digital agriculture and data analytics for precision nutrient management also opens new avenues for specialized service offerings and products, allowing for tailored fertilizer solutions that enhance crop productivity while reducing overall input requirements.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Enhanced Efficiency Fertilizers (EEFs) | +1.0% | Globally, strong in developed markets | Mid to Long-term (2026-2033) |

| Untapped Market Potential in Developing Economies (Africa, SE Asia) | +0.9% | Africa, South & Southeast Asia | Long-term (2027-2033) |

| Technological Advancements in Application Methods | +0.6% | North America, Europe, Australia | Mid-term (2026-2030) |

| Circular Economy & Phosphate Recycling Initiatives | +0.4% | Europe, Japan, increasing globally | Long-term (2028-2033) |

| Demand for Specialty Fertilizers for Specific Crops | +0.3% | Globally, particularly horticulture | Mid-term (2025-2030) |

Phosphate Fertilizer Market Challenges Impact Analysis

The phosphate fertilizer market is confronted by several significant challenges that necessitate strategic adaptation from industry participants. Environmental compliance remains a persistent hurdle, with increasing regulatory pressures worldwide aimed at mitigating nutrient runoff and greenhouse gas emissions from fertilizer production and use. Meeting these stringent standards often requires substantial capital investment in new technologies and processes, which can increase operational costs and complexity. Furthermore, the limited and geographically concentrated nature of high-grade phosphate rock reserves poses a long-term supply security challenge, fostering geopolitical tensions and price volatility.

Another critical challenge is the inherent sensitivity of agricultural markets to climatic variations and global economic downturns. Unfavorable weather patterns, such as droughts or floods, can severely impact crop yields and farmer incomes, directly leading to reduced demand for fertilizers. Similarly, economic recessions can compress agricultural spending, affecting fertilizer sales. The need for continuous innovation to develop more efficient and environmentally benign products also presents a formidable R&D challenge, requiring significant investment without guaranteed returns, as the market balances productivity needs with ecological responsibilities.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations | -0.8% | Europe, North America, China | Long-term (2025-2033) |

| Depletion of High-Grade Phosphate Rock Reserves | -0.7% | Globally, affecting major producers | Long-term (2030-2033) |

| Climate Change Impact on Agricultural Productivity | -0.5% | Globally, vulnerable agricultural regions | Mid to Long-term (2026-2033) |

| Supply Chain Disruptions & Logistics Costs | -0.4% | Globally, exacerbated by geopolitical events | Short to Mid-term (2025-2029) |

| Competition from Alternative Nutrient Sources | -0.3% | Developed markets with organic farming focus | Mid-term (2027-2032) |

Phosphate Fertilizer Market - Updated Report Scope

This report provides a comprehensive analysis of the global Phosphate Fertilizer Market, examining key trends, growth drivers, restraints, and opportunities shaping its trajectory from 2025 to 2033. It offers a detailed segmentation analysis across product types, applications, forms, and regions, alongside an in-depth competitive landscape featuring major market participants. The scope extends to assessing the impact of emerging technologies and evolving regulatory environments on market dynamics, providing strategic insights for stakeholders to navigate the complexities and capitalize on future growth prospects.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 68.3 billion |

| Market Forecast in 2033 | USD 97.4 billion |

| Growth Rate | 4.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | The Mosaic Company, Nutrien Ltd., OCP Group, Yara International ASA, ICL Group Ltd., PhosAgro, Sinofert Holdings Limited, EuroChem Group AG, CF Industries Holdings Inc., Coromandel International Limited, Indorama Corporation, Koch Industries Inc., Qatar Fertiliser Company (QAFCO), Ma'aden Phosphate Company, Uralkali PJSC, K+S AG, Hubei Xingfa Chemicals Group Co. Ltd., Sumitomo Chemical Co. Ltd., Saudi Basic Industries Corporation (SABIC), AgriChem Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The phosphate fertilizer market is intricately segmented to provide a granular view of its diverse components, facilitating a deeper understanding of market dynamics and consumer preferences. Product type segmentation, encompassing Diammonium Phosphate (DAP), Monoammonium Phosphate (MAP), Triple Superphosphate (TSP), and Single Superphosphate (SSP), reveals varying demands based on crop specific nutrient requirements, soil conditions, and agricultural practices globally. DAP and MAP typically dominate due to their high nutrient content and versatility across a broad range of crops and application methods.

Application-based segmentation highlights the primary end-uses, with grains and cereals, oilseeds and pulses, and fruits and vegetables being the major consumers. This segmentation underscores the direct link between global food production patterns and fertilizer demand. Furthermore, the market is analyzed by form, distinguishing between dry and liquid fertilizers, reflecting preferences influenced by application technology, cost-effectiveness, and nutrient delivery efficiency. Each segment's growth trajectory is influenced by a unique combination of agricultural trends, technological advancements, and regional economic factors.

- By Product Type: Diammonium Phosphate (DAP), Monoammonium Phosphate (MAP), Triple Superphosphate (TSP), Single Superphosphate (SSP), Other Phosphate Fertilizers

- By Application: Grains & Cereals, Oilseeds & Pulses, Fruits & Vegetables, Other Crops

- By Form: Dry, Liquid

Regional Highlights

- Asia Pacific: This region stands as the largest and fastest-growing market for phosphate fertilizers, driven by a massive population, increasing food demand, and extensive agricultural land in countries like China, India, and Southeast Asian nations. Government support for agricultural modernization and improving farming incomes further stimulate demand.

- North America: A mature market characterized by advanced agricultural practices, high adoption of precision farming, and a strong focus on high-yield crop cultivation. Demand here is stable, with a growing emphasis on enhanced efficiency and specialty fertilizers to optimize input use.

- Europe: The European market is highly regulated, prioritizing environmental sustainability and nutrient use efficiency. Growth is moderate, with a strong shift towards specialty and slow-release phosphate fertilizers to comply with strict environmental norms and reduce pollution.

- Latin America: This region, particularly Brazil and Argentina, represents a significant growth market due to expanding agricultural frontiers, large-scale cultivation of soybeans, corn, and sugarcane, and increasing exports of agricultural commodities. Investment in modern farming techniques is on the rise.

- Middle East and Africa (MEA): Africa is poised for substantial growth as efforts to enhance food security and develop agricultural infrastructure intensify. The Middle East, with its significant phosphate rock reserves (e.g., Morocco, Saudi Arabia), plays a crucial role in global supply, while also increasing domestic fertilizer consumption.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Phosphate Fertilizer Market.- The Mosaic Company

- Nutrien Ltd.

- OCP Group

- Yara International ASA

- ICL Group Ltd.

- PhosAgro

- Sinofert Holdings Limited

- EuroChem Group AG

- CF Industries Holdings Inc.

- Coromandel International Limited

- Indorama Corporation

- Koch Industries Inc.

- Qatar Fertiliser Company (QAFCO)

- Ma'aden Phosphate Company

- Uralkali PJSC

- K+S AG

- Hubei Xingfa Chemicals Group Co. Ltd.

- Sumitomo Chemical Co. Ltd.

- Saudi Basic Industries Corporation (SABIC)

- AgriChem Inc.

Frequently Asked Questions

What is phosphate fertilizer?

Phosphate fertilizer is any fertilizer material that contains phosphorus in forms available to plants, crucial for root development, flowering, and fruit/seed production. It is derived primarily from phosphate rock and essential for agricultural productivity.

What are the primary drivers of the phosphate fertilizer market?

Key drivers include global population growth leading to increased food demand, declining arable land necessitating higher yields, growing adoption of precision agriculture, and government initiatives supporting agricultural output worldwide.

What are the main environmental concerns associated with phosphate fertilizers?

The primary environmental concerns are nutrient runoff into water bodies, leading to eutrophication and algal blooms, which harm aquatic ecosystems. Over-application can also lead to soil nutrient imbalances.

How is AI impacting the phosphate fertilizer industry?

AI is impacting the industry through precision agriculture for optimized application, supply chain optimization, predictive analytics for demand and production, and assisting in the research and development of more efficient and sustainable fertilizer formulations.

Which regions exhibit the highest growth potential for phosphate fertilizers?

The Asia Pacific region, particularly countries like China and India, along with emerging markets in Africa, show the highest growth potential due to expanding agriculture, increasing food consumption, and efforts to improve crop yields.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted