Phenolic Resin Market

Phenolic Resin Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700125 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

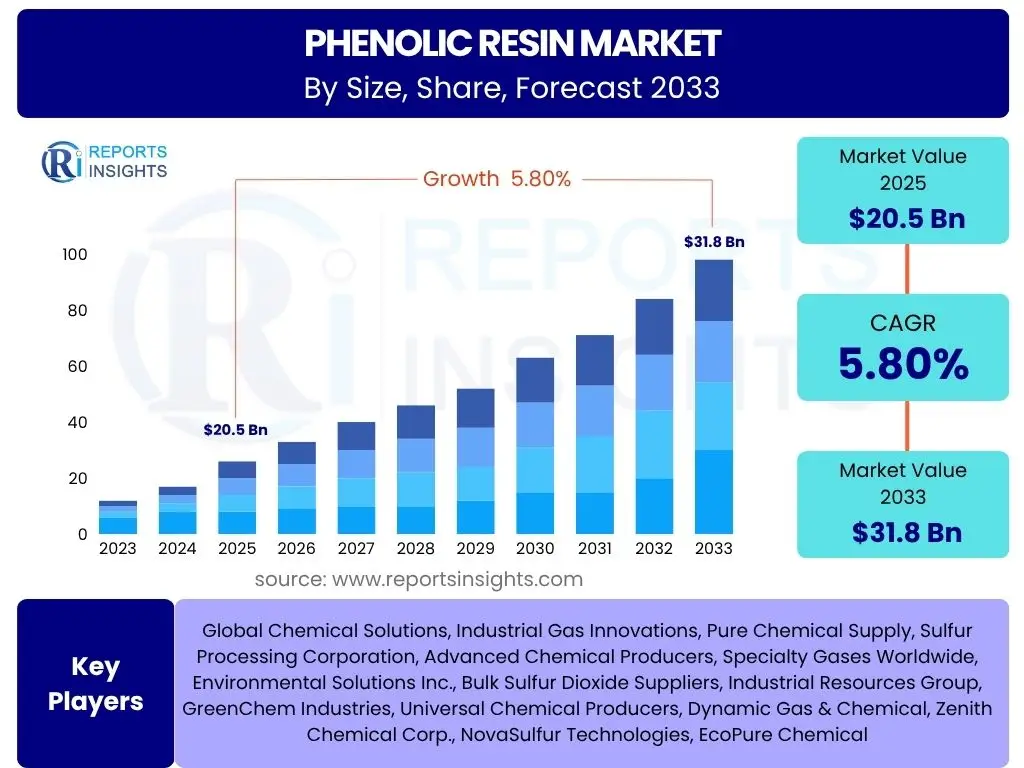

Phenolic Resin Market is projected to grow at a Compound annual growth rate (CAGR) of 5.8% between 2025 and 2033, reaching an estimated USD 20.5 Billion in 2025 and is projected to grow to USD 31.8 Billion by 2033 the end of the forecast period.

Key Phenolic Resin Market Trends & Insights

The phenolic resin market is experiencing dynamic shifts driven by evolving industrial demands and increasing focus on sustainability. Key trends include a growing preference for bio-based and environmentally friendly resin alternatives, driven by stringent environmental regulations and consumer demand for sustainable products. Additionally, technological advancements are leading to the development of high-performance phenolic resins with enhanced thermal stability, mechanical strength, and flame retardancy, opening new application avenues across various sectors. The integration of these advanced materials is crucial for industries aiming to improve product durability and safety while also addressing specific performance requirements in challenging environments.

- Shift towards sustainable and bio-based phenolic resin formulations.

- Increasing adoption in electric vehicle (EV) components for lightweighting and thermal management.

- Growing demand for fire-retardant materials in building and construction.

- Advancements in composite manufacturing utilizing phenolic resins.

- Expansion into specialty applications requiring high heat and chemical resistance.

- Digitalization and automation improving production efficiency and quality control.

- Emphasis on circular economy principles influencing resin lifecycle and recycling.

AI Impact Analysis on Phenolic Resin

Artificial Intelligence (AI) is set to revolutionize various facets of the phenolic resin market, from raw material sourcing to end-product development and sales. AI-driven analytics can optimize production processes by predicting equipment failures, refining reaction parameters, and improving yield, leading to significant cost savings and enhanced product consistency. Furthermore, AI can accelerate research and development by simulating molecular structures and predicting material properties, thus enabling faster innovation in novel resin formulations, including those with enhanced sustainability profiles or specialized performance characteristics. This capability significantly reduces the time and resources typically required for traditional empirical experimentation, fostering more rapid market introduction of new products.

- Optimization of production processes and energy consumption through predictive analytics.

- Accelerated research and development of new resin formulations and properties.

- Enhanced quality control and defect detection in manufacturing.

- Intelligent supply chain management for raw materials and finished products.

- Personalized customer solutions and demand forecasting for specific applications.

Key Takeaways Phenolic Resin Market Size & Forecast

- Market projected to reach USD 31.8 Billion by 2033.

- Compound Annual Growth Rate (CAGR) of 5.8% from 2025 to 2033.

- Significant growth fueled by construction, automotive, and electronics sectors.

- Bio-based resin development contributing to market expansion.

- Asia Pacific continues to lead market share and growth.

Phenolic Resin Market Drivers Analysis

The phenolic resin market is significantly propelled by robust demand from diverse end-use industries that leverage the material's superior properties. Its inherent thermal stability, chemical resistance, and excellent bonding capabilities make it indispensable in applications ranging from automotive components to construction materials. The escalating global construction activities, particularly in emerging economies, are driving the need for durable and fire-resistant building materials, where phenolic resins find extensive use in insulation and laminates. Similarly, the automotive sector's continuous evolution, marked by a shift towards lightweighting and enhanced safety features, fuels the demand for phenolic resins in friction materials, composite parts, and interior components.

Furthermore, the electronics industry relies heavily on phenolic resins for producing circuit boards and electrical laminates, benefiting from their insulating properties and dimensional stability. The growing global demand for electronics, spurred by digitalization and connectivity trends, directly translates into increased consumption of these resins. Beyond these sectors, the unique properties of phenolic resins also make them critical in abrasives, foundry applications, and specialty coatings, ensuring a broad and diversified demand base that underpins the market's consistent growth trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising demand from the construction industry for insulation and fire-retardant materials | +1.5% | Asia Pacific, Middle East & Africa, North America | Short to Medium Term (2025-2029) |

| Increasing use in the automotive sector for lightweight components and friction materials | +1.2% | Asia Pacific, Europe, North America | Medium Term (2027-2033) |

| Growing application in electrical and electronics for laminates and circuit boards | +1.0% | Asia Pacific, North America, Europe | Short to Medium Term (2025-2030) |

| Technological advancements leading to high-performance and specialty phenolic resins | +0.8% | Global, particularly developed regions | Medium to Long Term (2028-2033) |

| Expansion of the abrasives and foundry industries globally | +0.5% | Asia Pacific, Europe | Short Term (2025-2028) |

Phenolic Resin Market Restraints Analysis

Despite significant growth drivers, the phenolic resin market faces several notable restraints that could temper its expansion. One of the primary concerns is the volatility in the prices of key raw materials, namely phenol and formaldehyde. These petrochemical derivatives are subject to fluctuations based on crude oil prices, supply chain disruptions, and geopolitical events, directly impacting the production costs and profit margins for resin manufacturers. Such unpredictable cost structures can deter new investments and make long-term planning challenging for market players, especially smaller enterprises.

Another significant restraint is the increasing environmental scrutiny and stringent regulatory frameworks concerning formaldehyde emissions. Formaldehyde, a crucial component in phenolic resin synthesis, is classified as a hazardous substance, leading to tighter regulations on its production, handling, and application. This necessitates significant investments in emission control technologies and the development of low-formaldehyde or formaldehyde-free resin alternatives, which can be technologically challenging and costly. Furthermore, the market faces competition from alternative materials such as epoxy resins, polyurethanes, and melamine resins, which offer comparable or superior properties in certain applications, providing end-users with more choices and potentially limiting the market share of phenolic resins in specific segments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in prices of key raw materials (phenol, formaldehyde) | -0.9% | Global | Short to Medium Term (2025-2029) |

| Stringent environmental regulations regarding formaldehyde emissions | -0.7% | Europe, North America, Asia Pacific (China) | Medium to Long Term (2027-2033) |

| Competition from alternative resins (epoxy, polyurethane, melamine) | -0.5% | Global | Long Term (2030-2033) |

| Concerns over long-term health effects of traditional phenolic resin production | -0.3% | Developed regions, increasing globally | Medium to Long Term (2028-2033) |

Phenolic Resin Market Opportunities Analysis

The phenolic resin market is poised to capitalize on several emerging opportunities driven by innovation, sustainability goals, and evolving industrial requirements. A significant opportunity lies in the development and adoption of bio-based phenolic resins. As industries increasingly prioritize eco-friendly materials and reduce their carbon footprint, research into sustainable alternatives derived from renewable sources like lignin, cashew nutshell liquid, and natural oils is gaining momentum. These bio-based resins offer a greener alternative to traditional petroleum-derived products, aligning with global sustainability initiatives and potentially opening new markets driven by environmental consciousness and regulatory incentives.

Furthermore, the global shift towards lightweighting in the automotive, aerospace, and defense sectors presents a substantial opportunity for phenolic resins. Their excellent strength-to-weight ratio when used in composites makes them ideal for replacing heavier metallic components, contributing to fuel efficiency and reduced emissions. The rapid expansion of electric vehicles (EVs) also offers a niche for phenolic resins in battery components, insulation, and charging infrastructure due to their thermal stability and flame retardancy. Lastly, advancements in nanotechnology and material science are enabling the creation of enhanced phenolic resins with superior properties, such as improved impact resistance, higher temperature tolerance, and multifunctionality, which can unlock novel applications and command premium pricing in specialized high-performance markets.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and commercialization of bio-based phenolic resins | +1.3% | Europe, North America, Asia Pacific | Medium to Long Term (2028-2033) |

| Growing demand for lightweight materials in automotive and aerospace industries | +1.1% | Global, particularly developed economies | Medium Term (2027-2032) |

| Increasing application in electric vehicle (EV) manufacturing for thermal management and composites | +0.9% | Asia Pacific, Europe, North America | Short to Medium Term (2025-2030) |

| Innovations in resin properties through nanotechnology and advanced compounding techniques | +0.7% | Global | Long Term (2030-2033) |

| Expansion into emerging markets with rapid industrialization | +0.6% | Southeast Asia, Latin America, Africa | Short to Medium Term (2025-2030) |

Phenolic Resin Market Challenges Impact Analysis

The phenolic resin market, while promising, grapples with a set of inherent challenges that necessitate strategic responses from manufacturers. One significant hurdle is the increasing regulatory complexity surrounding the production and use of chemicals, particularly those involving volatile organic compounds (VOCs) and formaldehyde. Compliance with diverse and evolving environmental and health regulations across different geographies requires substantial investment in research, process modification, and certification, adding to operational costs and potentially slowing down market entry for new products or formulations. This regulatory burden can disproportionately affect smaller players and limit the widespread adoption of certain resin types.

Another critical challenge is managing supply chain disruptions, which have become more frequent and severe in recent years. Geopolitical instability, natural disasters, and global health crises can impact the availability and cost of raw materials like phenol and formaldehyde, leading to production delays and increased prices. Ensuring a resilient and diversified supply chain requires robust risk management strategies and potentially regionalizing production, which can be a complex logistical and financial undertaking. Furthermore, the market faces intense competition from established alternative materials and new entrants, requiring continuous innovation and differentiation to maintain market share and profitability. Developing cost-effective, high-performance, and environmentally compliant phenolic resin solutions remains a persistent challenge that demands significant R&D efforts and strategic partnerships.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Compliance with increasingly stringent environmental regulations and health standards | -0.8% | Europe, North America, key Asian countries | Medium to Long Term (2027-2033) |

| Managing supply chain disruptions and raw material availability challenges | -0.6% | Global | Short to Medium Term (2025-2029) |

| High research and development costs for sustainable and advanced resin formulations | -0.4% | Global | Medium Term (2027-2032) |

| Disposal and recycling challenges for phenolic resin-based products | -0.2% | Developed regions with strong environmental policies | Long Term (2030-2033) |

Phenolic Resin Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Phenolic Resin Market, offering critical insights into its current landscape and future growth trajectory. The report covers detailed market projections, trends, drivers, restraints, opportunities, and challenges influencing the industry across various segments and key geographical regions. It serves as an essential resource for stakeholders seeking to understand market dynamics, competitive intelligence, and strategic growth avenues.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 20.5 Billion |

| Market Forecast in 2033 | USD 31.8 Billion |

| Growth Rate | 5.8% from 2025 to 2033 |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Mitsui Chemicals, Hexion, DIC Corporation, Sumitomo Bakelite, Georgia-Pacific Chemicals, Chang Chun Group, Prefere Resins, SI Group, Kyowa Kirin, Shandong Shengquan Chemicals, ASK Chemicals, Kolon Industries, Arclin, Allnex, Ashland, BASF, Dairen Chemical, Jinan Shengquan Group, Capital Resin Corporation, Red Avenue New Materials Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Phenolic Resin Market is meticulously segmented to provide a granular understanding of its diverse applications and market dynamics. This comprehensive segmentation allows for precise analysis of growth drivers and challenges across various product types, applications, end-use industries, and forms, catering to the nuanced needs of different market participants. Understanding these distinct segments is crucial for strategic decision-making, identifying niche opportunities, and developing targeted market approaches.

By Type: This segment categorizes phenolic resins based on their chemical composition and curing characteristics, which dictate their specific applications and performance properties.

- Resol: These resins are typically used for their strong adhesive properties and resistance to heat, commonly found in laminates, coatings, and molding compounds.

- Novolac: Requiring a hardening agent, Novolac resins are known for their high strength and thermal stability, making them ideal for abrasives, friction materials, and refractory applications.

- Others: This category includes modified phenolic resins and specialized formulations designed for niche applications that demand unique performance attributes, such as enhanced flexibility or specific chemical resistance.

By Application: This segmentation highlights the primary uses of phenolic resins across various industrial and consumer products, demonstrating their versatility and indispensability in numerous manufacturing processes.

- Wood Adhesives: Extensive use in plywood, particleboard, and other engineered wood products due to strong bonding and moisture resistance.

- Building & Construction: Critical for insulation materials (e.g., phenolic foam), fire-resistant laminates, and composite panels that require structural integrity and safety features.

- Automotive: Employed in brake linings, clutch facings, engine components, and composite parts for their heat resistance and mechanical strength, contributing to vehicle safety and lightweighting.

- Electrical & Electronics: Essential for manufacturing printed circuit boards (PCBs), electrical laminates, and insulation components due to excellent dielectric properties and thermal stability.

- Abrasives: Binders for grinding wheels, sandpaper, and other abrasive tools, providing durability and heat resistance during high-friction operations.

- Coatings: Used in protective coatings requiring chemical resistance, hardness, and thermal stability for industrial and marine applications.

- Molding Compounds: For producing durable, heat-resistant molded articles used in various industries.

- Industrial (Foundry, Refractories): Crucial binders in foundry sands and refractory bricks for their high-temperature resistance and binding efficiency.

- Aerospace: In lightweight composites and flame-retardant interior components.

- Marine: For composite structures and fire safety applications.

- Oil & Gas: In various drilling and processing equipment due to chemical and thermal stability.

- Others: Including applications in consumer goods, sports equipment, and specialized industrial uses.

By End-Use Industry: This segment provides a broader perspective on the major industries that consume phenolic resins, illustrating the market's reliance on global industrial growth and sector-specific trends.

- Construction: Driven by infrastructure development and housing demand, utilizing resins in insulation, panels, and adhesives.

- Automotive: Propelled by vehicle production, electric vehicle growth, and the demand for performance and safety components.

- Electrical & Electronics: Supported by the expanding consumer electronics market, telecommunications, and industrial automation.

- Furniture: For durable and moisture-resistant wood products and laminates.

- Consumer Goods: In various molded articles and components requiring durability and heat resistance.

- Aerospace & Defense: For high-performance composites and fire-resistant materials in aircraft and defense equipment.

- Marine: For boat building and marine structural components due to water resistance and durability.

- Industrial Manufacturing: Encompassing a wide range of uses in foundry, abrasives, and other industrial processes.

By Form: This segmentation categorizes phenolic resins based on their physical state, which influences their handling, processing, and suitability for different manufacturing techniques.

- Liquid: Versatile and easy to process, commonly used in impregnating, coating, and adhesive applications.

- Solid: Often available in flakes or lumps, suitable for molding compounds, laminates, and certain adhesive formulations.

- Powder: Used in specific molding applications, abrasives, and refractory binders for precise material distribution and curing.

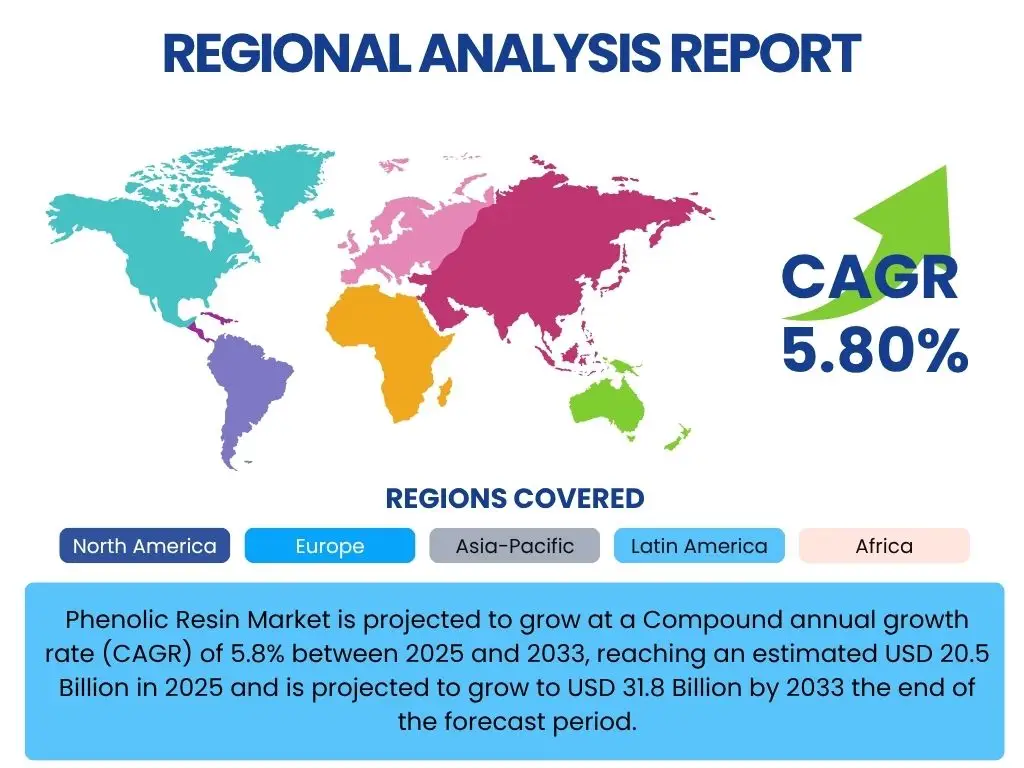

Regional Highlights

The global phenolic resin market exhibits significant regional variations, driven by industrial development, regulatory landscapes, and raw material availability. Asia Pacific stands as the leading region, accounting for the largest share of the market and demonstrating the highest growth rate. This dominance is primarily attributed to rapid industrialization, burgeoning construction activities, and the booming automotive and electronics manufacturing sectors in countries like China, India, Japan, and South Korea. The region benefits from a large consumer base, lower manufacturing costs, and increasing foreign investments, which collectively fuel the demand for phenolic resins across numerous applications.

Europe and North America represent mature markets for phenolic resins, characterized by stringent environmental regulations and a strong emphasis on sustainable and high-performance materials. While these regions exhibit steady growth, innovation is a key driver, with a focus on developing bio-based resins, advanced composites for aerospace and automotive, and specialized flame-retardant solutions. The demand here is largely driven by replacement and upgrade activities in infrastructure, along with a focus on advanced manufacturing techniques. Latin America, the Middle East, and Africa (MEA) are emerging markets, showing promising growth due to increasing industrialization, infrastructure development projects, and a rising focus on diversified manufacturing capabilities. Investments in construction, oil and gas, and automotive sectors are expected to bolster the demand for phenolic resins in these regions over the forecast period.

- Asia Pacific: Dominant market share and highest growth rate due to robust construction, automotive, and electronics industries in China, India, Japan, and South Korea.

- Europe: Stable growth driven by stringent regulations favoring high-performance and sustainable resins, with significant demand from automotive, construction, and industrial sectors.

- North America: Consistent demand from mature industries like automotive, aerospace, and construction, alongside a growing emphasis on bio-based and advanced material innovation.

- Latin America: Emerging market with growth propelled by infrastructure development, automotive manufacturing, and industrial expansion in Brazil and Mexico.

- Middle East and Africa (MEA): Witnessing increasing demand from construction, oil and gas, and developing manufacturing bases, although starting from a smaller base.

Top Key Players:

The market research report covers the analysis of key stake holders of the Phenolic Resin Market. Some of the leading players profiled in the report include -- Mitsui Chemicals

- Hexion

- DIC Corporation

- Sumitomo Bakelite

- Georgia-Pacific Chemicals

- Chang Chun Group

- Prefere Resins

- SI Group

- Kyowa Kirin

- Shandong Shengquan Chemicals

- ASK Chemicals

- Kolon Industries

- Arclin

- Allnex

- Ashland

- BASF

- Dairen Chemical

- Jinan Shengquan Group

- Capital Resin Corporation

- Red Avenue New Materials Group

Frequently Asked Questions:

What are phenolic resins used for?

Phenolic resins are versatile synthetic polymers primarily used as binders in wood products like plywood and particleboard, and extensively in friction materials for automotive brakes. They are also critical in the construction industry for insulation, in electrical laminates for circuit boards, and as high-temperature resistant components in aerospace and foundry applications.

What drives the phenolic resin market growth?

The phenolic resin market growth is largely driven by increasing demand from the construction sector for fire-retardant insulation and durable building materials, coupled with rising adoption in the automotive industry for lightweight components and friction materials. Growth in the electrical and electronics sector, along with advancements in specialty and bio-based resin formulations, further propels market expansion.

What are the main types of phenolic resins?

The two main types of phenolic resins are Resol and Novolac. Resol resins are thermosetting and self-curing, commonly used in adhesives and laminates. Novolac resins are thermoplastic and require a hardening agent for curing, often utilized in molding compounds, abrasives, and friction materials due to their superior strength and heat resistance.

What are the challenges in the phenolic resin market?

Key challenges in the phenolic resin market include the volatility in raw material prices, particularly phenol and formaldehyde, which impacts production costs. Additionally, stringent environmental regulations concerning formaldehyde emissions necessitate significant investment in compliance and the development of greener alternatives, while competition from other resin types also poses a challenge.

What is the future outlook for the phenolic resin market?

The future outlook for the phenolic resin market is positive, driven by sustained demand from core industries and emerging opportunities. Expected growth is fueled by advancements in bio-based resins, increasing applications in electric vehicles for thermal management, and expanding use in high-performance composites. Strategic investments in research and development for sustainable and enhanced formulations will be key to long-term market expansion.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted