Phenolic Resin for Casting Market

Phenolic Resin for Casting Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708778 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

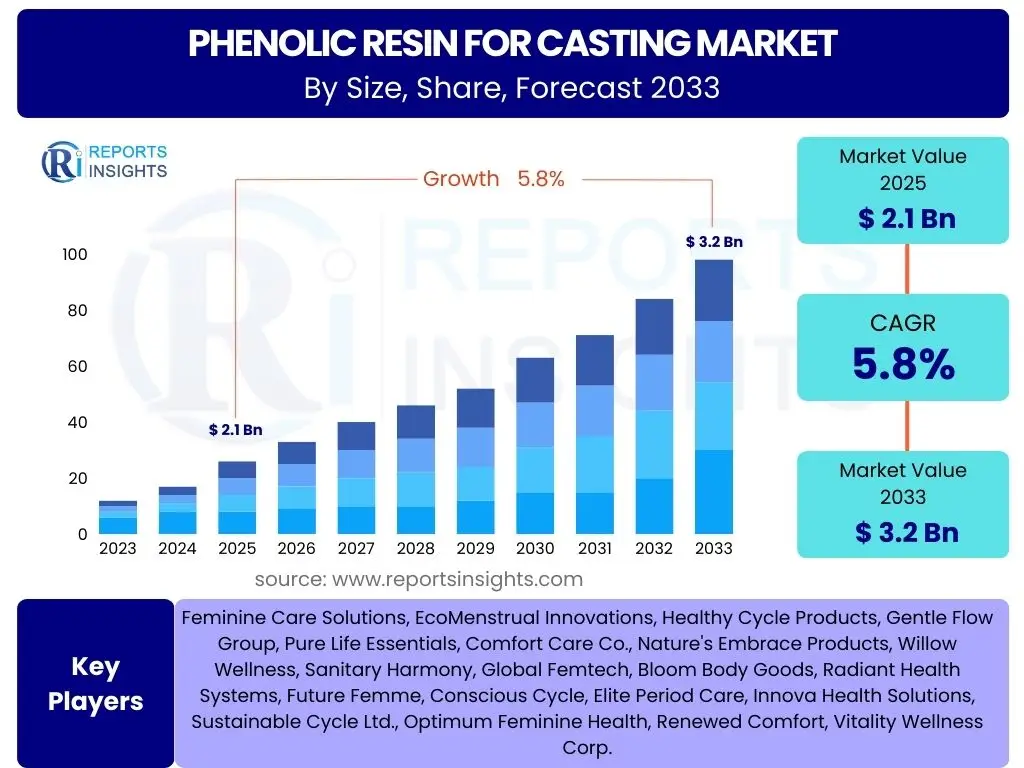

Phenolic Resin for Casting Market Size

According to Reports Insights Consulting Pvt Ltd, The Phenolic Resin for Casting Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 2.1 Billion in 2025 and is projected to reach USD 3.2 Billion by the end of the forecast period in 2033. This growth is primarily driven by the increasing demand from the automotive, construction, and foundry industries, where phenolic resins offer superior performance characteristics essential for high-quality casting processes. The robust expansion in industrialization and urbanization across emerging economies further underpins this market trajectory, creating sustained demand for advanced casting materials.

The market's expansion is also attributable to the continuous innovation in resin formulations, leading to enhanced properties such as improved thermal stability, mechanical strength, and reduced cure times. These advancements address critical needs within demanding applications, making phenolic resins an indispensable component in modern manufacturing. As industries seek more efficient and reliable casting solutions, the unique attributes of phenolic resins position them favorably for continued market penetration and growth, despite potential challenges from volatile raw material prices and environmental regulations.

Key Phenolic Resin for Casting Market Trends & Insights

User queries frequently focus on the evolving landscape of materials science and manufacturing processes within the casting sector. There is significant interest in how sustainability initiatives, technological advancements, and shifts in industrial demand are shaping the phenolic resin market. Users often seek to understand the adoption of eco-friendly alternatives, the integration of automation in foundries, and the impact of lightweighting trends in industries such as automotive and aerospace. Furthermore, the role of specialized resin formulations designed for specific casting techniques, like 3D printing, is a recurring theme, highlighting the market's dynamic nature and its response to broader industrial transformations.

Key insights reveal a strong emphasis on performance optimization and cost efficiency. Manufacturers are increasingly looking for phenolic resin solutions that not only meet stringent quality standards but also contribute to process improvements and waste reduction. The market is witnessing a move towards resins with lower free formaldehyde content, reflecting a growing awareness and regulatory pressure concerning health and environmental impacts. Additionally, the drive for greater energy efficiency in curing processes and the development of resins compatible with various sand types are central to current market innovations. These trends indicate a mature yet adaptable market, continuously striving for innovation while navigating complex operational and environmental requirements.

- Growing adoption of resins with reduced free formaldehyde content due to stricter environmental regulations.

- Increased demand for high-performance resins in automotive and aerospace sectors for lightweight components.

- Development of specialized phenolic resins for additive manufacturing (3D printing) in foundries.

- Focus on improved thermal stability and mechanical strength for demanding casting applications.

- Shifting towards more energy-efficient curing processes to reduce operational costs.

- Integration of advanced automation and digital technologies in foundry operations.

- Expansion of market into emerging economies driven by rapid industrialization and infrastructure development.

AI Impact Analysis on Phenolic Resin for Casting

Common user questions regarding AI's impact on the Phenolic Resin for Casting market frequently revolve around process optimization, material discovery, and supply chain management. Users are keen to understand how artificial intelligence can enhance the efficiency and precision of casting operations, from predicting optimal resin-to-sand ratios to monitoring cure cycles in real-time. There is also significant curiosity about AI's potential in designing novel resin formulations with improved properties, accelerating research and development cycles, and addressing specific performance requirements. Concerns often include the initial investment costs, the need for specialized data infrastructure, and the upskilling of the workforce to leverage AI effectively within traditional manufacturing environments.

The impact of AI in the phenolic resin for casting sector is multifaceted, extending from raw material sourcing to final product quality control. AI-driven predictive analytics can forecast demand fluctuations and optimize inventory levels, mitigating supply chain disruptions and reducing waste. In material science, AI algorithms are being employed to simulate molecular structures and predict material performance, drastically reducing the time and cost associated with traditional experimental methods. This allows for the rapid development of custom phenolic resins tailored for specific casting applications, such as high-temperature resistance or intricate geometries. While challenges exist in data collection and model training, the long-term benefits of AI in boosting productivity, enhancing product quality, and fostering innovation are increasingly recognized and pursued by leading market players.

- Optimizing resin formulation and mixing processes through AI-driven predictive analytics.

- Enhancing quality control and defect detection in casting using machine vision and AI algorithms.

- Predictive maintenance for foundry equipment, reducing downtime and operational costs.

- Accelerating the discovery and development of novel phenolic resin formulations with desired properties.

- Improving supply chain efficiency and demand forecasting for raw materials and finished products.

- Real-time monitoring and control of curing processes for improved consistency and reduced energy consumption.

Key Takeaways Phenolic Resin for Casting Market Size & Forecast

User inquiries concerning the key takeaways from the Phenolic Resin for Casting market size and forecast often focus on understanding the primary growth drivers, the longevity of market expansion, and the factors that could significantly alter the predicted trajectory. There is a strong interest in identifying which applications will experience the most substantial growth and the geographical regions expected to lead this expansion. Furthermore, users frequently seek concise summaries of market resilience against economic headwinds and technological disruptions, highlighting a desire for clear, actionable insights into future market dynamics.

The core takeaways indicate a robust and sustained growth trajectory for the phenolic resin for casting market through 2033, underpinned by consistent demand from foundational industries such as automotive, construction, and heavy machinery. While Asia Pacific is projected to remain the dominant region due to its burgeoning manufacturing sector, technological advancements in resin chemistry and process optimization will be critical determinants of market leadership and competitive advantage globally. The market's resilience will increasingly depend on its ability to adapt to evolving environmental regulations and embrace sustainable practices, alongside managing the volatility of raw material costs effectively. Innovation in specialized applications, particularly those demanding high performance and intricate geometries, will unlock further growth avenues, ensuring phenolic resins maintain their indispensable role in various industrial casting processes.

- The Phenolic Resin for Casting Market is set for consistent growth, projected to reach USD 3.2 Billion by 2033, driven by industrial expansion.

- Automotive and construction industries will remain primary demand generators, benefiting from advanced resin properties.

- Technological advancements in resin formulations and process efficiency are crucial for market competitiveness.

- Sustainability initiatives, including low-formaldehyde resins, are becoming non-negotiable for market players.

- Asia Pacific is expected to lead market expansion, fueled by robust manufacturing and infrastructure development.

- Raw material price fluctuations and environmental regulations represent key areas of strategic focus for market participants.

Phenolic Resin for Casting Market Drivers Analysis

The Phenolic Resin for Casting Market is propelled by several robust drivers rooted in industrial growth and technological advancements. The increasing demand for lightweight and high-performance components in the automotive sector, driven by stricter fuel efficiency standards and the rise of electric vehicles, directly fuels the need for advanced casting materials like phenolic resins. These resins offer superior strength-to-weight ratios and thermal stability, which are critical for engine blocks, brake components, and other vital automotive parts. Furthermore, the global expansion of infrastructure projects and the construction industry necessitates durable and reliable casting solutions for pipes, fittings, and structural elements, where phenolic resins play a pivotal role due to their excellent mechanical properties and resistance to harsh environments.

Beyond traditional sectors, the proliferation of complex machinery and equipment in various manufacturing industries, including heavy machinery and agricultural equipment, contributes significantly to market growth. These applications often require precision castings capable of withstanding extreme operational conditions, making phenolic resins an ideal choice. Continuous innovation in foundry technologies, such as the adoption of advanced molding and core-making processes that leverage the fast-curing and high-strength attributes of phenolic resins, further stimulates demand. The economic development and rapid industrialization in emerging economies, particularly across Asia Pacific, are creating new manufacturing hubs and increasing the overall consumption of casting products, thereby bolstering the phenolic resin market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand from Automotive Industry | +1.5% | Global, particularly APAC, Europe, North America | Short to Long-term |

| Growth in Construction and Infrastructure Development | +1.2% | APAC, Latin America, Middle East & Africa | Medium to Long-term |

| Advancements in Foundry Technology and Processes | +0.9% | Global | Medium-term |

| Rising Demand for High-Performance Industrial Castings | +0.8% | Global | Short to Long-term |

| Rapid Industrialization in Emerging Economies | +1.0% | China, India, Southeast Asia, Brazil | Long-term |

Phenolic Resin for Casting Market Restraints Analysis

Despite robust growth drivers, the Phenolic Resin for Casting Market faces several significant restraints that could impede its expansion. One primary concern is the volatility of raw material prices, particularly for phenol and formaldehyde, which are key precursors for phenolic resins. Fluctuations in crude oil prices and petrochemical supply chains directly impact production costs, subsequently affecting the final price of phenolic resins and potentially squeezing profit margins for manufacturers. This unpredictability can make long-term planning and investment challenging for market players, leading to cautious expansion strategies and potentially slowing innovation.

Another substantial restraint comes from stringent environmental regulations concerning emissions and the use of hazardous chemicals. Governments worldwide are increasingly imposing stricter limits on formaldehyde emissions from resin production and application, prompting manufacturers to invest in costly research and development for low-formaldehyde or formaldehyde-free alternatives. Compliance with these evolving regulations can significantly increase operational expenses and manufacturing complexities, especially for smaller market participants. Furthermore, the emergence of alternative materials and casting technologies, though currently limited in scope, poses a long-term threat as industries explore substitutes offering comparable performance with potentially lower environmental footprints or reduced costs. Economic slowdowns and geopolitical uncertainties can also dampen industrial output, leading to reduced demand for casting products and, consequently, phenolic resins.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Raw Material Prices (Phenol, Formaldehyde) | -1.3% | Global | Short to Medium-term |

| Stringent Environmental Regulations and Emission Standards | -1.0% | Europe, North America, APAC | Medium to Long-term |

| Competition from Alternative Casting Materials/Technologies | -0.7% | Global | Long-term |

| High Energy Consumption in Manufacturing Processes | -0.5% | Global | Medium-term |

| Economic Slowdowns and Geopolitical Instability | -0.9% | Specific Regions (e.g., Europe, parts of Asia) | Short-term |

Phenolic Resin for Casting Market Opportunities Analysis

The Phenolic Resin for Casting Market presents several compelling opportunities for growth and innovation. One significant area is the increasing adoption of sustainable and green casting technologies. With growing environmental consciousness and regulatory pressures, there is a rising demand for bio-based phenolic resins or those with significantly reduced environmental impact, such as lower VOC emissions and minimized hazardous substance content. Companies investing in research and development for these eco-friendly formulations can gain a substantial competitive advantage and tap into new market segments driven by corporate sustainability initiatives and consumer preferences. This shift provides an avenue for differentiation and caters to a market that is increasingly valuing environmental responsibility.

Another major opportunity lies in the burgeoning field of additive manufacturing (3D printing) for foundry applications. Phenolic resins, particularly in their liquid or powder forms, can be optimized for use in sand casting 3D printers, enabling the rapid production of complex core and mold designs with unparalleled precision and reduced lead times. This technology is revolutionizing prototyping and small-batch production, opening up entirely new markets for specialized phenolic resin formulations. Furthermore, the continuous expansion of application areas into specialized industries like aerospace, defense, and medical devices, where lightweight, high-strength, and thermally stable components are crucial, offers premium market segments. Strategic partnerships with technology providers and end-users to co-develop tailored resin solutions for these high-value applications can unlock significant revenue streams and drive advanced product development. The growth of specialized, high-performance applications demanding intricate geometries and superior material properties also creates unique niches for advanced phenolic resin solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Sustainable and Bio-based Resins | +1.4% | Europe, North America, Global | Medium to Long-term |

| Application in Additive Manufacturing (3D Printing) for Foundries | +1.1% | Global, particularly advanced manufacturing hubs | Medium to Long-term |

| Expansion into Niche, High-Performance Applications | +0.9% | Global (Aerospace, Defense, Medical) | Long-term |

| Technological Innovation in Resin Curing and Processing | +0.8% | Global | Short to Medium-term |

| Untapped Potential in Emerging Markets with Growing Foundries | +1.0% | Africa, Southeast Asia | Long-term |

Phenolic Resin for Casting Market Challenges Impact Analysis

The Phenolic Resin for Casting Market is not immune to various challenges that can hinder its growth and profitability. A significant challenge lies in managing the complex and often fragmented global supply chain for raw materials. Geopolitical tensions, trade disputes, and natural disasters can disrupt the availability and increase the cost of critical inputs like phenol and formaldehyde, leading to production delays and increased operational expenditures. Ensuring a resilient and diversified supply chain requires substantial strategic planning and investment, which can be particularly challenging for companies with limited resources.

Another prevalent challenge is the need for highly skilled labor in foundry operations and resin application. The precision required for mixing, molding, and curing phenolic resins demands experienced personnel, and a global shortage of such skilled workers can limit production capacity and increase labor costs. Attracting and retaining talent, as well as investing in training and development programs, represents a considerable ongoing challenge for the industry. Furthermore, maintaining consistent product quality across different batches and applications is critical but difficult, given the variability in raw materials and process conditions. Any deviation in quality can lead to casting defects, increased scrap rates, and reputational damage. The industry also faces the challenge of adapting quickly to evolving customer demands for specialized properties, which often requires significant R&D investment and a flexible manufacturing infrastructure, sometimes in the face of long development cycles and high capital costs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions and Raw Material Scarcity | -1.1% | Global | Short to Medium-term |

| Shortage of Skilled Labor in Foundry Operations | -0.8% | North America, Europe, parts of APAC | Medium to Long-term |

| Maintaining Consistent Product Quality and Performance | -0.6% | Global | Ongoing |

| High Capital Investment for New Technologies and Compliance | -0.7% | Global | Long-term |

| Intensifying Regulatory Scrutiny on Chemical Safety | -0.9% | Europe, North America, China | Medium to Long-term |

Phenolic Resin for Casting Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Phenolic Resin for Casting Market, offering valuable insights into its size, growth trajectory, key trends, and future outlook from 2025 to 2033. It meticulously examines market dynamics, including drivers, restraints, opportunities, and challenges that shape the competitive landscape. The scope encompasses detailed segmentation analysis by resin type, application, and end-use industry, alongside a thorough regional assessment to identify prominent growth pockets. Furthermore, the report profiles leading market players, offering strategic intelligence on their market positions, product portfolios, and recent developments, all aimed at equipping stakeholders with robust data for informed decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.1 Billion |

| Market Forecast in 2033 | USD 3.2 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Hitachi Chemical Company Ltd., Hexion Inc., Sumitomo Bakelite Co. Ltd., DIC Corporation, Ashland Global Holdings Inc., Georgia-Pacific Chemicals LLC, SI Group, Inc., Prefere Resins, Sprea S.p.A., D.R. Biochem Co., Ltd., Shanghai Plastics Co., Ltd., Jinan Shengquan Group Share-Holding Co., Ltd., Shandong Laiwu Runda Chemical Co., Ltd., Changzhou HuaRi Chemical Co., Ltd., Kyoeisha Chemical Co., Ltd., Plenco, Polynt S.p.A., Mitsui Chemicals Inc., Borden Chemical Inc., Formosa Plastics Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Phenolic Resin for Casting Market is meticulously segmented to provide a granular understanding of its diverse components and their individual contributions to overall market dynamics. This segmentation helps identify key revenue streams, emerging niches, and areas with high growth potential, allowing stakeholders to formulate targeted strategies. The market is primarily categorized by resin type, application, and end-use industry, reflecting the varied requirements and utilization patterns of phenolic resins across different industrial landscapes. Each segment exhibits unique characteristics and growth drivers, influencing the demand-supply balance and competitive strategies within the market.

Analyzing these segments offers critical insights into the evolving preferences of end-users and the technological advancements shaping specific application areas. For instance, the distinction between Novolac and Resol phenolic resins highlights differences in their curing mechanisms and suitability for various casting processes, directly impacting their market share. Similarly, examining applications like sand casting versus shell molding reveals the predominant technologies in use and where innovation is most impactful. Furthermore, breaking down the market by end-use industries, such as automotive or industrial machinery, provides a clear picture of the sectors driving demand and their specific material requirements, which is essential for product development and market positioning. This multi-dimensional segmentation ensures a comprehensive market overview, critical for strategic planning and investment decisions.

- By Type:

- Novolac Phenolic Resin: Characterized by requiring a hardener (e.g., hexamethylenetetramine) for cross-linking, Novolac resins offer superior heat resistance, dimensional stability, and mechanical strength, making them ideal for demanding foundry applications such as shell molding and hot-box core making. Their versatility and excellent binding properties contribute significantly to high-quality casting production, particularly in the automotive and heavy machinery sectors.

- Resol Phenolic Resin: These resins are self-curing under heat or with acidic catalysts and are widely used in no-bake and cold-box casting processes. Resol resins are valued for their fast curing times, excellent flow properties, and high strength, enabling efficient and precise mold and core production. They are extensively utilized in foundries seeking to optimize production cycles and reduce energy consumption, especially in the production of complex and intricate cast parts.

- By Application:

- Sand Casting: The most traditional and widely used casting process, where phenolic resins serve as binders for sand molds and cores. Their strength, thermal stability, and low gas evolution are critical for producing high-quality metal castings.

- Shell Molding: A high-precision casting process utilizing phenolic resin-coated sand to create thin, strong, and dimensionally accurate molds. Phenolic resins are essential for the integrity and fine finish achieved in shell molding, particularly for intricate components.

- Investment Casting: Although less prevalent, phenolic resins can be used in specific stages, such as for the binder in ceramic shell molds for precision casting, offering excellent dimensional accuracy and surface finish for complex parts.

- Others (Die Casting, Permanent Mold Casting): While primary binders in these processes are different, phenolic resins may be used in specific auxiliary applications or in hybrid processes for their unique properties.

- By End-Use Industry:

- Automotive: A dominant end-user, demanding phenolic resins for casting engine blocks, cylinder heads, brake drums, and other critical components where high strength, wear resistance, and thermal stability are paramount. The shift towards lightweighting also drives demand for specialized resins.

- Construction: Utilizes phenolic resins for casting components in heavy construction equipment, structural elements, pipes, and fittings, requiring durability, strength, and resistance to environmental factors.

- Industrial Machinery: Encompasses a broad range of equipment from agricultural machinery to general manufacturing tools, all relying on cast parts for robust performance. Phenolic resins ensure the production of reliable and durable components.

- Aerospace & Defense: A niche but high-value segment requiring castings with exceptional strength-to-weight ratios and thermal resistance for aircraft engines, structural parts, and defense equipment, pushing demand for advanced phenolic resin formulations.

- Energy: Includes components for power generation (turbines, generators) and oil & gas equipment, where castings must withstand extreme temperatures and pressures, making phenolic resins crucial for their production.

- Others (Marine, Medical): Diverse applications where specialized castings are needed, such as marine engine components, intricate medical device parts, or specialized tooling, leveraging the unique properties of phenolic resins.

Regional Highlights

- North America: The North American market for phenolic resin in casting is characterized by advanced foundry technologies and a strong emphasis on high-performance applications, particularly in the automotive, aerospace, and industrial machinery sectors. The region's focus on innovation and stringent quality standards drives the demand for premium phenolic resin formulations. While manufacturing output can fluctuate, a consistent need for durable and precision-cast components ensures a stable market. Environmental regulations are also a significant factor, pushing manufacturers towards low-emission and sustainable resin solutions. Investment in research and development remains high, aiming to optimize casting processes and introduce novel material properties. The region is seeing a gradual shift towards automation in foundries, which further supports the adoption of high-efficiency phenolic resins.

- Europe: Europe represents a mature but technologically advanced market for phenolic resins in casting, with a strong presence of automotive, industrial, and specialized machinery manufacturing. Strict environmental regulations, particularly regarding formaldehyde emissions and worker safety, are a major driver for the development and adoption of low-free-formaldehyde and greener phenolic resin systems. European foundries prioritize efficiency, quality, and sustainability, leading to consistent demand for high-performance and eco-friendly resin solutions. The region also benefits from robust R&D activities focused on enhancing resin properties for demanding applications and optimizing casting processes to meet precise engineering specifications. Economic stability and industrial heritage contribute to a steady, albeit slower, growth rate compared to emerging markets.

- Asia Pacific (APAC): The Asia Pacific region stands as the largest and fastest-growing market for phenolic resin in casting, primarily driven by rapid industrialization, burgeoning manufacturing sectors, and significant infrastructure development in countries like China, India, Japan, and South Korea. The automotive and construction industries are experiencing exponential growth, fueling a substantial demand for cast components and, consequently, phenolic resins. Lower manufacturing costs and abundant raw material availability contribute to the region's competitive advantage. While environmental regulations are becoming stricter, especially in China, the sheer volume of industrial output ensures sustained market expansion. The region is also a hub for foundry technology adoption and expansion, attracting significant investment from global players.

- Latin America: The Latin American market for phenolic resins in casting is characterized by steady growth, influenced by the automotive, construction, and agricultural machinery sectors, particularly in Brazil and Mexico. Economic developments and increasing foreign investment in manufacturing facilities are contributing to the demand for casting materials. While still developing compared to APAC or North America, there is a growing emphasis on modernizing foundry operations and adopting more efficient casting techniques. The market is sensitive to economic fluctuations and political stability, but the underlying industrial growth provides a solid foundation for phenolic resin consumption. Local production capacities are increasing, aiming to reduce reliance on imports and stabilize supply chains.

- Middle East and Africa (MEA): The MEA region exhibits emerging potential for phenolic resins in casting, primarily driven by investments in oil and gas infrastructure, construction, and nascent automotive manufacturing. Countries like Saudi Arabia, UAE, and South Africa are leading the industrialization efforts, creating a growing need for durable and high-performance cast components. The market is in its early stages of development but benefits from significant government spending on diversification of economies away from oil. Challenges include limited local manufacturing capabilities and reliance on imports, but the long-term outlook is positive with planned industrial growth and increasing demand for localized production of components.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Phenolic Resin for Casting Market.- Hitachi Chemical Company Ltd.

- Hexion Inc.

- Sumitomo Bakelite Co. Ltd.

- DIC Corporation

- Ashland Global Holdings Inc.

- Georgia-Pacific Chemicals LLC

- SI Group, Inc.

- Prefere Resins

- Sprea S.p.A.

- D.R. Biochem Co., Ltd.

- Shanghai Plastics Co., Ltd.

- Jinan Shengquan Group Share-Holding Co., Ltd.

- Shandong Laiwu Runda Chemical Co., Ltd.

- Changzhou HuaRi Chemical Co., Ltd.

- Kyoeisha Chemical Co., Ltd.

- Plenco

- Polynt S.p.A.

- Mitsui Chemicals Inc.

- Borden Chemical Inc.

- Formosa Plastics Corporation

Frequently Asked Questions

What is phenolic resin used for in casting?

Phenolic resins are primarily used as binders in foundry sand for making molds and cores in various casting processes, including sand casting, shell molding, and some precision casting applications. They provide high strength, thermal stability, excellent dimensional accuracy, and good resistance to high temperatures, making them essential for producing high-quality metal castings for industries like automotive, construction, and industrial machinery.

What is the current market size and forecast for phenolic resin in casting?

The Phenolic Resin for Casting Market is estimated at USD 2.1 Billion in 2025 and is projected to reach USD 3.2 Billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. This growth is driven by increasing demand from key end-use industries and ongoing advancements in casting technologies.

What are the main types of phenolic resins used in casting?

The two main types are Novolac phenolic resins and Resol phenolic resins. Novolac resins require a hardener (e.g., hexamine) for curing and are known for excellent heat resistance and strength in applications like shell molding. Resol resins are self-curing under heat or with acid catalysts, offering fast cure times and high strength for no-bake and cold-box processes.

Which region dominates the phenolic resin for casting market?

The Asia Pacific (APAC) region currently dominates the phenolic resin for casting market. This dominance is attributed to rapid industrialization, substantial growth in the automotive and construction sectors, and the expansion of manufacturing capabilities in countries such as China, India, and Southeast Asian nations.

What are the key trends influencing the phenolic resin for casting market?

Key trends include the growing demand for low-formaldehyde and sustainable resin formulations, increased adoption in high-performance applications (like lightweight automotive components), the integration of phenolic resins in additive manufacturing for foundry tooling, and the broader shift towards automation and efficiency in casting operations.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted