Pesticide intermediate Market

Pesticide intermediate Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707653 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

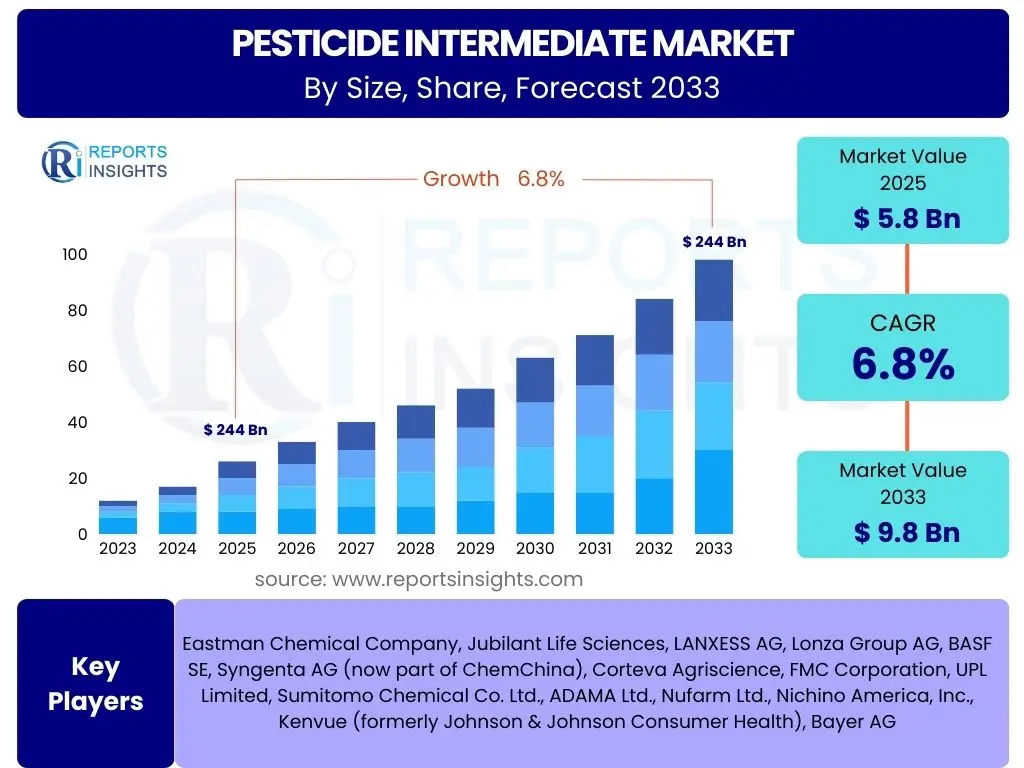

Pesticide intermediate Market Size

According to Reports Insights Consulting Pvt Ltd, The Pesticide intermediate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 5.8 Billion in 2025 and is projected to reach USD 9.8 Billion by the end of the forecast period in 2033.

Key Pesticide intermediate Market Trends & Insights

User inquiries frequently focus on the evolving landscape of the pesticide intermediate market, seeking to understand the significant forces shaping its trajectory. Common themes include the shift towards sustainable agricultural practices, the increasing demand for specialized and high-efficiency crop protection chemicals, and the impact of evolving regulatory frameworks. Stakeholders are keen to identify how these trends influence investment decisions, research and development priorities, and supply chain dynamics, particularly in key agricultural regions.

Further analysis of market sentiment reveals a strong interest in technological advancements within chemical synthesis and formulation, aiming for reduced environmental impact and enhanced efficacy. The global imperative for food security, coupled with growing pest resistance, continues to drive innovation in novel active ingredients and their precursors. This drives demand for intermediates that enable the production of advanced, targeted, and environmentally benign pesticide formulations. Understanding these underlying currents is crucial for strategic positioning and future growth in the sector.

- Shift towards bio-based and green chemistries in intermediate production.

- Increasing focus on high-performance and specialty intermediates for targeted pesticides.

- Digitalization and automation in manufacturing processes to enhance efficiency and quality.

- Growing demand for pesticide intermediates from emerging economies due to agricultural expansion.

- Consolidation among market players to leverage economies of scale and expand product portfolios.

AI Impact Analysis on Pesticide intermediate

User queries regarding the influence of Artificial intelligence (AI) on the pesticide intermediate sector primarily revolve around its potential to revolutionize discovery, development, and manufacturing processes. There is significant interest in how AI can accelerate the identification of novel chemical structures, optimize synthesis pathways for higher yields and purity, and predict molecular properties, thereby reducing the time and cost associated with traditional R&D. Concerns also include the practical implementation challenges and the need for specialized data infrastructure.

Furthermore, stakeholders are exploring AI's role in enhancing operational efficiencies, such as predictive maintenance in manufacturing plants, optimizing supply chain logistics for raw materials, and improving quality control through advanced analytics. AI-driven insights could lead to more sustainable production methods by minimizing waste and energy consumption. The application of AI in precision agriculture also has a downstream effect, driving demand for specific, highly effective intermediates that can be deployed with greater accuracy and efficiency, ultimately shaping future product portfolios.

- Accelerated discovery and design of novel pesticide intermediates through AI-driven molecular modeling.

- Optimization of chemical synthesis routes using AI algorithms for improved yield and reduced waste.

- Enhanced quality control and process automation in manufacturing facilities through AI and machine learning.

- Predictive analytics for supply chain management, optimizing inventory and logistics of raw materials and intermediates.

- Development of smart farming solutions driving demand for highly specific and potent pesticide intermediates.

Key Takeaways Pesticide intermediate Market Size & Forecast

Common user questions regarding the key takeaways from the pesticide intermediate market size and forecast highlight a strong desire to understand the market's fundamental drivers and long-term viability. Users are keen to identify the most impactful factors contributing to market expansion, such as global agricultural demands, technological advancements in crop protection, and shifts in regulatory landscapes. The primary insights sought revolve around strategic opportunities, potential threats, and the overall attractiveness of investing in this crucial segment of the agrochemical industry.

The market's resilience, despite regulatory pressures and sustainability mandates, underscores its essential role in maintaining global food security. A key takeaway is the sustained growth propelled by the continuous need for effective pest management solutions, which directly translates into steady demand for diverse intermediates. Furthermore, the forecast indicates a significant shift towards environmentally friendlier and more specialized intermediates, signaling a lucrative avenue for innovation and product differentiation among market participants. This evolution positions the market for continued expansion, driven by both volume and value growth in niche applications.

- The market is poised for robust growth, driven by increasing global food demand and agricultural intensification.

- Sustainable and bio-based pesticide intermediates represent a significant and growing segment.

- Regulatory policies, while challenging, are also fostering innovation in safer and more efficient intermediates.

- Asia Pacific is expected to remain the dominant and fastest-growing region due to agricultural expansion.

- Strategic partnerships and R&D investments in novel chemistries are crucial for market leadership.

Pesticide intermediate Market Drivers Analysis

The global pesticide intermediate market is primarily propelled by the escalating demand for food production worldwide, driven by a burgeoning global population. As arable land diminishes and climate change intensifies pest challenges, the necessity for effective crop protection solutions becomes paramount. This sustained demand for pesticides, in turn, directly fuels the need for their essential building blocks, the intermediates. Innovations in agricultural practices, such as intensive farming and precision agriculture, further necessitate the development of more advanced and targeted crop protection chemicals, thereby increasing the market for specialized intermediates.

Moreover, the increasing prevalence of pest resistance to existing pesticide formulations necessitates continuous research and development into novel active ingredients and chemistries. This R&D cycle creates a constant pipeline for new and diverse intermediates. Government initiatives and support for agricultural development, particularly in emerging economies, also play a significant role by promoting the adoption of modern farming techniques and crop protection products, consequently stimulating the demand for intermediates. The economic viability of agriculture in many regions heavily relies on robust pest management, solidifying the market's foundational drivers.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Food Demand | +1.5% | Global, particularly Asia Pacific, Latin America | Long-term (2025-2033) |

| Rising Pest Resistance and Crop Loss | +1.2% | Global, particularly North America, Europe | Mid-term (2027-2033) |

| Advancements in Agricultural Practices | +1.0% | North America, Europe, select APAC countries | Mid-term (2026-2030) |

| Growth in Bio-Pesticide Development | +0.8% | Europe, North America, India | Long-term (2028-2033) |

| Government Support & Subsidies for Agriculture | +0.7% | Emerging Economies (e.g., India, Brazil, China) | Short-term to Mid-term (2025-2029) |

Pesticide intermediate Market Restraints Analysis

The pesticide intermediate market faces significant headwinds from increasingly stringent environmental regulations and public concerns regarding the ecological impact of chemical use. Governments globally are imposing stricter limits on the use of certain chemicals, requiring more rigorous testing and approval processes, and in some cases, outright bans on specific active ingredients. These regulations directly impact the demand for the corresponding intermediates, compelling manufacturers to invest heavily in developing cleaner, safer alternatives, which often entails substantial research and development costs and longer time-to-market.

Another prominent restraint is the fluctuating cost and availability of raw materials. The production of many pesticide intermediates relies on petrochemical derivatives, whose prices are subject to global crude oil market volatility. Supply chain disruptions, geopolitical tensions, and trade barriers can also severely impact the steady supply of these critical raw materials, leading to increased production costs and potential delays. Furthermore, the growing consumer preference for organic and residue-free food products in developed markets poses a long-term challenge, as it shifts agricultural practices away from synthetic pesticides, thereby tempering the demand for conventional intermediates.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict Environmental Regulations & Bans | -1.3% | Europe, North America | Ongoing, Long-term |

| Volatile Raw Material Prices | -0.9% | Global, particularly Asia Pacific (for sourcing) | Short-term to Mid-term (2025-2029) |

| High R&D Costs & Long Approval Cycles | -0.7% | Global | Long-term (2025-2033) |

| Growing Consumer Preference for Organic Products | -0.5% | Europe, North America | Mid-term to Long-term (2027-2033) |

| Intellectual Property Infringement & Counterfeiting | -0.4% | Emerging Economies | Ongoing |

Pesticide intermediate Market Opportunities Analysis

The pesticide intermediate market is presented with significant opportunities through the accelerating trend of developing bio-based and eco-friendly pesticides. As regulatory scrutiny intensifies and consumer preferences shift towards sustainable agricultural practices, there is a burgeoning demand for intermediates derived from renewable resources or those enabling the production of biodegradable and less toxic active ingredients. Companies that can innovate and scale up the production of these green intermediates are poised to capture a substantial share of future market growth, distinguishing themselves in an increasingly environmentally conscious industry.

Furthermore, the expansion of precision agriculture and integrated pest management (IPM) techniques opens new avenues for specialized pesticide intermediates. These advanced farming methods require highly targeted and efficient crop protection solutions, leading to increased demand for intermediates that can produce highly specific, low-dose, and effective pesticides. Emerging economies, particularly in Asia Pacific and Latin America, offer immense untapped potential due to their vast agricultural lands, increasing adoption of modern farming technologies, and rising focus on improving crop yields. Strategic investments and market entry strategies tailored to these regions can unlock considerable growth for intermediate manufacturers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bio-based & Green Intermediates | +1.8% | Global, particularly Europe, North America | Long-term (2027-2033) |

| Expansion in Emerging Agricultural Markets | +1.5% | Asia Pacific, Latin America, Africa | Mid-term to Long-term (2026-2033) |

| Increasing Adoption of Precision Agriculture | +1.2% | North America, Europe, Australia | Mid-term (2026-2030) |

| Focus on Specialty & High-Value Intermediates | +1.0% | Global | Mid-term (2027-2033) |

| Strategic Collaborations & Partnerships | +0.6% | Global | Short-term to Mid-term (2025-2029) |

Pesticide intermediate Market Challenges Impact Analysis

The pesticide intermediate market faces substantial challenges stemming from complex and evolving global regulatory landscapes. Divergent chemical registration requirements across different countries and regions create significant hurdles for market entry and product commercialization. Compliance with these stringent and often changing regulations demands extensive resources for testing, documentation, and continuous monitoring, which can delay product launches and increase operational costs. The risk of sudden bans on key active ingredients or their intermediates further adds to market uncertainty and necessitates agile R&D strategies.

Another critical challenge is the intense competition from generic manufacturers, particularly in markets where patents for established active ingredients are expiring or have already expired. This proliferation of generic alternatives drives down prices for both the final pesticides and their intermediates, exerting downward pressure on profit margins for innovators. Furthermore, maintaining intellectual property rights and combating counterfeiting, especially in emerging markets, remains a persistent battle. Supply chain disruptions, triggered by geopolitical events, natural disasters, or pandemics, also pose a significant threat by disrupting raw material flows and finished product distribution, thereby impacting production schedules and market supply.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Regulatory Complexities & Compliance | -1.5% | Global, especially EU, US, China | Ongoing, Long-term |

| Competition from Generic Manufacturers | -1.0% | Global | Ongoing |

| Supply Chain Vulnerabilities & Disruptions | -0.8% | Global | Short-term to Mid-term (2025-2028) |

| Public Perception & Activist Pressure | -0.6% | Europe, North America | Ongoing |

| Waste Management & Environmental Liabilities | -0.5% | Global | Long-term (2027-2033) |

Pesticide intermediate Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global pesticide intermediate market, covering historical performance, current market dynamics, and future growth projections. It offers a detailed examination of market size, trends, drivers, restraints, opportunities, and challenges affecting the industry. The report also includes extensive segmentation analysis by various categories, comprehensive regional insights, and profiles of key industry players, offering strategic intelligence for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.8 Billion |

| Market Forecast in 2033 | USD 9.8 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Eastman Chemical Company, Jubilant Life Sciences, LANXESS AG, Lonza Group AG, BASF SE, Syngenta AG (now part of ChemChina), Corteva Agriscience, FMC Corporation, UPL Limited, Sumitomo Chemical Co. Ltd., ADAMA Ltd., Nufarm Ltd., Nichino America, Inc., Kenvue (formerly Johnson & Johnson Consumer Health), Bayer AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global pesticide intermediate market is comprehensively segmented to provide a granular understanding of its diverse components and drivers. This detailed segmentation allows for a precise analysis of specific product types, applications, end-use industries, and forms, highlighting the areas of highest growth potential and market concentration. Understanding these distinct segments is crucial for stakeholders to identify niche markets, tailor product development, and formulate targeted marketing and sales strategies, optimizing resource allocation and maximizing returns.

- By Type: This segment categorizes intermediates based on the chemical class of the final pesticide they produce.

- Organophosphorus Intermediates: Precursors for organophosphate pesticides.

- Pyrethroid Intermediates: Used in the synthesis of pyrethroid insecticides.

- Triazine Intermediates: Essential for triazine herbicides.

- Urea Derivatives: Used in various herbicide and fungicide formulations.

- Other Chemical Intermediates: Encompassing precursors for carbamates, neonicotinoids, and other novel chemistries.

- By Application: This segment focuses on the type of pesticide the intermediate is used to manufacture.

- Herbicides: Intermediates for weed control chemicals.

- Insecticides: Precursors for insect control agents.

- Fungicides: Used in the production of disease control agents.

- Rodenticides: Intermediates for rodent control chemicals.

- Other Crop Protection Chemicals: Includes growth regulators and desiccants.

- By End-Use Industry: This segment identifies the primary sectors consuming pesticides.

- Agriculture: Dominant segment, includes farming and crop production.

- Public Health: For vector control and public sanitation.

- Commercial & Industrial: For pest control in commercial establishments and industrial sites.

- Home & Garden: For domestic pest control and gardening applications.

- By Form: This segment classifies intermediates based on their physical state.

- Liquid: Liquid-form intermediates, often for ease of handling and reaction.

- Powder: Solid, powdered intermediates.

- Granular: Granular forms of intermediates, less common but used for specific applications.

Regional Highlights

- North America: A mature market characterized by advanced agricultural practices and a strong emphasis on R&D for specialty and high-value intermediates. Stringent regulatory frameworks drive innovation towards safer and more sustainable chemistries. The region's focus on precision agriculture and integrated pest management boosts demand for sophisticated intermediate compounds.

- Europe: Known for its rigorous regulatory environment and strong push towards green chemistry and sustainable agriculture. This region is a leader in developing and adopting bio-based intermediates and highly specific pesticide formulations. Investment in eco-friendly alternatives and reduced chemical residues significantly influences market trends.

- Asia Pacific (APAC): The largest and fastest-growing market, primarily driven by the enormous agricultural sector in countries like China, India, and Southeast Asia. Increasing population, rising food demand, and the adoption of modern farming techniques are fueling substantial growth in pesticide consumption and, consequently, intermediate demand. Lower manufacturing costs also attract significant investment.

- Latin America: A significant agricultural powerhouse, particularly in countries like Brazil and Argentina, with vast expanses of arable land and high crop production. The region exhibits robust growth in pesticide intermediate demand due to expanding cultivation areas, increasing pest resistance, and a growing focus on improving agricultural productivity.

- Middle East and Africa (MEA): An emerging market with considerable untapped potential. Growth is stimulated by government initiatives to enhance food security, diversify economies, and modernize agricultural practices. While smaller in scale currently, increasing investment in farming infrastructure and adoption of crop protection solutions are expected to drive steady growth in intermediate demand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Pesticide intermediate Market.- Eastman Chemical Company

- Jubilant Life Sciences

- LANXESS AG

- Lonza Group AG

- BASF SE

- Syngenta AG (now part of ChemChina)

- Corteva Agriscience

- FMC Corporation

- UPL Limited

- Sumitomo Chemical Co. Ltd.

- ADAMA Ltd.

- Nufarm Ltd.

- Nichino America, Inc.

- Kenvue (formerly Johnson & Johnson Consumer Health)

- Bayer AG

- Dow Chemical Company

- Huntsman Corporation

- Ashland Global Holdings Inc.

- Evonik Industries AG

- Croda International Plc

Frequently Asked Questions

What is a pesticide intermediate?

A pesticide intermediate is a chemical compound used as a raw material or precursor in the synthesis of active ingredients for various pesticide formulations. These intermediates are crucial building blocks that undergo further chemical reactions to produce the final pesticide products, such as herbicides, insecticides, or fungicides.

What are the primary drivers of the Pesticide intermediate Market?

The key drivers for the pesticide intermediate market include the increasing global demand for food due to population growth, the rising incidence of pest resistance necessitating new chemical solutions, advancements in agricultural practices requiring more sophisticated crop protection, and supportive government policies for agricultural development in various regions.

Which region dominates the Pesticide intermediate Market?

The Asia Pacific (APAC) region currently dominates the pesticide intermediate market and is projected to exhibit the fastest growth. This dominance is primarily driven by extensive agricultural activities in countries like China and India, coupled with increasing investments in modern farming technologies and a large agricultural land base.

What impact do regulations have on the Pesticide intermediate Market?

Regulations significantly influence the pesticide intermediate market by imposing stringent environmental and safety standards, which can lead to the banning of certain chemicals or increased R&D costs for compliance. While posing challenges, these regulations also spur innovation towards safer, more sustainable, and eco-friendlier intermediates, fostering long-term market evolution.

What are the key opportunities in the Pesticide intermediate Market?

Key opportunities in the pesticide intermediate market include the growing demand for bio-based and green chemistries, expansion into emerging agricultural markets, increasing adoption of precision agriculture techniques requiring specialized intermediates, and the potential for strategic collaborations to develop novel and more efficient chemical compounds.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted