Personal Loan Market

Personal Loan Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708404 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

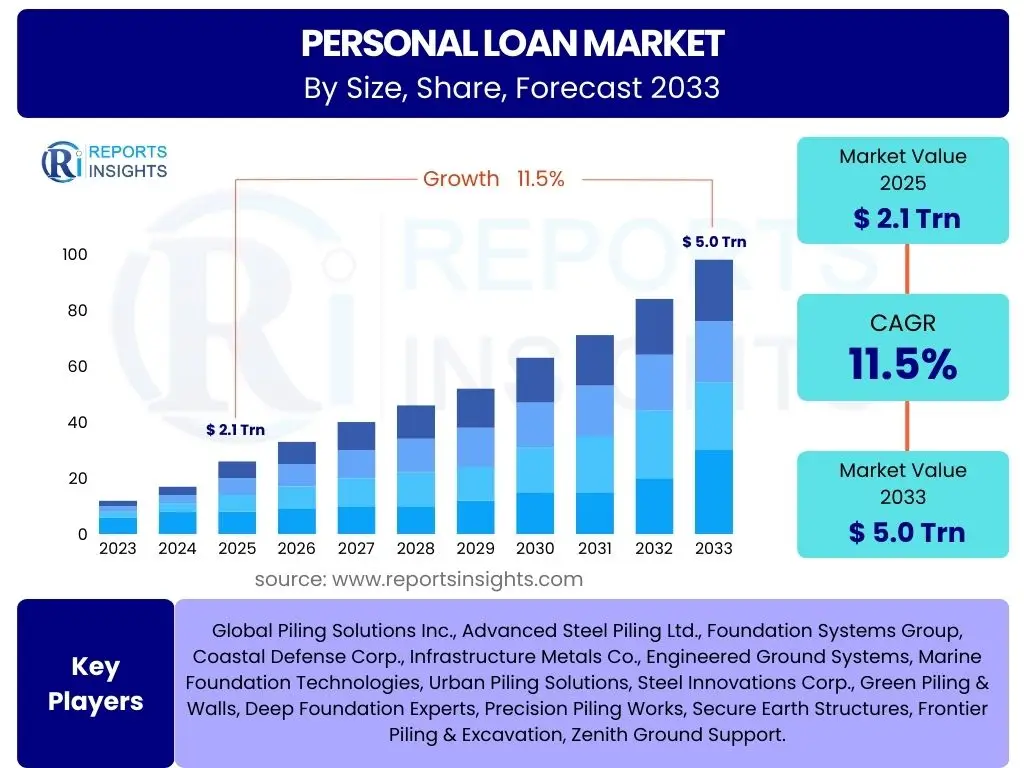

Personal Loan Market Size

According to Reports Insights Consulting Pvt Ltd, The Personal Loan Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2025 and 2033. The market is estimated at USD 2.1 trillion in 2025 and is projected to reach USD 5.0 trillion by the end of the forecast period in 2033.

Key Personal Loan Market Trends & Insights

The personal loan market is currently experiencing significant transformation driven by several key factors. Consumers are increasingly seeking flexible and immediate access to credit, spurred by the convenience offered by digital platforms and fintech innovations. This shift has led to a greater demand for personalized loan products tailored to individual financial needs and credit profiles. Furthermore, evolving regulatory landscapes in various regions are influencing lending practices, pushing for greater transparency and consumer protection while simultaneously adapting to new digital lending models. The macroeconomic environment, including interest rate fluctuations and inflation, also plays a crucial role in shaping consumer borrowing behavior and lender strategies.

Technological advancements, particularly in data analytics and artificial intelligence, are enabling lenders to assess creditworthiness more accurately and efficiently, expanding access to credit for a broader range of borrowers. This includes individuals with limited traditional credit histories who might benefit from alternative data scoring methods. The competitive landscape is also intensifying, with traditional banks, credit unions, and a burgeoning number of online lenders vying for market share, which drives innovation in product offerings, pricing, and customer experience. The emphasis on seamless, end-to-end digital application processes is a paramount trend, reflecting consumer preference for convenience and speed in financial transactions.

- Digitalization and Mobile-First Lending: Rapid adoption of online and mobile platforms for loan applications and management.

- Personalized Loan Products: Customization of loan terms, interest rates, and repayment schedules based on individual borrower profiles.

- Emergence of Fintech Lenders: Increasing market share of non-bank financial technology companies offering streamlined processes.

- Data-Driven Credit Scoring: Utilization of advanced analytics and alternative data for enhanced risk assessment and broader credit access.

- Regulatory Adaptation: Evolving compliance requirements influencing lending practices and consumer protection.

- Focus on Customer Experience: Emphasis on user-friendly interfaces, quick approval times, and transparent communication.

- Green and Socially Responsible Lending: Growing interest in loans aligned with environmental, social, and governance (ESG) principles.

- Embedded Finance: Integration of lending services directly into non-financial platforms, offering point-of-need credit.

AI Impact Analysis on Personal Loan

Artificial intelligence is profoundly reshaping the personal loan sector by enhancing operational efficiency, improving risk assessment, and personalizing customer experiences. Users frequently inquire about how AI contributes to faster loan approvals, more accurate fraud detection, and the development of tailored financial products. The integration of AI algorithms allows lenders to process vast amounts of applicant data, including traditional credit scores, banking habits, and even alternative data points, with unprecedented speed and precision. This capability significantly reduces manual intervention, minimizes human error, and accelerates the entire loan application and underwriting process, thereby meeting consumer demands for instant financial solutions.

Concerns often raised by users center around data privacy, algorithmic bias, and the transparency of AI-driven decisions. Lenders are actively addressing these issues by implementing robust data security protocols and developing explainable AI models to ensure fairness and compliance with ethical guidelines. The expectation is that AI will continue to drive innovation, leading to more inclusive lending practices that extend credit to underserved populations while maintaining prudent risk management. Ultimately, AI is viewed as a catalyst for a more efficient, accessible, and customer-centric personal loan market, transforming how loans are offered, managed, and repaid.

- Automated Underwriting and Loan Processing: AI-powered algorithms analyze applications, assess creditworthiness, and approve loans in minutes.

- Enhanced Fraud Detection: Machine learning models identify suspicious patterns and anomalies, significantly reducing fraudulent activities.

- Personalized Product Recommendations: AI analyzes customer financial behavior to offer highly customized loan products and repayment plans.

- Improved Customer Service: AI-driven chatbots and virtual assistants provide instant support, answer FAQs, and guide applicants through the process.

- Dynamic Risk Assessment: Continuous monitoring of borrower behavior and market conditions for real-time risk adjustments.

- Alternative Data Scoring: Utilization of non-traditional data points (e.g., utility payments, rental history) to assess credit for thin-file applicants.

- Predictive Analytics for Collections: AI helps identify borrowers at risk of default, enabling proactive intervention and personalized collection strategies.

- Operational Cost Reduction: Automation of repetitive tasks leads to significant savings in administrative and processing costs for lenders.

Key Takeaways Personal Loan Market Size & Forecast

The personal loan market is poised for robust expansion, driven by increasing consumer demand for flexible credit options and the continued digital transformation of financial services. Key questions from users often revolve around the factors fueling this growth and the implications for both borrowers and lenders. The significant projected CAGR reflects a global shift towards accessible and immediate financing solutions, with technology playing a pivotal role in enabling this accessibility. This growth is not merely an increase in loan volume but also a diversification of product offerings and a broadening of the customer base, including segments previously underserved by traditional banking models.

For lenders, the forecasted growth signals both opportunities for market penetration and the need for continuous innovation in risk management and customer engagement. The competitive intensity will likely drive further technological adoption, particularly in AI and data analytics, to maintain profitability and gain market share. For consumers, this translates into more choice, competitive interest rates, and streamlined application processes. The market's expansion is intrinsically linked to global economic stability, regulatory evolution, and the sustained appetite for consumer credit, making it a dynamic and increasingly important segment of the broader financial landscape.

- Significant Market Expansion: Expected to grow at a strong double-digit CAGR from 2025 to 2033, indicating high demand.

- Digital Dominance: Growth is primarily fueled by online and mobile lending platforms, offering speed and convenience.

- Consumer-Centric Shift: Emphasis on personalized loan products and superior customer experience will be crucial for market leaders.

- Technology as a Growth Enabler: AI, machine learning, and big data analytics are fundamental to efficient operations and broadened credit access.

- Diverse Borrower Base: Expansion into segments with non-traditional credit histories through innovative scoring methods.

- Competitive Landscape: Intensified competition among traditional banks, fintechs, and online lenders driving innovation.

- Regulatory Scrutiny: Increased focus on consumer protection and fair lending practices will shape market development.

- Economic Resilience: Market growth will be influenced by global economic conditions and consumer confidence levels.

Personal Loan Market Drivers Analysis

The personal loan market is primarily driven by an increasing consumer need for immediate and flexible access to funds for various purposes, ranging from debt consolidation and home improvements to unexpected medical expenses or significant purchases. The rise of digital banking and financial technology (fintech) has significantly lowered the barriers to entry for both lenders and borrowers, making the application process faster, more convenient, and more accessible than ever before. This digital transformation meets the modern consumer's expectation for seamless, on-demand financial services. Furthermore, economic growth in many regions, coupled with rising disposable incomes, encourages consumers to seek credit for discretionary spending and lifestyle upgrades.

Another significant driver is the growing awareness and acceptance of personal loans as a viable and often more affordable alternative to credit card debt for larger, planned expenditures or consolidating high-interest debts. Marketing efforts by lenders highlighting the benefits of structured repayment plans and lower interest rates contribute to this shift in consumer preference. Additionally, the ability of new lending models, particularly those leveraging AI and alternative data, to assess credit risk more accurately has opened up the market to a broader demographic, including young professionals and individuals with limited traditional credit histories. This inclusivity fuels market expansion by increasing the total addressable market for personal loan products.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Consumer Demand for Flexible Credit | +2.5% | Global | Long-term (2025-2033) |

| Rapid Digitalization and Fintech Innovation | +2.0% | North America, Asia Pacific, Europe | Mid-term (2025-2029) |

| Growing Awareness of Debt Consolidation Benefits | +1.5% | North America, Europe | Mid-term (2026-2030) |

| Expansion of Credit Access through Alternative Data | +1.8% | Emerging Markets (APAC, LATAM, MEA) | Long-term (2027-2033) |

| Favorable Economic Conditions and Disposable Income Growth | +1.2% | Global, particularly developing economies | Short to Mid-term (2025-2028) |

Personal Loan Market Restraints Analysis

Despite the robust growth projections, the personal loan market faces several significant restraints that could temper its expansion. Regulatory scrutiny and evolving compliance requirements represent a substantial hurdle for lenders, particularly as governments aim to protect consumers from predatory lending practices and ensure data privacy. This often leads to increased operational costs and complexity for financial institutions, potentially slowing down product innovation or market entry for new players. Additionally, fluctuations in interest rates, influenced by central bank policies and global economic conditions, can directly impact the affordability of personal loans for consumers and the profitability margins for lenders. Higher interest rates may deter borrowing, while lower rates can squeeze lender margins if not managed effectively.

Another key restraint is the inherent credit risk associated with unsecured lending. Personal loans are often unsecured, meaning they are not backed by collateral, making lenders more vulnerable to defaults. Economic downturns, rising unemployment rates, or personal financial crises can significantly increase default rates, prompting lenders to tighten credit standards, which in turn restricts market growth. The intense competition within the market also acts as a restraint on profitability, as lenders are often forced to offer more competitive rates and terms to attract borrowers, reducing overall revenue potential. Moreover, some consumers may prefer alternative financing options, such as credit cards, buy now pay later (BNPL) services, or home equity lines of credit, depending on their specific needs and credit profiles, diverting demand from personal loans.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Regulatory Frameworks and Compliance Costs | -1.5% | Global | Long-term (2025-2033) |

| Fluctuations in Interest Rates and Economic Volatility | -1.8% | Global | Short to Mid-term (2025-2029) |

| High Credit Risk and Potential for Loan Defaults | -1.7% | Global, particularly during economic downturns | Mid-term (2026-2031) |

| Intense Competition and Pressure on Profit Margins | -1.0% | North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Consumer Preference for Alternative Financing Options | -0.8% | Global | Mid-term (2027-2032) |

Personal Loan Market Opportunities Analysis

The personal loan market presents numerous opportunities for growth and innovation, particularly through the expansion into underserved segments. Millions of individuals globally, including young adults, immigrants, and those in rural areas, have limited access to traditional credit due to thin or non-existent credit histories. Fintech lenders, leveraging AI and alternative data sources, can bridge this gap by offering tailored products and more inclusive credit assessment models, thereby tapping into a vast, unexploited market. The rising demand for digital-first financial services also creates opportunities for lenders to invest in advanced mobile platforms and seamless user interfaces, enhancing customer experience and capturing a technologically savvy demographic.

Strategic partnerships represent another significant opportunity. Collaborations between traditional banks and fintech companies can combine the regulatory expertise and financial stability of incumbents with the agility and technological innovation of startups, leading to more competitive and accessible loan products. Furthermore, the growth of embedded finance, where lending options are integrated directly into e-commerce platforms or point-of-sale systems, offers immense potential for contextual and immediate credit offerings. Developing specialized personal loan products for specific life events such as education financing, medical emergencies, or green initiatives also allows lenders to differentiate their offerings and cater to niche demands, fostering market diversification and sustainable growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Tapping into Underserved and Unbanked Populations | +2.0% | Asia Pacific, Latin America, Africa | Long-term (2025-2033) |

| Development of Niche and Specialized Loan Products | +1.5% | Global | Mid to Long-term (2026-2033) |

| Strategic Partnerships between Traditional Banks and Fintechs | +1.8% | North America, Europe, Asia Pacific | Mid-term (2025-2030) |

| Expansion of Embedded Finance and Point-of-Sale Lending | +2.2% | Global | Long-term (2027-2033) |

| Leveraging AI for Hyper-Personalization and Customer Engagement | +1.7% | Global | Mid-term (2025-2031) |

Personal Loan Market Challenges Impact Analysis

The personal loan market faces several intricate challenges that can impede its growth trajectory. One significant challenge is managing escalating credit risk, especially during periods of economic uncertainty or recession. As personal loans are often unsecured, lenders must continuously refine their underwriting models and risk assessment strategies to mitigate the potential for increased defaults, which can significantly impact profitability and capital reserves. Another formidable challenge is navigating the complex and ever-evolving regulatory landscape. Regulators globally are intensifying their focus on consumer protection, fair lending practices, and data privacy, requiring lenders to invest heavily in compliance, potentially stifling innovation and increasing operational costs.

Technological disruption also presents a dual challenge. While it offers immense opportunities, staying abreast of rapid advancements in AI, machine learning, and cybersecurity requires continuous investment and expertise. Lenders must protect sensitive customer data from increasingly sophisticated cyber threats, ensuring robust security infrastructure and protocols. Furthermore, intense competition from a diverse range of players, including traditional banks, credit unions, and a myriad of fintech startups, makes customer acquisition and retention challenging. This competitive pressure often leads to reduced profit margins and demands constant innovation in product features, pricing, and customer experience. Lastly, the ethical implications of AI in lending, particularly regarding algorithmic bias and transparency, pose a critical challenge, requiring careful development and deployment of AI models to ensure fairness and avoid discriminatory outcomes.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Managing Escalating Credit Risk and Default Rates | -1.9% | Global | Mid-term (2025-2030) |

| Navigating Evolving Regulatory Landscape and Compliance | -1.6% | Global | Long-term (2025-2033) |

| Intense Competition and Pressure on Profitability | -1.3% | North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Data Security and Protection Against Cyber Threats | -1.0% | Global | Continuous |

| Ethical Considerations and Algorithmic Bias in AI Lending | -0.7% | Global | Long-term (2026-2033) |

Personal Loan Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Personal Loan Market, offering insights into its current size, historical performance, and future growth projections. It meticulously examines the key trends, drivers, restraints, opportunities, and challenges that shape the industry's landscape. The report also features a detailed impact analysis of artificial intelligence on lending processes and consumer behavior. Furthermore, it includes extensive segmentation analysis by various parameters, regional highlights, and profiles of key market players, furnishing stakeholders with a holistic understanding of market dynamics and strategic foresight.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.1 Trillion |

| Market Forecast in 2033 | USD 5.0 Trillion |

| Growth Rate | 11.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Financial Solutions, Apex Credit Innovations, Digital Lending Corp., Prime Capital Bank, Zenith Financial Group, SecurePay Loans, OmniCredit Services, Future Finance Hub, TrueWorth Lending, SwiftAdvance Financial, Stellar Bank Group, Elite Credit Solutions, Horizon Lending Partners, Quantum Financial, Unified Loans & Credit, Capital Flow Innovations, Progress Finance Ltd., Modern Money Market, Empower Lending, TrustOne Bank |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The personal loan market is segmented to provide a granular understanding of consumer needs, lender offerings, and market dynamics across various categories. These segmentations are critical for identifying niche opportunities, understanding competitive landscapes, and tailoring products to specific market demands. Analyzing the market through these different lenses allows stakeholders to pinpoint high-growth areas and develop targeted strategies that resonate with diverse borrower profiles and preferences.

Segmentation by loan type reveals the primary drivers of consumer borrowing, such as debt consolidation or home improvement, indicating where the strongest demand lies. Lender type segmentation highlights the evolving competitive landscape, showcasing the rise of fintechs against traditional banks. Understanding interest rate types and loan tenure helps in assessing risk appetite and financial planning among borrowers, while end-use segmentation provides insight into the underlying economic activities prompting personal loan applications. Finally, segmentation by application method and income group reflects the impact of digitalization and financial inclusion efforts on market accessibility.

- By Loan Type: Debt Consolidation Loans, Home Improvement Loans, Medical Loans, Wedding Loans, Travel Loans, Education Loans, Others

- By Lender Type: Banks, Credit Unions, Non-Banking Financial Companies (NBFCs), Fintech Lenders/Online Lenders, Peer-to-Peer (P2P) Lenders

- By Interest Rate Type: Fixed Rate Personal Loans, Variable Rate Personal Loans

- By Tenure: Short-term (Up to 1 year), Medium-term (1 to 5 years), Long-term (Above 5 years)

- By End-Use: Personal Expenses, Professional Expenses, Business Expenses

- By Application Method: Online, Offline

- By Income Group: Low Income, Middle Income, High Income

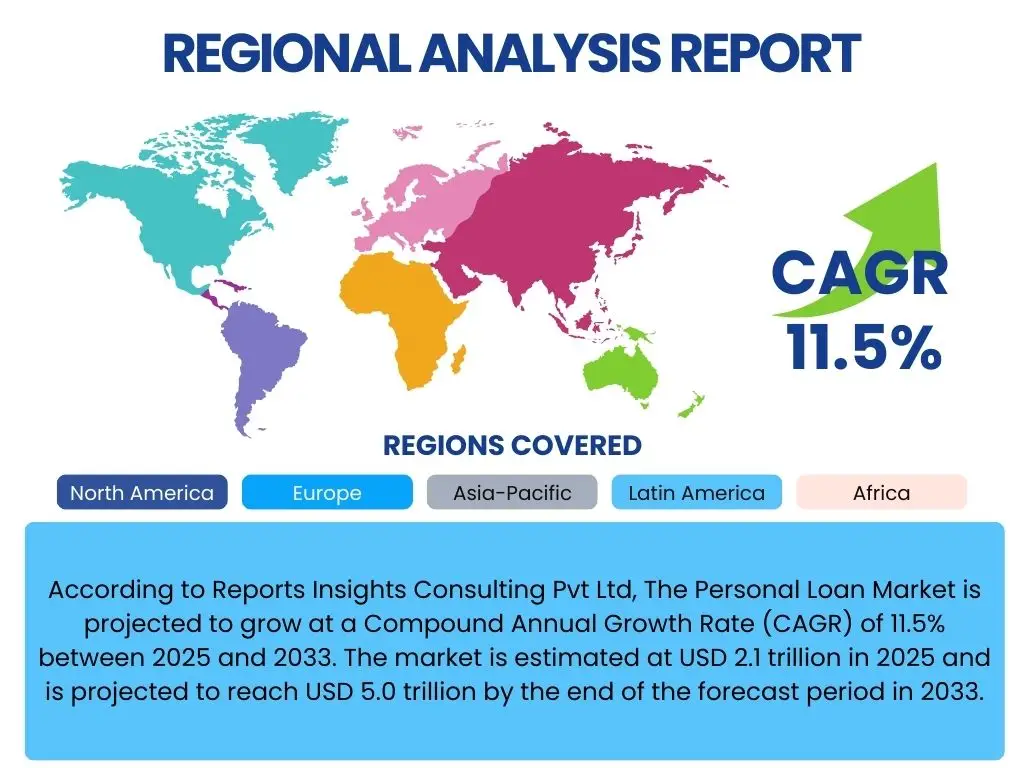

Regional Highlights

The personal loan market exhibits distinct regional dynamics influenced by economic conditions, regulatory environments, technological adoption rates, and cultural attitudes towards debt. North America, particularly the United States, represents a mature and highly competitive market, characterized by advanced digital lending infrastructure and a strong presence of both traditional banks and innovative fintech companies. High consumer awareness and a culture of credit utilization drive consistent demand for personal loans for various purposes, including debt consolidation and large purchases. Regulatory frameworks are generally well-established but continue to evolve, impacting lender operations and consumer protection.

Europe presents a diverse landscape, with varying levels of market maturity across countries. Western European nations show robust digital adoption and demand for consumer credit, while Eastern European markets are rapidly growing, fueled by increasing disposable incomes and financial inclusion initiatives. Asia Pacific is emerging as a powerhouse for personal loan growth, driven by large populations, increasing urbanization, rising middle-class incomes, and widespread mobile penetration. Countries like India and China are witnessing explosive growth in digital lending and fintech innovation, often catering to underserved segments. Latin America and the Middle East & Africa (MEA) are also experiencing significant growth, albeit from a lower base, as financial inclusion efforts intensify and digital infrastructure improves. These regions offer substantial opportunities for lenders willing to navigate varied regulatory complexities and cultural nuances.

- North America: Dominant market share with high digital penetration, sophisticated lending infrastructure, and strong consumer demand for debt consolidation and flexible credit. The U.S. and Canada lead in fintech innovation and diverse product offerings.

- Europe: Fragmented market with mature economies in Western Europe showing steady demand, and emerging markets in Eastern Europe demonstrating rapid growth. Regulatory harmonization efforts across the EU impact lending practices.

- Asia Pacific (APAC): Fastest-growing region, driven by large populations, increasing disposable incomes, and rapid digital transformation. India, China, and Southeast Asian countries are key growth engines, with significant adoption of mobile lending and alternative credit scoring.

- Latin America: Experiencing substantial growth fueled by increasing financial inclusion, urbanization, and a growing middle class. Digitalization is accelerating, though economic volatility and regulatory challenges remain key factors.

- Middle East and Africa (MEA): Emerging market with significant potential due to young populations, increasing internet penetration, and government initiatives promoting financial diversification and digital economy. Demand for personal financing is rising, particularly for small and medium-sized enterprises (SMEs) and consumer needs.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Personal Loan Market.- Global Financial Solutions

- Apex Credit Innovations

- Digital Lending Corp.

- Prime Capital Bank

- Zenith Financial Group

- SecurePay Loans

- OmniCredit Services

- Future Finance Hub

- TrueWorth Lending

- SwiftAdvance Financial

- Stellar Bank Group

- Elite Credit Solutions

- Horizon Lending Partners

- Quantum Financial

- Unified Loans & Credit

- Capital Flow Innovations

- Progress Finance Ltd.

- Modern Money Market

- Empower Lending

- TrustOne Bank

Frequently Asked Questions

What is the projected growth rate for the Personal Loan Market?

The Personal Loan Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2025 and 2033, indicating a robust expansion phase driven by increased demand for flexible credit solutions.

How is AI impacting the personal loan industry?

AI significantly impacts the personal loan industry by enabling automated underwriting, enhancing fraud detection, personalizing loan offers, improving customer service through chatbots, and utilizing alternative data for more inclusive credit scoring, thereby streamlining operations and expanding market access.

What are the primary drivers of the Personal Loan Market?

Key drivers include increasing consumer demand for flexible credit, rapid digitalization of lending services, the rise of fintech innovations, growing awareness of debt consolidation benefits, and the expansion of credit access through alternative data sources and favorable economic conditions.

What are the main challenges faced by the Personal Loan Market?

Major challenges include managing escalating credit risk and potential defaults, navigating complex and evolving regulatory landscapes, intense market competition that pressures profit margins, ensuring data security against cyber threats, and addressing ethical considerations surrounding algorithmic bias in AI lending models.

Which region is expected to show the fastest growth in the Personal Loan Market?

The Asia Pacific (APAC) region is expected to exhibit the fastest growth in the Personal Loan Market, driven by large populations, increasing disposable incomes, rapid urbanization, and widespread adoption of digital lending platforms and fintech solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted