PCB Market

PCB Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706148 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

PCB Market Size

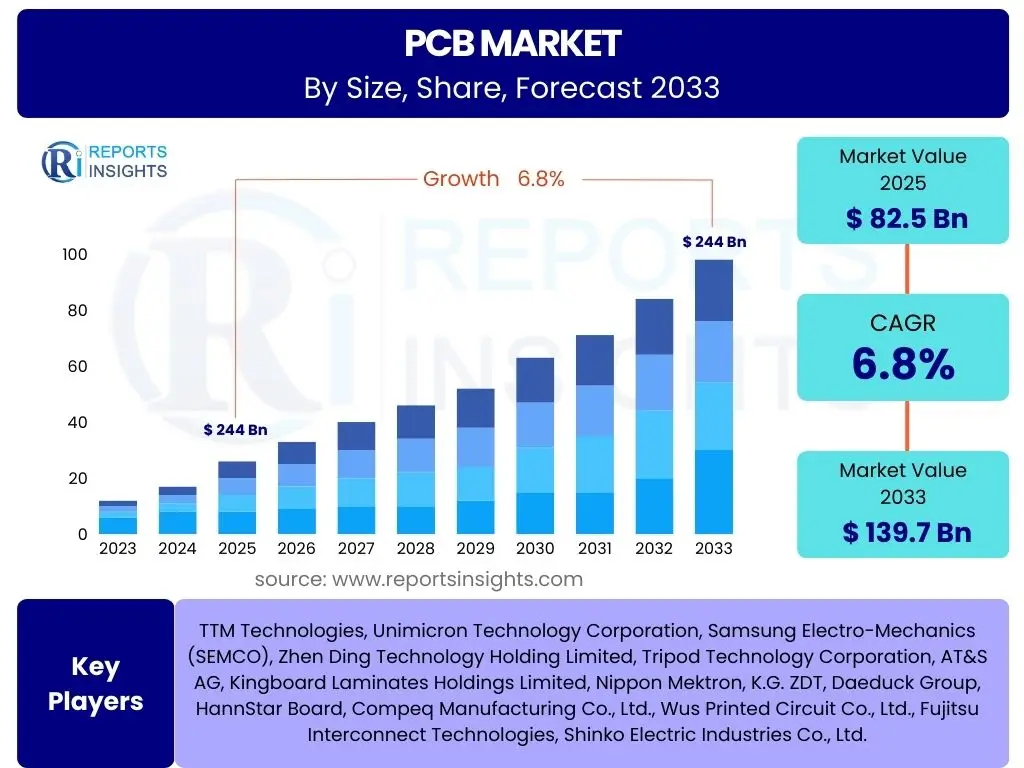

According to Reports Insights Consulting Pvt Ltd, The PCB Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 82.5 billion in 2025 and is projected to reach USD 139.7 billion by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by the escalating demand for advanced electronic devices across various sectors, including consumer electronics, automotive, telecommunications, and industrial automation. The continuous innovation in miniaturization, high-density interconnections, and flexible circuit technologies further underpins this expansion, pushing the boundaries of what PCBs can achieve in modern electronics.

The market's expansion is also significantly influenced by the global rollout of 5G infrastructure, the burgeoning Internet of Things (IoT) ecosystem, and the increasing complexity of automotive electronics, particularly in electric vehicles (EVs) and advanced driver-assistance systems (ADAS). These sectors demand high-performance, reliable, and compact PCBs capable of handling sophisticated functionalities. Furthermore, the rising adoption of smart manufacturing practices and Industry 4.0 initiatives necessitates more intricate and durable PCBs, contributing substantially to the market's positive outlook over the forecast period.

Key PCB Market Trends & Insights

The PCB market is undergoing significant transformation, driven by a confluence of technological advancements and evolving application demands. A primary focus for market stakeholders revolves around understanding how miniaturization and increased functionality are reshaping PCB design and manufacturing. Inquiries frequently pertain to the emergence of novel materials, the integration of higher frequency capabilities, and the growing imperative for eco-friendly production methods. These trends collectively underscore a shift towards more sophisticated, compact, and energy-efficient circuit board solutions, critical for the next generation of electronic devices.

Another crucial area of interest concerns the impact of connectivity technologies like 5G and the Internet of Things (IoT) on PCB requirements. Users often seek insights into how these technologies necessitate advancements in high-speed data transmission, thermal management, and robust signal integrity. Furthermore, the automotive sector's rapid evolution, particularly with electric vehicles and autonomous driving, presents unique demands for highly reliable and durable PCBs capable of operating in harsh environments. The convergence of these factors is steering the PCB market towards innovation in design, materials, and manufacturing processes, ensuring PCBs remain the foundational element for electronic innovation.

- Miniaturization and High-Density Interconnect (HDI) Technologies: Driving smaller, more powerful devices.

- Flexible and Rigid-Flex PCB Adoption: Enabling innovative designs for wearables, medical devices, and complex automotive systems.

- Advanced Material Integration: Use of low-loss, high-frequency, and improved thermal management substrates.

- 5G and IoT Device Proliferation: Increasing demand for high-speed, high-frequency, and reliable PCBs.

- Automotive Electronics Evolution: Growth in PCBs for EVs, ADAS, infotainment, and vehicle connectivity.

- Sustainable Manufacturing Practices: Emphasis on eco-friendly processes, materials, and recycling.

- Additive Manufacturing (3D Printing) for PCBs: Exploring new possibilities for complex geometries and rapid prototyping.

AI Impact Analysis on PCB

Artificial Intelligence (AI) is poised to revolutionize the Printed Circuit Board (PCB) industry across its entire lifecycle, from design to manufacturing and quality control. Users are keen to understand how AI can optimize complex design layouts, reduce development cycles, and enhance manufacturing efficiency. The primary expectation is that AI algorithms will streamline traditionally laborious tasks, such as component placement and routing, by identifying optimal solutions faster than human designers. Furthermore, there is significant interest in AI's capability to predict potential design flaws or manufacturing defects, thereby improving first-pass yield and reducing costly iterations. This intelligent automation promises to not only accelerate product development but also ensure higher reliability in the final product.

Beyond design, AI's impact extends profoundly into the manufacturing floor and supply chain management. Common inquiries relate to AI's role in predictive maintenance of manufacturing equipment, optimizing production schedules, and enhancing visual inspection for defect detection. By analyzing vast datasets from production lines, AI can identify patterns indicative of equipment failure or process deviations, enabling proactive intervention and minimizing downtime. Moreover, AI-powered systems can meticulously analyze images for microscopic flaws, far exceeding human capability in speed and accuracy. This integration of AI is transforming PCB manufacturing into a smarter, more efficient, and highly adaptive process, addressing concerns about cost, quality, and time-to-market.

- Design Automation and Optimization: AI-powered tools accelerate layout and routing, enhancing efficiency and performance.

- Predictive Maintenance: AI algorithms analyze equipment data to predict failures, minimizing downtime in manufacturing.

- Quality Control and Defect Detection: AI-driven visual inspection systems rapidly identify microscopic flaws, improving yield.

- Material Optimization: AI helps in selecting optimal materials based on performance requirements and cost factors.

- Supply Chain Management: AI improves forecasting, inventory management, and logistics for PCB components and raw materials.

- Smart Manufacturing and Industry 4.0 Integration: AI facilitates autonomous operations and real-time process adjustments.

Key Takeaways PCB Market Size & Forecast

The PCB market is characterized by a strong and consistent growth trajectory, driven by the indispensable role PCBs play in virtually all modern electronic devices. A key insight derived from market analyses is the foundational dependence of technological advancement across diverse sectors—from consumer electronics to automotive and aerospace—on increasingly sophisticated and reliable PCB solutions. Stakeholders frequently inquire about the underlying factors sustaining this growth and the specific technological innovations that will be pivotal for future expansion. This includes a clear understanding that while volume growth is important, value growth is increasingly tied to high-performance, specialized, and advanced PCB types.

Furthermore, the market's forecast highlights the critical importance of regional dynamics, particularly the dominance of the Asia Pacific region in both manufacturing and consumption. Future growth will be significantly influenced by continued investment in R&D for advanced materials, miniaturization techniques, and sustainable manufacturing processes. The insights indicate that adaptability to rapid technological cycles, resilience against supply chain disruptions, and a focus on specialized applications will be paramount for companies aiming to capitalize on the projected market expansion. The market is not just growing in size but also evolving in complexity and technical demands.

- Consistent Growth Trajectory: The PCB market is set for robust expansion through 2033, driven by electronic device proliferation.

- Diversified Application Base: Growth is broad-based, spanning consumer electronics, automotive, industrial, and telecommunications.

- Regional Market Dominance: Asia Pacific remains the central hub for both PCB production and consumption, influencing global trends.

- Technological Advancement as Core Driver: Miniaturization, HDI, flexible circuits, and advanced materials are key to innovation and market value.

- Supply Chain Resilience Imperative: Geopolitical factors and material availability necessitate robust and agile supply chain strategies.

PCB Market Drivers Analysis

The global PCB market's expansion is fundamentally propelled by the pervasive integration of electronics into everyday life and industrial processes. A key driver is the relentless consumer demand for smarter, more compact, and increasingly connected devices, ranging from smartphones and wearables to advanced home appliances. This necessitates PCBs with higher component densities and improved performance. Simultaneously, the rapid evolution of specialized industries such as automotive, telecommunications, and healthcare consistently demands more sophisticated and reliable circuit board solutions, tailored for specific high-performance or harsh environmental requirements.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Consumer Electronics | +1.5% | APAC, North America, Europe | Long-term |

| Growth in Automotive Electronics (EVs, ADAS) | +1.2% | Europe, North America, APAC (China, Japan) | Medium-term |

| Expansion of IoT and 5G Infrastructure | +1.0% | Global | Long-term |

| Advancements in Healthcare Devices & Wearables | +0.8% | North America, Europe | Medium-term |

| Industrial Automation & Industry 4.0 Adoption | +0.7% | Europe, APAC (Germany, Japan, China) | Medium-term |

PCB Market Restraints Analysis

While the PCB market exhibits strong growth potential, it also faces several significant restraints that could temper its expansion. One prominent challenge is the volatility of raw material prices, particularly for critical components like copper, epoxy resins, and fiberglass, which directly impact manufacturing costs and profit margins. Furthermore, the industry operates under increasingly stringent environmental regulations regarding chemical usage, waste disposal, and energy consumption, adding compliance costs and operational complexities. These factors, alongside broader macroeconomic uncertainties and geopolitical tensions, introduce significant risks to the industry's stability and growth projections.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -0.9% | Global | Short-term |

| Stringent Environmental Regulations | -0.7% | Europe, North America | Long-term |

| Supply Chain Vulnerabilities & Geopolitical Tensions | -0.6% | Global | Short-term to Medium-term |

| High R&D Costs for Advanced Materials & Processes | -0.5% | Global | Long-term |

PCB Market Opportunities Analysis

Despite existing challenges, the PCB market is rich with emerging opportunities driven by technological innovation and evolving industry needs. A significant opportunity lies in the expanding adoption of flexible and rigid-flex PCBs, which enable compact, lightweight, and versatile electronic designs crucial for next-generation wearables, medical devices, and aerospace applications. Moreover, the increasing demand for high-frequency and high-speed data transmission capabilities, particularly with the rollout of 5G networks and advanced computing, opens new avenues for specialized PCB types. The industry is also exploring novel manufacturing techniques, such as additive manufacturing, to overcome traditional design limitations and accelerate prototyping.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Flexible and Rigid-Flex PCBs | +1.1% | Global | Medium-term |

| Growing Demand for High-Frequency & High-Speed PCBs | +0.9% | North America, APAC | Long-term |

| Additive Manufacturing (3D Printing) for PCBs | +0.8% | Global | Long-term |

| Increased Focus on Green Manufacturing & Recycling Solutions | +0.6% | Europe, North America | Long-term |

PCB Market Challenges Impact Analysis

The PCB market faces inherent challenges that demand continuous innovation and strategic adaptation from manufacturers. Rapid technological obsolescence is a constant concern, as advancements in semiconductor technology and electronic component miniaturization frequently necessitate entirely new PCB designs and manufacturing processes, rendering older technologies quickly outdated. Furthermore, the global shortage of skilled labor, particularly in highly specialized areas of PCB design, fabrication, and testing, poses a significant hurdle to scaling production and adopting advanced techniques. These factors, compounded by the constant pressure for higher quality and reliability in increasingly complex applications, create a demanding operational environment for market players.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence & Innovation Cycles | -0.8% | Global | Long-term |

| Skilled Labor Shortage & Talent Retention | -0.7% | Global | Medium-term |

| Counterfeiting and Intellectual Property Infringement | -0.5% | Global | Medium-term |

| Stringent Quality Control & Reliability Requirements | -0.4% | Global | Long-term |

PCB Market - Updated Report Scope

This report provides an in-depth analysis of the global Printed Circuit Board (PCB) market, offering comprehensive insights into its current state, historical performance, and future growth prospects. It segments the market based on various factors, including type, substrate material, and application, to deliver a granular understanding of market dynamics. The study also covers key regional trends and competitive landscape analysis, identifying major players and their strategic initiatives, thereby equipping stakeholders with crucial information for informed decision-making and strategic planning within the evolving electronics manufacturing ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 82.5 Billion |

| Market Forecast in 2033 | USD 139.7 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | TTM Technologies, Unimicron Technology Corporation, Samsung Electro-Mechanics (SEMCO), Zhen Ding Technology Holding Limited, Tripod Technology Corporation, AT&S AG, Kingboard Laminates Holdings Limited, Nippon Mektron, K.G. ZDT, Daeduck Group, HannStar Board, Compeq Manufacturing Co., Ltd., Wus Printed Circuit Co., Ltd., Fujitsu Interconnect Technologies, Shinko Electric Industries Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The PCB market is extensively segmented to reflect the diverse technological requirements and application areas that drive its growth. Understanding these segments is crucial for identifying specific market opportunities and challenges. The primary segmentation is by type, categorizing PCBs based on their structural characteristics and flexibility, which directly impacts their suitability for various electronic applications. Further segmentation by substrate material provides insights into the raw material preferences driven by performance demands such as thermal management, signal integrity, and cost-efficiency. Finally, application-based segmentation highlights the key end-use industries that are significantly contributing to the market's demand, ranging from high-volume consumer electronics to specialized aerospace and medical devices.

- By Type: This segment includes Rigid PCBs, which are foundational for most electronics due to their durability; Flexible PCBs, offering bendability for compact and unique designs; Rigid-Flex PCBs, combining the benefits of both; High-Density Interconnect (HDI) PCBs, crucial for miniaturization; and Multilayer PCBs, enabling complex circuitry in limited space.

- By Substrate Material: Key materials include FR-4, the most common and cost-effective; Polyimide, preferred for flexible circuits due to its thermal stability; CEM (Composite Epoxy Material), a more cost-effective alternative to FR-4; PTFE (Polytetrafluoroethylene), used for high-frequency applications; and Ceramic, offering excellent thermal conductivity and stability for high-power applications.

- By Application: This segmentation covers critical end-use industries such as Consumer Electronics (smartphones, laptops, wearables), Automotive (EVs, ADAS, infotainment), Industrial Electronics (automation, power control), Telecommunications (5G infrastructure, network equipment), Medical Devices (diagnostics, implants), and Aerospace & Defense (avionics, radar systems).

Regional Highlights

The global PCB market exhibits distinct regional dynamics, largely influenced by manufacturing capabilities, technological adoption rates, and local demand across various industries. Asia Pacific (APAC) dominates the global PCB market, acting as both the largest production hub and the primary consumer of PCBs. Countries like China, Taiwan, South Korea, and Japan are at the forefront of manufacturing, benefiting from established electronics ecosystems, skilled labor, and significant investments in advanced production technologies. China, in particular, leverages its vast manufacturing infrastructure and a massive domestic market to maintain its leading position. Taiwan and South Korea are renowned for their high-end and advanced PCB production, especially for complex HDI and semiconductor packaging applications. This region's growth is fueled by strong consumer electronics demand, robust automotive sector expansion, and extensive telecommunications infrastructure development, including aggressive 5G rollouts.

North America represents a significant market for high-performance and specialized PCBs, driven by strong demand from the aerospace and defense, medical, and high-tech industrial sectors. The region emphasizes innovation in material science and advanced manufacturing techniques, supporting the development of highly reliable and sophisticated circuit boards for critical applications. The presence of leading technology companies and a focus on R&D contributes to North America's strong position in value-added PCB segments. While not as dominant in mass production as APAC, its emphasis on advanced design and niche markets ensures continued growth, particularly with the proliferation of IoT devices and electric vehicle technologies requiring robust and secure PCB solutions.

Europe stands as a mature market with a strong emphasis on industrial automation, automotive electronics, and specialized medical devices. Germany, France, and the UK are key contributors, focusing on high-quality, high-reliability PCBs that meet stringent European regulatory standards. The region is actively investing in Industry 4.0 initiatives, driving demand for complex PCBs in smart factories and automated systems. Furthermore, Europe's strong automotive sector, transitioning rapidly towards electric and autonomous vehicles, provides a consistent demand for advanced PCBs capable of handling high power and complex sensor integration. Sustainability and eco-friendly manufacturing practices are also gaining significant traction in European PCB production, influencing material choices and process innovations.

Latin America and the Middle East & Africa (MEA) regions are emerging markets for PCBs, characterized by developing electronics manufacturing bases and increasing adoption of digital technologies. Latin America's growth is propelled by expanding consumer electronics assembly, automotive manufacturing, and telecommunications infrastructure upgrades. Countries like Brazil and Mexico are witnessing increased local production capabilities, supported by foreign investments. In MEA, the demand for PCBs is driven by investments in smart city projects, telecommunications network expansion, and growing industrialization. While these regions currently hold smaller market shares compared to APAC, North America, and Europe, they offer substantial future growth potential as their electronic industries mature and disposable incomes rise, leading to greater adoption of electronic devices and advanced infrastructure.

- Asia Pacific (APAC): Dominates global production and consumption, driven by China, Taiwan, South Korea, and Japan. Strong growth in consumer electronics, automotive, and 5G infrastructure.

- North America: Focus on high-performance PCBs for aerospace, defense, medical devices, and high-tech industrial applications. Emphasis on R&D and advanced materials.

- Europe: Key markets in Germany, France, and UK. Driven by industrial automation, automotive electronics (EVs), and medical devices, with a strong focus on high reliability and sustainability.

- Latin America: Emerging market with growing electronics assembly and automotive sectors, particularly in Brazil and Mexico.

- Middle East & Africa (MEA): Growth spurred by telecommunications infrastructure development, smart city initiatives, and increasing industrialization.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the PCB Market.- TTM Technologies

- Unimicron Technology Corporation

- Samsung Electro-Mechanics (SEMCO)

- Zhen Ding Technology Holding Limited

- Tripod Technology Corporation

- AT&S AG

- Kingboard Laminates Holdings Limited

- Nippon Mektron

- K.G. ZDT

- Daeduck Group

- HannStar Board

- Compeq Manufacturing Co., Ltd.

- Wus Printed Circuit Co., Ltd.

- Fujitsu Interconnect Technologies

- Shinko Electric Industries Co., Ltd.

Frequently Asked Questions

What is a Printed Circuit Board (PCB) and its primary function?

A Printed Circuit Board (PCB) is a board that mechanically supports and electrically connects electronic components using conductive tracks, pads, and other features etched from copper sheets laminated onto a non-conductive substrate. Its primary function is to provide a reliable and efficient platform for mounting and interconnecting electronic components, forming the foundation of almost all modern electronic devices.

What are the main types of PCBs and their applications?

The main types of PCBs include Rigid PCBs (found in computers, TVs), Flexible PCBs (used in wearables, cameras, medical devices due to their bendability), Rigid-Flex PCBs (combining both rigid and flexible areas for complex, compact designs in aerospace, military, and medical applications), High-Density Interconnect (HDI) PCBs (for smartphones and tablets due to miniaturization needs), and Multilayer PCBs (for complex electronics requiring high component density).

How is the automotive industry influencing PCB market growth?

The automotive industry is a significant driver of PCB market growth, particularly with the rapid evolution of Electric Vehicles (EVs) and Advanced Driver-Assistance Systems (ADAS). Modern vehicles require a growing number of sophisticated PCBs for power management, infotainment systems, sensor arrays, navigation, and autonomous driving functions. These applications demand high-reliability, durable, and often high-frequency PCBs capable of performing in harsh automotive environments, fueling innovation and demand in the market.

What role does 5G technology play in the expansion of the PCB market?

5G technology is a pivotal factor in the expansion of the PCB market, as its widespread deployment necessitates high-frequency, low-loss, and high-speed PCBs. Base stations, network infrastructure, and 5G-enabled devices all require specialized PCBs capable of handling the increased data rates and higher frequencies of 5G networks. This demand is driving innovation in PCB materials and manufacturing processes, particularly for boards designed to maintain signal integrity at millimeter-wave frequencies, significantly contributing to market growth.

What are the key sustainability trends impacting PCB manufacturing?

Key sustainability trends impacting PCB manufacturing include the adoption of halogen-free materials, lead-free soldering processes, and the reduction of hazardous waste through improved chemical management. There is also a growing emphasis on energy efficiency in manufacturing operations and the development of more recyclable or biodegradable PCB substrates. These efforts are driven by increasing environmental regulations, corporate social responsibility initiatives, and consumer demand for greener electronic products, pushing the industry towards more eco-friendly production methods.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted