Pathology Device Market

Pathology Device Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707296 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Pathology Device Market Size

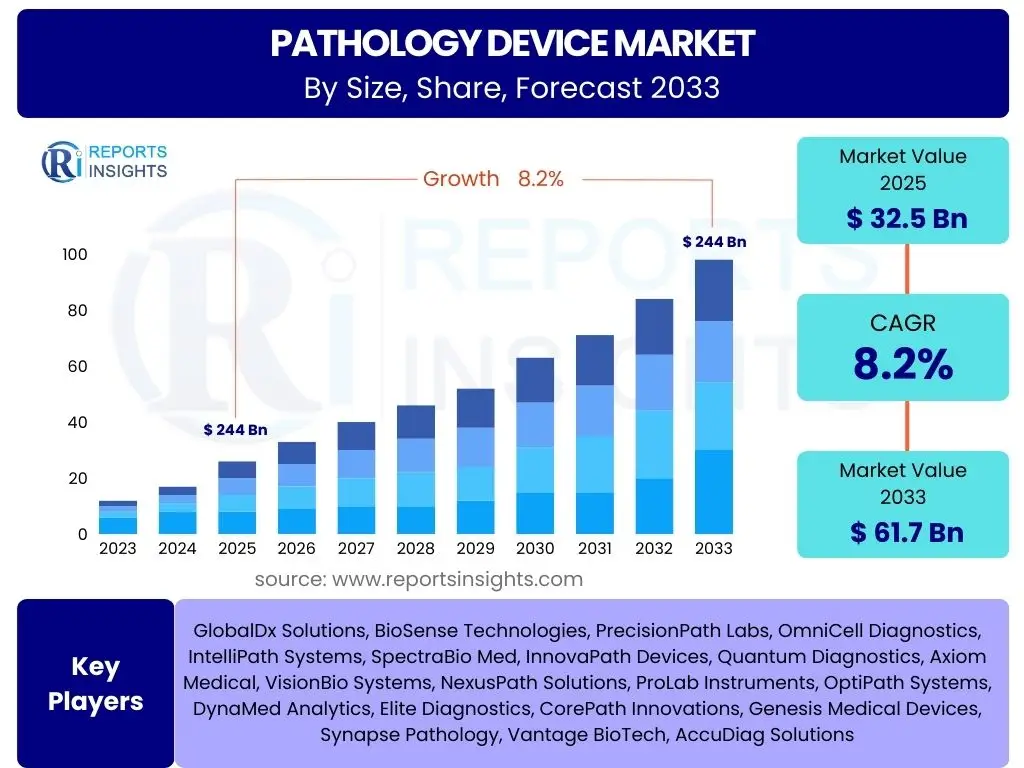

According to Reports Insights Consulting Pvt Ltd, The Pathology Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% between 2025 and 2033. The market is estimated at USD 32.5 Billion in 2025 and is projected to reach USD 61.7 Billion by the end of the forecast period in 2033.

Key Pathology Device Market Trends & Insights

The pathology device market is experiencing significant transformation driven by advancements in digital technology and a growing demand for precise diagnostics. Common inquiries from users revolve around the integration of artificial intelligence and machine learning, the increasing adoption of digital pathology workflows, and the shift towards personalized medicine. Stakeholders are keen to understand how these trends are impacting diagnostic accuracy, laboratory efficiency, and overall patient outcomes. The market is also seeing a rise in demand for automated systems to reduce human error and improve throughput, alongside a heightened focus on the development of compact and cost-effective devices suitable for various healthcare settings.

Furthermore, the COVID-19 pandemic significantly accelerated the adoption of remote diagnostic capabilities, including telepathology, underscoring the necessity for robust digital infrastructure. This push towards remote solutions continues to shape investment priorities and technological development within the sector. There is also a notable trend towards integrating multi-omics data with traditional pathology, providing a more holistic view for disease understanding and treatment planning. This convergence of technologies aims to enhance diagnostic precision and enable more targeted therapeutic interventions, marking a crucial step towards truly personalized healthcare.

- Accelerated adoption of digital pathology solutions for enhanced workflow efficiency.

- Increasing integration of Artificial Intelligence (AI) and Machine Learning (ML) for image analysis and diagnostic support.

- Growing demand for automated pathology systems to reduce manual intervention and improve throughput.

- Expansion of personalized medicine initiatives driving the need for advanced companion diagnostics.

- Emergence of telepathology and remote diagnostic capabilities, especially post-pandemic.

- Shift towards integrated diagnostic platforms combining various analytical techniques.

AI Impact Analysis on Pathology Device

User queries regarding the impact of AI on pathology devices frequently center on its capabilities in automating routine tasks, enhancing diagnostic accuracy, and enabling predictive analytics. There is significant interest in how AI algorithms can interpret complex pathological images, identify subtle anomalies, and assist pathologists in making more consistent and rapid diagnoses. Users also express concerns about data privacy, the ethical implications of AI in healthcare, and the potential for job displacement, alongside the need for robust validation of AI models in clinical settings. The general consensus is that AI will augment, rather than replace, human expertise, transforming the pathologist's role into a more consultative and analytical one.

The integration of AI is expected to revolutionize several aspects of pathology, from initial specimen processing to final report generation. AI-powered image analysis tools can quantify cellular features, detect rare events, and correlate morphological findings with molecular data, which is critical for precision oncology. This capability is particularly valuable in high-volume laboratories, where it can significantly reduce turnaround times and improve diagnostic throughput. Moreover, AI is poised to facilitate the discovery of novel biomarkers and accelerate research by identifying patterns in vast datasets that might be imperceptible to the human eye, thus opening new avenues for disease understanding and treatment development.

- Enhances diagnostic accuracy and consistency through automated image analysis.

- Reduces turnaround times for diagnoses, improving laboratory efficiency.

- Facilitates quantitative analysis of pathological features, aiding in disease grading and prognosis.

- Supports the discovery of new biomarkers and accelerates research efforts.

- Enables predictive analytics for disease progression and treatment response.

- Automates routine tasks, freeing up pathologists for complex cases and consultations.

Key Takeaways Pathology Device Market Size & Forecast

The Pathology Device Market is poised for substantial growth, driven by an escalating global disease burden, particularly chronic conditions like cancer, and continuous technological innovation. Common user questions highlight the market's resilience and its critical role in modern healthcare, emphasizing the shift towards more sophisticated, automated, and digital diagnostic solutions. The forecast indicates a robust expansion, underlining the increasing investment in healthcare infrastructure and the demand for early and accurate disease detection capabilities worldwide. This growth is a testament to the essential nature of pathology services in patient care pathways.

Strategic insights suggest that digital transformation, propelled by AI and advanced imaging, will be central to future market development, offering opportunities for enhanced efficiency and diagnostic precision. Market stakeholders are focusing on improving connectivity, interoperability, and data security to support these digital ecosystems. Furthermore, the expansion into emerging economies, coupled with a focus on cost-effective and accessible solutions, represents a significant avenue for market penetration and sustained growth. The market's future will be defined by its capacity to integrate diverse technologies and meet the evolving needs of a global patient population.

- The market is projected for significant expansion, reaching USD 61.7 Billion by 2033 with an 8.2% CAGR.

- Digital pathology and AI integration are pivotal growth accelerators, improving diagnostics and workflow.

- Rising prevalence of chronic diseases and aging populations are primary demand drivers.

- Automation and advanced imaging technologies are key to improving laboratory efficiency and accuracy.

- Emerging markets offer substantial untapped growth opportunities due to developing healthcare infrastructure.

Pathology Device Market Drivers Analysis

The pathology device market is predominantly driven by the increasing global incidence of chronic diseases, particularly cancer, which necessitates early and accurate diagnosis. The aging population worldwide also contributes significantly to market expansion, as older demographics are more susceptible to various pathologies requiring diagnostic intervention. Technological advancements, including the proliferation of digital pathology, AI-powered analysis, and molecular diagnostics, are revolutionizing the field, enhancing diagnostic capabilities, and improving laboratory workflows. These innovations enable faster, more precise, and efficient diagnoses, thereby driving their adoption across healthcare settings.

Furthermore, rising healthcare expenditures and a growing emphasis on preventive care and early disease detection by governments and healthcare organizations are fueling the demand for advanced pathology devices. The increasing awareness among patients regarding timely diagnosis and treatment also plays a crucial role. Additionally, the development of personalized medicine, which relies heavily on precise diagnostic information derived from pathology, is creating a demand for sophisticated and integrated diagnostic platforms. These interconnected factors collectively propel the growth trajectory of the pathology device market globally.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Prevalence of Chronic Diseases | +1.5% | Global, particularly North America, APAC | Long-term |

| Aging Global Population | +1.2% | Europe, North America, Japan | Mid to Long-term |

| Technological Advancements in Digital Pathology & AI | +1.8% | North America, Europe, China | Short to Mid-term |

| Increasing Healthcare Expenditure & Awareness | +1.0% | Emerging Economies, Latin America | Mid-term |

Pathology Device Market Restraints Analysis

Despite robust growth, the pathology device market faces several significant restraints. The high initial cost of advanced pathology equipment, particularly digital pathology scanners and integrated AI systems, represents a substantial barrier to adoption, especially for smaller laboratories or healthcare facilities in developing regions. This capital expenditure, coupled with ongoing maintenance and software licensing fees, can deter potential buyers. Moreover, the stringent regulatory frameworks governing medical devices, especially in developed markets like North America and Europe, lead to lengthy approval processes and high compliance costs, thereby slowing down market entry for new innovations.

Another critical restraint is the scarcity of skilled professionals capable of operating and interpreting results from highly specialized pathology devices, particularly those involving advanced digital and AI platforms. This talent gap necessitates significant investment in training and education, which can further inflate operational costs. Additionally, data security and privacy concerns surrounding the handling of sensitive patient information in digital pathology systems pose a significant challenge. Addressing these concerns requires robust cybersecurity measures and compliance with global data protection regulations, adding complexity and cost to system deployment. Infrastructure limitations, particularly in emerging economies, such as unreliable power supply and insufficient network connectivity, also impede the widespread adoption of advanced digital pathology solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Devices | -0.8% | Global, particularly developing regions | Mid to Long-term |

| Stringent Regulatory Landscape | -0.7% | North America, Europe | Short to Mid-term |

| Lack of Skilled Professionals | -0.6% | Global, particularly remote areas | Mid to Long-term |

| Data Security & Privacy Concerns | -0.5% | Global | Short-term |

Pathology Device Market Opportunities Analysis

The pathology device market presents numerous growth opportunities, particularly stemming from the accelerating adoption of telepathology and remote diagnostic capabilities. This trend, bolstered by advancements in connectivity and digital imaging, allows for expert diagnoses from distant locations, expanding access to specialized pathology services, especially in underserved or rural areas. The ongoing shift towards personalized medicine also opens vast avenues for innovation, as it necessitates highly specific and sensitive diagnostic tools to guide tailored therapeutic interventions. This demand drives the development of integrated platforms capable of analyzing complex molecular and histological data.

Furthermore, the significant untapped market potential in developing countries, characterized by improving healthcare infrastructure and increasing healthcare expenditure, offers substantial growth prospects for pathology device manufacturers. These regions are increasingly investing in modern diagnostic capabilities to address their growing disease burdens. The integration of multi-omics data (genomics, proteomics, metabolomics) with traditional pathology also represents a nascent but powerful opportunity, promising a more comprehensive understanding of disease pathogenesis and progression. This holistic approach is crucial for advancing precision diagnostics and developing more effective treatments, driving demand for devices that can facilitate such integrated analyses. Additionally, the growing focus on preventative healthcare globally increases the volume of screening and early detection tests, directly boosting the demand for pathology devices.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Telepathology & Remote Diagnostics | +1.7% | Global, particularly remote and rural areas | Short to Mid-term |

| Growth in Personalized Medicine | +1.9% | North America, Europe, Asia Pacific | Mid to Long-term |

| Untapped Markets in Developing Countries | +1.6% | Asia Pacific, Latin America, MEA | Long-term |

| Integration of Multi-Omics Data | +1.4% | Global, R&D focused regions | Mid to Long-term |

Pathology Device Market Challenges Impact Analysis

The pathology device market faces several formidable challenges that can impede its growth and widespread adoption. Interoperability issues among different digital pathology platforms, laboratory information systems (LIS), and hospital information systems (HIS) remain a significant hurdle. This lack of seamless data exchange and integration can create workflow inefficiencies, data silos, and hinder the full potential of digital transformation in pathology labs. Healthcare providers often struggle with the complexity of integrating diverse vendor solutions, leading to increased IT costs and operational delays.

Another key challenge is the inherent resistance to adopting new technologies within traditional pathology workflows. Many established laboratories are hesitant to transition from conventional microscopy to digital systems due to perceived disruptions in workflow, the need for significant capital investment, and the learning curve associated with new software and hardware. Cybersecurity threats also pose a growing concern, as digital pathology systems handle vast amounts of sensitive patient data, making them attractive targets for cyberattacks. Ensuring robust data protection and compliance with evolving privacy regulations, such as GDPR and HIPAA, is a continuous and complex undertaking. Furthermore, the complexities surrounding reimbursement policies for advanced digital and AI-powered pathology services can create financial uncertainties for providers, impacting the rate of adoption for these innovative technologies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Interoperability Issues | -0.9% | Global, particularly integrated healthcare systems | Short to Mid-term |

| Resistance to New Technology Adoption | -0.7% | Established laboratories, older professionals | Mid-term |

| Cybersecurity Threats & Data Privacy | -0.8% | Global | Short to Mid-term |

| Reimbursement Complexities | -0.6% | North America, Europe | Long-term |

Pathology Device Market - Updated Report Scope

This comprehensive market research report on the Pathology Device Market provides an in-depth analysis of market size, trends, drivers, restraints, opportunities, and challenges across various segments and regions. The scope encompasses detailed insights into product types, applications, end-users, and key technologies shaping the industry landscape. It offers strategic foresight into future market dynamics, highlighting key growth areas and potential investment opportunities for stakeholders. The report aims to equip businesses with actionable intelligence to navigate the evolving market and formulate effective strategies for sustainable growth and competitive advantage.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 32.5 Billion |

| Market Forecast in 2033 | USD 61.7 Billion |

| Growth Rate | 8.2% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | GlobalDx Solutions, BioSense Technologies, PrecisionPath Labs, OmniCell Diagnostics, IntelliPath Systems, SpectraBio Med, InnovaPath Devices, Quantum Diagnostics, Axiom Medical, VisionBio Systems, NexusPath Solutions, ProLab Instruments, OptiPath Systems, DynaMed Analytics, Elite Diagnostics, CorePath Innovations, Genesis Medical Devices, Synapse Pathology, Vantage BioTech, AccuDiag Solutions |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Pathology Device Market is comprehensively segmented based on product type, application, end-user, and technology to provide a granular view of its diverse landscape. This segmentation allows for a detailed analysis of market dynamics within each category, highlighting key growth areas and niche opportunities. The product type segment covers a wide array of instruments and consumables essential for pathological analysis, from basic microscopes to advanced digital scanners and AI-powered software. Application segmentation focuses on the various disease areas where pathology devices are crucial for diagnosis and monitoring, with oncology being a dominant segment due to the high incidence of cancer globally.

End-user segmentation differentiates the market based on the types of facilities utilizing these devices, including hospitals, diagnostic laboratories, and research institutions, each with unique requirements and purchasing patterns. The technology segment delves into the specific methodologies employed, such as digital pathology, molecular pathology, and immunohistochemistry, reflecting the continuous innovation and evolution in diagnostic approaches. This multi-dimensional segmentation is critical for understanding market demand, competitive positioning, and strategic planning across the global pathology device ecosystem.

- By Product Type: Microscopes, Scanners, Imaging Systems, Tissue Processors, Stainers, Microtomes & Cryostats, Consumables, Software & Services, Automated Systems.

- By Application: Cancer Diagnostics, Infectious Disease Diagnostics, Neurological Disorders Diagnostics, Gastrointestinal Diseases Diagnostics, Renal Diseases Diagnostics, Autoimmune Diseases Diagnostics, Other Applications.

- By End-User: Hospitals, Diagnostic & Clinical Laboratories, Academic & Research Institutes, Pharmaceutical & Biotechnology Companies, Contract Research Organizations (CROs).

- By Technology: Digital Pathology, Molecular Pathology, Immunohistochemistry (IHC), Cytopathology, Histopathology, Flow Cytometry.

Regional Highlights

- North America: This region dominates the pathology device market, driven by high healthcare expenditure, the presence of leading research institutions, early adoption of advanced technologies like digital pathology and AI, and a high prevalence of chronic diseases. The U.S. and Canada are significant contributors to market growth due fueled by favorable reimbursement policies and increasing R&D investments.

- Europe: A mature market with substantial demand for advanced diagnostic tools, especially in countries like Germany, the UK, and France. Growth is supported by robust healthcare infrastructure, government initiatives for disease screening, and increasing adoption of automation in laboratories. Stringent regulatory standards also drive innovation towards high-quality devices.

- Asia Pacific (APAC): Expected to exhibit the highest CAGR during the forecast period due to rapidly developing healthcare infrastructure, a large patient pool, increasing healthcare awareness, and rising disposable incomes in countries like China, India, and Japan. Government initiatives to improve diagnostic capabilities and expand access to healthcare are major growth drivers.

- Latin America: This region is characterized by improving healthcare access and increasing investment in modern medical facilities. Countries like Brazil and Mexico are emerging as key markets, driven by rising chronic disease prevalence and a growing demand for accurate diagnostics.

- Middle East & Africa (MEA): Represents an emerging market with significant growth potential, primarily driven by increasing healthcare spending, the establishment of new hospitals and diagnostic centers, and a rising focus on medical tourism. Investments in advanced diagnostic technologies are steadily increasing in major economies like Saudi Arabia, UAE, and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Pathology Device Market.- GlobalDx Solutions

- BioSense Technologies

- PrecisionPath Labs

- OmniCell Diagnostics

- IntelliPath Systems

- SpectraBio Med

- InnovaPath Devices

- Quantum Diagnostics

- Axiom Medical

- VisionBio Systems

- NexusPath Solutions

- ProLab Instruments

- OptiPath Systems

- DynaMed Analytics

- Elite Diagnostics

- CorePath Innovations

- Genesis Medical Devices

- Synapse Pathology

- Vantage BioTech

- AccuDiag Solutions

Frequently Asked Questions

Analyze common user questions about the Pathology Device market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate for the Pathology Device Market?

The Pathology Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% between 2025 and 2033, reaching an estimated value of USD 61.7 Billion by 2033.

How is AI impacting the Pathology Device Market?

AI is significantly impacting the market by enhancing diagnostic accuracy through automated image analysis, reducing turnaround times, supporting biomarker discovery, and automating routine tasks, thereby augmenting the pathologist's capabilities.

What are the primary drivers of growth in the Pathology Device Market?

Key drivers include the rising global prevalence of chronic diseases, an aging population, continuous technological advancements in digital pathology and AI, increasing healthcare expenditure, and a growing emphasis on personalized medicine.

What are the main challenges faced by the Pathology Device Market?

Major challenges include high initial costs of advanced devices, stringent regulatory frameworks, a shortage of skilled professionals, data security and privacy concerns, and interoperability issues between different digital systems.

Which regions offer significant growth opportunities in the Pathology Device Market?

While North America and Europe are established markets, the Asia Pacific region, particularly countries like China and India, offers the highest growth opportunities due to developing healthcare infrastructure and increasing healthcare awareness.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted