Patch Panel Market

Patch Panel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707911 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Patch Panel Market Size

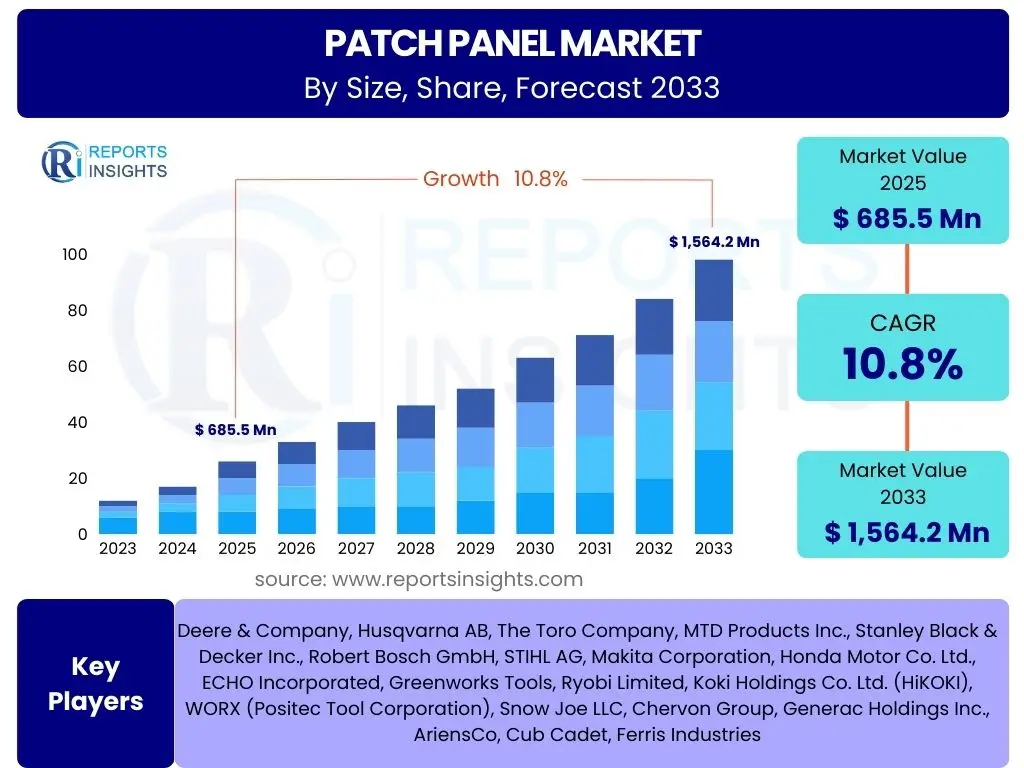

According to Reports Insights Consulting Pvt Ltd, The Patch Panel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.8% between 2025 and 2033. The market is estimated at USD 685.5 Million in 2025 and is projected to reach USD 1,564.2 Million by the end of the forecast period in 2033.

Key Patch Panel Market Trends & Insights

The Patch Panel Market is undergoing significant evolution driven by the relentless demand for higher bandwidth, increased network density, and the growing complexity of IT infrastructure. A primary trend involves the shift towards fiber optic patch panels, particularly in data centers and enterprise networks, to support advanced applications requiring faster data transmission speeds and greater reliability. This move is complemented by the integration of higher-density solutions, allowing more connections within a smaller footprint, which is crucial for optimizing rack space and improving network scalability.

Another prominent trend observed is the increasing adoption of modular patch panel systems. These systems offer enhanced flexibility, allowing network administrators to easily upgrade, reconfigure, or expand network infrastructure without complete overhauls. This modularity not only reduces long-term operational costs but also streamlines maintenance processes, making networks more adaptable to future technological advancements. Furthermore, the integration of Power over Ethernet (PoE) capabilities within copper patch panels is gaining traction, simplifying deployments for devices like IP cameras, VoIP phones, and wireless access points by delivering both data and power over a single cable, thereby reducing cabling complexity and power infrastructure requirements.

The market is also witnessing a surge in intelligent or "smart" patch panel solutions, which incorporate advanced features for remote monitoring, automated documentation, and real-time connectivity status. These innovations are crucial for proactive network management, minimizing downtime, and ensuring optimal performance in increasingly complex network environments. The continuous expansion of cloud computing, edge computing, and the Internet of Things (IoT) further underpins these trends, necessitating robust, flexible, and high-performance physical layer infrastructure that patch panels inherently provide.

- Transition to Fiber Optic Patch Panels for high-speed data.

- Increased demand for High-Density Patch Panel solutions.

- Rising adoption of Modular Patch Panel systems for flexibility.

- Integration of Power over Ethernet (PoE) in copper panels.

- Emergence of Smart Patch Panels with monitoring capabilities.

- Focus on improved cable management and airflow optimization.

- Standardization efforts for future-proof network infrastructure.

AI Impact Analysis on Patch Panel

The advent of Artificial Intelligence (AI) profoundly impacts the demands placed on network infrastructure, including patch panels, primarily through the exponential generation and processing of data. AI applications, such as machine learning training, real-time analytics, and sophisticated simulations, require massive data throughput and ultra-low latency, necessitating high-performance, resilient, and efficiently managed physical network layers. This drives the adoption of advanced fiber optic patch panels capable of handling terabit-level speeds and the precise management of numerous high-bandwidth connections within data centers and supercomputing facilities where AI workloads are executed.

Beyond demanding higher performance, AI also offers opportunities for optimizing the management and operation of network infrastructure itself. While patch panels are passive components, AI can play a crucial role in intelligent infrastructure management systems that monitor network traffic patterns, predict potential bottlenecks, and even automate provisioning or reconfiguration tasks. For instance, AI-powered analytics can process data from network monitoring tools to recommend optimal patch panel layouts, identify underutilized ports, or flag connection issues before they escalate, thereby enhancing network reliability and operational efficiency. The integration of "smart" features within patch panels, such as sensors for environmental conditions or connection status, could further feed into AI-driven network management platforms, enabling more predictive and proactive maintenance.

Furthermore, the growth of edge AI and distributed AI models will necessitate robust and scalable network connectivity closer to the data source. This will drive demand for patch panels in new environments, including smart factories, intelligent buildings, and autonomous vehicle infrastructure, requiring solutions that are rugged, compact, and capable of supporting diverse connectivity needs. The push for automated and self-optimizing networks, often leveraging AI, will inherently rely on a well-organized and high-performance physical layer that patch panels facilitate, emphasizing the need for structured cabling and easy-to-manage connectivity points to support future AI-driven network architectures.

- Increased demand for high-performance patch panels due to AI data processing.

- AI-driven network management systems optimize patch panel utilization and maintenance.

- Potential for "smart" patch panels with embedded sensors for AI integration.

- Growth of edge AI drives patch panel demand in new distributed environments.

- AI mandates robust and scalable physical layer for ultra-low latency.

- Automated network provisioning can leverage well-structured patch panel data.

Key Takeaways Patch Panel Market Size & Forecast

The Patch Panel Market is poised for substantial growth over the forecast period, driven primarily by the escalating demand for high-speed data transmission, the continuous expansion of data centers, and the widespread adoption of digital transformation initiatives across various industries. The market's upward trajectory is a direct reflection of the indispensable role patch panels play in organizing and managing the complex physical layer of modern network infrastructures. Their ability to facilitate flexible connectivity, simplify troubleshooting, and ensure network scalability positions them as foundational components in an increasingly interconnected world.

A significant takeaway is the increasing bifurcation of the market, with strong growth in both advanced fiber optic solutions for high-bandwidth applications and intelligent copper solutions catering to Power over Ethernet (PoE) demands in enterprise environments. This indicates a maturing market that is adapting to diverse technological requirements rather than a single dominant solution. The emphasis on modularity and high-density designs will continue to be critical, as organizations seek to optimize their physical space and future-proof their network investments against evolving bandwidth needs.

Looking ahead, the market's forecast growth underscores the ongoing investment in network infrastructure globally, propelled by trends such as 5G deployment, cloud computing expansion, and the proliferation of IoT devices. These factors collectively ensure a sustained demand for efficient and reliable patch panel solutions. For stakeholders, understanding these dynamics, particularly the shift towards intelligent and high-performance offerings, will be crucial for strategic planning and capitalizing on the significant market opportunities presented by the digital age.

- Consistent growth propelled by data center expansion and digital transformation.

- Fiber optic solutions driving high-bandwidth application growth.

- Modular and high-density designs are key for future network scalability.

- PoE-enabled copper panels cater to enterprise and IoT connectivity.

- Intelligent patch panel solutions gaining traction for enhanced management.

- Market resilience linked to global infrastructure investments and 5G/IoT.

- Crucial role in network organization, troubleshooting, and flexibility.

Patch Panel Market Drivers Analysis

The Patch Panel Market is significantly propelled by several key drivers, primarily stemming from the exponential growth in data traffic and the expanding global digital infrastructure. The construction and expansion of data centers, driven by cloud computing, big data analytics, and virtualization, necessitate robust and scalable physical layer connectivity solutions, where patch panels are essential for efficient cable management and interconnection. As organizations migrate more operations to the cloud and rely heavily on data-intensive applications, the demand for high-performance networking components, including advanced patch panels, naturally rises to ensure reliable and high-speed data flow.

Furthermore, the increasing adoption of high-speed internet and broadband services globally, alongside the proliferation of Internet of Things (IoT) devices, fuels the demand for organized and efficient network infrastructure. Smart homes, smart cities, and industrial IoT applications require extensive network deployments, from edge devices to core networks, all relying on structured cabling and patch panels to manage the vast number of connections. The ongoing upgrade cycles for older network infrastructure, particularly the transition from slower Ethernet standards to Gigabit and 10 Gigabit Ethernet (and beyond), also contribute significantly to market growth as businesses and telecommunication providers invest in newer, more capable patch panel solutions to support these enhanced speeds.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for high-speed internet & bandwidth | +2.5% | Global (APAC, North America) | Short-to-Medium Term |

| Increased data center construction & expansion | +2.3% | North America, APAC, Europe | Medium-to-Long Term |

| Proliferation of IoT devices and smart buildings | +1.8% | Global | Medium-to-Long Term |

| Expansion of enterprise networks and cloud computing | +2.0% | Global | Short-to-Medium Term |

Patch Panel Market Restraints Analysis

Despite the robust growth drivers, the Patch Panel Market faces certain restraints that could temper its expansion. One significant restraint is the relatively high initial installation cost associated with advanced patch panel systems, especially fiber optic and high-density solutions. While these systems offer long-term benefits in terms of performance and scalability, the upfront investment in specialized cabling, connectors, and skilled labor can be a deterrent for smaller businesses or those with limited IT budgets. This cost factor often leads some organizations to defer upgrades or opt for less sophisticated, lower-cost alternatives, particularly in price-sensitive markets.

Another challenge stems from the increasing complexity involved in managing high-density cabling infrastructure. As patch panels accommodate more ports in smaller spaces, the task of installation, troubleshooting, and ongoing maintenance becomes more intricate. This complexity can lead to increased labor costs, higher potential for human error, and longer downtime during network reconfigurations. The scarcity of highly skilled technicians capable of efficiently deploying and managing these complex systems further exacerbates this issue, posing a bottleneck to widespread adoption in some regions.

Furthermore, the ongoing advancements in wireless communication technologies, such as Wi-Fi 6/6E and 5G, present a perceived alternative to wired infrastructure in certain scenarios. While patch panels remain fundamental for backbone and critical connections, the increasing capability and reliability of wireless solutions for end-device connectivity might reduce the overall number of wired ports required in some enterprise or residential environments. While wireless and wired infrastructure are often complementary, the perception of wireless as a complete substitute can impact investment decisions for new wired installations, particularly in less critical areas.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial installation costs for advanced systems | -1.2% | Global (Emerging Economies) | Short-to-Medium Term |

| Complexities in managing high-density cabling infrastructure | -0.8% | Global | Medium Term |

| Competition from wireless technologies in certain applications | -0.5% | Global | Short-to-Medium Term |

Patch Panel Market Opportunities Analysis

The Patch Panel Market is ripe with opportunities driven by several emerging trends and technological shifts. One significant opportunity lies in the continuous upgrade cycles for existing network infrastructure across enterprises, data centers, and telecommunication networks. As organizations increasingly migrate to higher bandwidth standards like 10, 40, 100 Gigabit Ethernet, and beyond, there is a constant need to replace older, lower-capacity patch panels with modern, high-performance fiber optic or Category 6a/7/8 copper solutions. This sustained demand for upgrades ensures a recurring revenue stream for manufacturers and solution providers.

The advent of "smart" or intelligent patch panels represents another substantial growth avenue. These next-generation panels incorporate features such as integrated sensors, remote monitoring capabilities, and automated infrastructure management (AIM) software integration. Such intelligence allows for real-time visibility into port status, connection mapping, and environmental conditions, significantly improving network uptime, simplifying troubleshooting, and reducing operational costs. The demand for these advanced solutions is particularly strong in large data centers and critical network environments seeking to enhance efficiency and reliability through automation and proactive management.

Furthermore, the global expansion of Fiber-to-the-Home (FTTx) and Fiber-to-the-Business (FTTB) deployments presents a considerable opportunity for fiber optic patch panels. Governments and telecommunication companies worldwide are investing heavily in extending fiber optic networks to provide ultra-high-speed internet access, especially in underserved rural areas and rapidly developing urban centers. This massive infrastructure rollout requires a vast quantity of fiber patch panels for managing and distributing optical connections at various points within the network, from central offices to subscriber premises, ensuring robust and scalable connectivity for future generations.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of "smart" or intelligent patch panels | +1.5% | North America, Europe, APAC | Medium-to-Long Term |

| Growth in fiber-to-the-home/business (FTTx) deployments | +1.8% | APAC, Europe, Latin America | Medium-to-Long Term |

| Demand for modular and scalable solutions | +1.0% | Global | Short-to-Medium Term |

| Upgrade cycles for older network infrastructure | +1.2% | Global | Short-to-Medium Term |

Patch Panel Market Challenges Impact Analysis

The Patch Panel Market faces several challenges that can impede its growth trajectory and operational efficiency. One significant challenge is the rapid pace of technological advancements in networking, which often leads to shorter product lifecycles and pressure on manufacturers to continuously innovate. As new Ethernet standards and fiber optic technologies emerge, existing patch panel designs can quickly become outdated, requiring substantial R&D investments to keep pace. This creates a constant need for compatibility and backward integration while simultaneously developing solutions for future high-bandwidth requirements, posing a complex balancing act for market players.

Another critical challenge revolves around the increasing demand for skilled labor to install and manage complex, high-density patch panel systems, especially fiber optic deployments. The precision required for fiber splicing, termination, and testing, combined with the intricacies of managing hundreds or thousands of connections in a small space, necessitates highly trained technicians. A shortage of such skilled professionals, particularly in developing regions, can lead to installation delays, errors, and suboptimal network performance, ultimately hindering market adoption and customer satisfaction. Training and certification programs are crucial but often represent a significant investment for companies.

Furthermore, intense price competition from generic or unbranded products, particularly in the lower-end copper patch panel segment, presents a continuous challenge. While established brands offer superior quality, reliability, and support, cheaper alternatives can undercut pricing, especially in projects where budget constraints are paramount. This commoditization pressure forces manufacturers to continually optimize their production processes, innovate to differentiate their offerings, and compete on factors beyond just price, such as performance, ease of installation, and advanced features. Maintaining profitability amidst this competitive landscape requires strategic positioning and a clear value proposition.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid technological advancements and evolving standards | -0.9% | Global | Short-to-Medium Term |

| Skilled labor shortage for complex installations | -0.7% | Global (Developing Regions) | Medium Term |

| Price competition from generic products | -1.0% | Global | Short-to-Medium Term |

Patch Panel Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Patch Panel Market, offering critical insights into its current size, growth drivers, restraints, opportunities, and future projections. The report meticulously segments the market by type, port density, application, and end-use industry, providing a granular view of market dynamics across key regions. It also includes an extensive competitive landscape analysis, profiling leading players and their strategic initiatives, to offer stakeholders a clear understanding of the market's competitive environment and potential growth avenues. The scope includes detailed forecasts for market size and growth rates from 2025 to 2033, building upon historical data from 2019 to 2023.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 685.5 Million |

| Market Forecast in 2033 | USD 1,564.2 Million |

| Growth Rate | 10.8% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | CommScope, Panduit, Leviton, Corning, Nexans, Legrand, Belden, Siemon, Hubbell, D-Link, TE Connectivity, Schneider Electric, Furukawa Electric, ADC Krone, Excel Networking |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Patch Panel Market is meticulously segmented to provide a detailed understanding of its various components and their individual market dynamics. This segmentation allows for precise analysis of market trends, consumer preferences, and growth opportunities across different product types, performance capacities, and end-use applications. Understanding these segments is crucial for stakeholders to develop targeted strategies and allocate resources effectively within this evolving market landscape.

The segmentation by type distinguishes between copper and fiber optic patch panels, reflecting the fundamental differences in their underlying technology and application scenarios. Copper panels are further categorized by their Ethernet standards (Cat5e, Cat6, Cat6a, Cat7, Cat8), catering to varying bandwidth requirements in local area networks, while fiber optic panels are differentiated by connector types (SC, LC, MPO/MTP) and typically serve high-speed data centers and backbone networks. This distinction highlights the diverse technological needs within the market and the specialized solutions available to address them.

Further segmentation by port density provides insights into the market's demand for space-efficient solutions, ranging from 12-port to 96-port and other ultra-high-density configurations. This aspect is particularly relevant for data centers and large enterprises aiming to maximize rack space. Additionally, segmenting by application (data centers, enterprise, telecom, industrial, residential, broadcast) and end-use industry (IT & Telecom, BFSI, Healthcare, Manufacturing, Government, Education) reveals the specific vertical markets driving demand, showcasing how different sectors leverage patch panel technology to meet their unique networking requirements.

- By Type: Copper (Cat5e, Cat6, Cat6a, Cat7, Cat8), Fiber Optic (SC, LC, MPO/MTP), Modular

- By Port Density: 12-port, 24-port, 48-port, 96-port, Other High-Density

- By Application: Data Centers, Enterprise Networks, Telecommunications, Industrial, Residential, Broadcast

- By End-Use Industry: IT & Telecom, BFSI, Healthcare, Manufacturing, Government, Education, Others

- By Form Factor: Rack-mount, Wall-mount

Regional Highlights

- North America: This region is a leading market for patch panels, driven by the presence of numerous data centers, robust enterprise network expansions, and early adoption of advanced networking technologies. Significant investments in cloud infrastructure and smart building initiatives further bolster market growth. The demand for high-performance fiber optic and high-density copper panels is particularly strong.

- Europe: Europe exhibits substantial growth due to digital transformation initiatives, increasing investments in telecommunication infrastructure, and the expansion of smart cities. Countries like Germany, the UK, and France are key contributors, focusing on upgrading existing network infrastructure and deploying next-generation fiber networks. Emphasis on energy efficiency and sustainable solutions also influences product adoption.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by rapid economic development, urbanization, and massive investments in IT and telecom infrastructure across countries like China, India, Japan, and South Korea. The proliferation of mobile devices, internet users, and the expansion of data centers drive immense demand for scalable and cost-effective patch panel solutions. FTTx deployments are a major catalyst.

- Latin America: This region demonstrates steady growth, primarily due to increasing internet penetration, expanding enterprise networks, and growing investments in data center facilities. Countries such as Brazil and Mexico are leading the charge in modernizing their digital infrastructure, creating opportunities for both copper and fiber optic patch panels, particularly in the telecommunications and government sectors.

- Middle East and Africa (MEA): The MEA region is experiencing emerging growth, driven by ambitious smart city projects (e.g., in UAE, Saudi Arabia), diversification from oil-dependent economies, and significant investments in developing robust ICT infrastructure. The expansion of broadband connectivity and cloud services across the region is creating new demand for structured cabling and patch panel solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Patch Panel Market.- CommScope

- Panduit

- Leviton

- Corning

- Nexans

- Legrand

- Belden

- Siemon

- Hubbell

- D-Link

- TE Connectivity

- Schneider Electric

- Furukawa Electric

- ADC Krone

- Excel Networking

- Digitus Professional

- Opterna

- Phoenix Contact

- Molex

- AFL

Frequently Asked Questions

What is a patch panel and its primary function?

A patch panel is a mounted hardware assembly containing a number of ports that connect incoming and outgoing lines of a local area network (LAN) or other communication system. Its primary function is to provide a centralized, flexible, and organized point for managing network cables, allowing for easy connection, disconnection, and reconfiguration of network devices and circuits.

Why are patch panels considered important for network infrastructure?

Patch panels are crucial for network infrastructure because they enhance organization, reduce cable clutter, and simplify troubleshooting. They protect active network equipment ports from wear and tear, enable flexible network reconfigurations without disrupting the entire system, and provide a clear, manageable interface for all wired connections, ultimately improving network reliability and reducing maintenance costs.

What are the main types of patch panels available in the market?

The main types of patch panels include copper patch panels, primarily used for Ethernet networks and segmented by category (Cat5e, Cat6, Cat6a, Cat7, Cat8), and fiber optic patch panels, designed for high-speed data transmission using fiber optic cables, typically categorized by connector types (SC, LC, MPO/MTP). Modular patch panels, which allow for a mix of copper and fiber, are also increasingly popular.

How do patch panels contribute to overall network efficiency and scalability?

Patch panels contribute to network efficiency by providing a structured cabling system that minimizes signal interference and facilitates quick identification and resolution of connectivity issues. They enhance scalability by allowing easy addition or removal of network devices without extensive re-cabling, supporting future upgrades to higher bandwidths, and optimizing rack space through high-density designs, thus future-proofing network investments.

What future trends are significantly impacting patch panel technology and market demand?

Future trends significantly impacting patch panel technology include the increasing demand for ultra-high-density solutions for hyperscale data centers, the continued transition to fiber optic panels to support 100GbE and beyond, and the integration of "smart" features for intelligent infrastructure management. The proliferation of Power over Ethernet (PoE) devices and the global expansion of FTTx deployments are also driving demand for specialized and high-performance patch panel solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted