Paper and Paperboard Container and Packaging Market

Paper and Paperboard Container and Packaging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700339 | Last Updated : July 24, 2025 |

Format : ![]()

![]()

![]()

![]()

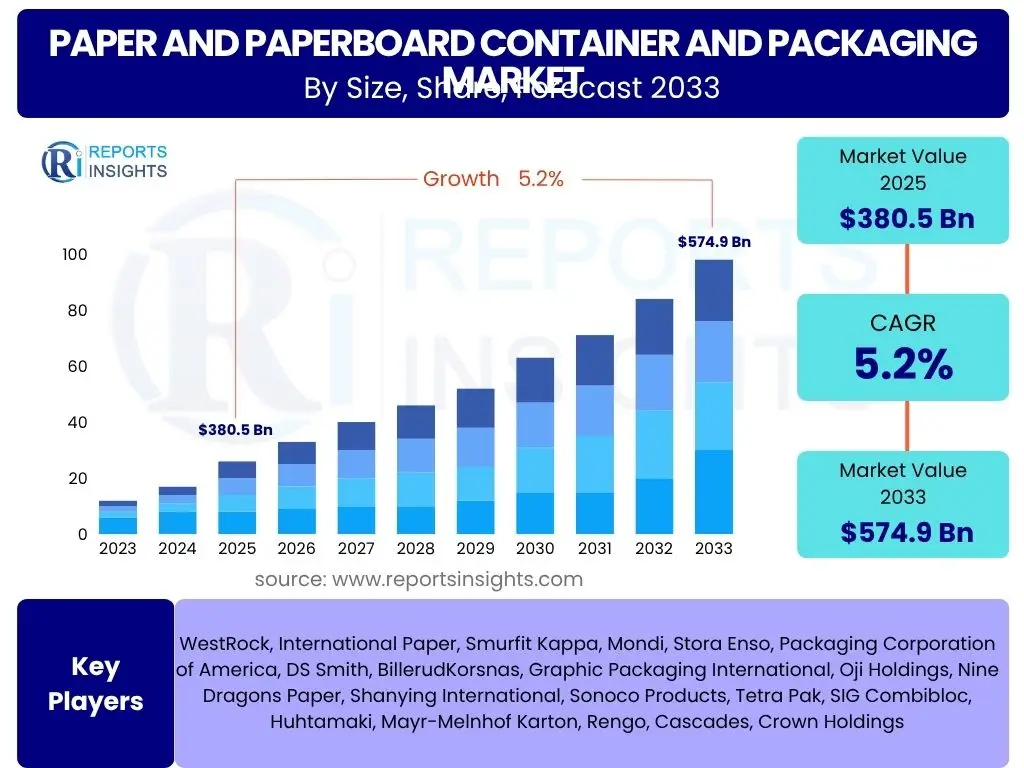

Paper and Paperboard Container and Packaging Market Size

Paper and Paperboard Container and Packaging Market is projected to grow at a Compound annual growth rate (CAGR) of 5.2% between 2025 and 2033, valued at USD 380.5 billion in 2025 and is projected to grow to USD 574.9 billion by 2033, the end of the forecast period.

Key Paper and Paperboard Container and Packaging Market Trends & Insights

The paper and paperboard container and packaging market is undergoing significant transformation, driven by evolving consumer preferences, regulatory shifts, and technological advancements. Key trends shaping its trajectory include:

- Increasing demand for sustainable and recyclable packaging solutions.

- Rapid expansion of e-commerce necessitating robust and lightweight packaging.

- Technological innovations in paperboard, enhancing barrier properties and durability.

- Growing preference for fiber-based packaging over single-use plastics.

- Development of smart packaging features for enhanced traceability and consumer engagement.

- Focus on circular economy principles in packaging design and production.

- Expansion into new applications like liquid food and pharmaceutical packaging.

- Adoption of automation and digitalization in packaging manufacturing processes.

- Lightweighting initiatives to reduce material consumption and transportation costs.

AI Impact Analysis on Paper and Paperboard Container and Packaging

Artificial Intelligence (AI) is set to revolutionize the paper and paperboard container and packaging market by optimizing various stages of the value chain, from design to end-of-life management. AI's capabilities in data analysis, predictive modeling, and automation offer unprecedented opportunities for efficiency and innovation:

- Enhanced demand forecasting and supply chain optimization using predictive analytics.

- Automated quality control and defect detection in manufacturing processes.

- AI-powered design tools for optimizing packaging aesthetics, structural integrity, and material usage.

- Robotics and automation for efficient packaging assembly, sorting, and logistics.

- Improved waste management and recycling processes through AI-driven sorting and material identification.

- Personalized packaging solutions based on consumer data and AI insights.

- Predictive maintenance for manufacturing equipment, reducing downtime and operational costs.

- Sustainability tracking and reporting, leveraging AI to monitor environmental impact.

Key Takeaways Paper and Paperboard Container and Packaging Market Size & Forecast

- The market is poised for significant growth, driven primarily by sustainability mandates and e-commerce expansion.

- Paper and paperboard are increasingly preferred alternatives to conventional plastics due to environmental concerns.

- Technological advancements in material science are enhancing the functional properties of paper packaging.

- Asia Pacific is expected to remain a dominant region, with strong growth in emerging economies.

- Strategic partnerships and mergers are prevalent as companies seek to consolidate market share and innovation capabilities.

- Investment in advanced manufacturing technologies and AI integration will be critical for future competitiveness.

- The shift towards customized and secure packaging solutions is a notable trend across various end-use sectors.

- Regulatory frameworks globally are accelerating the adoption of fiber-based packaging.

Paper and Paperboard Container and Packaging Market Drivers Analysis

The paper and paperboard container and packaging market is propelled by a confluence of powerful drivers, primarily centered around global shifts towards sustainability, the expansion of digital commerce, and continuous innovation in material science. These factors collectively create a robust demand for paper-based packaging solutions, positioning them as essential components across diverse industries. The increasing consumer awareness regarding environmental impact, coupled with stringent government regulations against single-use plastics, significantly bolsters the market's growth trajectory. Furthermore, the burgeoning e-commerce sector demands high volumes of protective, lightweight, and customizable packaging, which paper and paperboard products are well-equipped to provide. Innovations in manufacturing processes and material composition also contribute, enabling paper packaging to meet diverse functional requirements previously challenging for fiber-based materials.| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Push for Sustainability and Eco-friendly Packaging | +1.5% | Europe, North America, APAC (China, India), Latin America | Long-term (2025-2033) |

| E-commerce Expansion and Increased Demand for Shipping Packaging | +1.2% | Global, particularly APAC (China, India), North America, Europe | Medium to Long-term (2025-2033) |

| Ban and Restriction on Single-Use Plastics | +0.8% | Europe, Asia Pacific (India, Southeast Asia), North America, Africa | Medium-term (2025-2029) |

| Innovations in Paperboard Technology and Barrier Coatings | +0.7% | Developed Economies (North America, Europe), R&D hubs in APAC | Long-term (2025-2033) |

| Growth in Food and Beverage Industry and Consumer Goods Sector | +1.0% | Global, especially emerging markets in APAC, Latin America, MEA | Long-term (2025-2033) |

| Increasing Awareness of Recycling and Circular Economy | +0.5% | Europe, North America, parts of Asia (Japan, South Korea) | Medium to Long-term (2025-2033) |

| Demand for Lightweight and Cost-Effective Packaging Solutions | +0.3% | Global, particularly logistics-intensive industries | Medium to Long-term (2025-2033) |

Paper and Paperboard Container and Packaging Market Restraints Analysis

Despite the robust growth drivers, the paper and paperboard container and packaging market faces several significant restraints that could impede its expansion. These challenges often stem from the inherent nature of the raw materials, the energy-intensive manufacturing processes, and the competitive landscape dominated by alternative packaging materials. Volatility in raw material prices, particularly pulp and recycled paper, directly impacts production costs and profitability margins for manufacturers. Environmental concerns related to deforestation, even if often misattributed to responsibly sourced paper, lead to stringent regulations and public scrutiny. Furthermore, the battle for market share against plastics, glass, and metals, which offer superior barrier properties for certain applications, remains a constant pressure. The capital-intensive nature of setting up and upgrading paper mills also presents a barrier to entry and expansion.| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices (Pulp, Recycled Fiber) | -0.9% | Global, affecting major producing and consuming regions | Short to Medium-term (2025-2028) |

| Competition from Alternative Packaging Materials (Plastics, Glass, Metal) | -0.8% | Global, especially in food, beverage, and personal care sectors | Long-term (2025-2033) |

| High Energy Consumption and Operational Costs | -0.6% | Global, impacting regions with higher energy prices (e.g., Europe) | Medium to Long-term (2025-2033) |

| Stringent Environmental Regulations and Deforestation Concerns | -0.5% | Europe, North America, Southeast Asia, Brazil | Long-term (2025-2033) |

| Limitations in Barrier Properties for Certain Applications (Moisture, Oxygen) | -0.4% | Global, relevant for food, pharma, and sensitive product packaging | Long-term (2025-2033) |

| Challenges in Waste Collection and Recycling Infrastructure in Developing Regions | -0.3% | APAC, Latin America, MEA | Long-term (2025-2033) |

| High Capital Investment Required for New Production Capacities | -0.2% | Global, impacting new entrants and expansion plans | Long-term (2025-2033) |

Paper and Paperboard Container and Packaging Market Opportunities Analysis

The paper and paperboard container and packaging market is rich with opportunities, particularly as global focus shifts towards sustainable and innovative solutions. The increasing demand for biodegradable and compostable packaging presents a significant avenue for growth, allowing manufacturers to cater to environmentally conscious consumers and regulatory requirements. Developments in smart packaging technologies, such as integrated sensors and QR codes, unlock new possibilities for enhanced product traceability, supply chain efficiency, and consumer engagement. Furthermore, the vast, untapped potential in emerging economies, driven by rising disposable incomes and expanding retail sectors, offers significant market penetration opportunities. Customization and personalization trends, coupled with the ability to optimize packaging for reduced material usage (lightweighting), also provide competitive advantages. These opportunities collectively highlight the market's adaptive capacity and its potential for continued evolution.| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Fully Biodegradable and Compostable Packaging Solutions | +1.3% | Europe, North America, APAC (Japan, South Korea) | Long-term (2027-2033) |

| Integration of Smart Packaging Technologies (RFID, QR Codes, Sensors) | +0.9% | Developed economies, tech-savvy markets | Medium to Long-term (2026-2033) |

| Untapped Potential in Emerging Economies with Growing Consumer Bases | +1.1% | APAC (India, Indonesia), Latin America (Brazil, Mexico), MEA | Long-term (2025-2033) |

| Lightweighting and Material Optimization for Reduced Resource Consumption | +0.7% | Global, particularly in logistics and e-commerce sectors | Medium to Long-term (2025-2033) |

| Increased Demand for Customized and Personalized Packaging | +0.6% | North America, Europe, parts of APAC | Medium-term (2025-2029) |

| Expansion into Niche Markets (e.g., Sustainable Luxury Packaging, Pharmaceutical) | +0.5% | Global, with regional pockets of high-value markets | Long-term (2025-2033) |

| Advancements in Recycling Technologies and Infrastructure | +0.4% | Europe, North America, East Asia | Long-term (2027-2033) |

Paper and Paperboard Container and Packaging Market Challenges Impact Analysis

The paper and paperboard container and packaging market, while experiencing significant growth, is not without its share of formidable challenges. These often relate to the functional limitations of paper as a material, complexities within global supply chains, and the persistent issue of waste management. Developing paper-based packaging with adequate moisture and oxygen barrier properties to protect sensitive products remains a key technical hurdle, limiting its applicability in certain food and pharmaceutical sectors. Furthermore, the global nature of raw material sourcing and product distribution exposes the industry to frequent supply chain disruptions, impacted by geopolitical events, trade policies, and natural disasters. Despite the inherent recyclability of paper, inadequate waste management infrastructure in many regions leads to significant volumes ending up in landfills, undermining the industry's sustainability narrative. High capital investment for new technologies and product security concerns also pose substantial hurdles.| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technical Limitations in Moisture and Barrier Properties for Specific Applications | -0.7% | Global, especially food, beverage, and pharmaceutical industries | Long-term (2025-2033) |

| Supply Chain Disruptions and Geopolitical Instability | -0.8% | Global, particularly regions reliant on imports/exports | Short to Medium-term (2025-2028) |

| Ineffective Waste Management and Recycling Infrastructure in Many Regions | -0.6% | APAC, Latin America, MEA, parts of Eastern Europe | Long-term (2025-2033) |

| High Capital Investment for Adopting New Technologies and Expanding Capacity | -0.5% | Global, impacting smaller players and developing markets | Long-term (2025-2033) |

| Counterfeiting and Ensuring Product Security and Authenticity | -0.4% | Global, especially for high-value goods (e.g., luxury, pharma) | Medium to Long-term (2025-2033) |

| Public Perception and Greenwashing Concerns | -0.3% | Developed economies with high environmental awareness | Medium-term (2025-2029) |

| Increasing Regulatory Scrutiny on Chemical Additives in Paperboard | -0.2% | Europe, North America, some parts of Asia | Medium-term (2025-2029) |

Paper and Paperboard Container and Packaging Market - Updated Report Scope

This updated report provides a comprehensive analysis of the Paper and Paperboard Container and Packaging Market, detailing market size, growth trends, key drivers, restraints, opportunities, and challenges. It offers in-depth insights into market segmentation, regional dynamics, and the competitive landscape, equipping stakeholders with crucial data for strategic decision-making. The report leverages extensive primary and secondary research to deliver precise forecasts and actionable intelligence, focusing on the period from 2025 to 2033, with historical data from 2019 to 2023.| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 380.5 billion |

| Market Forecast in 2033 | USD 574.9 billion |

| Growth Rate | 5.2% CAGR from 2025 to 2033 |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | WestRock, International Paper, Smurfit Kappa, Mondi, Stora Enso, Packaging Corporation of America, DS Smith, BillerudKorsnas, Graphic Packaging International, Oji Holdings, Nine Dragons Paper, Shanying International, Sonoco Products, Tetra Pak, SIG Combibloc, Huhtamaki, Mayr-Melnhof Karton, Rengo, Cascades, Crown Holdings |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The paper and paperboard container and packaging market is comprehensively segmented to provide a detailed understanding of its diverse applications and material compositions. These segmentations allow for a granular analysis of market dynamics, revealing specific growth drivers and challenges across different product types, material uses, and end-use industries. Understanding these segments is crucial for identifying targeted opportunities and developing tailored market strategies.The key segmentations defining the market include:

- By Product Type: This segment includes a range of paper and paperboard packaging formats, each serving distinct purposes.

- Corrugated Boxes: Widely used for shipping and protective packaging, especially in e-commerce and industrial applications.

- Folding Cartons: Popular for consumer goods, food, and pharmaceuticals due to their printability and structural integrity.

- Liquid Packaging Cartons: Specialized cartons designed for beverages and liquid foods, often with multi-layered structures.

- Paper Bags and Sacks: Used for retail, groceries, and bulk dry goods.

- Other Products: Encompasses a variety of specialized solutions such as molded fiber pulp products for protective cushioning, wraps, and labels.

- By Material Type: The market differentiates between materials based on their origin and environmental impact.

- Virgin Paperboard: Made from fresh wood pulp, often preferred for high-strength or food-contact applications.

- Recycled Paperboard: Produced from recycled paper fibers, highlighting the industry's commitment to circularity and resource efficiency.

- By End-Use Industry: This segmentation highlights the diverse sectors that rely on paper and paperboard packaging.

- Food and Beverage: A major consumer, including sub-segments like Dairy (milk cartons, yogurt cups), Bakery & Confectionery (cake boxes, candy wrappers), Fruits & Vegetables (produce trays, berry containers), Meat, Poultry & Seafood (specialized trays, portion packs), and Others (ready meals, snack foods).

- E-commerce: Driven by the need for robust and presentable shipping packaging.

- Healthcare: For pharmaceutical products, medical devices, and hospital supplies requiring sterile and tamper-evident packaging.

- Personal Care and Cosmetics: Utilizes paperboard for product boxes, tubes, and display packaging due to its aesthetic appeal.

- Consumer Goods: Broad category including electronics, home care products, and various retail items.

- Industrial Packaging: For heavy-duty applications, protective transit, and component packaging.

- Other Industries: Includes textiles, automotive parts, and various light manufacturing sectors.

- By Application: This categorizes packaging based on its role in the product's journey.

- Primary Packaging: The packaging directly enclosing the product (e.g., cereal box).

- Secondary Packaging: Groups primary packages together (e.g., a case of multiple cereal boxes).

- Tertiary Packaging: Used for bulk handling and shipping, protecting secondary packages during transport (e.g., corrugated pallets).

Regional Highlights

The global paper and paperboard container and packaging market exhibits distinct regional dynamics, with specific geographies driving growth based on economic development, regulatory environments, and consumer preferences. Each region contributes uniquely to the overall market landscape, showcasing different strengths and growth catalysts.- Asia Pacific (APAC): This region stands as the undisputed leader in the paper and paperboard packaging market, driven by its massive population, rapid urbanization, and burgeoning manufacturing and e-commerce sectors. Countries like China and India are experiencing explosive growth in consumer goods consumption and online retail, necessitating vast quantities of packaging. The increasing adoption of sustainable practices in Japan and South Korea also contributes to the region's dominance. Low labor costs and robust industrial bases further cement APAC's position as a key production hub.

- Europe: Europe is a mature yet highly innovative market, characterized by stringent environmental regulations and a strong emphasis on sustainability and circular economy principles. The region is at the forefront of developing advanced barrier coatings and fully recyclable paper packaging solutions. Countries such as Germany, the UK, and France are significant consumers, driven by a well-developed retail sector and increasing consumer demand for eco-friendly products. European initiatives to curb plastic waste have significantly boosted the adoption of paper and paperboard alternatives across various industries, from food service to retail.

- North America: This region is a major market propelled by robust e-commerce growth, a high disposable income driving consumer spending, and increasing awareness of sustainable packaging. The United States, in particular, demonstrates substantial demand for corrugated boxes for shipping and folding cartons for processed foods and beverages. Innovations in lightweighting and the development of intelligent packaging solutions are prominent here. Regulatory pressures and corporate sustainability goals are also pushing companies to transition towards paper-based options.

- Latin America: The market in Latin America is witnessing steady growth, primarily influenced by rising urbanization, expanding retail infrastructure, and increasing foreign investment in manufacturing. Countries like Brazil and Mexico are key contributors, driven by a growing middle class and evolving consumer habits that favor packaged goods. While still developing in terms of recycling infrastructure, the region shows increasing receptiveness to sustainable packaging solutions, opening avenues for paper and paperboard expansion, particularly in the food and beverage sector.

- Middle East and Africa (MEA): This region presents emerging opportunities, with growth driven by economic diversification, infrastructure development, and increasing disposable incomes. Countries in the GCC region are investing in logistics and e-commerce, creating demand for shipping and protective packaging. In Africa, rapid population growth and expanding modern retail formats are fueling the need for basic consumer goods packaging. While environmental regulations are still evolving, there is a growing recognition of the need for sustainable practices, indicating future growth potential for paper and paperboard packaging.

Top Key Players:

The market research report covers the analysis of key stake holders of the Paper and Paperboard Container and Packaging Market. Some of the leading players profiled in the report include -- WestRock

- International Paper

- Smurfit Kappa

- Mondi

- Stora Enso

- Packaging Corporation of America

- DS Smith

- BillerudKorsnas

- Graphic Packaging International

- Oji Holdings

- Nine Dragons Paper

- Shanying International

- Sonoco Products

- Tetra Pak

- SIG Combibloc

- Huhtamaki

- Mayr-Melnhof Karton

- Rengo

- Cascades

- Crown Holdings

Frequently Asked Questions:

What is the current market size of paper and paperboard packaging?

The global Paper and Paperboard Container and Packaging Market was valued at USD 380.5 billion in 2025. It is projected to reach USD 574.9 billion by 2033, demonstrating a Compound Annual Growth Rate (CAGR) of 5.2% during the forecast period from 2025 to 2033.What are the main drivers for the growth of paper and paperboard packaging?

The primary drivers include the escalating global demand for sustainable and eco-friendly packaging solutions, the rapid expansion of the e-commerce sector requiring robust and lightweight shipping materials, and increasing governmental regulations and consumer preferences leading to a ban or restriction on single-use plastics.How is sustainability impacting the paper and paperboard packaging market?

Sustainability is a core driver, pushing the market towards biodegradable, compostable, and highly recyclable paper-based solutions. It encourages innovations in material science for improved barrier properties without compromising environmental integrity, and influences consumer purchasing decisions towards more eco-conscious packaging choices.What role does e-commerce play in the paper and paperboard packaging industry?

E-commerce is a significant growth catalyst, generating massive demand for protective, lightweight, and customizable paper and paperboard packaging. This includes corrugated boxes for shipping, folding cartons for product presentation, and innovative designs that enhance both product safety during transit and the unboxing experience for consumers.What are the key trends shaping the future of paper and paperboard packaging?

Key trends include the widespread adoption of smart packaging technologies for traceability and consumer engagement, continuous innovation in barrier coatings to expand applicability, initiatives for lightweighting and material optimization, and the growing demand for highly customized and personalized packaging designs, alongside a strong emphasis on circular economy principles.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted