Osteosynthesi Product Market

Osteosynthesi Product Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704919 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Osteosynthesi Product Market Size

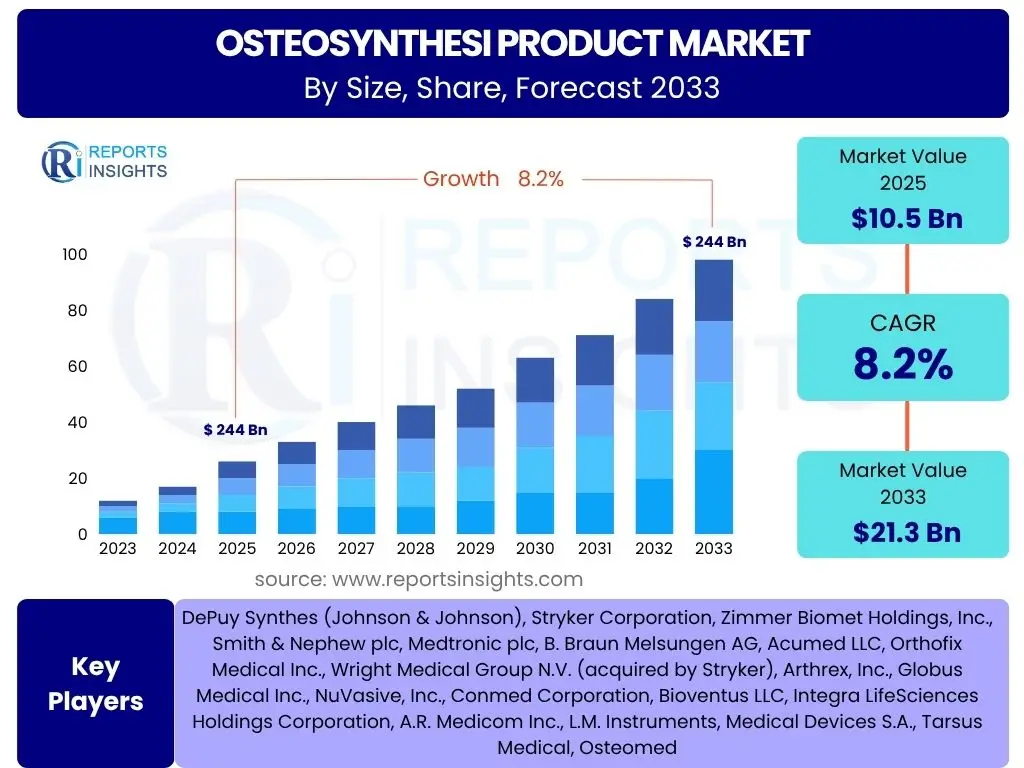

According to Reports Insights Consulting Pvt Ltd, The Osteosynthesi Product Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% between 2025 and 2033. The market is estimated at USD 10.5 billion in 2025 and is projected to reach USD 21.3 billion by the end of the forecast period in 2033.

Key Osteosynthesi Product Market Trends & Insights

Analysis of common user questions reveals significant interest in the evolving landscape of osteosynthesis products, particularly concerning material advancements, surgical techniques, and patient outcomes. There is a strong emphasis on understanding how these products are becoming more patient-specific, less invasive, and more effective in promoting bone healing. Users frequently inquire about the integration of advanced technologies like 3D printing and robotic assistance, as well as the increasing adoption of bioresorbable materials that negate the need for secondary removal surgeries. The demand for products that reduce surgical time and improve post-operative recovery is also a recurring theme.

Furthermore, inquiries often highlight the shift towards personalized medicine within orthopedics, where osteosynthesis solutions are tailored to individual patient anatomy and fracture patterns. The growing awareness and adoption of minimally invasive surgical (MIS) approaches are driving innovation in instrument design and implant geometries. This includes developments in smaller, more precise fixation devices and specialized delivery systems. The convergence of digital planning tools with advanced manufacturing processes is enabling a new era of customized osteosynthesis, addressing complex fracture cases with greater precision and predictability, ultimately leading to improved patient satisfaction and functional recovery.

- Shift towards bioresorbable and biodegradable implants for reduced secondary surgeries.

- Increased adoption of 3D printing for patient-specific and anatomically precise implants.

- Integration of minimally invasive surgical (MIS) techniques and specialized instrumentation.

- Growing application of smart implants with sensor technology for real-time monitoring of healing.

- Emphasis on enhanced surface coatings and biomaterials for improved biocompatibility and osteointegration.

- Expansion of product portfolios to address complex trauma and reconstructive surgeries.

- Development of innovative plating and nailing systems for diverse anatomical sites.

AI Impact Analysis on Osteosynthesi Product

Common user questions regarding AI's impact on osteosynthesis products center on its potential to revolutionize surgical planning, execution, and post-operative care. Users are keen to understand how AI-powered analytics can assist in precise fracture classification, implant selection, and pre-operative simulation, thereby enhancing surgical accuracy and reducing complications. There is also significant curiosity about AI's role in robotic-assisted surgeries, where it can guide instruments with sub-millimeter precision, improving surgical outcomes, especially in complex orthopedic procedures. Furthermore, inquiries highlight the potential for AI to personalize treatment plans based on patient-specific data, leading to more predictable and effective bone healing.

Beyond the operating room, users explore how AI can contribute to the development of next-generation osteosynthesis products by analyzing vast datasets of patient outcomes, material performance, and surgical techniques. This data-driven approach can accelerate the design and optimization of new implants, making them more robust, biocompatible, and tailored to diverse patient populations. AI algorithms are also envisioned to play a role in real-time monitoring of implant stability and bone healing post-surgery, using data from smart implants to alert clinicians to potential issues or provide insights into recovery progress. This integration of AI promises a future where osteosynthesis is not just about mechanical fixation but also about intelligent, adaptive healing solutions.

- AI-enhanced pre-operative planning and surgical simulation for improved precision.

- Robotic-assisted surgery guided by AI algorithms for accurate implant placement.

- Data analytics and machine learning for optimizing implant design and material selection.

- Personalized treatment recommendations based on AI analysis of patient data and historical outcomes.

- Real-time monitoring of bone healing and implant stability using AI-powered smart implants.

- Predictive analytics for identifying patients at higher risk of complications or non-union.

- Streamlined inventory management and supply chain optimization through AI forecasting.

Key Takeaways Osteosynthesi Product Market Size & Forecast

Analysis of common user questions regarding the osteosynthesis product market size and forecast reveals a strong interest in the underlying factors driving growth and the specific segments poised for significant expansion. Users are particularly focused on understanding the sustained demand fueled by an aging global population, the increasing incidence of trauma and sports-related injuries, and advancements in surgical techniques that expand the applicability of these products. There is also a keen interest in identifying which regions will exhibit the most dynamic growth and the role of emerging economies in shaping the future market landscape. The overarching theme is one of consistent expansion driven by both demographic shifts and technological innovation.

A key insight derived from these inquiries is the market's resilience and adaptability, continuously integrating new materials and digital technologies to meet evolving clinical needs. The forecast highlights a robust growth trajectory, underscoring the indispensable role of osteosynthesis products in modern orthopedic and trauma care. Furthermore, the emphasis on personalized medicine and minimally invasive solutions is not just a trend but a fundamental driver that will sustain market expansion, making the market attractive for both established players and new innovators focusing on patient-centric solutions and efficiency in surgical procedures.

- Consistent market growth projected due to aging population and rising trauma cases.

- Technological advancements in materials and surgical techniques are key growth catalysts.

- Significant opportunities in emerging economies due to improving healthcare infrastructure.

- Increased demand for personalized and anatomically specific osteosynthesis solutions.

- Minimally invasive approaches are driving innovation and market adoption.

- Bioabsorbable implants represent a high-growth segment, reducing re-operation rates.

- Digital integration in surgical planning and execution is enhancing market value.

Osteosynthesi Product Market Drivers Analysis

The osteosynthesis product market is primarily driven by a confluence of demographic shifts, increasing incidence of injuries, and continuous technological advancements in orthopedic care. The global aging population is a significant factor, as older individuals are more susceptible to fragility fractures, particularly hip, spine, and wrist fractures, necessitating surgical intervention with osteosynthesis products. Additionally, the rising prevalence of sports-related injuries, road traffic accidents, and occupational hazards across all age groups contributes significantly to the demand for bone fixation devices. These factors collectively create a persistent and growing patient pool requiring orthopedic trauma and reconstructive surgeries, which are highly reliant on effective osteosynthesis solutions.

Technological innovation further propels market growth by enhancing the efficacy, safety, and application range of osteosynthesis products. Advancements in biomaterials, such as titanium alloys with improved biocompatibility and strength, and the development of bioresorbable polymers, are expanding treatment options and improving patient outcomes. The advent of 3D printing allows for the creation of patient-specific implants, addressing complex anatomical challenges with unprecedented precision. Furthermore, the integration of minimally invasive surgical techniques, coupled with specialized instrumentation for osteosynthesis, reduces patient morbidity, shortens hospital stays, and accelerates recovery, making these procedures more appealing and widely adopted. These innovations not only improve clinical outcomes but also drive the replacement and upgrade cycles for existing products, fueling market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Geriatric Population | +0.8% | North America, Europe, Asia Pacific (e.g., Japan, China) | Long-term (2025-2033) |

| Rising Incidence of Trauma and Sports Injuries | +0.7% | Global, particularly developing economies with increasing road accidents | Medium-term to Long-term |

| Technological Advancements in Implant Materials and Design | +0.6% | North America, Europe (R&D hubs) | Medium-term to Long-term |

| Growing Adoption of Minimally Invasive Surgical Techniques | +0.5% | Global, particularly developed healthcare markets | Medium-term |

| Increasing Healthcare Expenditure and Infrastructure Development | +0.4% | Emerging Economies (e.g., China, India, Brazil) | Long-term |

Osteosynthesi Product Market Restraints Analysis

Despite the robust growth prospects, the osteosynthesis product market faces several significant restraints that could impede its expansion. One primary concern is the high cost associated with advanced osteosynthesis products, including premium materials, complex designs, and sophisticated manufacturing processes. This elevated cost can be a barrier to adoption, particularly in healthcare systems with budget constraints or in developing regions where affordability is a major consideration. The cost burden extends beyond the product itself to include surgical procedures, which often require specialized equipment and highly trained personnel, further limiting accessibility for a broader patient base.

Another significant restraint is the stringent regulatory landscape governing medical devices. Osteosynthesis products, being implantable devices, are subject to rigorous testing, clinical trials, and approval processes by regulatory bodies such as the FDA in the US and the EMA in Europe. These processes are time-consuming, expensive, and complex, often delaying market entry for innovative products and increasing research and development costs. Furthermore, product recalls due to manufacturing defects or adverse patient outcomes can severely damage market confidence and incur substantial financial losses for manufacturers. The potential for post-operative complications, such as infection, non-union, or implant failure, also acts as a restraint, influencing patient and physician perception and potentially leading to a cautious approach to new product adoption.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Osteosynthesis Products | -0.6% | Global, particularly emerging markets | Long-term |

| Stringent Regulatory Approval Processes | -0.5% | North America, Europe | Medium-term |

| Risk of Post-operative Complications (e.g., Infection, Non-union) | -0.4% | Global | Long-term |

| Lack of Skilled Surgeons in Certain Regions | -0.3% | Emerging Economies | Long-term |

| Reimbursement Challenges and Healthcare Budget Constraints | -0.2% | Global, particularly public healthcare systems | Medium-term |

Osteosynthesi Product Market Opportunities Analysis

The osteosynthesis product market is ripe with numerous opportunities for growth and innovation, driven by evolving patient needs, technological advancements, and untapped geographic potential. One significant opportunity lies in the burgeoning field of personalized medicine, where custom-designed and 3D-printed implants can address unique patient anatomies and complex fracture patterns more effectively than off-the-shelf solutions. This customization not only promises superior patient outcomes but also opens new revenue streams for manufacturers capable of rapid prototyping and on-demand production. Furthermore, the development of smart implants embedded with sensors offers the potential for real-time monitoring of bone healing, implant stability, and even drug delivery, transforming post-operative care and follow-up.

Another major opportunity exists in expanding market penetration in emerging economies. Countries in Asia Pacific, Latin America, and the Middle East & Africa are experiencing significant improvements in healthcare infrastructure, increasing access to advanced medical treatments, and a growing middle class with higher disposable incomes. These regions represent a vast patient population and an escalating demand for sophisticated orthopedic procedures and products. Manufacturers can capitalize on this by developing cost-effective, high-quality solutions tailored to regional needs and by establishing local manufacturing or distribution partnerships. Additionally, the increasing focus on preventive care and early intervention for musculoskeletal disorders presents opportunities for products that facilitate less invasive procedures and faster recovery, appealing to a broader demographic interested in maintaining active lifestyles.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Patient-Specific and 3D-Printed Implants | +0.9% | Global, particularly developed markets | Medium-term to Long-term |

| Expansion into Emerging Markets (e.g., APAC, LATAM) | +0.8% | Asia Pacific, Latin America, Middle East & Africa | Long-term |

| Innovation in Bioresorbable and Biologically Active Materials | +0.7% | North America, Europe, Key R&D Centers | Medium-term |

| Integration of Smart Technology (Sensors, AI) into Implants | +0.6% | Global, especially tech-forward healthcare systems | Long-term |

| Increasing Demand for Minimally Invasive Solutions | +0.5% | Global | Medium-term |

Osteosynthesi Product Market Challenges Impact Analysis

The osteosynthesis product market faces several inherent challenges that can significantly impact its growth trajectory and operational efficiency. One of the primary challenges is the intense competition among a relatively high number of established players and emerging innovators. This competitive landscape puts constant pressure on pricing, research and development investment, and market differentiation, making it difficult for companies to maintain high profit margins or gain significant market share without continuous innovation. Furthermore, the rapid pace of technological advancements, while an opportunity, also presents a challenge, requiring companies to continuously invest in R&D to remain competitive and ensure their product portfolios are up-to-date with the latest clinical demands and material science breakthroughs. Failure to adapt can lead to product obsolescence and loss of market relevance.

Another significant challenge is navigating the complex and evolving global regulatory environment. As medical device regulations become increasingly stringent, particularly in key markets like the EU (with MDR implementation) and the US, manufacturers face higher costs and longer timelines for product approvals. This complexity can hinder new product introductions and limit market access, especially for smaller companies or those new to the market. Moreover, intellectual property rights and patent protection are crucial in this innovation-driven market; however, defending these rights against infringement can be costly and protracted. The global supply chain disruptions, experienced particularly in recent years, also pose a recurring challenge, affecting the availability of raw materials, manufacturing components, and timely delivery of finished products, which can lead to production delays and impact profitability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition and Pricing Pressure | -0.5% | Global | Long-term |

| Navigating Complex and Evolving Regulatory Landscapes | -0.4% | North America, Europe, Asia Pacific | Medium-term to Long-term |

| High R&D Costs and Need for Continuous Innovation | -0.3% | Global | Long-term |

| Global Supply Chain Disruptions and Raw Material Volatility | -0.2% | Global | Short-term to Medium-term |

| Ethical and Legal Considerations of New Technologies (e.g., AI, 3D printing) | -0.1% | Global | Long-term |

Osteosynthesi Product Market - Updated Report Scope

This comprehensive report provides a detailed analysis of the global osteosynthesis product market, covering market size estimations, historical data from 2019 to 2023, and future projections up to 2033. It thoroughly examines key market trends, growth drivers, formidable restraints, emerging opportunities, and significant challenges impacting the industry. The report also includes an in-depth impact analysis of Artificial Intelligence on the market landscape, offering insights into its transformative potential. Furthermore, it segments the market comprehensively by product type, material, application, and end-user, providing a granular view of market dynamics across key geographical regions, identifying major players, and offering strategic insights for stakeholders. The scope includes a detailed overview of the product landscape, technological advancements, and the competitive environment, facilitating informed decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 10.5 billion |

| Market Forecast in 2033 | USD 21.3 billion |

| Growth Rate | 8.2% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | DePuy Synthes (Johnson & Johnson), Stryker Corporation, Zimmer Biomet Holdings, Inc., Smith & Nephew plc, Medtronic plc, B. Braun Melsungen AG, Acumed LLC, Orthofix Medical Inc., Wright Medical Group N.V. (acquired by Stryker), Arthrex, Inc., Globus Medical Inc., NuVasive, Inc., Conmed Corporation, Bioventus LLC, Integra LifeSciences Holdings Corporation, A.R. Medicom Inc., L.M. Instruments, Medical Devices S.A., Tarsus Medical, Osteomed |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The osteosynthesis product market is extensively segmented to provide a granular understanding of its diverse components and their respective growth dynamics. This segmentation is crucial for identifying specific market niches, understanding competitive landscapes within each category, and pinpointing areas of high growth potential. The market is primarily broken down by product type, encompassing a wide range of fixation devices such as plates, screws, intramedullary nails, wires, pins, and external fixators, each designed for specific fracture patterns and anatomical locations. Further differentiation is made by the materials used in these products, including traditional options like titanium and stainless steel, as well as innovative bioabsorbable polymers and PEEK, reflecting trends towards improved biocompatibility and reduced need for secondary surgeries.

Beyond product and material, the market is segmented by various applications, covering major orthopedic areas like trauma, spine fixation, craniofacial fixation, and dental applications, which highlights the broad utility of osteosynthesis products across different surgical specialties. Finally, segmentation by end-user categories, such as hospitals, ambulatory surgical centers, and specialty clinics, provides insights into the primary consumers of these products and their unique purchasing patterns and infrastructure requirements. This multi-layered segmentation allows for a detailed assessment of market performance, technological adoption rates, and regional preferences, offering a comprehensive view of the osteosynthesis landscape and guiding strategic investment decisions for stakeholders.

- By Product Type: Plates, Screws, Intramedullary Nails, Wires & Pins, External Fixators, Bone Grafts & Substitutes, Others.

- By Material: Titanium Alloys, Stainless Steel, PEEK, Bioabsorbable Materials, Others.

- By Application: Trauma, Spine Fixation, Craniofacial Fixation, Dental Fixation, Veterinary Orthopedics, Deformity Correction, Others.

- By End User: Hospitals, Ambulatory Surgical Centers (ASCs), Orthopedic Clinics, Specialty Trauma Centers.

Regional Highlights

- North America: Dominates the market due to a high incidence of sports injuries and trauma, advanced healthcare infrastructure, high healthcare expenditure, and the presence of major market players and robust R&D activities. Early adoption of advanced technologies like 3D-printed implants and robotic-assisted surgeries further contributes to its leadership.

- Europe: A significant market driven by an aging population, rising orthopedic disorders, and well-established healthcare systems. Countries like Germany, France, and the UK are key contributors, focusing on innovative biomaterials and minimally invasive techniques. Stringent regulatory frameworks also ensure high-quality product standards.

- Asia Pacific (APAC): Expected to exhibit the fastest growth over the forecast period. This growth is attributed to improving healthcare infrastructure, increasing medical tourism, a large patient pool, rising disposable incomes, and growing awareness about advanced orthopedic treatments. China, India, and Japan are at the forefront of this regional expansion, with increasing investments in healthcare facilities and local manufacturing capabilities.

- Latin America: Showing steady growth due to increasing healthcare investments, a growing awareness of modern surgical techniques, and rising incidences of trauma. Countries like Brazil and Mexico are key markets, benefiting from expanding access to medical technologies and a developing healthcare sector.

- Middle East and Africa (MEA): A nascent but rapidly growing market, primarily driven by increasing healthcare expenditure, developing medical infrastructure, and a rise in medical tourism in certain countries. Demand is growing for basic and advanced osteosynthesis products as healthcare access improves across the region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Osteosynthesi Product Market.- DePuy Synthes (Johnson & Johnson)

- Stryker Corporation

- Zimmer Biomet Holdings, Inc.

- Smith & Nephew plc

- Medtronic plc

- B. Braun Melsungen AG

- Acumed LLC

- Orthofix Medical Inc.

- Wright Medical Group N.V. (acquired by Stryker)

- Arthrex, Inc.

- Globus Medical Inc.

- NuVasive, Inc.

- Conmed Corporation

- Bioventus LLC

- Integra LifeSciences Holdings Corporation

- A.R. Medicom Inc.

- L.M. Instruments

- Medical Devices S.A.

- Tarsus Medical

- Osteomed

Frequently Asked Questions

What are osteosynthesis products and what are they used for?

Osteosynthesis products are medical devices, such as plates, screws, nails, and wires, used in orthopedic surgery to stabilize and fix fractured bones, promoting proper healing and alignment. They are essential for treating trauma, correcting deformities, and performing reconstructive surgeries.

How large is the global osteosynthesis product market and what is its growth forecast?

The global osteosynthesis product market is estimated at USD 10.5 billion in 2025 and is projected to reach USD 21.3 billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 8.2% during the forecast period.

What are the latest technological advancements in osteosynthesis products?

Key advancements include the development of bioresorbable implants that dissolve over time, 3D-printed patient-specific devices for precise fit, smart implants with sensors for monitoring, and the integration of AI and robotics for enhanced surgical planning and execution.

Which regions are leading the osteosynthesis product market?

North America currently holds the largest market share due to advanced healthcare infrastructure and high incidence of injuries. Asia Pacific is projected to be the fastest-growing region, driven by improving healthcare access and increasing demand in emerging economies.

What are the primary drivers and restraints impacting the osteosynthesis product market?

The market is driven by an aging global population, rising trauma cases, and technological innovations. Restraints include high product costs, stringent regulatory approval processes, and the risk of post-operative complications.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted