Organic Foundry Binder Market

Organic Foundry Binder Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702778 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Organic Foundry Binder Market Size

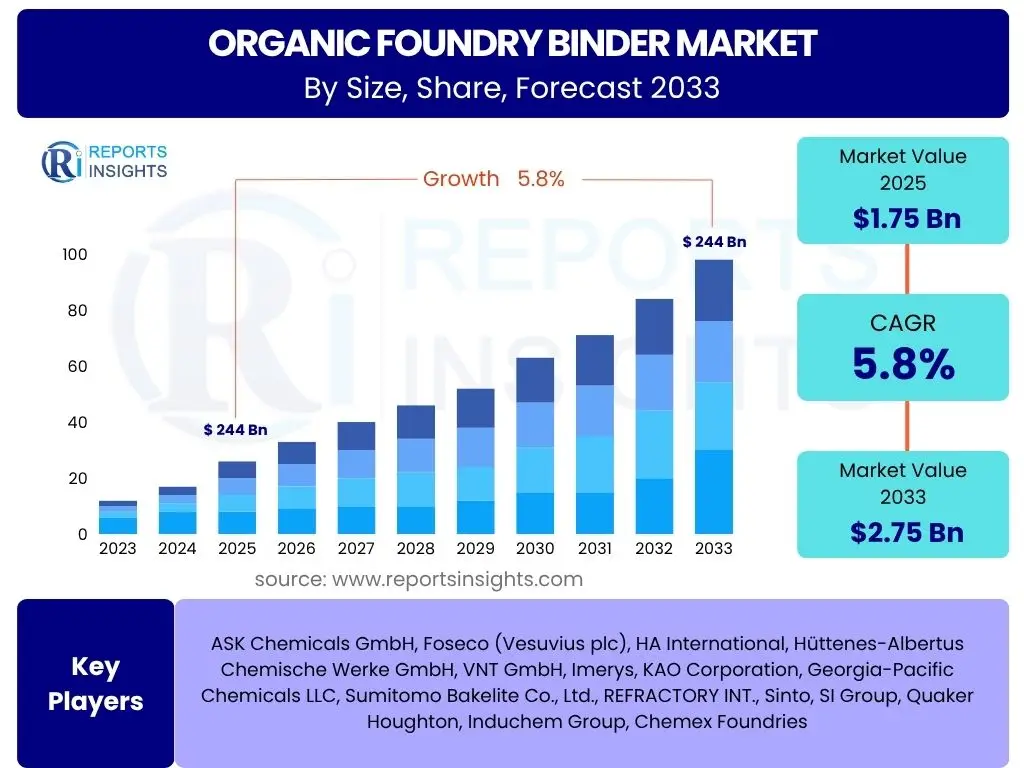

According to Reports Insights Consulting Pvt Ltd, The Organic Foundry Binder Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 1.75 Billion in 2025 and is projected to reach USD 2.75 Billion by the end of the forecast period in 2033.

Key Organic Foundry Binder Market Trends & Insights

User inquiries frequently highlight the evolving landscape of the organic foundry binder market, driven by a confluence of technological advancements, environmental consciousness, and shifting industrial demands. A prominent trend is the increasing focus on developing and adopting eco-friendly and low-emission binder systems, responding to stringent environmental regulations and growing industry commitment to sustainability. This includes binders with reduced volatile organic compound (VOC) emissions and those derived from renewable resources, moving away from traditional hazardous chemicals. The market is also experiencing a surge in demand for high-performance binders capable of producing complex cast geometries with superior dimensional accuracy and surface finish, crucial for applications in the automotive and aerospace sectors.

Furthermore, the automation and digitalization of foundry operations are influencing binder selection, with a preference for binders that facilitate higher production efficiency, faster curing times, and compatibility with advanced molding processes. The globalization of manufacturing and the expansion of automotive and heavy machinery industries in emerging economies are also significant drivers, creating new markets for advanced organic binders. Customization and specialized binder solutions for niche applications, such as lightweighting in vehicles and precision components for electronics, represent another area of growth. The interaction between binder chemistry and sand properties is continually being optimized to enhance casting quality and reduce waste, signifying a mature yet innovative market.

- Shift towards eco-friendly and low-emission binder systems.

- Rising demand for high-performance binders for complex casting.

- Integration with automation and digitalization in foundry processes.

- Growing adoption in emerging automotive and industrial manufacturing hubs.

- Development of specialized binders for advanced material applications.

AI Impact Analysis on Organic Foundry Binder

User queries regarding the impact of Artificial intelligence (AI) on the organic foundry binder sector primarily revolve around efficiency gains, quality improvement, and predictive capabilities within foundry operations. There is significant interest in how AI can optimize binder formulation, leading to enhanced performance and reduced material waste. AI-driven analytics can process vast amounts of data from casting processes, including temperature, pressure, and material composition, to predict the optimal binder-to-sand ratio and curing parameters, thereby minimizing defects and improving yield rates. This data-centric approach also extends to predictive maintenance of foundry equipment, which relies heavily on specific binder properties, ensuring consistent production quality and extending machinery lifespan.

Beyond process optimization, users are keen to understand AI's role in research and development for new binder chemistries. AI and machine learning algorithms can rapidly screen potential new organic compounds and predict their properties, significantly accelerating the discovery and development of novel, sustainable, and high-performance binder systems. Supply chain management for raw materials used in binders is another area where AI is expected to bring substantial benefits, offering predictive insights into price fluctuations and availability, enabling more resilient procurement strategies. The integration of AI tools for quality control, such as automated visual inspection of molds and castings, allows for immediate identification of imperfections related to binder performance, ensuring superior product quality and reducing the need for manual checks.

- Optimization of binder formulation and process parameters for enhanced performance.

- Predictive analytics for defect reduction and yield improvement in casting.

- Accelerated discovery and development of novel binder chemistries through AI-driven R&D.

- Enhanced supply chain resilience for binder raw materials.

- Automated quality control and inspection, improving final product quality.

Key Takeaways Organic Foundry Binder Market Size & Forecast

Common user questions about the Organic Foundry Binder market size and forecast consistently point towards an expectation of sustained growth, driven by fundamental industrial expansion and a concurrent push for sustainability. The market is poised for robust expansion, primarily fueled by increasing global automotive production, growth in industrial machinery manufacturing, and significant infrastructure development, all of which rely heavily on high-quality metal castings. The forecast indicates that while traditional applications will continue to form the bedrock of demand, emerging trends in lightweighting and advanced manufacturing techniques will increasingly influence binder consumption patterns. This suggests a dynamic market where innovation in binder technology, particularly towards environmentally benign solutions, will be a key determinant of market leadership and growth trajectory.

The projected substantial increase in market value reflects not only an expansion in volume but also a premium being placed on specialized and high-performance binder solutions. Geographically, Asia Pacific is expected to remain a dominant force due to its manufacturing prowess, but North America and Europe will also show steady growth, propelled by technological upgrades and strict environmental compliance. The interplay of raw material availability, regulatory frameworks, and technological advancements will shape the market's progression. Stakeholders are keen on understanding how these factors will collectively impact investment decisions, supply chain strategies, and competitive positioning within the forecast period, emphasizing the need for flexible and innovative business models.

- Steady market growth driven by industrial and automotive sector expansion.

- Increased demand for high-performance and environmentally compliant binders.

- Significant market value appreciation reflecting technological advancements.

- Asia Pacific to retain leadership, with stable growth in developed regions.

- Innovation in sustainable binder chemistry will be crucial for market positioning.

Organic Foundry Binder Market Drivers Analysis

The organic foundry binder market is propelled by several robust drivers, primarily stemming from the global growth of key end-use industries. The flourishing automotive sector, particularly the rising production of electric vehicles and lightweight components, necessitates advanced casting technologies and high-performance organic binders to achieve complex geometries and reduce vehicle weight. Concurrently, the expansion of industrial machinery, construction, and infrastructure development worldwide creates a steady demand for high-quality metal castings, directly impacting binder consumption. These industries require reliable and precise castings for engines, structural components, and various equipment, for which organic binders offer superior performance characteristics compared to some inorganic alternatives, especially in terms of strength and mold stability.

Another significant driver is the increasing stringency of environmental regulations regarding emissions and waste disposal in the foundry industry. This pressure compels manufacturers to adopt more eco-friendly organic binder systems that reduce volatile organic compounds (VOCs) and hazardous air pollutants (HAPs), leading to the development of new generations of binders that align with green manufacturing principles. Furthermore, technological advancements in casting processes, such as 3D printing of molds and cores, and the growing complexity of component designs, mandate binders that offer excellent dimensional accuracy, improved surface finish, and adaptability to high-speed production lines. The shift towards higher strength and lighter materials in various applications also encourages the use of advanced organic binders that can withstand demanding casting conditions while contributing to the overall quality and efficiency of the final product.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Automotive Production (especially EVs and Lightweighting) | +1.5% | Asia Pacific, Europe, North America | 2025-2033 |

| Increasing Stringency of Environmental Regulations | +1.2% | Europe, North America, Global | 2025-2033 |

| Expansion of Industrial Machinery and Infrastructure | +1.0% | Asia Pacific, Latin America, Middle East | 2025-2033 |

| Technological Advancements in Casting Processes | +0.8% | Global | 2025-2033 |

| Demand for High-Performance and Precision Castings | +0.7% | Global | 2025-2033 |

Organic Foundry Binder Market Restraints Analysis

Despite robust growth drivers, the organic foundry binder market faces certain restraints that could impede its trajectory. One significant challenge is the volatility of raw material prices. Organic binders are largely derived from petrochemicals, agricultural products, or other specialty chemicals, whose supply and cost are subject to global economic conditions, geopolitical events, and climate impacts. Fluctuations in the prices of key raw materials such as phenolic resins, furfuryl alcohol, and various solvents can directly impact the manufacturing costs of binders, leading to price increases for end-users and potentially slowing down adoption, particularly for smaller foundries operating on thin margins. This unpredictability makes long-term planning and cost management complex for binder manufacturers.

Another restraint is the increasing competition from inorganic binders, which are gaining traction due to their inherently lower emissions and superior thermal stability in certain applications. While organic binders offer excellent performance in many areas, the drive for even stricter environmental compliance and zero-emission foundries could favor the adoption of inorganic alternatives, especially in niche segments. Furthermore, the high initial investment required for sophisticated binder mixing and handling equipment, coupled with the need for specialized training for foundry personnel, can be a deterrent for new entrants or smaller foundries considering an upgrade to advanced organic binder systems. The overall economic slowdowns and disruptions in manufacturing supply chains, such as those witnessed during global health crises, also pose a significant restraint as they directly impact the demand for cast metal components and, consequently, foundry binders.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility | -0.9% | Global | 2025-2033 |

| Competition from Inorganic Binders | -0.7% | Europe, North America | 2025-2033 |

| High Initial Investment & Operational Costs | -0.5% | Emerging Markets | 2025-2030 |

| Regulatory Challenges and Compliance Complexity | -0.4% | Global | 2025-2033 |

Organic Foundry Binder Market Opportunities Analysis

Significant opportunities are emerging within the organic foundry binder market, primarily driven by the ongoing emphasis on sustainability and the evolution of manufacturing technologies. The increasing demand for green and biodegradable binders presents a substantial growth avenue. As industries worldwide commit to reducing their environmental footprint, there is a strong market pull for organic binders derived from renewable resources or those with significantly lower environmental impacts throughout their lifecycle, including reduced emissions during the casting process and easier disposal of spent sand. This trend fosters innovation in bio-based and low-VOC binder formulations, attracting investments in research and development and offering a competitive edge to companies that can meet these evolving sustainability criteria.

Another key opportunity lies in the expanding applications of advanced casting techniques, such as additive manufacturing (3D printing) of molds and cores. While 3D printing often uses binder jetting technologies that require specific binder chemistries, organic binders can be adapted or newly developed to serve this growing segment, enabling the production of highly complex and customized metal components with reduced lead times. The burgeoning growth in emerging economies, particularly in Asia Pacific and Latin America, where industrialization and infrastructure development are accelerating, represents a vast untapped market for foundry products and, by extension, organic binders. These regions are witnessing a surge in automotive, construction, and heavy machinery manufacturing, necessitating the adoption of modern casting practices and materials. Furthermore, the development of specialized organic binders tailored for new alloys and high-performance materials offers niche market penetration, particularly in aerospace, defense, and high-tech electronics sectors where material properties and precision are paramount.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Eco-Friendly and Bio-based Binders | +1.3% | Global | 2025-2033 |

| Growth in Additive Manufacturing (3D Printing) | +1.0% | North America, Europe, Asia Pacific | 2027-2033 |

| Industrialization in Emerging Economies | +0.9% | Asia Pacific, Latin America, Africa | 2025-2033 |

| Demand for Binders in Specialized Alloys/Applications | +0.7% | Global | 2025-2033 |

Organic Foundry Binder Market Challenges Impact Analysis

The organic foundry binder market faces several challenges that require strategic responses from industry players. One significant hurdle is the management and disposal of spent foundry sand, which contains residual binder materials. Environmental regulations are increasingly stringent regarding the landfilling of industrial waste, compelling foundries to invest in costly sand reclamation processes or seek alternative binder systems that facilitate easier and more environmentally sound disposal or recycling. The complexity of these processes and the associated costs can impact the overall profitability of casting operations and influence binder selection, especially for smaller or less capitalized foundries.

Another persistent challenge is maintaining consistent quality and performance of binders across various operational conditions and raw material batches. Slight variations in binder properties can lead to casting defects, increased scrap rates, and production inefficiencies, which directly impact the competitiveness of foundries. Achieving optimal binder performance requires meticulous process control, robust quality assurance, and often, customization for specific casting applications and sand types, which adds to operational complexity. Furthermore, the need for skilled labor capable of handling advanced binder systems and operating sophisticated foundry equipment presents a significant challenge. A shortage of trained professionals can hinder the adoption of new technologies and limit the efficiency gains that modern organic binders are designed to deliver, particularly in regions where industrial skills are in high demand.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Waste Management and Sand Reclamation Costs | -0.8% | Global | 2025-2033 |

| Achieving Consistent Quality and Performance | -0.6% | Global | 2025-2033 |

| Skilled Labor Shortage and Training Requirements | -0.5% | North America, Europe | 2025-2033 |

| Supply Chain Disruptions | -0.4% | Global | 2025-2028 |

Organic Foundry Binder Market - Updated Report Scope

This report offers an in-depth analysis of the global Organic Foundry Binder Market, providing comprehensive insights into its current market size, historical performance, and future growth projections. It meticulously details market trends, drivers, restraints, opportunities, and challenges influencing the industry landscape. The scope includes a thorough segmentation analysis by binder type, application, and end-use industry, alongside a detailed regional breakdown. The report also profiles key market players, offering a competitive landscape overview crucial for strategic decision-making. Its objective is to equip stakeholders with actionable intelligence to navigate market complexities and identify lucrative growth avenues within the forecast period.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.75 Billion |

| Market Forecast in 2033 | USD 2.75 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ASK Chemicals GmbH, Foseco (Vesuvius plc), HA International, Hüttenes-Albertus Chemische Werke GmbH, VNT GmbH, Imerys, KAO Corporation, Georgia-Pacific Chemicals LLC, Sumitomo Bakelite Co., Ltd., REFRACTORY INT., Sinto, SI Group, Quaker Houghton, Induchem Group, Chemex Foundries |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The organic foundry binder market is comprehensively segmented to provide a detailed understanding of its diverse components and their respective contributions to overall market dynamics. This granular analysis allows stakeholders to identify specific growth areas and tailor strategies to capitalize on emerging opportunities within various product categories and end-use applications. The segmentation by type includes various organic binder chemistries, each possessing unique properties and suited for different casting processes, while segmentation by application highlights the key industries driving demand, reflecting the broad utility of metal castings across the global economy. This multi-faceted approach ensures a holistic view of the market's structure.

Further breakdown by end-use industry clarifies the primary consumers of organic foundry binders, encompassing foundries, specialized die-casting companies, and a wide array of metal casting manufacturers catering to diverse sectors. This level of detail is crucial for suppliers to understand the specific needs and performance requirements across different industrial settings, from high-volume automotive component production to precision casting for aerospace. The interplay between these segments, influenced by technological shifts and regulatory demands, shapes the competitive landscape and innovation priorities within the market. Understanding these interdependencies is vital for developing targeted marketing and product development strategies that resonate with the specific demands of each market niche.

- By Type: Cold Box (Phenolic Urethane, Polyol Isocyanate), No-Bake (Phenolic Urethane, Furan, Alkyd Urethane), Shell, Hot Box, Green Sand Binders (Starch, Dextrin).

- By Application: Automotive, Aerospace & Defense, Industrial Machinery, Construction, Energy (Oil & Gas, Power Generation), Marine, Others.

- By End-Use Industry: Foundries, Die Casting Companies, Metal Casting Manufacturers.

Regional Highlights

- North America: Characterized by strong demand from the automotive and aerospace sectors, coupled with increasing adoption of advanced casting technologies and a focus on environmental compliance. Key countries include the United States and Canada, witnessing modernization of foundry facilities.

- Europe: Driven by stringent environmental regulations promoting eco-friendly binder solutions and a robust industrial base in Germany, France, and the UK, focusing on high-precision and specialized castings.

- Asia Pacific (APAC): The largest and fastest-growing market, propelled by rapid industrialization, burgeoning automotive production in China, India, and Japan, and significant infrastructure development across the region.

- Latin America: Exhibits steady growth in countries like Brazil and Mexico, fueled by expanding automotive manufacturing and mining sectors, leading to increased demand for robust industrial castings.

- Middle East and Africa (MEA): Emerging as a growing market due to increasing investments in oil & gas, infrastructure, and diversification of manufacturing sectors in countries like Saudi Arabia and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Organic Foundry Binder Market.- ASK Chemicals GmbH

- Foseco (Vesuvius plc)

- HA International

- Hüttenes-Albertus Chemische Werke GmbH

- VNT GmbH

- Imerys

- KAO Corporation

- Georgia-Pacific Chemicals LLC

- Sumitomo Bakelite Co., Ltd.

- REFRACTORY INT.

- Sinto

- SI Group

- Quaker Houghton

- Induchem Group

- Chemex Foundries

- Wacker Chemie AG

- BASF SE

- Dow Inc.

- Lanxess AG

- Mitsui Chemicals, Inc.

Frequently Asked Questions

Analyze common user questions about the Organic Foundry Binder market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Organic Foundry Binder Market?

The Organic Foundry Binder Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, driven by industrial expansion and technological advancements.

Which factors are primarily driving the demand for organic foundry binders?

Key drivers include the growth in automotive production, increasing industrial machinery manufacturing, stringent environmental regulations promoting eco-friendly solutions, and advancements in casting technologies requiring high-performance binders.

What are the main challenges faced by the Organic Foundry Binder Market?

Major challenges involve managing raw material price volatility, competition from inorganic binders, high initial investment costs for advanced systems, and complexities related to waste management and sand reclamation.

How is AI impacting the Organic Foundry Binder Market?

AI is influencing the market through optimization of binder formulations, predictive analytics for defect reduction, accelerated R&D for new chemistries, improved supply chain resilience, and enhanced automated quality control in foundry operations.

Which regions are expected to dominate the Organic Foundry Binder Market?

Asia Pacific is anticipated to be the largest and fastest-growing market due to significant industrialization, while North America and Europe will also exhibit steady growth driven by technological upgrades and environmental compliance.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted