Organic Fertilizer Market

Organic Fertilizer Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704378 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

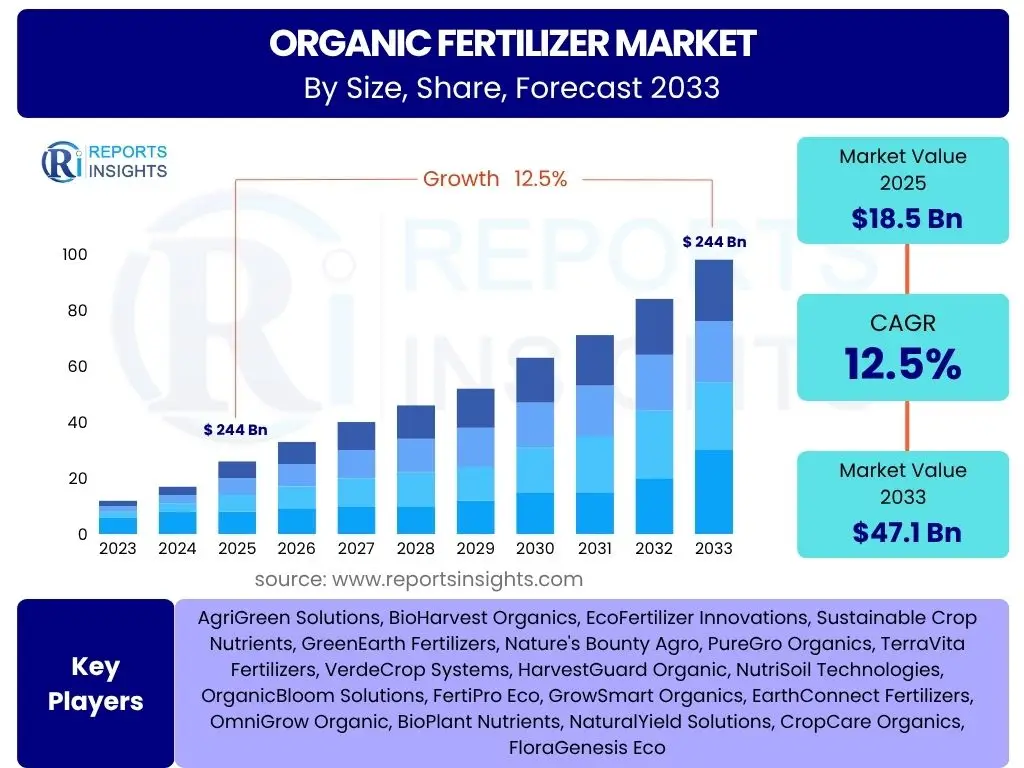

Organic Fertilizer Market Size

According to Reports Insights Consulting Pvt Ltd, The Organic Fertilizer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 47.1 Billion by the end of the forecast period in 2033.

Key Organic Fertilizer Market Trends & Insights

The organic fertilizer market is experiencing significant transformation, driven by a global shift towards sustainable agricultural practices and increasing consumer awareness regarding the environmental and health benefits of organic food. Key trends indicate a robust adoption rate of organic farming methods, spurred by supportive government policies and certifications aimed at promoting ecological balance and soil health. Innovations in bio-based solutions and nutrient delivery systems are also shaping the market, offering more efficient and specialized organic fertilizer options.

A notable insight is the growing emphasis on circular economy principles within the agricultural sector, leading to increased utilization of agricultural waste and by-products for organic fertilizer production. This not only addresses waste management concerns but also provides cost-effective raw materials. Furthermore, the rising demand for diverse organic crop types, including fruits, vegetables, and specialty crops, is diversifying product offerings and driving regional market expansion, particularly in emerging economies where agricultural intensification is a priority.

- Accelerated adoption of sustainable and regenerative agricultural practices globally.

- Rising consumer demand for organic and chemical-free food products.

- Increased governmental support through subsidies, certifications, and favorable regulations for organic farming.

- Technological advancements in organic fertilizer production, including bio-fermentation and nutrient extraction from natural sources.

- Growing focus on soil health restoration and biodiversity preservation.

- Emergence of customized and crop-specific organic fertilizer formulations.

- Integration of circular economy principles, utilizing agricultural and municipal waste for nutrient recovery.

- Expansion of organic farmland areas worldwide, particularly in developing regions.

AI Impact Analysis on Organic Fertilizer

The integration of Artificial Intelligence (AI) in the organic fertilizer sector is poised to revolutionize traditional farming practices by enhancing precision, efficiency, and sustainability. Users frequently inquire about how AI can optimize nutrient application, predict soil health issues, and streamline supply chains for organic products. AI-driven solutions are being developed to analyze vast datasets related to soil composition, climate patterns, and crop nutrient requirements, enabling farmers to make informed decisions regarding organic fertilizer dosage and timing, thereby minimizing waste and maximizing efficacy.

AI's influence extends beyond application to the entire value chain, from raw material sourcing and quality control to product development and market distribution. Predictive analytics powered by AI can forecast demand for specific organic fertilizers, optimize inventory management, and identify potential disruptions in the supply chain, ensuring a consistent and cost-effective supply. Moreover, AI is facilitating the development of advanced organic formulations through intelligent blending and real-time monitoring of microbial activities, addressing key user concerns about the variability and consistency of organic inputs.

- Precision nutrient management through AI-powered soil analysis and predictive analytics, optimizing organic fertilizer application.

- Enhanced crop monitoring and disease detection using AI vision systems, informing targeted organic nutrient strategies.

- Optimization of organic fertilizer blending and formulation processes for improved efficacy and consistency.

- AI-driven supply chain optimization, improving logistics, reducing waste, and ensuring timely delivery of organic inputs.

- Predictive modeling for yield forecasting and resource allocation in organic farming systems.

- Automated quality control and traceability of organic raw materials and finished products.

- Development of smart irrigation systems integrated with organic nutrient delivery for water efficiency.

Key Takeaways Organic Fertilizer Market Size & Forecast

The Organic Fertilizer market is poised for substantial growth over the forecast period, reflecting a significant paradigm shift in global agricultural practices. A key takeaway is the robust Compound Annual Growth Rate (CAGR) projected, primarily driven by escalating environmental consciousness, stringent regulatory frameworks promoting sustainable farming, and an undeniable surge in consumer preference for organic food products. This growth trajectory indicates a resilient market dynamic, capable of overcoming existing challenges such as raw material availability and higher production costs, through innovation and increasing economies of scale.

Furthermore, the market forecast highlights the increasing investment in research and development aimed at producing more efficient, cost-effective, and diverse organic fertilizer formulations. This includes advancements in bio-stimulants, microbial fertilizers, and enhanced compost technologies. The forecast underscores the crucial role of government initiatives and international collaborations in expanding organic farmland and promoting the adoption of organic inputs, making the market not just a niche segment but a core component of future global food security and environmental sustainability strategies.

- The market exhibits a strong growth momentum, indicating a fundamental shift towards sustainable agriculture.

- Environmental and health benefits are primary drivers of market expansion.

- Significant opportunities exist in emerging economies due to increasing population and arable land.

- Technological innovations are crucial for overcoming production challenges and enhancing product efficacy.

- Government policies and support mechanisms play a pivotal role in accelerating market adoption and growth.

- Demand for organic fertilizers is diversified across various crop types, from cereals to high-value fruits and vegetables.

- The market is becoming increasingly competitive, fostering innovation and product differentiation.

Organic Fertilizer Market Drivers Analysis

The organic fertilizer market is primarily driven by a confluence of factors including growing environmental concerns, increasing demand for organic food, and supportive government policies. As global populations become more aware of the detrimental effects of chemical fertilizers on soil health, water quality, and biodiversity, there is a distinct shift towards sustainable agricultural practices. This rising consciousness directly fuels the demand for organic alternatives that are environmentally benign and promote long-term ecological balance.

Furthermore, the expanding global organic food market acts as a significant catalyst. Consumers are increasingly willing to pay a premium for food products that are free from synthetic chemicals, pesticides, and genetically modified organisms, directly correlating with the use of organic inputs like fertilizers. Governments worldwide are also instituting various supportive measures, including subsidies, certification programs, and regulatory frameworks, to encourage organic farming and reduce reliance on synthetic chemicals. These policy interventions not only incentivize farmers to transition to organic methods but also create a stable demand environment for organic fertilizers.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Organic Food | +1.8% | Global, especially North America & Europe | Long-term |

| Increasing Environmental Concerns & Soil Health Degradation | +1.5% | Global | Mid-term to Long-term |

| Supportive Government Regulations & Subsidies for Organic Farming | +1.2% | Europe, North America, parts of Asia Pacific | Mid-term |

| Rising Awareness of Health Benefits of Organic Produce | +1.0% | Developed & Emerging Economies | Short-term to Mid-term |

| Advancements in Organic Farming Technologies | +0.9% | Global | Long-term |

Organic Fertilizer Market Restraints Analysis

Despite significant growth drivers, the organic fertilizer market faces several restraints that could impede its expansion. One primary challenge is the higher production cost associated with organic fertilizers compared to their synthetic counterparts. The processing of organic raw materials, often involving composting, fermentation, or extraction, can be labor-intensive and require specialized infrastructure, which translates to higher unit costs for farmers. This cost disparity can deter conventional farmers from making the transition, especially in regions with limited financial resources or lack of access to subsidies.

Another significant restraint is the limited availability and inconsistent quality of raw materials. Organic fertilizers rely on natural sources such as animal manure, plant residues, and compost, which can vary in nutrient content and availability depending on regional agricultural practices and seasonality. Ensuring a consistent supply of high-quality raw materials at scale remains a logistical hurdle for manufacturers. Furthermore, the slower nutrient release rate of organic fertilizers, while beneficial for long-term soil health, can be perceived as a drawback by farmers seeking immediate crop response, a characteristic often associated with fast-acting chemical fertilizers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Production Cost Compared to Synthetic Fertilizers | -0.8% | Global, especially developing regions | Mid-term |

| Limited and Inconsistent Raw Material Availability | -0.7% | Global | Short-term to Mid-term |

| Slower Nutrient Release Rate | -0.6% | Global | Short-term |

| Lack of Awareness and Education Among Farmers | -0.5% | Asia Pacific, Africa, Latin America | Mid-term |

| Scalability Challenges for Large-Scale Organic Farming | -0.4% | Global | Long-term |

Organic Fertilizer Market Opportunities Analysis

The organic fertilizer market presents numerous opportunities for growth and innovation, particularly through product diversification and expansion into untapped geographical regions. A significant opportunity lies in the development of novel organic formulations, such as bio-stimulants, microbial inoculants, and nutrient-enhanced composts, which can address specific crop needs and soil deficiencies more effectively. These advanced products offer higher efficacy and targeted nutrient delivery, appealing to farmers seeking optimized performance from organic inputs. Furthermore, the integration of advanced technologies like nanotechnology and genetic engineering (for beneficial microbes) holds potential for creating next-generation organic fertilizers with superior characteristics.

Emerging economies, particularly in Asia Pacific and Latin America, represent vast untapped markets with significant agricultural potential and a growing interest in sustainable practices. As these regions experience increasing awareness of environmental issues and a rising middle class demanding organic food, the adoption of organic fertilizers is expected to accelerate. Strategic partnerships between manufacturers, research institutions, and agricultural cooperatives can also unlock new opportunities by facilitating knowledge transfer, improving supply chain efficiencies, and developing region-specific solutions. Additionally, the increasing focus on precision agriculture methodologies opens avenues for integrating organic fertilizers into smart farming systems, enhancing their value proposition for modern agricultural enterprises.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Product Innovation (e.g., bio-stimulants, microbial fertilizers) | +1.3% | Global | Long-term |

| Expansion into Emerging Markets (Asia Pacific, Latin America) | +1.1% | Asia Pacific, Latin America, Africa | Mid-term to Long-term |

| Integration with Precision Agriculture and Smart Farming | +1.0% | North America, Europe, progressive farms globally | Long-term |

| Utilizing Agricultural and Municipal Waste for Production | +0.9% | Global | Mid-term |

| Strategic Partnerships and Collaborations Across Value Chain | +0.8% | Global | Mid-term |

Organic Fertilizer Market Challenges Impact Analysis

The organic fertilizer market, despite its strong growth trajectory, faces several inherent challenges that require innovative solutions. One significant hurdle is ensuring consistent quality and nutrient content across different batches and sources of organic raw materials. Unlike synthetic fertilizers with standardized chemical compositions, the variability in natural ingredients can lead to inconsistencies in product performance, which can be a deterrent for farmers seeking predictable results. Establishing robust quality control mechanisms and industry standards is crucial to build farmer confidence and facilitate broader adoption.

Another major challenge revolves around the scalability of production and the logistics of supply chain management. Producing organic fertilizers at a large scale to meet burgeoning demand requires substantial investment in infrastructure, reliable sourcing of raw materials, and efficient processing technologies. The bulk nature of many organic fertilizers also presents logistical challenges in terms of transportation and storage, especially across vast agricultural regions. Furthermore, competition from well-established and often cheaper synthetic fertilizers, combined with limited awareness among some farming communities about the long-term benefits of organic alternatives, continues to pose a significant barrier to market penetration and expansion.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Quality Control and Standardization Issues | -0.7% | Global | Short-term to Mid-term |

| Scalability of Production and Supply Chain Logistics | -0.6% | Global | Mid-term |

| Competition from Established Synthetic Fertilizers | -0.5% | Global | Long-term |

| Regulatory Complexities and Certification Processes | -0.4% | Specific regions (e.g., EU, US) | Mid-term |

| Perception of Slower Nutrient Availability | -0.3% | Global | Short-term |

Organic Fertilizer Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Organic Fertilizer market, encompassing its current size, historical performance, and future projections. The scope includes a detailed examination of market dynamics such as drivers, restraints, opportunities, and challenges that shape the industry landscape. Furthermore, the report offers extensive segmentation analysis by type, crop type, form, and application, providing granular insights into various market sub-segments. It also highlights regional market trends and competitive landscapes, profiling key players and their strategic initiatives, thus offering a holistic view for stakeholders and industry participants.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 47.1 Billion |

| Growth Rate | 12.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | AgriGreen Solutions, BioHarvest Organics, EcoFertilizer Innovations, Sustainable Crop Nutrients, GreenEarth Fertilizers, Nature's Bounty Agro, PureGro Organics, TerraVita Fertilizers, VerdeCrop Systems, HarvestGuard Organic, NutriSoil Technologies, OrganicBloom Solutions, FertiPro Eco, GrowSmart Organics, EarthConnect Fertilizers, OmniGrow Organic, BioPlant Nutrients, NaturalYield Solutions, CropCare Organics, FloraGenesis Eco |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global organic fertilizer market is comprehensively segmented to provide granular insights into various product categories, application areas, and end-user preferences. This segmentation is crucial for understanding specific market dynamics, identifying niche opportunities, and tailoring product development and marketing strategies. The market is primarily bifurcated by the source of the fertilizer (Type), the specific agricultural produce it is applied to (Crop Type), its physical state (Form), and its end-use environment (Application), each reflecting distinct growth drivers and competitive landscapes.

Analyzing these segments allows stakeholders to pinpoint areas of high growth potential, assess competitive intensity within specific niches, and respond effectively to evolving consumer and agricultural needs. For instance, the demand for plant-based organic fertilizers is rapidly increasing due to the rise of vegan farming and concerns over animal welfare, while the solid form remains dominant for large-scale agricultural applications due to ease of handling. Understanding these distinctions is vital for strategic planning and resource allocation in the diverse organic fertilizer market.

- By Type:

- Plant-based (e.g., Seaweed, Compost, Green Manure)

- Animal-based (e.g., Bone Meal, Blood Meal, Manure)

- Mineral-based (e.g., Rock Phosphate, Gypsum)

- By Crop Type:

- Cereals & Grains

- Fruits & Vegetables

- Oilseeds & Pulses

- Turf & Ornamentals

- Others (e.g., Plantations, Forage)

- By Form:

- Liquid

- Solid (e.g., Pellets, Granules, Powder)

- By Application:

- Farming (Agriculture)

- Gardening (Horticulture, Home Gardens)

- Others (e.g., Nurseries, Landscaping)

Regional Highlights

The global organic fertilizer market exhibits diverse growth patterns across different regions, influenced by varying agricultural practices, regulatory landscapes, and consumer preferences. North America and Europe currently represent significant market shares, primarily driven by early adoption of organic farming, stringent environmental regulations, and a high consumer awareness of organic produce. These regions also benefit from well-established organic food industries and supportive government policies that incentivize sustainable agriculture. The demand in these areas is sustained by an increasing number of certified organic farms and growing investment in organic research and development.

Asia Pacific is projected to be the fastest-growing region, fueled by expanding agricultural land, a burgeoning population with rising disposable incomes, and increasing awareness regarding food safety and environmental impact. Countries like China, India, and Australia are making significant strides in promoting organic farming through national initiatives and subsidies. Latin America also presents considerable growth opportunities, particularly in countries with vast agricultural resources and a growing export market for organic produce. Meanwhile, the Middle East and Africa (MEA) region is showing nascent growth, driven by efforts to diversify agricultural economies and enhance food security through sustainable practices, albeit from a smaller base.

- North America: Leading the market due to high consumer demand for organic food, established organic farming infrastructure, and supportive environmental regulations. Strong adoption of precision organic farming.

- Europe: Characterized by stringent organic certification standards, robust governmental support through Common Agricultural Policy (CAP) reforms, and a mature organic food market. Focus on reducing chemical input.

- Asia Pacific (APAC): Emerging as the fastest-growing region, driven by increasing awareness, growing population, expanding arable land, and government initiatives to promote sustainable agriculture in countries like China, India, and Australia.

- Latin America: Significant growth potential due to abundant agricultural resources, increasing exports of organic produce, and rising domestic demand for healthy food. Countries like Brazil and Argentina are key players.

- Middle East & Africa (MEA): Showing nascent growth, primarily driven by government efforts to enhance food security, diversify agricultural practices, and address desertification and soil degradation challenges.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Organic Fertilizer Market.- AgriGreen Solutions

- BioHarvest Organics

- EcoFertilizer Innovations

- Sustainable Crop Nutrients

- GreenEarth Fertilizers

- Nature's Bounty Agro

- PureGro Organics

- TerraVita Fertilizers

- VerdeCrop Systems

- HarvestGuard Organic

- NutriSoil Technologies

- OrganicBloom Solutions

- FertiPro Eco

- GrowSmart Organics

- EarthConnect Fertilizers

- OmniGrow Organic

- BioPlant Nutrients

- NaturalYield Solutions

- CropCare Organics

- FloraGenesis Eco

Frequently Asked Questions

What is organic fertilizer and how does it differ from chemical fertilizer?

Organic fertilizers are derived from natural sources such as plant residues, animal waste, and minerals, enriching soil fertility through biological processes. They slowly release nutrients, improve soil structure, and support microbial life. In contrast, chemical (synthetic) fertilizers are manufactured from inorganic compounds, provide immediate nutrient release, but can harm soil health and pollute water over time.

Why is organic fertilizer gaining popularity globally?

Organic fertilizer is gaining popularity due to increasing environmental concerns, a rising consumer demand for organic and chemical-free food, and growing awareness of soil degradation issues. Supportive government policies, health benefits associated with organic produce, and advancements in sustainable agriculture also contribute significantly to its widespread adoption.

What are the primary types of organic fertilizers available in the market?

The primary types of organic fertilizers include plant-based sources like compost, seaweed, and green manure; animal-based sources such as bone meal, blood meal, and various manures; and naturally occurring mineral-based options like rock phosphate and gypsum. Each type offers different nutrient profiles and benefits for specific crops and soil conditions.

How large is the global organic fertilizer market, and what is its projected growth?

The global organic fertilizer market was estimated at USD 18.5 Billion in 2025 and is projected to reach USD 47.1 Billion by 2033. It is expected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% during the forecast period, driven by increasing sustainable farming practices and consumer preferences.

What are the key challenges facing the organic fertilizer market?

Key challenges for the organic fertilizer market include the higher production cost compared to synthetic alternatives, inconsistent availability and quality of raw materials, and the slower nutrient release rate of organic products. Additionally, scaling production to meet growing demand and regulatory complexities pose significant hurdles.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted