Operating Room Device Market

Operating Room Device Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_678083 | Last Updated : July 17, 2025 |

Format : ![]()

![]()

![]()

![]()

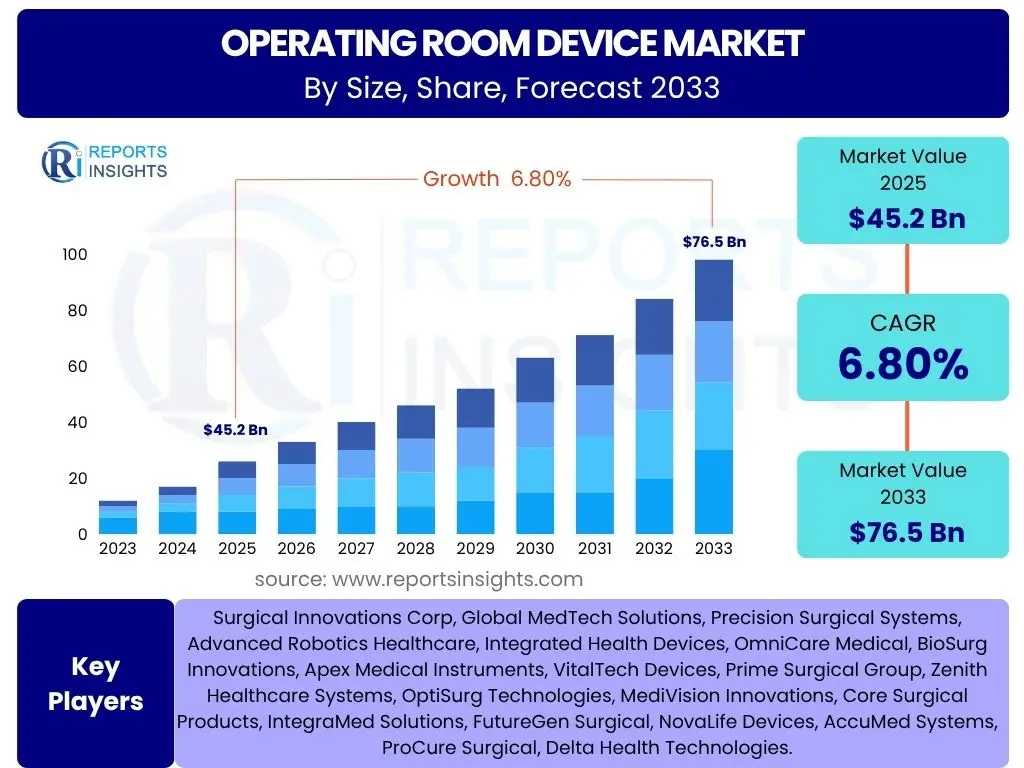

Operating Room Device Market is projected to grow at a Compound annual growth rate (CAGR) of 8.5% between 2025 and 2033, valued at USD 15.2 billion in 2025 and is projected to grow to USD 29.8 billion By 2033 the end of the forecast period.

Key Operating Room Device Market Trends & Insights

The Operating Room Device Market is experiencing dynamic shifts driven by significant technological advancements and evolving healthcare demands. A prominent trend involves the increasing adoption of robotics and automation in surgical procedures, leading to enhanced precision, reduced invasiveness, and faster patient recovery times. Furthermore, the integration of advanced imaging technologies and real-time data analytics is revolutionizing surgical planning and intraoperative guidance, providing surgeons with unprecedented clarity and control. The emphasis on creating integrated and smart operating rooms, leveraging connectivity and IoT devices, is also a key development aimed at optimizing workflow, improving patient safety, and streamlining resource management. This holistic approach ensures that all devices within the OR environment communicate seamlessly, contributing to a more efficient and error-free surgical experience.

Another significant insight revolves around the growing focus on personalized medicine and tailored surgical approaches. As healthcare moves towards more individualized patient care, operating room devices are becoming increasingly adaptable to specific patient anatomies and disease profiles, ensuring better surgical outcomes. The market is also witnessing a surge in demand for minimally invasive surgical instruments and techniques, driven by patient preference for less pain, smaller incisions, and quicker return to daily activities. Moreover, sustainability and environmental considerations are influencing device design and manufacturing, with a push towards reusable components and energy-efficient systems. The expanding geriatric population and the rising prevalence of chronic diseases necessitating surgical interventions further underscore the robust growth trajectory of this market, compelling continuous innovation in operating room technologies to meet diverse and complex healthcare needs.

- Increasing adoption of robotic-assisted surgical systems for enhanced precision.

- Integration of advanced imaging and navigation technologies for improved intraoperative guidance.

- Development of integrated and hybrid operating rooms for seamless workflow.

- Growing demand for minimally invasive surgical devices and techniques.

- Emphasis on patient safety, infection control, and improved surgical outcomes.

- Leveraging IoT and AI for smart OR solutions and predictive analytics.

- Shift towards personalized surgical approaches and customized instrumentation.

- Rising focus on energy efficiency and sustainability in OR device design.

- Expansion of ambulatory surgical centers driving demand for compact and efficient devices.

- Telemedicine and remote assistance capabilities enhancing surgical training and support.

AI Impact Analysis on Operating Room Device

Artificial Intelligence (AI) is rapidly transforming the landscape of operating room devices, fundamentally changing how surgeries are planned, executed, and recovered from. AI algorithms are being integrated into robotic surgical systems to enhance precision, automate repetitive tasks, and provide real-time feedback to surgeons, significantly improving surgical accuracy and reducing the potential for human error. Beyond surgical assistance, AI plays a crucial role in predictive analytics for operating room scheduling and inventory management, optimizing resource utilization and minimizing waste. Furthermore, AI-powered image recognition and analysis capabilities are revolutionizing diagnostics and intraoperative guidance, allowing for more accurate tumor detection, tissue differentiation, and navigation within complex anatomical structures, thereby leading to more effective and safer surgical interventions.

The influence of AI extends to personalized surgical planning, where it can analyze vast amounts of patient data, including medical history, imaging, and genomic information, to create customized surgical strategies. This level of personalization optimizes outcomes and reduces complications. AI also contributes to enhanced patient monitoring during and after surgery, detecting subtle changes in vital signs or physiological parameters that might indicate complications, enabling timely intervention. Moreover, AI-driven simulations and virtual reality training platforms are preparing surgeons for complex procedures, allowing them to practice in a risk-free environment. This continuous innovation, propelled by AI, not only elevates surgical efficacy and patient safety but also paves the way for more efficient and cost-effective healthcare delivery within the operating room environment.

- AI-powered robotic surgical systems enhancing precision and automating tasks.

- Predictive analytics for optimized OR scheduling and resource management.

- Advanced image analysis for real-time surgical guidance and diagnostics.

- Enhanced surgical navigation systems with AI-driven anatomical mapping.

- Automated patient monitoring and early detection of complications.

- Personalized surgical planning based on comprehensive patient data.

- AI-driven simulation and training platforms for surgeons.

- Data analytics for performance optimization and quality improvement in ORs.

Key Takeaways Operating Room Device Market Size & Forecast

- The Operating Room Device Market is poised for substantial growth, projected to nearly double in value by 2033.

- Significant CAGR indicates robust demand driven by technological advancements and healthcare infrastructure development.

- Increasing adoption of minimally invasive surgical procedures is a primary growth catalyst.

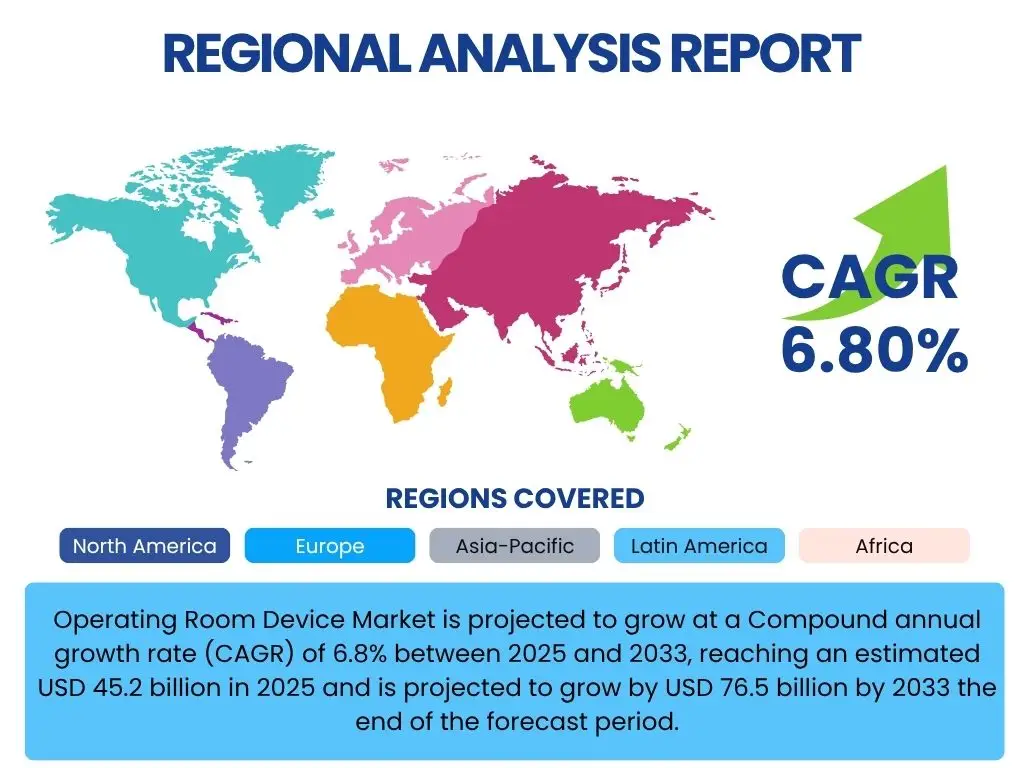

- North America and Europe currently dominate the market due to advanced healthcare systems and high adoption rates.

- Asia Pacific is emerging as the fastest-growing region, fueled by rising healthcare spending and medical tourism.

- Aging global population and increasing prevalence of chronic diseases are key demographic drivers.

- Focus on integrated and smart operating room solutions is transforming traditional OR environments.

- Investment in research and development by market players is accelerating innovation in surgical devices.

- Patient safety, efficiency, and improved outcomes remain central to device development and market expansion.

Operating Room Device Market Drivers Impact Analysis

The Operating Room Device Market is significantly propelled by several key drivers, each contributing to its expansion and innovation. A primary driver is the accelerating pace of technological advancements, particularly in robotics, advanced imaging, and minimally invasive surgical techniques. These innovations enhance surgical precision, reduce recovery times, and improve patient outcomes, making sophisticated OR devices indispensable. The integration of digital technologies, such as Artificial Intelligence and the Internet of Things, further amplifies this impact by enabling smarter, more interconnected operating rooms that optimize workflow and patient care. This continuous evolution in technology not only makes existing procedures safer and more effective but also enables new, less invasive surgical possibilities, directly fueling the demand for advanced operating room equipment.

Another crucial driver is the increasing global prevalence of chronic diseases, coupled with an aging population, both of which necessitate a higher volume of surgical interventions. Conditions such as cardiovascular diseases, orthopedic disorders, and various forms of cancer require complex surgeries, thus driving the demand for specialized operating room devices. Furthermore, the rising healthcare expenditure worldwide, particularly in emerging economies, alongside significant investments in healthcare infrastructure development, provides a conducive environment for market growth. Governments and private healthcare providers are increasingly focusing on improving surgical facilities and adopting advanced technologies to meet the growing patient needs, consequently bolstering the sales and adoption of state-of-the-art operating room equipment across various regions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technological Advancements in Robotics and Imaging | +2.5% | Global, particularly North America, Europe, Asia Pacific (Japan, South Korea) | Short-term to Long-term |

| Increasing Prevalence of Chronic Diseases and Aging Population | +2.0% | Global, significant in developed economies (North America, Europe) | Long-term |

| Growing Demand for Minimally Invasive Surgeries | +1.8% | Global, widespread adoption | Mid-term to Long-term |

| Rising Healthcare Expenditure and Infrastructure Development | +1.5% | Emerging economies (APAC, Latin America, MEA), developing regions | Mid-term to Long-term |

| Emphasis on Patient Safety and Infection Control | +1.2% | Global, particularly critical in hospital settings | Short-term to Mid-term |

| Expansion of Ambulatory Surgical Centers (ASCs) | +1.0% | North America, Europe, expanding in other regions | Mid-term |

| Integration of AI and Digital Health Solutions | +0.5% | Global, particularly in technologically advanced healthcare systems | Short-term to Long-term |

Operating Room Device Market Restraints Impact Analysis

While the Operating Room Device Market demonstrates robust growth, it also faces significant restraints that can impede its full potential. A primary challenge is the remarkably high cost associated with advanced operating room devices, including robotic surgical systems, sophisticated imaging equipment, and integrated OR solutions. These substantial upfront investment costs can be prohibitive for many healthcare facilities, especially smaller hospitals or those in developing regions with limited budgets, thereby restricting widespread adoption. The economic burden is further compounded by the ongoing maintenance expenses, specialized training requirements for staff, and the rapid obsolescence of technology, which necessitates frequent upgrades or replacements, adding to the overall cost of ownership.

Another major restraint involves the stringent regulatory frameworks and lengthy approval processes governing medical devices in various regions. Regulatory bodies, such as the FDA in the United States and the EMA in Europe, impose rigorous testing, clinical trials, and documentation requirements to ensure device safety and efficacy. This complex and time-consuming approval pathway can delay market entry for innovative products, increasing research and development costs for manufacturers. Furthermore, the shortage of skilled professionals capable of operating and maintaining highly specialized OR equipment poses a significant challenge, particularly in regions with limited healthcare training infrastructure. Reimbursement challenges and the risk of device-related complications also add to the constraints, influencing purchasing decisions and market accessibility for advanced operating room technologies.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Operating Room Devices | -1.8% | Global, more pronounced in developing economies and budget-constrained facilities | Long-term |

| Stringent Regulatory Frameworks and Approval Processes | -1.5% | North America, Europe, highly regulated markets | Long-term |

| Shortage of Skilled Healthcare Professionals and Training Needs | -1.2% | Global, particularly in regions with limited medical education infrastructure | Mid-term to Long-term |

| Reimbursement Challenges and Budgetary Constraints for Hospitals | -0.8% | Global, varying impact based on national healthcare policies | Mid-term |

| Risk of Device-Related Infections and Complications | -0.5% | Global, critical concern for patient safety and healthcare costs | Short-term to Mid-term |

Operating Room Device Market Opportunities Impact Analysis

The Operating Room Device Market is ripe with significant opportunities that can drive its expansion and foster innovation. One major opportunity lies in the rapid emergence and increasing adoption of hybrid operating rooms. These advanced surgical suites integrate sophisticated imaging systems (like MRI, CT, and angiography) directly within the OR, allowing for real-time visualization and guidance during complex procedures. This integration facilitates minimally invasive approaches and complex interventions, reducing the need for patient transfers and improving overall surgical precision and outcomes. The demand for such integrated solutions is growing as healthcare facilities strive for higher efficiency and improved patient safety in a single, technologically advanced environment.

Another substantial opportunity is presented by the untapped potential in emerging economies across Asia Pacific, Latin America, and the Middle East and Africa. These regions are witnessing a significant increase in healthcare spending, coupled with a growing awareness of advanced medical treatments and rising patient expectations. As healthcare infrastructure develops and access to medical services expands in these areas, there will be a substantial demand for modern operating room devices. Furthermore, the increasing focus on personalized medicine and precision surgery offers a unique avenue for device manufacturers to develop highly specialized instruments and technologies tailored to individual patient needs. The continuous development of smart operating rooms, leveraging IoT, AI, and connectivity for enhanced workflow and data management, also represents a transformative opportunity for market players to deliver comprehensive, integrated solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Hybrid Operating Rooms | +1.5% | Global, particularly in developed healthcare markets (North America, Europe) | Mid-term to Long-term |

| Development of Smart Operating Rooms (IoT Integration) | +1.2% | Global, driven by technological adoption in healthcare facilities | Short-term to Long-term |

| Untapped Potential in Emerging Economies | +1.0% | Asia Pacific, Latin America, Middle East, and Africa | Long-term |

| Focus on Personalized Medicine and Precision Surgery | +0.8% | Global, driven by advancements in genomics and data analytics | Mid-term to Long-term |

| Growth in Telemedicine and Remote Surgical Assistance | +0.5% | Global, accelerated by digitalization of healthcare | Short-term to Mid-term |

Operating Room Device Market Challenges Impact Analysis

Despite its significant growth prospects, the Operating Room Device Market faces several notable challenges that can influence its trajectory and require strategic navigation. One major challenge is the increasing threat of cybersecurity risks, particularly as operating room devices become more interconnected and integrated with hospital networks. These smart devices, while enhancing efficiency, also present potential vulnerabilities to data breaches, ransomware attacks, or malicious tampering, which could compromise patient data, disrupt surgical procedures, or even endanger patient lives. Ensuring robust cybersecurity protocols and developing secure-by-design devices is paramount, but it adds complexity and cost to device development and deployment.

Another significant challenge revolves around the rapid technological obsolescence inherent in the medical device industry. The swift pace of innovation means that cutting-edge devices can quickly become outdated, necessitating frequent upgrades or replacements for healthcare facilities to maintain optimal performance and remain competitive. This cycle of continuous investment can be financially burdensome for hospitals, especially those with tight budgets, and it complicates long-term purchasing and strategic planning. Furthermore, ethical considerations surrounding the widespread adoption of AI and automation in surgical procedures, along with potential supply chain disruptions impacting the availability of critical components, also represent hurdles that manufacturers and healthcare providers must address to ensure the sustainable growth and responsible deployment of operating room devices.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cybersecurity Risks for Connected Devices | -1.0% | Global, particularly in regions with high digital adoption in healthcare | Short-term to Long-term |

| Rapid Technological Obsolescence | -0.7% | Global, impacting budget allocation and investment cycles for healthcare providers | Mid-term |

| Ethical Considerations Surrounding AI and Automation | -0.5% | Global, influencing public perception and regulatory oversight | Long-term |

| Supply Chain Disruptions and Raw Material Volatility | -0.4% | Global, impacting manufacturing and delivery timelines | Short-term to Mid-term |

| Resistance to Adopting New Technologies due to Training Needs and Workflow Changes | -0.3% | Global, particularly in institutions with limited training resources | Short-term |

Operating Room Device Market - Updated Report Scope

The comprehensive report on the Operating Room Device Market provides an in-depth analysis of market dynamics, growth drivers, restraints, opportunities, and challenges. It covers detailed market segmentation across various types, applications, and end-use industries, alongside a thorough regional analysis to offer a holistic view of the market landscape. The report also includes profiles of key industry players, offering insights into their strategies, product portfolios, and market positioning, providing invaluable intelligence for stakeholders and decision-makers seeking to understand and capitalize on the evolving trends within the global operating room device sector.

| Report Attributes | Report Details |

|---|---|

| Report Name | Operating Room Device Market |

| Market Size in 2025 | USD 15.2 billion |

| Market Forecast in 2033 | USD 29.8 billion |

| Growth Rate | CAGR of 2025 to 2033 8.5% |

| Number of Pages | 250 |

| Key Companies Covered | Stryker Corporation, Hill-Rom Holdings, Skytron, Steris, Dragerwerk, Getinge AB, GE Healthcare, Koninklijke Philips, Smiths Medica, Mizuho OSI, Storz Medical AG |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis

Market Product Type Segmentation:- Surgical Imaging Displays

- Movable Imaging Displays

- Vital Signs Monitoring Devices

- Other

- Hospitals

- Ambulatory Surgical Centers

- Others

Regional Highlights

- North America: This region consistently holds a dominant share in the Operating Room Device Market, primarily due to its advanced healthcare infrastructure, high adoption rates of cutting-edge medical technologies, and significant investments in research and development. The presence of major market players, favorable reimbursement policies, and a high prevalence of chronic diseases also contribute to its leading position. The United States, in particular, is a key market within North America, driven by sophisticated surgical procedures and a strong focus on patient safety and efficiency.

- Europe: Europe represents another significant market for operating room devices, characterized by robust healthcare systems, an aging population, and a strong emphasis on technological innovation. Countries such as Germany, France, and the United Kingdom are at the forefront of adopting advanced surgical technologies, including robotics and integrated OR solutions. Government initiatives to upgrade healthcare facilities and increasing healthcare expenditure further support market growth in this region.

- Asia Pacific (APAC): The Asia Pacific region is projected to exhibit the highest growth rate in the Operating Room Device Market over the forecast period. This rapid expansion is attributed to improving healthcare infrastructure, increasing healthcare spending, a large patient pool, and growing medical tourism. Countries like China, India, Japan, and South Korea are experiencing a surge in demand for advanced surgical equipment as they modernize their healthcare systems and focus on providing high-quality medical care.

- Latin America: This region is experiencing steady growth in the operating room device market, driven by increasing government initiatives to improve healthcare access, rising awareness about advanced surgical treatments, and a growing number of private healthcare investments. Brazil and Mexico are leading countries in this region, with growing medical device imports and a focus on upgrading hospital facilities.

- Middle East and Africa (MEA): The MEA region is also witnessing significant development in its healthcare sector, propelled by increasing oil revenues, government investments in healthcare infrastructure, and a rise in medical tourism, particularly in countries like Saudi Arabia and UAE. The adoption of advanced operating room devices is gradually increasing as these nations strive to provide world-class medical services.

Top Key Players:

The market research report covers the analysis of key stake holders of the Operating Room Device Market. Some of the leading players profiled in the report include -- Stryker Corporation

- Hill-Rom Holdings

- Skytron

- Steris

- Dragerwerk

- Getinge AB

- GE Healthcare

- Koninklijke Philips

- Smiths Medica

- Mizuho OSI

- Storz Medical AG

Frequently Asked Questions:

What is the projected growth rate of the Operating Room Device Market?

The Operating Room Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033, reaching an estimated value of USD 29.8 billion by 2033 from USD 15.2 billion in 2025.

What are the primary drivers of the Operating Room Device Market?

Key drivers include technological advancements in robotics and imaging, the increasing prevalence of chronic diseases and an aging global population, growing demand for minimally invasive surgeries, rising healthcare expenditure, and a strong emphasis on patient safety and infection control.

How is AI impacting the Operating Room Device Market?

AI is transforming the market by enhancing robotic surgical precision, enabling predictive analytics for OR scheduling, providing advanced image analysis for real-time guidance, and supporting personalized surgical planning, leading to improved outcomes and efficiency.

Which regions are leading the Operating Room Device Market?

North America currently leads the Operating Room Device Market due to advanced healthcare infrastructure and high technology adoption. Europe also holds a significant share, while Asia Pacific is emerging as the fastest-growing region owing to developing healthcare systems and increasing investments.

What are the key trends shaping the Operating Room Device Market?

Key trends include the increasing adoption of robotic-assisted surgery, the integration of advanced imaging and navigation technologies, the development of integrated and hybrid operating rooms, a growing demand for minimally invasive procedures, and the leveraging of IoT and AI for smart OR solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted