Open Stack Service Market

Open Stack Service Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702107 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

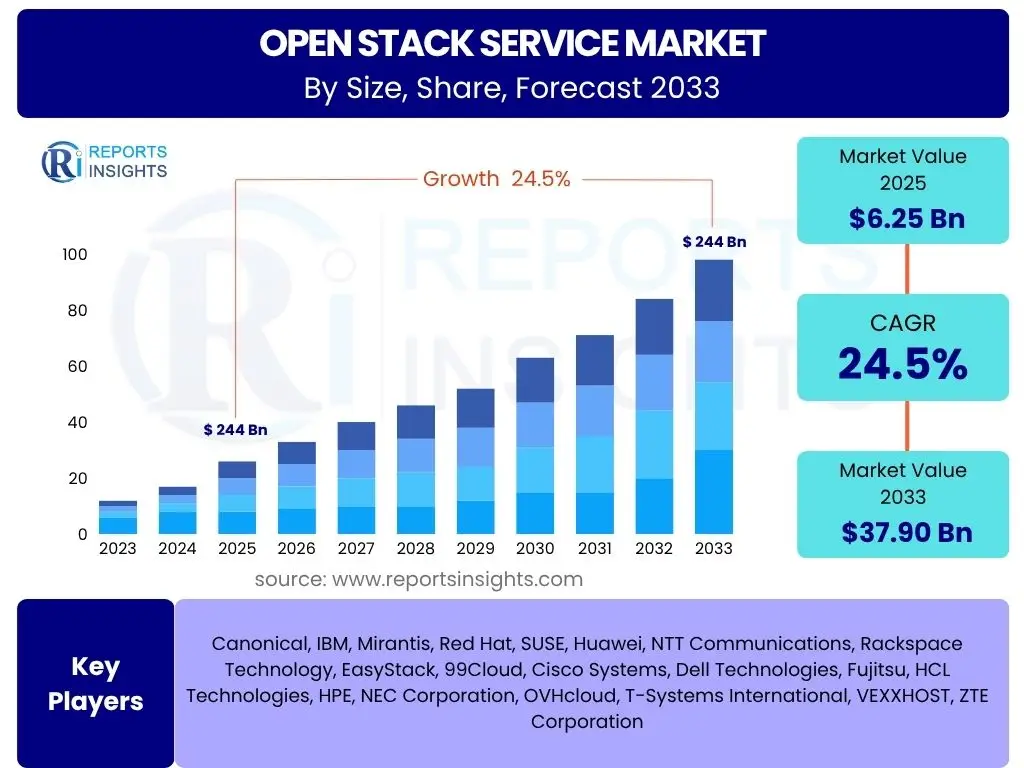

Open Stack Service Market Size

According to Reports Insights Consulting Pvt Ltd, The Open Stack Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 24.5% between 2025 and 2033. The market is estimated at USD 6.25 Billion in 2025 and is projected to reach USD 37.90 Billion by the end of the forecast period in 2033.

Key Open Stack Service Market Trends & Insights

The Open Stack Service market is experiencing significant evolution, driven by the increasing demand for open-source, flexible, and scalable cloud infrastructure. Users frequently inquire about the trajectory of OpenStack adoption, its role in modern IT architectures, and the emerging technologies it integrates with. Current trends indicate a strong shift towards hybrid and multi-cloud strategies, where OpenStack provides the foundational private cloud component. The convergence of containerization technologies, such as Kubernetes, with OpenStack is a prominent trend, enhancing agility and developer productivity. Furthermore, there is a growing emphasis on edge computing deployments, where OpenStack’s distributed architecture proves highly beneficial for managing localized workloads and data processing closer to the source.

Another critical insight is the maturing ecosystem of OpenStack, moving beyond early adoption challenges to offer more robust, enterprise-grade solutions. Managed OpenStack services are gaining traction, addressing the complexity concerns often associated with in-house deployments by providing expertise, support, and automation. This trend allows organizations to leverage the power of OpenStack without the burden of extensive operational overhead. The community-driven nature of OpenStack also ensures continuous innovation and adaptation to new technological demands, including advancements in network function virtualization (NFV) for telecommunications and the integration of artificial intelligence and machine learning (AI/ML) frameworks, positioning OpenStack as a resilient and future-proof cloud platform.

- Accelerated adoption of hybrid and multi-cloud strategies leveraging OpenStack for private cloud components.

- Increased integration of container orchestration platforms like Kubernetes with OpenStack for agile application deployment.

- Rising demand for OpenStack in edge computing environments to process data closer to the source.

- Growth in managed OpenStack services, simplifying deployment and operations for enterprises.

- Continuous evolution of OpenStack's features to support advanced workloads such as Network Function Virtualization (NFV) and Artificial Intelligence/Machine Learning (AI/ML).

AI Impact Analysis on Open Stack Service

User inquiries about AI's impact on Open Stack Service primarily revolve around how OpenStack can support AI workloads, the integration of AI tools, and the benefits of running AI on an open-source cloud platform. The analysis reveals that Artificial Intelligence profoundly influences the Open Stack Service market by driving demand for scalable, high-performance computing infrastructure capable of handling data-intensive AI and Machine Learning (ML) operations. OpenStack's ability to orchestrate virtual machines, bare metal servers, and containerized environments makes it an ideal platform for deploying and managing AI model training and inference workloads, especially those requiring GPU acceleration. The flexibility and customizability of OpenStack allow organizations to build bespoke AI platforms tailored to their specific data governance and compliance requirements.

Furthermore, AI is not only a workload for OpenStack but also a tool to enhance its operations. AI-driven analytics can optimize resource allocation, predict potential infrastructure failures, and automate routine management tasks within OpenStack environments, leading to improved efficiency and reduced operational costs. The open-source nature of OpenStack fosters community collaboration in developing AI-specific services and integrations, such as specialized images for popular AI frameworks or tools for managing large datasets required for ML. This synergy positions OpenStack as a robust, agile, and cost-effective foundation for developing and deploying a wide range of AI applications, from intelligent automation to advanced data analytics, thereby expanding its utility and market reach within the enterprise and research sectors.

- Increased demand for OpenStack infrastructure to host and manage resource-intensive AI and Machine Learning (ML) workloads, including GPU orchestration.

- Development of AI-driven operational tools within OpenStack for enhanced resource optimization, predictive analytics, and automated infrastructure management.

- Facilitation of customized AI model training and inference environments due to OpenStack's flexibility and control over underlying hardware.

- Growth of specialized OpenStack services and integrations catering to AI development frameworks and big data processing needs.

- Positioning of OpenStack as a cost-effective and agile platform for organizations building private and hybrid cloud AI solutions.

Key Takeaways Open Stack Service Market Size & Forecast

Common user questions regarding key takeaways from the Open Stack Service market size and forecast often focus on understanding the market's long-term viability, its strategic importance for enterprises, and the primary drivers of its projected growth. The market insights reveal a robust and sustained growth trajectory for Open Stack Service, driven by the increasing global emphasis on digital transformation, cloud-native application development, and the strategic advantages of open-source technologies. The substantial projected growth from USD 6.25 Billion in 2025 to USD 37.90 Billion by 2033 underscores OpenStack's critical role as a foundational platform for private, hybrid, and multi-cloud environments, signifying its transition from an emerging technology to a mature enterprise solution.

A significant takeaway is that organizations are increasingly valuing the flexibility, cost-effectiveness, and avoidance of vendor lock-in offered by OpenStack, making it a preferred choice for building scalable and customizable cloud infrastructures. The forecast also highlights the growing importance of managed services, which mitigate complexity and skill gap challenges, thus broadening OpenStack's appeal to a wider range of enterprises, including those with limited in-house expertise. This indicates that while the core OpenStack technology continues to evolve, the services layer around it is crucial for unlocking its full market potential, enabling businesses to focus on innovation rather than infrastructure management.

- The Open Stack Service market demonstrates significant and sustained growth, projected at a 24.5% CAGR, indicating strong enterprise adoption.

- OpenStack is cementing its position as a vital component for private, hybrid, and multi-cloud strategies due to its flexibility and open-source nature.

- Managed OpenStack services are crucial enablers, addressing operational complexities and expanding market reach to diverse organizations.

- The market's expansion is fueled by the strategic advantages of cost-effectiveness, customization, and vendor lock-in avoidance.

- OpenStack's adaptability to emerging technologies like AI/ML, edge computing, and containerization ensures its long-term relevance and market value.

Open Stack Service Market Drivers Analysis

The Open Stack Service market is significantly propelled by several key drivers that reflect evolving enterprise IT needs and strategic priorities. Foremost among these is the escalating demand for hybrid and multi-cloud architectures, where OpenStack provides a robust and customizable platform for private cloud components, ensuring seamless integration with public cloud services. The inherent cost-effectiveness of open-source solutions, combined with the avoidance of vendor lock-in, presents a compelling value proposition for organizations seeking greater control and flexibility over their cloud infrastructure. These factors empower businesses to optimize their IT spending while retaining the agility to adapt to changing technological landscapes.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Adoption of Hybrid and Multi-Cloud Strategies | +1.8% | Global | 2025-2033 |

| Cost-Effectiveness and Avoidance of Vendor Lock-in | +1.5% | Global | 2025-2033 |

| Growing Demand for Open-Source Infrastructure | +1.2% | North America, Europe, APAC | 2025-2030 |

| Rise of Containerization and DevOps Methodologies | +1.0% | Global | 2025-2033 |

| Expansion of Edge Computing Deployments | +0.9% | North America, Europe, Asia Pacific | 2028-2033 |

Open Stack Service Market Restraints Analysis

Despite its significant growth potential, the Open Stack Service market faces several restraints that could temper its expansion. A primary challenge is the perceived complexity associated with deploying, managing, and maintaining OpenStack environments, which often requires specialized technical expertise. This complexity can deter organizations, particularly small and medium-sized enterprises (SMEs), from adopting OpenStack. Additionally, the intense competition from established public cloud providers, who offer fully managed and often simpler-to-consume cloud services, poses a significant hurdle. These providers leverage extensive global infrastructure and comprehensive service portfolios, making them a default choice for many businesses seeking immediate cloud solutions without the overhead of infrastructure management.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Perceived Complexity of Deployment and Management | -1.2% | Global | 2025-2030 |

| Intense Competition from Public Cloud Providers | -1.0% | Global | 2025-2033 |

| Shortage of Skilled OpenStack Professionals | -0.8% | Global | 2025-2033 |

| Security and Compliance Concerns for Private Clouds | -0.5% | Europe, North America | 2025-2030 |

| High Initial Investment and Operational Overhead | -0.4% | Emerging Markets | 2025-2028 |

Open Stack Service Market Opportunities Analysis

The Open Stack Service market is ripe with opportunities that can significantly accelerate its growth trajectory. The proliferation of edge computing and 5G infrastructure presents a substantial avenue for OpenStack, as its distributed architecture is well-suited for managing localized data processing and network functions at the edge. This allows for low-latency applications and efficient data handling in a rapidly expanding digital landscape. Moreover, the increasing adoption of AI and Machine Learning (ML) workloads, which require scalable and customized infrastructure, creates a strong demand for OpenStack's flexible resource orchestration capabilities. Organizations are looking for platforms that can efficiently support demanding AI training and inference, and OpenStack provides the control and performance needed.

Another significant opportunity lies in the burgeoning market for managed OpenStack services. As the complexity of operating OpenStack can be a barrier, third-party providers offering comprehensive managed solutions can alleviate operational burdens for enterprises, making OpenStack more accessible to a broader range of organizations. Additionally, government initiatives and policies promoting open-source technologies for digital sovereignty and secure national cloud infrastructures create a favorable environment for OpenStack adoption. These opportunities, combined with the continuous evolution of the OpenStack platform to integrate with new technologies like serverless computing and advanced networking, position the market for sustained expansion by addressing critical emerging needs.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Edge Computing and 5G Infrastructure | +1.5% | Global | 2026-2033 |

| Increasing Demand for AI/ML Workload Support | +1.3% | North America, Asia Pacific | 2025-2033 |

| Growth of Managed OpenStack Services Market | +1.0% | Global | 2025-2030 |

| Government and Public Sector Initiatives for Open Source | +0.8% | Europe, Asia Pacific, Latin America | 2025-2033 |

| Strategic Partnerships and Ecosystem Development | +0.6% | Global | 2025-2033 |

Open Stack Service Market Challenges Impact Analysis

The Open Stack Service market encounters several significant challenges that could impede its growth, requiring strategic responses from service providers and the community. One persistent challenge is the complexity and steep learning curve associated with deploying, configuring, and managing OpenStack, which often necessitates a highly skilled workforce that is in short supply. This talent gap can lead to higher operational costs and slower adoption rates, particularly for organizations lacking dedicated internal teams. Furthermore, achieving seamless interoperability with diverse legacy systems and various public cloud offerings remains a hurdle. While OpenStack promotes flexibility, integrating it into existing heterogeneous IT environments can be a complex and time-consuming process, impacting overall project timelines and budgets.

Another critical challenge is the potential for fragmentation within the OpenStack ecosystem due to the sheer number of projects and diverse vendor implementations. While beneficial for customization, this can sometimes lead to compatibility issues and make it difficult for users to navigate the landscape and choose optimal solutions. Maintaining long-term support and updates for specific OpenStack distributions can also be a concern for enterprises reliant on stable, predictable environments. Addressing these challenges requires continuous efforts in simplifying OpenStack deployment tools, enhancing training and certification programs, fostering stronger interoperability standards, and promoting cohesive community development to ensure the platform remains accessible, reliable, and competitive against proprietary cloud alternatives.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity and Requirement for Specialized Expertise | -1.5% | Global | 2025-2033 |

| Interoperability with Existing IT Infrastructure and Public Clouds | -1.0% | Global | 2025-2030 |

| Ecosystem Fragmentation and Version Management | -0.7% | Global | 2025-2033 |

| Data Security and Compliance in Hybrid Environments | -0.5% | Europe, North America | 2025-2030 |

| Perception of Open Source Support and Reliability | -0.3% | Global | 2025-2028 |

Open Stack Service Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Open Stack Service Market, covering historical trends, current market dynamics, and future projections from 2025 to 2033. It offers critical insights into market size, growth drivers, restraints, opportunities, and challenges, along with detailed segmentation analysis and regional breakdowns. The report also includes a thorough examination of the competitive landscape, profiling key market players to provide a holistic view of the industry. This extensive scope is designed to assist stakeholders in making informed strategic decisions and understanding the evolving nature of the OpenStack ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.25 Billion |

| Market Forecast in 2033 | USD 37.90 Billion |

| Growth Rate | 24.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Canonical, IBM, Mirantis, Red Hat, SUSE, Huawei, NTT Communications, Rackspace Technology, EasyStack, 99Cloud, Cisco Systems, Dell Technologies, Fujitsu, HCL Technologies, HPE, NEC Corporation, OVHcloud, T-Systems International, VEXXHOST, ZTE Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Open Stack Service market is meticulously segmented across various dimensions to provide a granular understanding of its components and growth pockets. This detailed segmentation enables a precise analysis of specific service types, deployment models, organization sizes, and industry verticals, highlighting unique market dynamics and opportunities within each category. Understanding these segments is crucial for stakeholders to identify niche markets, tailor service offerings, and develop targeted strategies that align with specific customer needs and industry demands, thereby maximizing market penetration and revenue potential across the diverse OpenStack ecosystem.

- By Service Type:

- Consulting Services: Strategic guidance for OpenStack implementation and optimization.

- Integration Services: Facilitating seamless integration of OpenStack with existing IT infrastructure.

- Support and Maintenance Services: Ongoing technical assistance and operational continuity for OpenStack environments.

- Managed Services: Comprehensive outsourced management of OpenStack cloud infrastructure.

- Professional Services: Customized solutions including development, training, and specialized project support.

- By Deployment Model:

- Public Cloud: OpenStack services offered by third-party providers over the public internet.

- Private Cloud: OpenStack deployed exclusively for a single organization, either on-premises or hosted by a third party.

- Hybrid Cloud: A combination of private and public OpenStack environments working together.

- By Organization Size:

- Small and Medium-sized Enterprises (SMEs): Businesses with limited IT resources seeking managed OpenStack solutions.

- Large Enterprises: Corporations requiring scalable, customizable, and high-performance OpenStack deployments for complex workloads.

- By Industry Vertical:

- IT and Telecommunications: Key adopters for NFV, network infrastructure, and application hosting.

- Banking, Financial Services, and Insurance (BFSI): Driven by data security, compliance, and hybrid cloud needs.

- Retail and E-commerce: For scalable backend infrastructure and robust customer experience platforms.

- Healthcare and Life Sciences: For secure data management, research computing, and compliance-driven cloud.

- Manufacturing: For IoT, industrial automation, and edge computing applications.

- Government and Defense: For data sovereignty, secure private clouds, and specialized computing.

- Education: For research environments, virtual labs, and institutional IT infrastructure.

- Media and Entertainment: For content delivery, rendering, and streaming services requiring high scalability.

- Others: Including energy, utilities, transportation, and logistics.

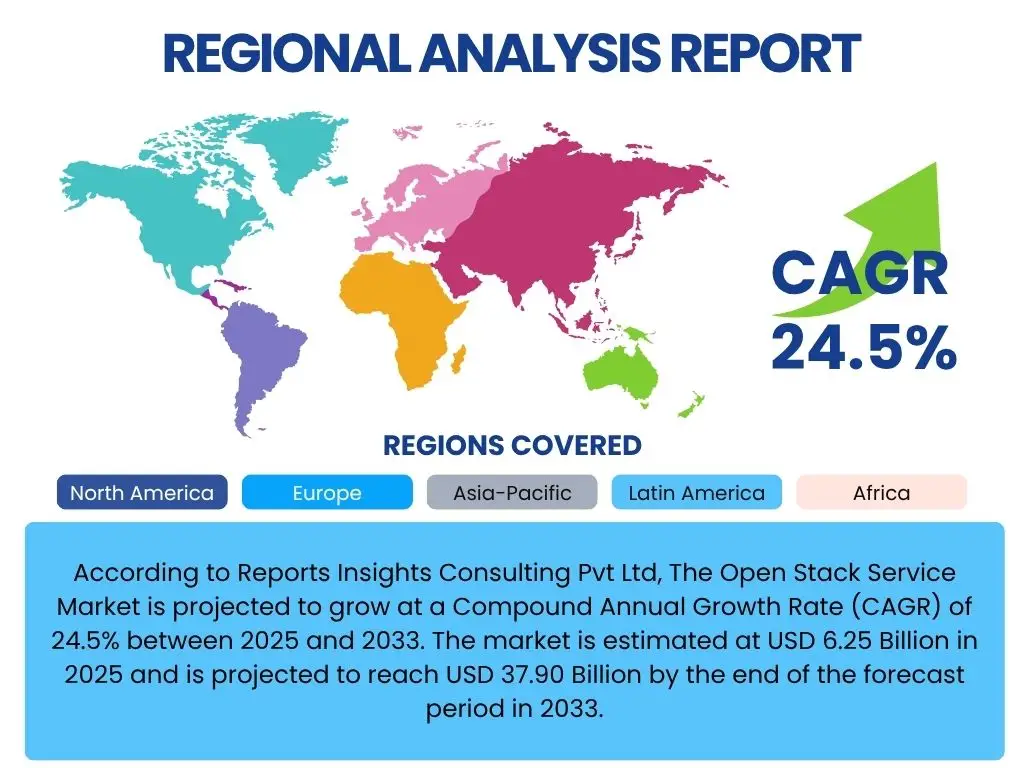

Regional Highlights

- North America: This region is a leading market for Open Stack Service, driven by early adoption of cloud technologies, significant investments in digital transformation, and a strong presence of key technology providers and large enterprises. The demand for hybrid cloud solutions and the push for open-source alternatives to proprietary systems are significant factors. High levels of technological innovation and a robust ecosystem for IT infrastructure development further propel market growth.

- Europe: Europe represents a substantial market for Open Stack Service, particularly influenced by stringent data sovereignty regulations (such as GDPR) and a growing emphasis on building sovereign cloud capabilities. Countries like Germany, the UK, and France are actively investing in open-source solutions to reduce dependency on non-European cloud providers. The region also sees increasing adoption in the telecommunications sector for NFV deployments and private cloud initiatives in government and banking sectors.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region in the Open Stack Service market due to rapid digitalization across industries, burgeoning IT infrastructure development, and increasing enterprise cloud adoption in countries like China, India, and Japan. The need for scalable and cost-effective cloud solutions for a large and diverse market, coupled with significant investments in 5G and edge computing, positions APAC as a high-potential growth area.

- Latin America: This region is experiencing steady growth, fueled by rising internet penetration, increasing investments in IT infrastructure, and a growing awareness of the benefits of open-source technologies. Countries like Brazil and Mexico are seeing higher adoption rates, particularly among small and medium-sized businesses looking for flexible and economical cloud solutions to support their digital growth initiatives.

- Middle East and Africa (MEA): The MEA region is emerging as a promising market for Open Stack Service, driven by government-led digital transformation agendas, smart city initiatives, and diversification efforts away from oil-dependent economies. Significant investments in data centers and cloud infrastructure, particularly in countries like UAE, Saudi Arabia, and South Africa, are creating opportunities for OpenStack deployments in both private and hybrid cloud models.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Open Stack Service Market.- Canonical

- IBM

- Mirantis

- Red Hat

- SUSE

- Huawei

- NTT Communications

- Rackspace Technology

- EasyStack

- 99Cloud

- Cisco Systems

- Dell Technologies

- Fujitsu

- HCL Technologies

- HPE

- NEC Corporation

- OVHcloud

- T-Systems International

- VEXXHOST

- ZTE Corporation

Frequently Asked Questions

Analyze common user questions about the Open Stack Service market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is OpenStack Service?

OpenStack service refers to the provision, management, and support of cloud computing infrastructure built on the open-source OpenStack platform. It encompasses a range of offerings including consulting, integration, managed services, and technical support, enabling organizations to deploy and operate private, public, or hybrid cloud environments using OpenStack software components for compute, storage, networking, and other cloud resources.

Why should organizations use OpenStack services?

Organizations utilize OpenStack services to gain the benefits of an open-source cloud platform without the complexities of in-house management. Key advantages include avoiding vendor lock-in, significant cost savings compared to proprietary cloud solutions, enhanced flexibility and customization capabilities, robust security controls for private environments, and the ability to build scalable infrastructure tailored to specific business needs, supported by expert professional services.

Who are the primary users or industries adopting OpenStack services?

OpenStack services are primarily adopted by large enterprises, telecommunications providers, government agencies, and research institutions. Industries such as IT and Telecom, BFSI, Retail, Healthcare, and Manufacturing increasingly leverage OpenStack for their private and hybrid cloud strategies, demanding scalable, secure, and customizable infrastructure for critical workloads, including Network Function Virtualization (NFV), big data analytics, and Artificial Intelligence (AI) applications.

What are the main benefits of using OpenStack for cloud infrastructure?

The main benefits of using OpenStack for cloud infrastructure include unparalleled flexibility and customization, allowing organizations to build clouds precisely to their specifications. It offers significant cost efficiency due to its open-source nature, eliminating licensing fees and reducing operational expenses. Furthermore, OpenStack promotes vendor neutrality, preventing reliance on a single provider, and provides robust control over data security and compliance, especially for sensitive workloads and hybrid cloud strategies.

How does OpenStack compare to public cloud platforms like AWS or Azure?

OpenStack differs from public cloud platforms like AWS or Azure by primarily serving as an open-source software stack for building private and hybrid cloud environments, offering organizations complete control over their infrastructure and data. While public clouds provide readily available, fully managed services with a pay-as-you-go model, OpenStack enables greater customization, cost optimization for large-scale private deployments, and avoidance of vendor lock-in. OpenStack services bridge the gap by providing expert support and management, making its capabilities accessible without the extensive operational burden.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted