Online Grocery Service Market

Online Grocery Service Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707083 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

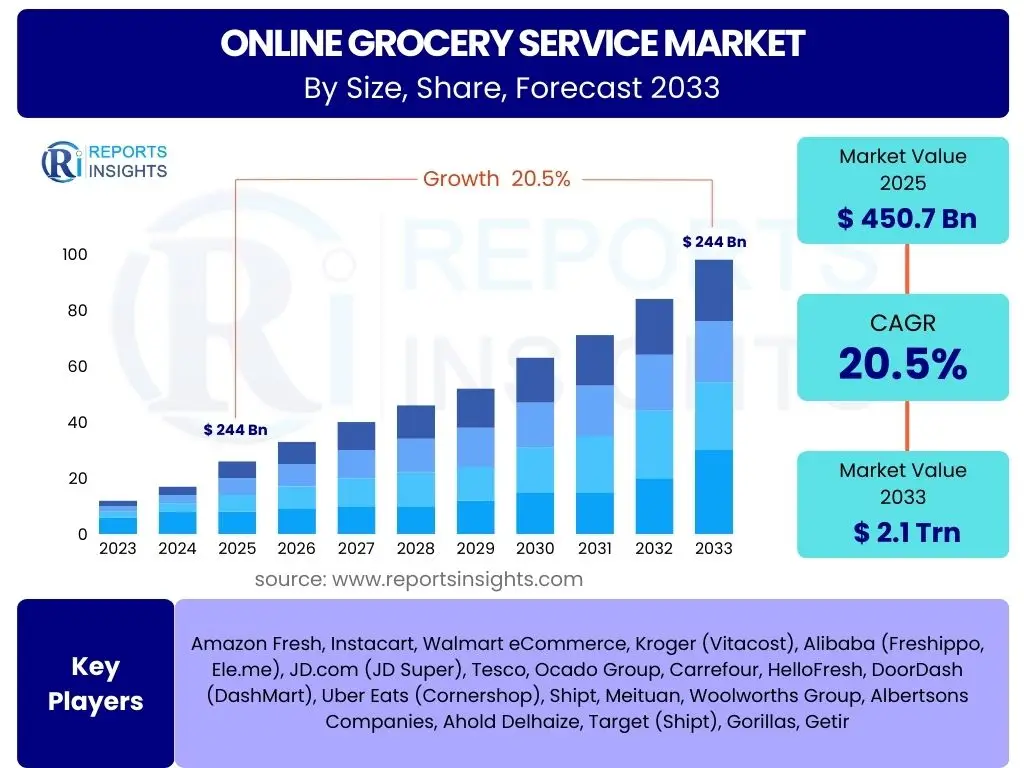

Online Grocery Service Market Size

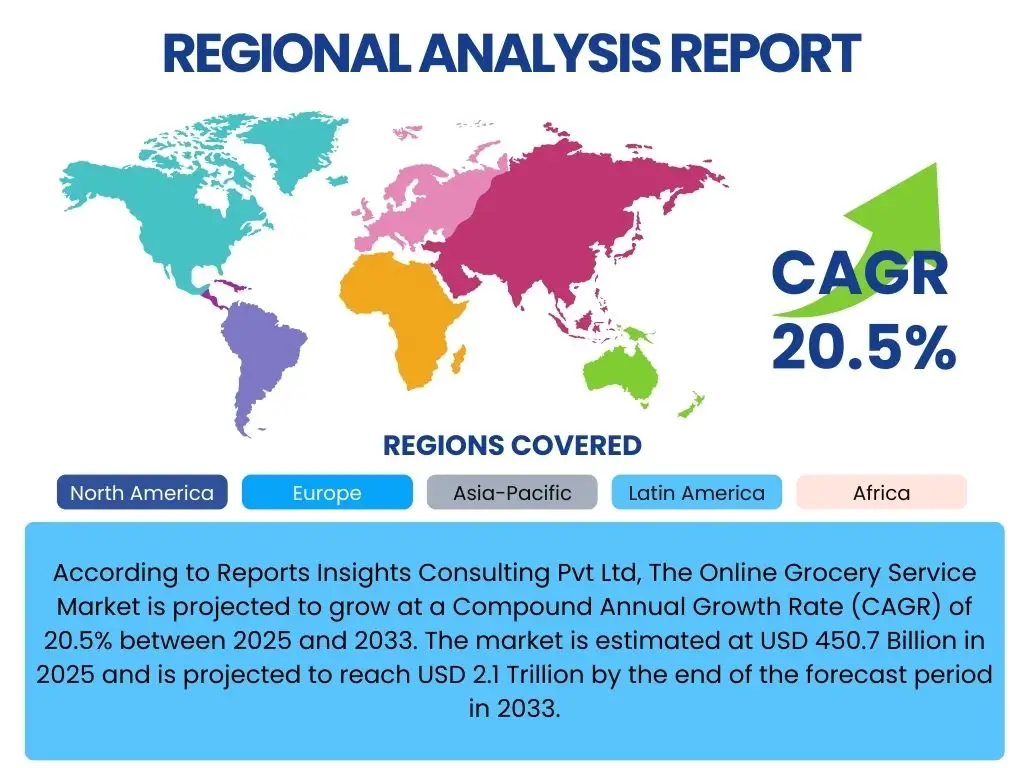

According to Reports Insights Consulting Pvt Ltd, The Online Grocery Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 20.5% between 2025 and 2033. The market is estimated at USD 450.7 Billion in 2025 and is projected to reach USD 2.1 Trillion by the end of the forecast period in 2033.

Key Online Grocery Service Market Trends & Insights

User queries frequently center on the evolving landscape of online grocery services, seeking information on innovations, consumer behavior shifts, and technological adoptions. The market is currently experiencing rapid transformation driven by consumer demand for convenience, speed, and personalized experiences, alongside significant advancements in logistics and digital platforms. Key trends indicate a move towards more efficient delivery models, greater integration of technology, and a focus on niche markets and sustainable practices.

The increasing penetration of smartphones and widespread internet access globally are foundational drivers, enabling broader adoption of online grocery platforms. Furthermore, the expansion of product categories beyond fresh produce to include meal kits, specialty foods, and non-food household items reflects a diversification strategy by service providers. This holistic approach aims to capture a larger share of household spending and solidify consumer loyalty by becoming a one-stop solution for diverse needs.

- Hyper-personalization of shopping experiences using AI and data analytics.

- Expansion of quick commerce (q-commerce) for ultra-fast deliveries.

- Growth of subscription-based models for recurring grocery needs.

- Increased focus on sustainable packaging and ethical sourcing.

- Rise of 'dark stores' and automated fulfillment centers for efficiency.

- Integration of augmented reality (AR) for virtual product inspection.

- Diversification into non-grocery categories like household goods and electronics.

AI Impact Analysis on Online Grocery Service

Common user questions regarding AI's influence on online grocery services often revolve around its applications in improving efficiency, personalizing customer experiences, and optimizing supply chains. There is significant interest in how AI can address logistical challenges, reduce food waste, and provide more intuitive shopping interfaces. Users are also keen to understand the balance between AI-driven automation and the need for human touchpoints in customer service and quality control.

AI is fundamentally reshaping the operational backbone and customer-facing aspects of the online grocery sector. From predictive analytics guiding inventory management to sophisticated recommendation engines enhancing the shopping journey, its applications are diverse and impactful. The ability of AI to process vast amounts of data allows for unprecedented levels of efficiency and customization, addressing long-standing challenges related to perishable goods, fluctuating demand, and complex delivery networks. As AI capabilities mature, its role in automating last-mile delivery and ensuring product freshness through optimized logistics is becoming increasingly vital.

- Personalized Recommendations: AI analyzes past purchases and browsing behavior to suggest relevant products, increasing basket size and customer satisfaction.

- Demand Forecasting: Predictive AI models anticipate consumer demand, optimizing inventory levels and reducing food waste.

- Route Optimization: AI algorithms determine the most efficient delivery routes, cutting fuel costs and delivery times.

- Automated Warehousing: AI-powered robots and automation systems improve the speed and accuracy of order fulfillment in dark stores and distribution centers.

- Customer Service Chatbots: AI-driven chatbots handle routine inquiries, providing instant support and freeing up human agents for complex issues.

- Quality Control: AI-powered vision systems can inspect produce for freshness and quality before delivery.

- Dynamic Pricing: AI adjusts product prices in real-time based on supply, demand, and competitor pricing.

Key Takeaways Online Grocery Service Market Size & Forecast

User inquiries about key takeaways from the online grocery service market size and forecast consistently highlight the sector's robust growth trajectory and its increasing significance in the global retail landscape. Insights sought often include understanding the primary drivers of this expansion, the enduring impact of recent global events, and the factors poised to sustain this momentum into the next decade. The overriding sentiment is a recognition of online grocery not as a temporary trend, but as a fundamental shift in consumer purchasing habits and retail infrastructure.

The market is poised for significant expansion, transitioning from a niche convenience to a mainstream retail channel. The projected multi-trillion dollar valuation by 2033 underscores a profound transformation in how consumers acquire their groceries. This growth is underpinned by continuous innovation in delivery models, technological integration, and an expanding geographical footprint. The adaptability of online grocery platforms to cater to diverse consumer needs, from same-day delivery to specialized dietary options, will be crucial for sustained growth and market leadership.

- The Online Grocery Service Market is experiencing exponential growth, projected to reach USD 2.1 Trillion by 2033.

- Digital transformation, urbanization, and convenience-driven consumer preferences are core growth enablers.

- Technology integration, particularly AI and automation, is critical for operational efficiency and customer experience.

- Market expansion is global, with strong growth anticipated across North America, Asia Pacific, and Europe.

- Diversification of services, including quick commerce and subscription models, will define future competitive landscapes.

- Sustainability initiatives and ethical sourcing are emerging as significant differentiators for service providers.

Online Grocery Service Market Drivers Analysis

The online grocery service market is fundamentally driven by shifts in consumer lifestyles and technological advancements. The increasing demand for convenience, particularly among urban populations and dual-income households, has spurred the adoption of online platforms that eliminate the need for physical store visits. This convenience extends to time savings, reduced travel, and the ability to shop anytime, anywhere. Furthermore, the enhanced digital literacy across various demographics, coupled with widespread smartphone penetration, provides the necessary technological infrastructure for seamless online transactions and order management, making online grocery services accessible to a broader consumer base.

The expansion of internet connectivity, especially in emerging economies, is unlocking new customer segments, further fueling market growth. Beyond convenience, the ability of online platforms to offer a wider product assortment than many physical stores, including niche, organic, or international products, caters to diverse consumer preferences. The enduring impact of global health crises has also accelerated the shift towards online channels, solidifying new purchasing habits. Service providers are continually innovating their delivery models, including same-day and express delivery options, to meet consumer expectations for speed, thereby reinforcing the appeal of online grocery.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Internet & Smartphone Penetration | +3.5% | Global, especially APAC, Latin America | Long-term (2025-2033) |

| Growing Demand for Convenience & Time-Saving | +2.8% | North America, Europe, Urban APAC | Ongoing (2025-2033) |

| Urbanization & Changing Lifestyles | +2.2% | Global, particularly developing economies | Long-term (2025-2033) |

| Wider Product Selection & Niche Offerings | +1.9% | Global | Medium-term (2025-2029) |

| Advancements in Logistics & Delivery Models | +1.5% | Global | Ongoing (2025-2033) |

| Rising Disposable Incomes & Digital Adoption | +1.0% | APAC, Latin America, MEA | Long-term (2025-2033) |

Online Grocery Service Market Restraints Analysis

Despite the robust growth, the online grocery service market faces several significant restraints that can impede its full potential. A primary concern for consumers is the perceived lack of control over product quality and freshness, particularly for perishable items like fruits, vegetables, and meats. Unlike in-store shopping where consumers can handpick items, online orders rely on the judgment of pickers, leading to potential dissatisfaction. This trust deficit can be a major barrier to widespread adoption, especially among demographics accustomed to traditional shopping methods.

Another substantial restraint is the complexity and cost associated with cold chain logistics and last-mile delivery. Maintaining optimal temperatures for perishable goods throughout the supply chain, from warehouse to doorstep, is expensive and operationally challenging. The cost of labor for picking and delivery, coupled with vehicle maintenance and fuel, often results in higher overall operational costs for online providers, which can translate into higher prices or delivery fees for consumers, making the service less attractive compared to traditional grocery shopping. Moreover, intense competition and price sensitivity in the grocery sector further compress profit margins, making it difficult for online players to sustain operations without significant capital investment.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Concerns over Product Freshness & Quality | -2.0% | Global | Ongoing (2025-2033) |

| High Delivery Costs & Logistics Complexity | -1.8% | Global, especially dense urban areas | Long-term (2025-2033) |

| Lack of Physical Product Interaction | -1.5% | Global, varying by demographic | Ongoing (2025-2033) |

| Intense Competition & Price Sensitivity | -1.2% | Global, highly competitive markets | Ongoing (2025-2033) |

| Cybersecurity & Data Privacy Concerns | -0.8% | Global | Medium-term (2025-2029) |

| Limited Availability in Rural Areas | -0.5% | Developing regions, rural areas in developed countries | Long-term (2025-2033) |

Online Grocery Service Market Opportunities Analysis

The online grocery service market is ripe with opportunities for expansion and innovation, particularly through geographical penetration and service diversification. Untapped rural markets and smaller towns present significant growth potential as internet infrastructure improves and consumer awareness increases beyond major metropolitan areas. Furthermore, the development of localized supply chains, supporting regional farmers and producers, can resonate with consumer demand for fresh, ethically sourced, and locally produced goods, thereby creating a unique value proposition and fostering community ties.

Technological integration, especially with Artificial Intelligence and Machine Learning, offers extensive avenues for enhancing operational efficiencies and customer satisfaction. This includes advanced demand forecasting, personalized marketing, and highly optimized delivery routes that can significantly reduce costs and environmental impact. The development of innovative delivery models, such as autonomous vehicles, drone delivery in specific zones, and partnerships with local businesses for pickup points, can revolutionize last-mile logistics. Moreover, expanding service offerings beyond groceries to include household essentials, ready-to-eat meals, and even pharmacy items, positions online platforms as comprehensive lifestyle solutions, capturing a larger share of consumer spending and building stronger customer loyalty through convenience and breadth of selection.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Untapped Rural & Tier-2 Markets | +2.5% | APAC, Latin America, parts of MEA | Long-term (2025-2033) |

| Integration of AI/ML for Personalization & Efficiency | +2.0% | Global | Ongoing (2025-2033) |

| Development of Subscription Models & Loyalty Programs | +1.8% | North America, Europe, Urban APAC | Medium-term (2025-2029) |

| Focus on Sustainable & Ethical Sourcing/Delivery | +1.5% | Europe, North America | Long-term (2025-2033) |

| Strategic Partnerships with Local Retailers & Farms | +1.2% | Global, varying by local market dynamics | Medium-term (2025-2029) |

| Leveraging Dark Stores & Micro-fulfillment Centers | +0.8% | Dense urban areas globally | Short-term (2025-2027) |

Online Grocery Service Market Challenges Impact Analysis

The online grocery service market is not without its significant challenges, which require strategic foresight and substantial investment to overcome. Ensuring profitability remains a core hurdle, primarily due to the high operational costs associated with picking, packing, and especially last-mile delivery. The narrow margins inherent in the grocery retail sector mean that inefficiencies in logistics or customer acquisition can severely impact a company's bottom line. Additionally, managing the supply chain for perishable goods, with varying shelf lives and specific storage requirements, presents a complex logistical challenge that traditional retail models often handle with greater ease.

Intense competition from both established retail giants transitioning online and agile start-ups continually pressures pricing and service innovation. This competitive landscape necessitates continuous investment in technology, marketing, and infrastructure, straining financial resources. Furthermore, attracting and retaining skilled labor for picking, packing, and delivery, particularly in a gig-economy model, poses challenges related to wages, benefits, and worker satisfaction. Regulatory complexities, including food safety standards, labor laws, and data privacy regulations, also add layers of operational and compliance challenges that can vary significantly by region, requiring robust legal and operational frameworks to navigate effectively.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Profitability in High-Cost Operations | -2.2% | Global | Long-term (2025-2033) |

| Managing Complex Cold Chain Logistics | -1.7% | Global | Ongoing (2025-2033) |

| Intense Competition & Market Saturation | -1.5% | Developed markets (North America, Europe) | Ongoing (2025-2033) |

| Customer Acquisition & Retention Costs | -1.0% | Global | Medium-term (2025-2029) |

| Labor Shortages & Retention in Delivery Roles | -0.8% | North America, Europe | Short-term (2025-2027) |

| Data Security & Privacy Compliance | -0.5% | Europe (GDPR), North America, APAC | Ongoing (2025-2033) |

Online Grocery Service Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Online Grocery Service Market, offering insights into its current state, historical performance, and future growth projections. The scope includes a detailed examination of market size, key trends, drivers, restraints, opportunities, and challenges influencing the industry's trajectory. It also features a thorough segmentation analysis across various parameters and highlights regional market dynamics, identifying key growth regions and countries.

The report incorporates an assessment of AI's transformative impact on the sector, from enhancing operational efficiencies to revolutionizing customer experiences. Strategic profiles of leading market players are included to provide competitive intelligence and understand market positioning. Designed to equip stakeholders with actionable intelligence, this document serves as a vital resource for strategic planning, investment decisions, and market entry strategies within the rapidly evolving online grocery landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 450.7 Billion |

| Market Forecast in 2033 | USD 2.1 Trillion |

| Growth Rate | 20.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amazon Fresh, Instacart, Walmart eCommerce, Kroger (Vitacost), Alibaba (Freshippo, Ele.me), JD.com (JD Super), Tesco, Ocado Group, Carrefour, HelloFresh, DoorDash (DashMart), Uber Eats (Cornershop), Shipt, Meituan, Woolworths Group, Albertsons Companies, Ahold Delhaize, Target (Shipt), Gorillas, Getir |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The online grocery service market is meticulously segmented to provide a granular understanding of its diverse facets and varying consumer behaviors. These segments help in identifying specific growth areas, understanding competitive dynamics within niches, and tailoring business strategies to particular market demands. Segmentation by product type reveals preferences for fresh vs. packaged goods, while delivery models highlight the consumer's choice between scheduled convenience and immediate gratification. Platform type further indicates the dominance of mobile-first shopping experiences, reflecting broader digital consumption trends.

Payment methods reveal consumer trust and preferred transaction modes, while age-group segmentation offers insights into generational adoption patterns and spending habits. Each segment plays a crucial role in defining the overall market landscape, enabling businesses to focus their resources on the most promising areas. Understanding these segmentations is paramount for market players to develop targeted marketing campaigns, optimize service offerings, and ensure sustained relevance in a rapidly evolving digital retail environment.

- By Product Type:

- Fresh Produce (Fruits, Vegetables, Meat & Seafood)

- Packaged Foods

- Beverages

- Household & Personal Care Products

- Dairy & Bakery

- Others

- By Delivery Model:

- Pick-up (Curbside Pick-up, In-store Pick-up)

- Home Delivery (Scheduled Delivery, Express Delivery/Quick Commerce)

- By Platform Type:

- Websites/Desktop

- Mobile Applications

- By Payment Method:

- Online Payment (Credit/Debit Card, Net Banking, Mobile Wallets)

- Cash on Delivery

- By Consumer Age Group:

- Gen Z

- Millennials

- Gen X

- Baby Boomers

Regional Highlights

- North America: A mature market characterized by high digital penetration and strong consumer adoption of online services. The region benefits from established infrastructure, robust e-commerce ecosystems, and a high concentration of key players, with a growing emphasis on convenience-driven models like quick commerce and subscription services.

- Europe: Exhibits diverse market dynamics across countries, with Western European nations showing high adoption rates driven by urbanization and digital literacy. Southern and Eastern Europe are rapidly catching up, fueled by increasing internet penetration and rising disposable incomes. Regulatory considerations and sustainability initiatives are particularly impactful here.

- Asia Pacific (APAC): The fastest-growing region, propelled by large populations, rapid urbanization, increasing smartphone penetration, and a burgeoning middle class. Countries like China and India are leading the charge with innovative mobile-first strategies and expansive delivery networks. Localized solutions and competitive pricing are critical success factors.

- Latin America: An emerging market with significant growth potential, driven by expanding e-commerce infrastructure, increasing internet access, and a youthful, tech-savvy population. Challenges include logistical complexities and varying economic stability, but opportunities abound in urban centers.

- Middle East and Africa (MEA): A nascent but promising market, experiencing growth due to increasing urbanization, digital transformation initiatives, and a young demographic. Investment in logistics and last-mile delivery infrastructure is crucial for unlocking the region's full potential, especially in GCC countries and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Online Grocery Service Market.- Amazon Fresh

- Instacart

- Walmart eCommerce

- Kroger (Vitacost)

- Alibaba (Freshippo, Ele.me)

- JD.com (JD Super)

- Tesco

- Ocado Group

- Carrefour

- HelloFresh

- DoorDash (DashMart)

- Uber Eats (Cornershop)

- Shipt

- Meituan

- Woolworths Group

- Albertsons Companies

- Ahold Delhaize

- Target (Shipt)

- Gorillas

- Getir

Frequently Asked Questions

Analyze common user questions about the Online Grocery Service market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate for the Online Grocery Service Market?

The Online Grocery Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 20.5% between 2025 and 2033.

What are the primary drivers of growth in the Online Grocery Service Market?

Key drivers include increasing internet and smartphone penetration, growing demand for convenience, urbanization, and advancements in logistics and delivery models.

How is AI impacting the Online Grocery Service sector?

AI significantly impacts online grocery through personalized recommendations, optimized demand forecasting, efficient route planning, automated warehousing, and enhanced customer service via chatbots.

What are the main challenges faced by online grocery service providers?

Major challenges include achieving profitability amidst high operational costs, managing complex cold chain logistics for perishable goods, intense market competition, and securing skilled labor for delivery.

Which regions are expected to show the most significant growth in the online grocery market?

The Asia Pacific (APAC) region is expected to exhibit the fastest growth, followed by North America and Europe, driven by increasing digital adoption and consumer demand.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted