Oncology Market

Oncology Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703866 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Oncology Market Size

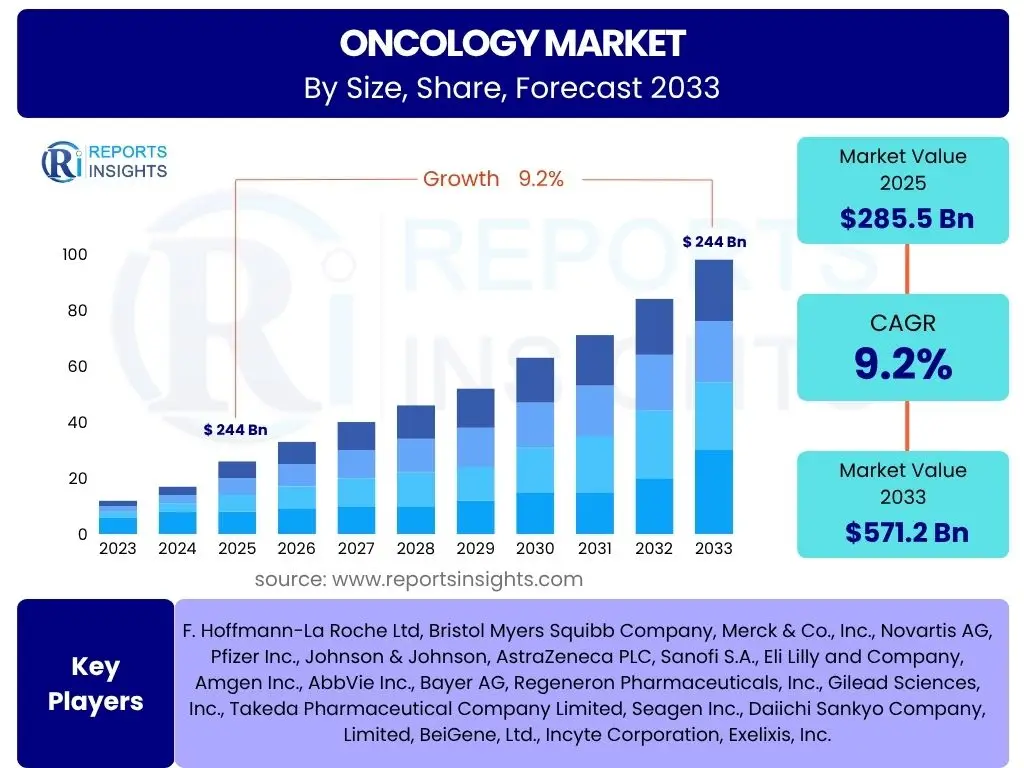

According to Reports Insights Consulting Pvt Ltd, The Oncology Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.2% between 2025 and 2033. The market is estimated at USD 285.5 Billion in 2025 and is projected to reach USD 571.2 Billion by the end of the forecast period in 2033.

Key Oncology Market Trends & Insights

The oncology market is currently shaped by a confluence of transformative trends, driven by scientific breakthroughs, technological advancements, and evolving patient needs. Users frequently inquire about the progression of precision medicine, the rise of novel therapeutic modalities, and the increasing integration of digital health solutions. These inquiries reflect a broader interest in how treatments are becoming more targeted, less invasive, and more accessible, leading to improved patient outcomes and a more efficient healthcare ecosystem. The focus is shifting from conventional broad-spectrum treatments to highly personalized approaches, which are redefining treatment paradigms and market dynamics.

Another significant area of user interest centers on the expansion of immunotherapy and cell-based therapies, along with the burgeoning field of AI-driven drug discovery and diagnostics. The market is witnessing a rapid adoption of these innovative solutions, which promise to revolutionize cancer care by offering more effective and durable responses. Furthermore, global demographic shifts, particularly the aging population, and the rising prevalence of various cancer types globally are creating sustained demand for advanced oncology solutions. These trends collectively highlight a dynamic market characterized by continuous innovation and a commitment to addressing the complex challenges of cancer management.

- Escalation of precision medicine and targeted therapies.

- Rapid advancements in immunotherapy, including CAR T-cell therapies.

- Integration of artificial intelligence and machine learning in drug discovery and diagnostics.

- Growth in companion diagnostics to guide personalized treatment.

- Increasing focus on early cancer detection and prevention.

- Expansion of biosimilars for oncology drugs reducing treatment costs.

- Rising adoption of liquid biopsies for non-invasive cancer monitoring.

- Decentralization of clinical trials with real-world data integration.

AI Impact Analysis on Oncology

Common user questions regarding AI's impact on oncology frequently address its potential to revolutionize drug discovery, enhance diagnostic accuracy, and personalize treatment regimens. Users are keen to understand how AI algorithms can accelerate the identification of novel drug targets, predict patient responses to therapies, and optimize clinical trial design, thereby shortening development timelines and reducing costs. There is a palpable expectation that AI will bring unprecedented efficiencies to R&D, moving away from traditional, lengthy, and expensive processes towards a more data-driven and predictive approach. Concerns often revolve around data privacy, ethical implications of autonomous decision-making in healthcare, and the need for robust validation of AI models to ensure patient safety and efficacy.

Furthermore, inquiries often delve into AI's role in improving diagnostic precision through image analysis and pathology, identifying subtle disease markers, and assisting oncologists in making more informed treatment decisions. The potential for AI to integrate vast amounts of patient data, including genomic, proteomic, and clinical information, to generate tailored treatment plans is a key area of interest. This personalized approach aims to maximize therapeutic efficacy while minimizing adverse effects. Expectations are high for AI to transform every stage of the cancer care continuum, from initial screening and diagnosis to treatment selection, monitoring, and even post-treatment survivorship, ultimately leading to superior patient outcomes and a more sustainable healthcare system.

- Accelerated drug discovery and target identification.

- Enhanced diagnostic accuracy through advanced image analysis.

- Personalized treatment planning based on patient genomic and clinical data.

- Improved prediction of therapeutic response and potential side effects.

- Optimization of clinical trial design and patient recruitment.

- Development of intelligent screening tools for early cancer detection.

- Streamlined data management and analysis in oncology research.

- Potential for remote monitoring and AI-driven telehealth services.

Key Takeaways Oncology Market Size & Forecast

Analysis of common user questions concerning key takeaways from the oncology market size and forecast reveals a strong interest in understanding the primary forces driving market expansion, identifying the most promising therapeutic areas, and recognizing the regions poised for significant growth. Users frequently seek clarity on which segments, such as immunotherapy or targeted therapies, are expected to contribute most substantially to market value, indicating a desire to pinpoint high-growth investment opportunities. There is also a consistent query about the long-term sustainability of the market's robust growth, considering factors like increasing healthcare expenditure, an aging global population, and the continuous pipeline of innovative treatments entering the market.

Furthermore, insights are often sought regarding the impact of emerging technologies and regulatory frameworks on market trajectory. The prevailing sentiment is that the oncology market will continue its upward trend, propelled by relentless innovation, rising disease incidence, and a global commitment to improving cancer care. The sustained investment in research and development, coupled with strategic collaborations among pharmaceutical companies, biotech firms, and academic institutions, is expected to introduce groundbreaking therapies. This collective effort ensures a dynamic landscape where market growth is not only driven by existing needs but also by the proactive development of future solutions.

- Robust market expansion fueled by a high unmet medical need and continuous innovation.

- Significant growth contributions from novel therapeutic modalities, particularly immunotherapy and precision oncology.

- North America and Europe to maintain dominant market shares due to advanced healthcare infrastructure and high R&D investments.

- Asia Pacific emerging as a high-growth region driven by increasing cancer incidence and improving healthcare access.

- Strong pipeline of oncology drugs poised to enter the market, sustaining future growth.

- Increasing adoption of advanced diagnostic tools supporting personalized treatment strategies.

- Emphasis on value-based care and cost-effectiveness influencing treatment adoption.

Oncology Market Drivers Analysis

The oncology market's consistent growth is primarily propelled by a confluence of impactful drivers, chief among them being the escalating global incidence of various cancer types. As populations age and lifestyle factors contribute to disease progression, the sheer volume of new cancer diagnoses creates an inherent and expanding demand for advanced diagnostic tools and therapeutic interventions. This demographic shift, coupled with improved early detection methods, ensures a continuously expanding patient pool requiring sophisticated cancer care solutions. The persistent high unmet need for effective treatments for many aggressive and rare cancers further incentivizes substantial investment in research and development, fueling innovation.

Technological advancements also serve as a paramount driver, with breakthroughs in genomics, proteomics, and artificial intelligence fundamentally transforming drug discovery, personalized medicine, and diagnostic capabilities. These innovations enable the development of highly targeted therapies, immunotherapies, and gene-editing approaches that offer superior efficacy and reduced side effects compared to traditional treatments. Furthermore, increasing healthcare expenditure globally, particularly in developed and rapidly developing economies, facilitates greater access to advanced oncology treatments and diagnostics. Favorable regulatory policies, including expedited approval pathways for breakthrough therapies, also play a critical role in bringing innovative cancer drugs to market more swiftly, accelerating patient access and market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Cancer Incidence Rates | +2.5% | Global, particularly Asia Pacific and MEA | Long-term (2025-2033) |

| Advancements in R&D and Technology | +2.0% | North America, Europe | Mid to Long-term (2025-2033) |

| Growing Geriatric Population | +1.5% | Global, especially Developed Economies | Long-term (2025-2033) |

| Increasing Healthcare Expenditure | +1.0% | North America, Europe, China | Mid-term (2025-2030) |

| Favorable Regulatory Policies and Drug Approvals | +0.8% | US, EU, Japan | Short to Mid-term (2025-2028) |

Oncology Market Restraints Analysis

Despite the robust growth trajectory, the oncology market faces several significant restraints that could temper its expansion. One of the most prominent challenges is the exceedingly high cost associated with novel cancer therapies, particularly targeted drugs, immunotherapies, and cell and gene therapies. These treatments, while highly effective, often come with price tags that can strain healthcare budgets and limit patient access, especially in regions with less developed reimbursement policies or lower per capita income. The financial burden can lead to difficult decisions for healthcare systems, insurers, and individual patients, potentially hindering the widespread adoption of innovative treatments.

Furthermore, stringent regulatory approval processes, while necessary for patient safety, can significantly delay the market entry of new drugs. The rigorous requirements for clinical trials, including lengthy phases and the need for extensive safety and efficacy data, contribute to the high cost and prolonged timeline of drug development. The emergence of drug resistance, particularly in targeted therapies and immunotherapies, also poses a continuous challenge, necessitating the development of new treatment lines and contributing to the complexity of patient management. Moreover, the severe side effects associated with many potent oncology drugs can impact patient adherence and overall quality of life, leading to treatment discontinuations or the need for extensive supportive care, which adds to healthcare costs and complexity.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Cancer Therapies | -1.8% | Global, particularly Emerging Economies | Long-term (2025-2033) |

| Stringent Regulatory Approval Processes | -1.2% | US, EU, Japan | Mid to Long-term (2025-2033) |

| Development of Drug Resistance | -1.0% | Global | Long-term (2025-2033) |

| Adverse Drug Reactions and Side Effects | -0.7% | Global | Mid-term (2025-2030) |

| Intellectual Property and Patent Expirations | -0.5% | Global | Short to Mid-term (2025-2029) |

Oncology Market Opportunities Analysis

The oncology market is replete with significant opportunities for growth and innovation, driven by evolving scientific understanding and technological advancements. One of the most promising avenues lies in the continued development and commercialization of personalized medicine and precision oncology. Advances in genomic sequencing and molecular profiling allow for highly specific treatment strategies tailored to an individual patient's genetic makeup and tumor characteristics, leading to improved efficacy and reduced toxicity. This shift promises to redefine treatment paradigms, moving beyond one-size-fits-all approaches towards more targeted interventions.

Furthermore, the untapped potential of emerging markets, particularly in Asia Pacific, Latin America, and parts of the Middle East, represents a substantial growth opportunity. These regions are experiencing rising cancer incidence, improving healthcare infrastructure, and increasing disposable incomes, which collectively enhance patient access to advanced oncology treatments. Strategic collaborations, mergers, and acquisitions between pharmaceutical companies, biotech firms, and academic institutions are also key opportunities, fostering shared expertise, accelerating research, and diversifying product pipelines. The growing demand for companion diagnostics, which are essential for guiding targeted therapies, and the expansion into niche indications, such as rare cancers or specific biomarker-driven subsets, also present lucrative pathways for market expansion and value creation within the oncology sector.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Personalized Medicine & Precision Oncology | +2.3% | Global, especially North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Expansion in Emerging Markets | +1.8% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

| Strategic Collaborations and Partnerships | +1.5% | Global | Mid to Long-term (2025-2033) |

| Advancements in Gene and Cell Therapies | +1.2% | North America, Europe | Mid-term (2025-2030) |

| Rising Demand for Companion Diagnostics | +0.9% | Global | Short to Mid-term (2025-2028) |

Oncology Market Challenges Impact Analysis

The oncology market, despite its rapid advancements, grapples with several formidable challenges that can impede its growth and widespread accessibility. Reimbursement hurdles represent a significant barrier, particularly for innovative and high-cost therapies. Payers, including government agencies and private insurers, often struggle with the budget impact of new treatments, leading to restrictive coverage policies or prolonged negotiation processes. This can delay patient access to life-saving drugs, especially in healthcare systems that prioritize cost-effectiveness over immediate access to novel therapies, thereby limiting market penetration.

Another critical challenge is the inherent complexity of cancer as a disease, characterized by its diverse molecular subtypes, evolutionary nature, and the development of treatment resistance. This complexity necessitates continuous research and development, often leading to high R&D costs and a high failure rate in clinical trials. The ethical considerations surrounding novel therapies, such as gene editing and advanced cell therapies, also present regulatory and societal challenges that require careful navigation. Furthermore, the global shortage of skilled healthcare professionals specializing in oncology, coupled with the need for sophisticated infrastructure to administer and monitor advanced treatments, poses a logistical challenge, particularly in underserved regions, impacting the efficient delivery of cancer care and potentially limiting market expansion.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Reimbursement Issues and Payer Pressure | -1.5% | Global, particularly Europe and Emerging Markets | Long-term (2025-2033) |

| Complex and Lengthy Clinical Trial Processes | -1.0% | Global | Long-term (2025-2033) |

| Ethical and Regulatory Considerations for New Therapies | -0.8% | North America, Europe | Mid-term (2025-2030) |

| Shortage of Skilled Oncology Professionals | -0.6% | Global | Long-term (2025-2033) |

| Intellectual Property Disputes and Competition | -0.4% | Global | Short to Mid-term (2025-2029) |

Oncology Market - Updated Report Scope

This report provides a comprehensive analysis of the global oncology market, offering in-depth insights into market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. It encompasses a detailed examination of current market trends, the impact of emerging technologies like Artificial Intelligence, and future projections, aiming to equip stakeholders with a clear understanding of market dynamics and strategic pathways for growth. The scope covers the historical performance of the market alongside meticulous forecasts, providing a robust framework for strategic planning and decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 285.5 Billion |

| Market Forecast in 2033 | USD 571.2 Billion |

| Growth Rate | 9.2% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | F. Hoffmann-La Roche Ltd, Bristol Myers Squibb Company, Merck & Co., Inc., Novartis AG, Pfizer Inc., Johnson & Johnson, AstraZeneca PLC, Sanofi S.A., Eli Lilly and Company, Amgen Inc., AbbVie Inc., Bayer AG, Regeneron Pharmaceuticals, Inc., Gilead Sciences, Inc., Takeda Pharmaceutical Company Limited, Seagen Inc., Daiichi Sankyo Company, Limited, BeiGene, Ltd., Incyte Corporation, Exelixis, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The oncology market is comprehensively segmented to provide a granular understanding of its diverse components, allowing for targeted analysis of growth opportunities and challenges within specific areas. This segmentation helps in identifying high-growth sub-sectors, understanding patient needs, and tailoring strategic initiatives. The market is primarily categorized by cancer type, therapy type, drug class, end-user, and distribution channel, each offering unique insights into the market's structure and dynamics. Understanding these segments is crucial for stakeholders to effectively navigate the complex landscape of cancer diagnosis and treatment, and to develop solutions that address specific medical requirements and market demands.

The segmentation by cancer type highlights the prevalence and treatment approaches for various forms of cancer, from highly prevalent types like lung and breast cancer to rarer indications. Therapy type segmentation reveals the evolving landscape of treatment modalities, distinguishing between traditional chemotherapy and cutting-edge immunotherapies and targeted therapies. Drug class segmentation further breaks down the market by the nature of the pharmacological agents, including biologics and cytotoxic drugs. End-user and distribution channel segments provide insights into where and how oncology products and services are delivered, from large hospital networks to specialized clinics and online pharmacies, reflecting the infrastructure supporting cancer care delivery worldwide.

- By Cancer Type: Lung Cancer, Breast Cancer, Colorectal Cancer, Prostate Cancer, Liver Cancer, Stomach Cancer, Cervical Cancer, Blood Cancer, Other Cancer Types

- By Therapy Type: Chemotherapy, Immunotherapy, Targeted Therapy, Hormonal Therapy, Radiation Therapy, Others

- By Drug Class: Cytotoxic Drugs, Biologics (Monoclonal Antibodies, Recombinant Proteins, Vaccines), Hormonal Drugs, Others

- By End User: Hospitals, Specialty Clinics, Cancer Research Centers, Ambulatory Surgical Centers, Others

- By Distribution Channel: Hospital Pharmacies, Retail Pharmacies, Online Pharmacies

Regional Highlights

- North America: Dominates the global oncology market share due to high cancer prevalence, advanced healthcare infrastructure, significant R&D investments, and rapid adoption of novel therapies. The U.S. remains a key market, characterized by extensive clinical trial activities and a robust pharmaceutical industry.

- Europe: Represents a substantial market, driven by increasing awareness, favorable reimbursement policies in key countries like Germany, France, and the UK, and strong government support for cancer research. However, pricing pressure and health technology assessment pose challenges.

- Asia Pacific (APAC): Expected to exhibit the highest growth rate during the forecast period. This growth is attributed to the rising cancer incidence, improving healthcare access, growing disposable incomes, and the increasing focus of global players on expanding their presence in countries like China, India, and Japan.

- Latin America: Showing nascent growth with increasing healthcare expenditure and a growing patient pool, though challenges remain regarding healthcare access and reimbursement for advanced therapies. Brazil and Mexico are emerging as key regional markets.

- Middle East and Africa (MEA): A smaller but rapidly developing market, driven by increasing investment in healthcare infrastructure, rising cancer awareness, and efforts to improve access to advanced treatments, particularly in countries within the GCC region and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Oncology Market.- F. Hoffmann-La Roche Ltd

- Bristol Myers Squibb Company

- Merck & Co., Inc.

- Novartis AG

- Pfizer Inc.

- Johnson & Johnson

- AstraZeneca PLC

- Sanofi S.A.

- Eli Lilly and Company

- Amgen Inc.

- AbbVie Inc.

- Bayer AG

- Regeneron Pharmaceuticals, Inc.

- Gilead Sciences, Inc.

- Takeda Pharmaceutical Company Limited

- Seagen Inc.

- Daiichi Sankyo Company, Limited

- BeiGene, Ltd.

- Incyte Corporation

- Exelixis, Inc.

Frequently Asked Questions

What is the projected growth rate of the Oncology Market?

The Oncology Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.2% between 2025 and 2033, reaching an estimated USD 571.2 Billion by the end of the forecast period.

What are the primary drivers of growth in the Oncology Market?

Key drivers include the rising global incidence of cancer, significant advancements in research and development leading to innovative therapies, the increasing geriatric population, and growing healthcare expenditure worldwide.

How is Artificial Intelligence impacting the Oncology Market?

AI is revolutionizing oncology by accelerating drug discovery, enhancing diagnostic accuracy through advanced image analysis, enabling personalized treatment planning, and optimizing clinical trial design, leading to more efficient and effective cancer care.

Which therapeutic segments are experiencing the most significant growth?

Immunotherapy and targeted therapy segments are experiencing the most significant growth due to their high efficacy, specificity, and ability to offer personalized treatment approaches, leading to improved patient outcomes.

What are the main challenges faced by the Oncology Market?

Major challenges include the high cost of novel therapies and associated reimbursement issues, stringent and lengthy regulatory approval processes, the ongoing development of drug resistance, and the global shortage of skilled oncology professionals.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted