OLED Encapsulation Adhesive Market

OLED Encapsulation Adhesive Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_678110 | Last Updated : July 17, 2025 |

Format : ![]()

![]()

![]()

![]()

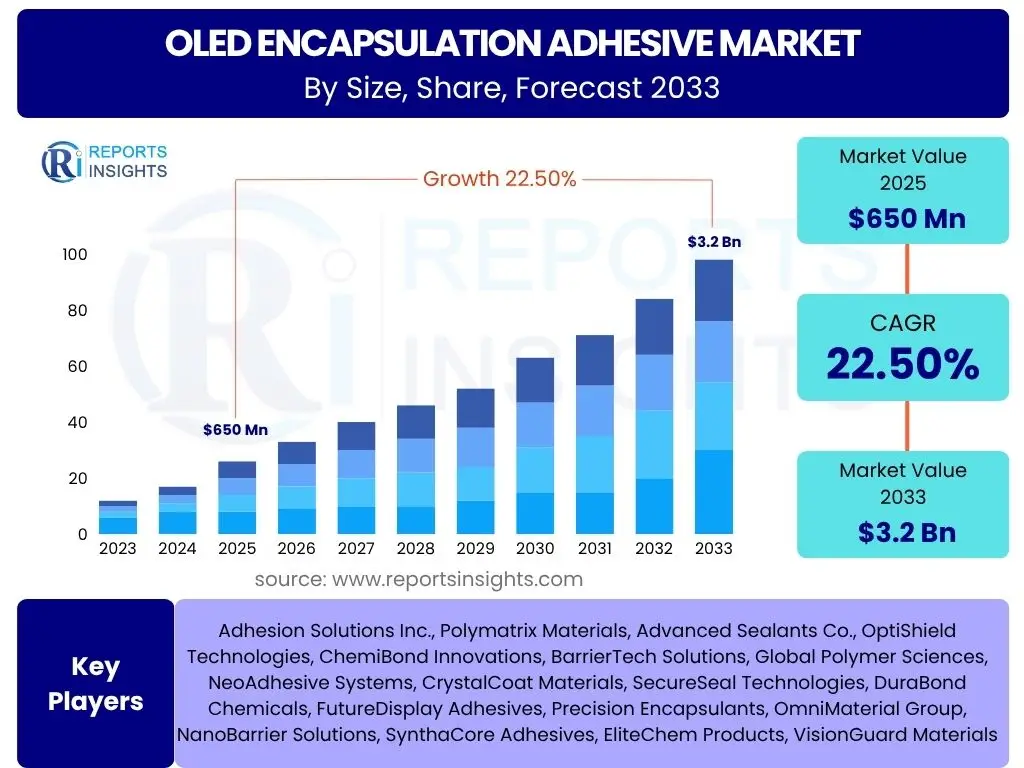

OLED Encapsulation Adhesive Market is projected to grow at a Compound annual growth rate (CAGR) of 18.5% between 2025 and 2033, reaching a valuation of USD 850 million in 2025 and is projected to grow by USD 3.5 billion by 2033, the end of the forecast period.

Key OLED Encapsulation Adhesive Market Trends & Insights

The OLED encapsulation adhesive market is experiencing dynamic shifts driven by advancements in display technology and increasing consumer demand for high-performance devices. Key trends include the growing adoption of flexible and foldable OLED displays, necessitating more robust and adaptable encapsulation solutions. There is also a significant push towards thinner, lighter, and more durable encapsulation materials to meet the stringent requirements of next-generation electronic devices, coupled with an increasing focus on environmentally friendly and sustainable adhesive formulations.

- Increasing demand for flexible and foldable OLED displays.

- Growing adoption of OLED technology in automotive applications.

- Focus on developing ultra-thin and highly durable encapsulation layers.

- Shift towards environmentally friendly and bio-based adhesive solutions.

- Integration of advanced barrier properties for enhanced moisture and oxygen protection.

AI Impact Analysis on OLED Encapsulation Adhesive

Artificial Intelligence (AI) is set to revolutionize various facets of the OLED encapsulation adhesive market, from material discovery to manufacturing process optimization and quality control. AI-driven simulations can predict the performance of novel adhesive formulations, significantly accelerating research and development cycles. Furthermore, AI can enhance production efficiency by optimizing curing processes, reducing material waste, and ensuring consistent quality in large-scale manufacturing environments, thereby offering substantial cost savings and performance improvements.

- AI-driven material discovery and formulation optimization for enhanced adhesive properties.

- Predictive analytics for quality control and defect detection during encapsulation processes.

- Optimization of manufacturing parameters (e.g., curing time, temperature) using machine learning algorithms.

- AI-powered supply chain management for raw material procurement and logistics efficiency.

- Simulation and modeling of encapsulation performance under various environmental conditions.

Key Takeaways OLED Encapsulation Adhesive Market Size & Forecast

- The global OLED encapsulation adhesive market is poised for robust growth, driven by expanding OLED adoption across diverse industries.

- The market is projected to achieve a significant Compound Annual Growth Rate (CAGR) of 18.5% from 2025 to 2033, reflecting strong underlying demand.

- By 2033, the market is expected to reach a substantial valuation of USD 3.5 billion, indicating a nearly four-fold increase from its 2025 estimated size of USD 850 million.

- Technological advancements in display manufacturing and increased R&D investments in encapsulation solutions are key drivers for this impressive expansion.

- The Asia Pacific region is anticipated to remain the dominant market, fueled by the presence of major display manufacturers and a large consumer electronics production base.

OLED Encapsulation Adhesive Market Drivers Impact Analysis

The OLED encapsulation adhesive market is fundamentally driven by the escalating global demand for advanced display technologies. As consumers increasingly seek devices with superior visual quality, thinner profiles, and enhanced durability, the need for effective encapsulation solutions becomes paramount. The widespread adoption of OLED panels across various sectors, including consumer electronics, automotive, and digital signage, creates a strong impetus for market expansion.

Technological innovation further fuels this growth. The continuous development of flexible, foldable, and rollable OLED displays necessitates high-performance adhesives capable of withstanding mechanical stress, environmental exposure, and repeated bending cycles without compromising display integrity. This demand for specialized and robust encapsulation materials drives significant investment in research and development, leading to novel adhesive formulations with improved barrier properties, adhesion strength, and processability. These advancements are crucial for enabling the next generation of display products and sustaining market momentum.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for OLED Displays Across Applications | +6.5% | Global, particularly APAC (South Korea, China), North America, Europe | Long-term (2025-2033) |

| Advancements in Flexible and Foldable Display Technologies | +4.0% | Global, with strong innovation hubs in South Korea, China, Japan, USA | Mid to Long-term (2027-2033) |

| Growing Adoption of OLED in Automotive Displays | +3.0% | Europe, North America, Japan, China | Mid to Long-term (2026-2033) |

| Emphasis on Enhanced Display Durability and Lifespan | +2.5% | Global, especially high-end consumer electronics markets | Long-term (2025-2033) |

| Miniaturization and Thinner Display Requirements | +2.0% | Global, driven by smartphone and wearable manufacturers | Mid-term (2025-2030) |

OLED Encapsulation Adhesive Market Restraints Impact Analysis

Despite the robust growth prospects, the OLED encapsulation adhesive market faces several inherent restraints that could temper its expansion. One significant challenge is the high manufacturing cost associated with OLED displays themselves, which directly impacts the overall cost of the final product. As encapsulation adhesives are a critical component, their cost, particularly for advanced formulations, can add to this burden, making OLED technology less competitive against established display technologies like LCDs in certain segments.

Furthermore, the complexity of the OLED manufacturing process, including the application and curing of encapsulation adhesives, demands highly specialized equipment and controlled environments. Any disruptions in the supply chain for raw materials, especially for unique chemical components, or intellectual property disputes related to patented adhesive technologies, can create bottlenecks and increase production costs. The performance requirements for OLED encapsulation are exceptionally high, demanding materials that offer near-perfect barrier properties against moisture and oxygen, which are inherently expensive and challenging to produce consistently at scale, thus posing a continuous technical and economic hurdle.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs of OLED Displays | -3.5% | Global, impacts price competitiveness in all regions | Long-term (2025-2033) |

| Supply Chain Vulnerabilities and Raw Material Price Volatility | -2.0% | Global, particularly regions dependent on specific chemical suppliers (e.g., China, Europe) | Mid-term (2025-2028) |

| Competition from Alternative Display Technologies (e.g., MiniLED) | -1.5% | Global, competitive in high-end TV and monitor segments | Mid to Long-term (2026-2033) |

| Stringent Regulatory Landscape and Environmental Concerns | -1.0% | Europe, North America, Japan | Long-term (2025-2033) |

OLED Encapsulation Adhesive Market Opportunities Impact Analysis

The OLED encapsulation adhesive market is ripe with opportunities, primarily driven by the continuous evolution of display technologies and the pursuit of novel applications. The emergence of next-generation display formats, such as transparent, stretchable, and rollable OLEDs, presents a significant avenue for innovation in encapsulation materials. These advanced display types require adhesives with unique properties, including optical clarity, extreme flexibility, and enhanced mechanical resilience, pushing the boundaries of current material science.

Furthermore, the increasing focus on sustainability across industries offers a compelling opportunity for manufacturers to develop and commercialize eco-friendly encapsulation adhesives. This includes bio-based formulations, recyclable materials, and processes that minimize energy consumption and waste. Investing in sustainable solutions not only addresses growing environmental concerns but also positions companies favorably in markets increasingly prioritizing green technologies. Additionally, the expansion of OLED technology into new industrial and niche applications, beyond traditional consumer electronics, opens up untapped revenue streams and diversification possibilities for adhesive providers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Transparent, Stretchable, and Rollable OLEDs | +4.5% | Global, R&D intensive regions (South Korea, Japan, USA, Europe) | Long-term (2028-2033) |

| Development of Eco-friendly and Sustainable Encapsulation Solutions | +3.0% | Europe, North America, Japan, driving global standards | Mid to Long-term (2026-2033) |

| Expansion into New Industrial and Niche Applications (e.g., Medical, Aerospace) | +2.5% | North America, Europe, targeted APAC markets | Mid-term (2025-2030) |

| Increasing Focus on Cost-Effective and High-Performance Solutions | +2.0% | Global, especially emerging economies and competitive markets | Long-term (2025-2033) |

OLED Encapsulation Adhesive Market Challenges Impact Analysis

The OLED encapsulation adhesive market faces inherent technical complexities that present significant challenges to continuous innovation and market penetration. Achieving perfect encapsulation, which is crucial for preventing moisture and oxygen ingress that degrades OLED performance, remains a formidable task. This requires adhesives with exceptionally low water vapor transmission rates (WVTR) and oxygen transmission rates (OTR), properties that are difficult to achieve consistently across varied application methods and device architectures.

Furthermore, ensuring long-term stability and reliability of the encapsulation layer under diverse environmental conditions, including high temperatures, humidity, and mechanical stress, is a continuous technical hurdle. Balancing properties such as adhesion strength, flexibility, optical clarity, and thermal stability in a single adhesive formulation presents a complex material science problem. As OLED technology evolves towards thinner, flexible, and even stretchable forms, these encapsulation challenges intensify, requiring novel material designs and manufacturing processes that can be both cost-effective and scalable for mass production.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Perfect Barrier Properties Against Moisture and Oxygen | -2.5% | Global, fundamental technical challenge | Long-term (2025-2033) |

| Ensuring Long-Term Stability and Reliability of Encapsulation | -2.0% | Global, critical for device longevity | Long-term (2025-2033) |

| Technical Complexities in Manufacturing and Application Processes | -1.5% | Global, particularly for new manufacturers entering the market | Mid-term (2025-2028) |

| Balancing Performance with Cost-Effectiveness for Mass Production | -1.0% | Global, especially in competitive consumer electronics sectors | Long-term (2025-2033) |

OLED Encapsulation Adhesive Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global OLED encapsulation adhesive market, covering key market dynamics, segmentation, regional insights, and competitive landscape. It offers strategic insights for stakeholders to navigate market opportunities and challenges effectively, providing a robust foundation for informed decision-making and strategic planning.

| Report Attributes | Report Details |

|---|---|

| Report Name | OLED Encapsulation Adhesive Market |

| Market Size in 2025 | USD 850 million |

| Market Forecast in 2033 | USD 3.5 billion |

| Growth Rate | CAGR of 2025 to 2033 18.5% |

| Number of Pages | 280 |

| Key Companies Covered | Tesa, AGC, 3M, NITTO DENKO, Sumitomo, DowDupnt, Kyoritsu, Nanonlx, NSG, Nagese, Nanonic, KANGDEXIN COMPOSITE MATERIAL |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis

: Market Product Type Segmentation:-- Instant Encapsulating Adhesives

- Pressure Sensitive Encapsulating Adhesives

- Others

- Passive-matrix OLED

- Active-matrix OLED

- Others

Regional Highlights

- Asia Pacific (APAC): The APAC region is the dominant and fastest-growing market for OLED encapsulation adhesives, primarily driven by the presence of major display panel manufacturers in South Korea, China, and Japan. The region benefits from substantial investments in OLED production capacities and a high concentration of consumer electronics manufacturing, particularly smartphones, TVs, and wearables, which are key end-use segments.

- North America: North America represents a significant market for OLED encapsulation adhesives, characterized by high adoption of premium consumer electronics, a strong automotive sector integrating advanced displays, and robust research and development activities in cutting-edge display technologies. The region's demand is driven by innovation and early adoption of new OLED applications.

- Europe: Europe is a key market, propelled by its strong automotive industry's increasing integration of OLED displays for dashboards and infotainment systems. Furthermore, the region's focus on high-end consumer electronics and a growing emphasis on sustainable and high-performance materials contribute to the demand for advanced encapsulation adhesives.

- Latin America & Middle East and Africa (MEA): These emerging regions are witnessing gradual growth in the OLED encapsulation adhesive market. Growth is primarily spurred by increasing disposable incomes, expanding penetration of consumer electronics, and developing local manufacturing capabilities, though at a slower pace compared to the established markets.

Top Key Players:

The market research report covers the analysis of key stakeholders of the OLED Encapsulation Adhesive Market. Some of the leading players profiled in the report include -:- Tesa

- AGC

- 3M

- NITTO DENKO

- Sumitomo

- DowDupnt

- Kyoritsu

- Nanonlx

- NSG

- Nagese

- Nanonic

- KANGDEXIN COMPOSITE MATERIAL

Frequently Asked Questions:

What is OLED encapsulation adhesive?

OLED encapsulation adhesive is a specialized material used to protect organic light-emitting diode (OLED) displays from moisture, oxygen, and other environmental contaminants that can degrade their performance and lifespan. It forms a crucial protective barrier over the sensitive organic layers, ensuring the long-term stability and functionality of OLED screens in devices like smartphones, televisions, and wearables.

Why is encapsulation crucial for OLED displays?

Encapsulation is vital for OLED displays because the organic materials used in their construction are highly susceptible to damage from moisture and oxygen. Even trace amounts of these elements can cause pixel degradation, dark spots, and reduced brightness, leading to premature display failure. Effective encapsulation adhesives create an impermeable seal, safeguarding the delicate OLED components and significantly extending the display's operational life.

What are the primary applications of OLED encapsulation adhesives?

OLED encapsulation adhesives are primarily used in a wide range of electronic devices featuring OLED displays. This includes consumer electronics such as smartphones, tablets, smartwatches, and high-definition televisions. Beyond personal devices, they are increasingly adopted in automotive infotainment systems, digital signage, virtual reality headsets, and emerging flexible and foldable display technologies, due to their superior protective capabilities.

What are the main types of OLED encapsulation adhesives?

The main types of OLED encapsulation adhesives include Instant Encapsulating Adhesives, which often cure rapidly upon exposure to light or heat, and Pressure Sensitive Encapsulating Adhesives, which form strong bonds under pressure without requiring a curing process. Other types may involve a combination of these properties or specific formulations designed for particular display structures, such as thin-film encapsulation (TFE) layers or desiccant-integrated adhesives, each offering unique benefits for diverse OLED manufacturing requirements.

What factors are driving the growth of the OLED encapsulation adhesive market?

The OLED encapsulation adhesive market growth is driven by several key factors: the escalating global demand for OLED displays in various electronic devices, significant advancements in flexible and foldable display technologies requiring specialized protection, and the increasing integration of OLEDs in automotive applications. Additionally, the continuous pursuit of enhanced display durability, extended lifespan, and the miniaturization of electronic devices are propelling the demand for high-performance encapsulation solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted