OLED Display Driver IC Market

OLED Display Driver IC Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708181 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

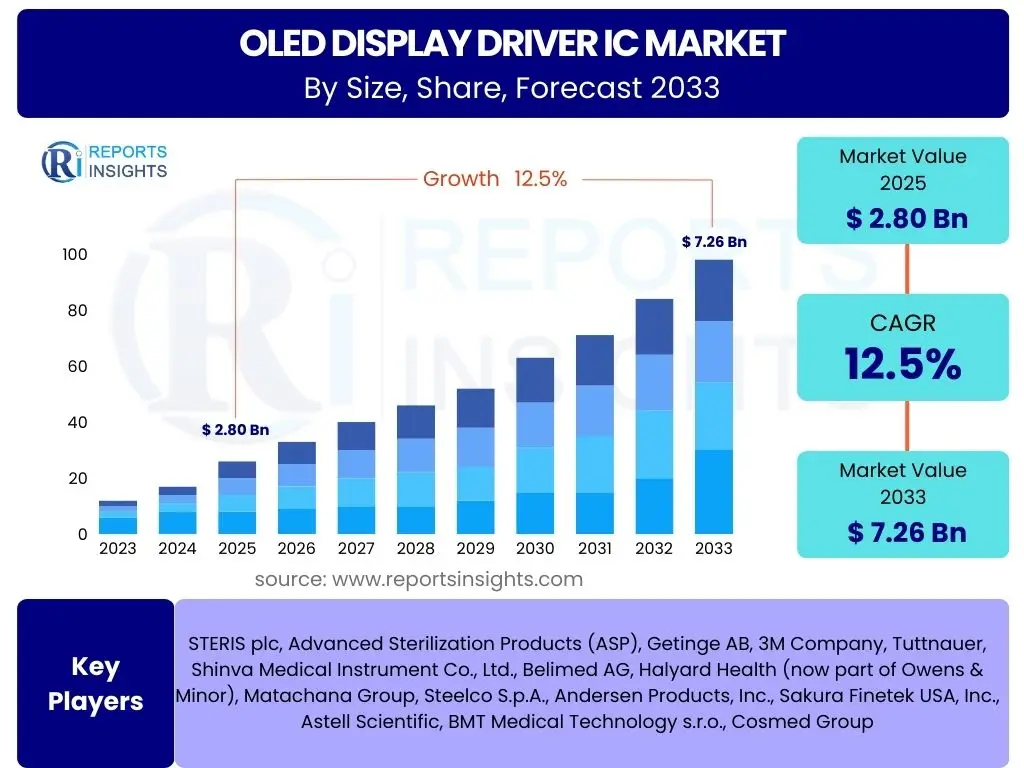

OLED Display Driver IC Market Size

According to Reports Insights Consulting Pvt Ltd, The OLED Display Driver IC Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2033. The market is estimated at USD 2.80 Billion in 2025 and is projected to reach USD 7.26 Billion by the end of the forecast period in 2033.

Key OLED Display Driver IC Market Trends & Insights

User inquiries frequently highlight the accelerating shift towards OLED technology across various consumer electronics and industrial applications as a primary driver for the display driver IC market. The demand for higher resolutions, increased power efficiency, and more sophisticated display functionalities, such as variable refresh rates and always-on capabilities, are consistently raised as key areas of interest. Consumers and industry professionals are also keenly observing the integration of advanced technologies like Touch and Display Driver Integration (TDDI) to streamline manufacturing processes and enhance user experience.

Another significant trend garnering attention involves the expansion of OLED into new segments beyond premium smartphones, including automotive infotainment systems, augmented reality (AR) devices, and large-screen televisions. The miniaturization of components and the increasing complexity of display control algorithms are driving innovation in IC design. Furthermore, the push for sustainable manufacturing practices and energy-efficient designs is influencing the development of next-generation OLED display driver ICs, making power consumption a critical performance metric.

- Growing adoption of OLED displays in smartphones, wearables, and automotive applications.

- Development of integrated TDDI (Touch and Display Driver Integration) solutions.

- Increasing demand for high-resolution, low-power, and high refresh rate displays.

- Expansion of OLED technology into new segments like AR/VR and industrial displays.

- Focus on energy-efficient and compact driver IC designs.

AI Impact Analysis on OLED Display Driver IC

Common user questions regarding the impact of Artificial Intelligence (AI) on OLED Display Driver ICs often revolve around how AI can enhance display performance, optimize power consumption, and streamline the design and manufacturing processes. Users are curious about AI's role in real-time image processing, adaptive brightness control, and content-aware adjustments that can significantly improve visual quality and user experience. The potential for AI to dynamically manage pixel behavior and refresh rates for optimal power efficiency in varied usage scenarios is also a key area of interest, reflecting a broader industry trend towards smarter, more autonomous device functionalities.

Beyond performance enhancements, the influence of AI on the developmental lifecycle of OLED Display Driver ICs is a recurring theme. There is significant interest in how AI-powered tools can accelerate chip design, verification, and testing, potentially reducing time-to-market and development costs. Concerns often include the computational overhead and power requirements of integrating AI directly into ICs, as well as the need for robust algorithms that can adapt to diverse display types and application environments. The long-term implications for competitive advantage through AI-driven differentiation in display technology remain a central focus for market participants.

- AI-driven optimization of display performance and image quality through real-time processing.

- Enhanced power management and adaptive brightness control via AI algorithms.

- Accelerated design and verification of complex OLED driver ICs using AI tools.

- Implementation of AI for defect detection and yield improvement in manufacturing.

- Development of smart displays with AI-enabled content awareness and user experience personalization.

Key Takeaways OLED Display Driver IC Market Size & Forecast

User queries regarding key takeaways from the OLED Display Driver IC market size and forecast consistently point to the robust growth trajectory driven by the pervasive adoption of OLED technology. The market's significant expansion, projected to more than double in value over the forecast period, underscores the ongoing technological migration from traditional LCDs to more vibrant and energy-efficient OLED panels across diverse applications. This growth is not merely volumetric but also qualitative, emphasizing the increasing sophistication and functional integration within driver ICs to meet evolving consumer and industry demands for superior visual experiences and power efficiency.

A critical insight highlighted by the forecast is the pivotal role of innovation in sustaining market momentum. The continuous development of solutions like TDDI, alongside advancements in power management and support for higher resolutions, will be crucial for competitive positioning. Furthermore, the market's trajectory is heavily influenced by the expansion into new high-growth segments such as automotive displays, augmented reality, and large-format televisions, which are expected to drive substantial demand. Stakeholders are advised to focus on strategic investments in R&D and supply chain optimization to capitalize on these emerging opportunities and navigate the dynamic landscape effectively.

- The OLED Display Driver IC market is set for substantial growth, driven by expanding OLED adoption.

- Technological advancements, particularly in TDDI and power efficiency, are critical growth enablers.

- Emerging applications in automotive, AR/VR, and large-screen displays offer significant market expansion opportunities.

- Strategic partnerships and supply chain resilience will be crucial for market participants.

- Investment in R&D for next-generation, high-performance driver ICs is essential to maintain competitive edge.

OLED Display Driver IC Market Drivers Analysis

The OLED Display Driver IC market is significantly propelled by several key factors that contribute to its robust expansion. The most prominent driver is the accelerating global adoption of OLED displays across a multitude of electronic devices. As consumers increasingly demand superior visual experiences characterized by vibrant colors, deep blacks, and higher contrast ratios, manufacturers are pivoting towards OLED technology. This widespread integration, particularly in premium smartphones, smartwatches, and gradually extending into tablets and laptops, necessitates a continuous supply of advanced display driver ICs capable of supporting these sophisticated panels.

Another crucial driver is the ongoing technological innovation within the display industry, specifically the trend towards higher resolutions, faster refresh rates, and enhanced power efficiency. Modern OLED displays require driver ICs that can meticulously control millions of individual pixels, manage power consumption efficiently for extended battery life, and support features like variable refresh rates for smoother user interfaces. Furthermore, the emergence of new form factors, such as foldable and rollable displays, presents unique challenges and opportunities for IC manufacturers, demanding highly flexible and miniaturized driver solutions that push the boundaries of current technology. These innovations collectively stimulate demand and investment in the OLED driver IC segment.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing OLED Adoption in Smartphones & Wearables | +2.8% | Global, particularly Asia Pacific & North America | 2025-2033 |

| Technological Advancements in Display Resolutions & Refresh Rates | +2.3% | Global | 2025-2033 |

| Expansion into Automotive & AR/VR Applications | +1.9% | North America, Europe, Asia Pacific | 2026-2033 |

| Growing Demand for Power-Efficient Display Solutions | +1.5% | Global | 2025-2031 |

| Development of Flexible and Foldable Displays | +1.0% | Asia Pacific (South Korea, China) | 2027-2033 |

OLED Display Driver IC Market Restraints Analysis

Despite its robust growth potential, the OLED Display Driver IC market faces several significant restraints that could temper its expansion. One primary concern is the relatively higher manufacturing cost of OLED panels compared to traditional LCDs, which directly impacts the cost structure of the associated driver ICs. This cost disparity can hinder widespread adoption, particularly in budget-sensitive product categories and emerging markets, limiting the total addressable market for these specialized ICs. The complexity of OLED panel manufacturing, including stringent material requirements and intricate fabrication processes, adds to the overall expense, creating a barrier for cost-conscious manufacturers and consumers.

Another notable restraint is the intense competition and significant capital investment required for research and development in this highly specialized field. The development of advanced driver ICs demands substantial financial outlays for R&D, sophisticated testing equipment, and highly skilled engineering talent. This high barrier to entry can limit the number of new players and consolidate market power among established giants, potentially slowing innovation in certain niche areas. Furthermore, the volatility in raw material prices and the complexities of global supply chains can introduce uncertainties and cost fluctuations, making long-term planning and consistent pricing challenging for manufacturers of OLED display driver ICs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs of OLED Panels | +1.8% | Global, particularly price-sensitive markets | 2025-2033 |

| Intense Competition & High R&D Investment | +1.5% | Global | 2025-2033 |

| Technological Complexities & Integration Challenges | +1.2% | Global | 2025-2030 |

| Supply Chain Volatility and Raw Material Price Fluctuations | +0.9% | Global | 2025-2029 |

| Limited Adoption in Certain Cost-Sensitive Segments | +0.7% | Emerging Economies | 2025-2033 |

OLED Display Driver IC Market Opportunities Analysis

The OLED Display Driver IC market presents numerous growth opportunities stemming from evolving technological landscapes and expanding application domains. A significant opportunity lies in the burgeoning automotive sector, where OLED displays are increasingly being integrated into infotainment systems, digital dashboards, and rear-seat entertainment units. The demand for vivid, customizable, and durable displays in vehicles, coupled with the need for high-reliability driver ICs, opens a substantial new market segment. As autonomous driving technologies advance, the requirement for sophisticated human-machine interfaces (HMIs) will further accelerate the adoption of OLEDs, creating consistent demand for specialized driver IC solutions.

Another promising avenue for growth is the rapid expansion of augmented reality (AR) and virtual reality (VR) devices. These immersive technologies rely heavily on high-resolution, low-latency micro-OLED displays to deliver compelling user experiences, driving the need for compact, highly efficient, and fast display driver ICs. The continuous innovation in these fields, coupled with declining production costs and increasing consumer adoption, will fuel demand for purpose-built driver solutions. Furthermore, the long-term trend towards larger OLED televisions and professional monitors, which require highly complex multi-channel driver ICs for uniform brightness and color accuracy, offers additional revenue streams. These opportunities, supported by ongoing technological advancements, position the market for sustained expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Adoption in Automotive Display Systems | +2.5% | Europe, North America, Asia Pacific (China, Japan) | 2026-2033 |

| Emergence of AR/VR Devices and Micro-OLED Displays | +2.1% | North America, Asia Pacific | 2027-2033 |

| Growth in Large-Screen OLED TVs and Professional Monitors | +1.7% | North America, Europe, Asia Pacific | 2025-2032 |

| Demand for Customization and Integration in Niche Applications | +1.3% | Global | 2025-2033 |

| Advancements in Manufacturing Efficiency and Cost Reduction | +1.0% | Asia Pacific (South Korea, Taiwan) | 2025-2030 |

OLED Display Driver IC Market Challenges Impact Analysis

The OLED Display Driver IC market faces several notable challenges that could influence its growth trajectory and competitive landscape. One significant challenge revolves around the increasingly stringent power consumption requirements for portable and battery-operated devices. As devices become smaller and more feature-rich, maintaining long battery life is paramount, demanding driver ICs that can operate with extremely high power efficiency. Designing such ICs, especially for high-resolution and high refresh rate OLED panels, presents complex engineering hurdles, often requiring innovative circuit designs and advanced process technologies to minimize energy leakage and optimize power delivery under varying load conditions.

Another critical challenge is the inherent technological complexity associated with driving OLED panels, particularly those with advanced features like variable refresh rates, always-on display modes, and high dynamic range (HDR) support. Ensuring pixel-level uniformity, preventing burn-in, and managing dynamic range across different content types require highly sophisticated algorithms and robust IC architectures. Integrating these advanced functionalities into a compact and cost-effective package, while maintaining reliability and thermal performance, adds considerable complexity to the design and manufacturing process. Furthermore, the rapid pace of display technology evolution means driver IC manufacturers must constantly innovate to keep up, often facing shortened product lifecycles and significant R&D pressure to stay competitive in a fast-moving market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Meeting Stringent Power Consumption Requirements | +1.6% | Global | 2025-2033 |

| Technological Complexity of Advanced OLED Features | +1.4% | Global | 2025-2031 |

| Ensuring Display Uniformity and Preventing Burn-in | +1.1% | Global | 2025-2030 |

| Rapid Pace of Display Technology Evolution | +0.8% | Global | 2025-2033 |

| IP Infringement and Intense Price Pressure | +0.6% | Asia Pacific | 2025-2028 |

OLED Display Driver IC Market - Updated Report Scope

This report offers a comprehensive analysis of the global OLED Display Driver IC market, encompassing historical data, current market dynamics, and future projections. It delves into the market size, growth drivers, restraints, opportunities, and challenges, providing a detailed understanding of the industry landscape. The study segments the market by various criteria, including display type, panel size, product type, resolution, and application, offering granular insights into each segment's performance and potential. Furthermore, a thorough regional analysis is presented, highlighting key market trends and competitive landscapes across major geographical areas. The report also profiles leading market players, offering strategic insights into their product portfolios, recent developments, and competitive strategies, to provide stakeholders with a holistic view of the market's current state and future prospects.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.80 Billion |

| Market Forecast in 2033 | USD 7.26 Billion |

| Growth Rate | 12.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Samsung System LSI, Novatek Microelectronics, Himax Technologies, Synaptics, MagnaChip Semiconductor, Parade Technologies, Raydium Semiconductor, LG Display, Silicon Works (Lusem), MediaTek, ROHM Semiconductor, Texas Instruments, Renesas Electronics, Toshiba, Microchip Technology, STMicroelectronics, NXP Semiconductors, Analog Devices, Dialog Semiconductor, FocalTech Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The OLED Display Driver IC market is comprehensively segmented to provide granular insights into its diverse components and evolving dynamics. This segmentation facilitates a deeper understanding of market trends, consumer preferences, and technological shifts across various applications and product categories. Analyzing these segments helps in identifying key growth areas, understanding competitive landscapes, and formulating targeted business strategies. The detailed breakdown covers display technologies, panel dimensions, driver IC types, display resolutions, and end-use applications, offering a multifaceted view of the market's structure and future potential.

- By Display Type: This segment distinguishes between AMOLED (Active Matrix OLED) and PMOLED (Passive Matrix OLED) technologies. AMOLED, with its superior performance and larger panel capabilities, dominates premium and high-end applications, while PMOLED finds niche uses in simpler, smaller displays.

- By Panel Size: Categorization into Small & Medium Panels (e.g., smartphones, wearables, automotive dashboards) and Large Panels (e.g., TVs, monitors) reflects the varied requirements for driver ICs based on display dimensions and complexity.

- By Product Type: This segment includes Touch and Display Driver Integration (TDDI), which combines touch and display functions into a single IC for compact designs, and traditional Display Driver ICs (DDIs), further broken down into Source Drivers, Gate Drivers, and Timing Controllers (T-CONs) for specialized functions.

- By Resolution: Encompasses various display resolutions from High Definition (HD) to Full HD (FHD), Quad HD (QHD), Ultra HD (UHD/4K), and Others (e.g., 8K, custom resolutions), reflecting the increasing demand for sharper and more detailed imagery.

- By Application: This crucial segment delineates the market by end-use industries, including Smartphones, Wearables, Tablets & Laptops, Automotive Displays, Smart TVs, Industrial Displays, and Other emerging applications such as AR/VR headsets and medical devices.

Regional Highlights

- Asia Pacific (APAC): Dominates the OLED Display Driver IC market due to the presence of major OLED panel manufacturers and leading consumer electronics brands, particularly in South Korea, China, Japan, and Taiwan. Rapid urbanization, increasing disposable incomes, and a large consumer base drive the demand for OLED-enabled devices.

- North America: A significant market driven by early adoption of advanced technologies, strong R&D investments, and a robust automotive sector. The demand for high-end smartphones, premium TVs, and emerging AR/VR applications contributes to market growth.

- Europe: Characterized by a strong focus on automotive displays, industrial applications, and high-end consumer electronics. Stringent regulatory standards for display quality and power efficiency further influence the adoption of advanced OLED driver ICs.

- Latin America: An emerging market experiencing gradual growth, primarily driven by increasing smartphone penetration and the growing availability of OLED-equipped devices in key economies like Brazil and Mexico.

- Middle East & Africa (MEA): Shows steady growth, fueled by rising disposable incomes, infrastructure development, and increasing demand for consumer electronics, particularly smartphones and smart TVs.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the OLED Display Driver IC Market.- Samsung System LSI

- Novatek Microelectronics

- Himax Technologies

- Synaptics

- MagnaChip Semiconductor

- Parade Technologies

- Raydium Semiconductor

- LG Display

- Silicon Works (Lusem)

- MediaTek

- ROHM Semiconductor

- Texas Instruments

- Renesas Electronics

- Toshiba

- Microchip Technology

- STMicroelectronics

- NXP Semiconductors

- Analog Devices

- Dialog Semiconductor

- FocalTech Systems

Frequently Asked Questions

What is the projected growth rate for the OLED Display Driver IC market?

The OLED Display Driver IC market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2033, driven by expanding OLED adoption across various applications.

Which applications are driving the demand for OLED Display Driver ICs?

Key applications driving demand include smartphones, wearables, automotive displays, smart TVs, and emerging segments like AR/VR devices, all requiring high-performance and power-efficient OLED driver solutions.

What are the primary technological trends in OLED Display Driver ICs?

Major technological trends include the integration of Touch and Display Driver Integration (TDDI), advancements for higher resolutions and refresh rates, enhanced power efficiency, and support for flexible and foldable display form factors.

How does AI impact the OLED Display Driver IC market?

AI significantly impacts the market by enabling real-time display optimization, adaptive power management, accelerated chip design, and enhanced quality control during manufacturing, leading to smarter and more efficient displays.

What are the main challenges faced by the OLED Display Driver IC market?

Key challenges include managing stringent power consumption requirements, overcoming the technological complexity of advanced OLED features, ensuring display uniformity and preventing burn-in, and navigating the rapid pace of display technology evolution.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted