Oleate Ester Market

Oleate Ester Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705004 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

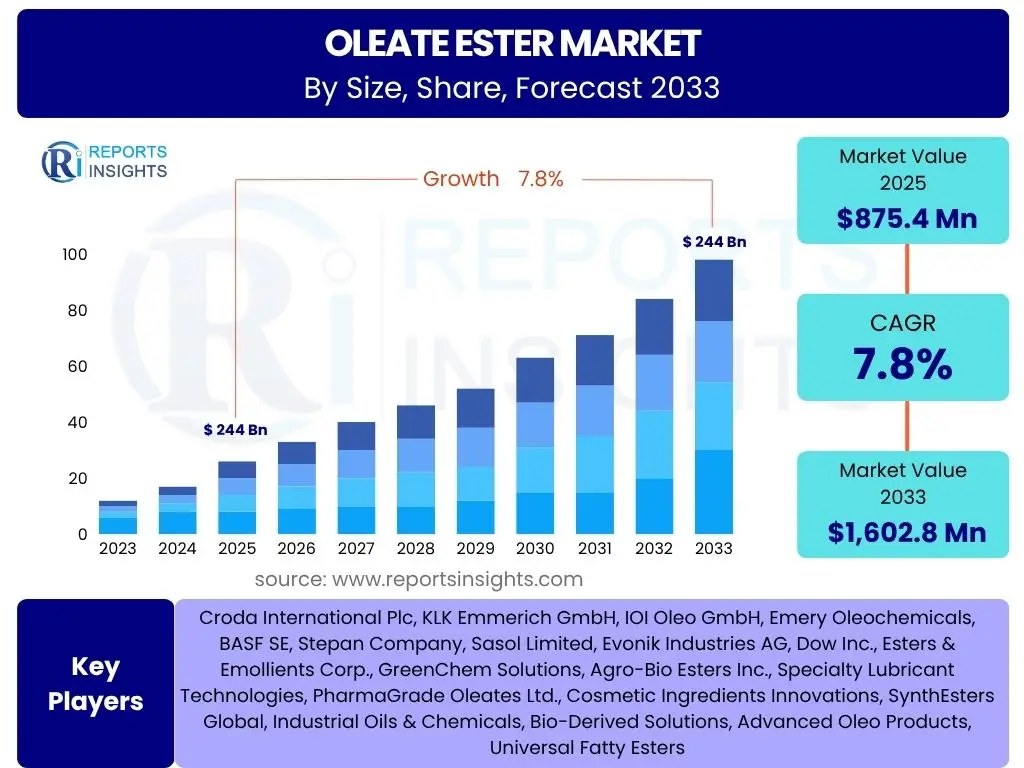

Oleate Ester Market Size

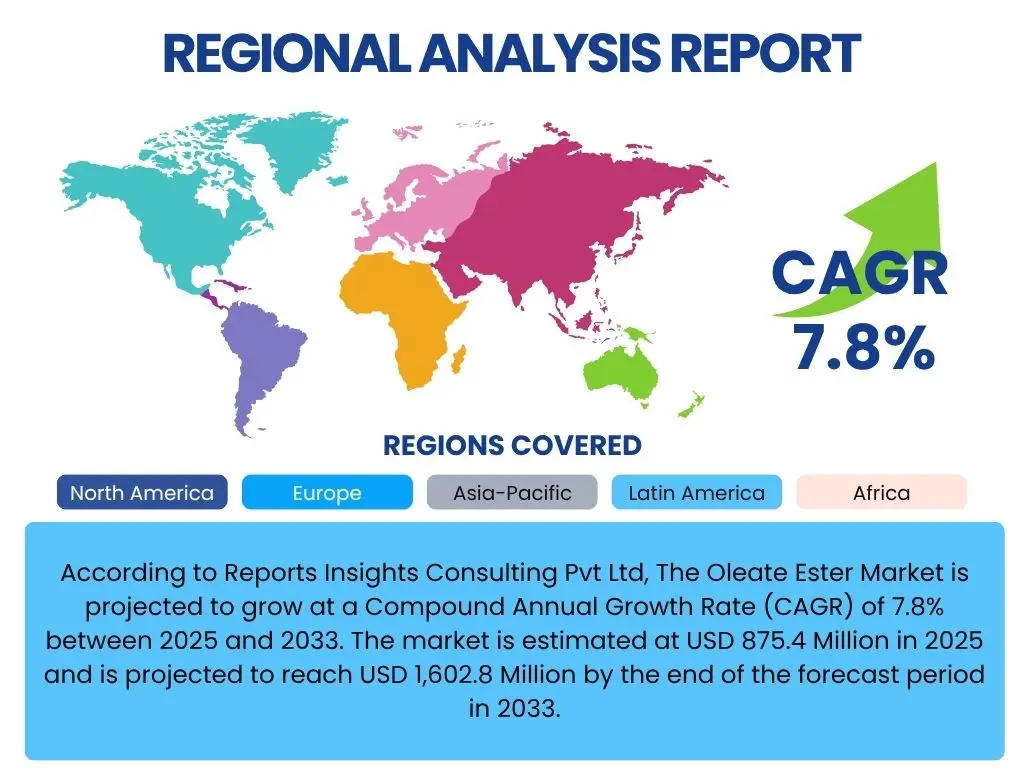

According to Reports Insights Consulting Pvt Ltd, The Oleate Ester Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 875.4 Million in 2025 and is projected to reach USD 1,602.8 Million by the end of the forecast period in 2033.

Key Oleate Ester Market Trends & Insights

The Oleate Ester market is experiencing significant evolution, driven by shifts towards sustainable and bio-based products, alongside expanding applications across diverse industries. Consumer preferences for natural and less harmful ingredients in personal care and cosmetic products are profoundly influencing product formulations, favoring oleate esters derived from renewable sources. Furthermore, the burgeoning demand for high-performance, environmentally friendly lubricants and industrial fluids is opening new avenues for oleate esters, leveraging their excellent lubricity and biodegradability profiles. Innovation in manufacturing processes, including enzymatic synthesis and green chemistry techniques, is also becoming a critical trend, aiming to reduce environmental footprints and improve product purity.

Beyond the core applications, the pharmaceutical and food sectors are increasingly recognizing the utility of oleate esters as excipients, emulsifiers, and delivery agents, contributing to the market's broadening scope. The convergence of these trends suggests a market moving towards more specialized, higher-value applications, with a strong emphasis on product customization and regulatory compliance. Companies are investing in research and development to address these specific industry needs, leading to the introduction of novel oleate ester derivatives tailored for enhanced performance and stability in challenging environments.

- Increasing demand for bio-based and sustainable oleate esters across end-use industries.

- Growing adoption in the personal care and cosmetics sector due to emulsifying and emollient properties.

- Expansion of oleate esters into high-performance lubricant and metalworking fluid formulations.

- Rising focus on regulatory compliance and the development of environmentally friendly alternatives.

- Technological advancements in esterification processes, including enzymatic and solvent-free methods.

- Emergence of new applications in pharmaceuticals, food and beverages, and agriculture.

AI Impact Analysis on Oleate Ester

Artificial intelligence is poised to revolutionize various aspects of the Oleate Ester market, from raw material sourcing and synthesis to supply chain management and demand forecasting. AI-powered analytical tools can optimize reaction parameters in esterification processes, leading to higher yields, improved purity, and reduced energy consumption. This translates into more efficient production and lower operational costs. Furthermore, AI can accelerate the discovery and development of novel oleate ester derivatives by simulating molecular interactions and predicting material properties, significantly shortening the R&D cycle for new formulations tailored to specific industrial needs.

Beyond production, AI's influence extends to supply chain optimization, where predictive analytics can forecast demand fluctuations, manage inventory levels, and identify potential disruptions, ensuring a more resilient and responsive supply chain for raw materials like oleic acid and alcohols, as well as finished products. AI can also enhance quality control by analyzing real-time process data to detect anomalies and ensure consistent product quality, which is crucial for sensitive applications in pharmaceuticals and personal care. While the full integration of AI is still in its nascent stages for many chemical manufacturers, its potential to drive efficiency, innovation, and sustainability across the oleate ester value chain is undeniable.

- Enhanced R&D and new product development through AI-driven molecular modeling and property prediction.

- Optimized production processes, including reaction conditions and yield maximization, via machine learning algorithms.

- Improved supply chain efficiency and resilience through AI-powered demand forecasting and inventory management.

- Advanced quality control and anomaly detection in manufacturing processes using real-time data analysis.

- Development of smart formulations and customized oleate ester blends based on specific application requirements.

Key Takeaways Oleate Ester Market Size & Forecast

The Oleate Ester market is set for substantial growth, driven by an increasing shift towards sustainable and bio-based chemical solutions across multiple end-use industries. The projected CAGR of 7.8% underscores a robust expansion trajectory, indicating healthy demand for these versatile compounds. A primary growth catalyst is the escalating consumer preference for natural ingredients in personal care and cosmetic formulations, where oleate esters serve as excellent emollients, emulsifiers, and spreading agents. Concurrently, the rising adoption of high-performance, environmentally friendly lubricants and metalworking fluids is contributing significantly to market expansion, leveraging the inherent biodegradability and superior lubricity of these esters.

Regional dynamics play a pivotal role, with Asia Pacific expected to emerge as a dominant market due to rapid industrialization, burgeoning personal care markets, and increasing investments in manufacturing capabilities. North America and Europe, while mature, will continue to drive demand for specialized, high-value oleate ester applications, particularly in pharmaceuticals and premium cosmetics, spurred by stringent regulatory environments favoring sustainable products. The market’s resilience will be tested by raw material price volatility and regulatory complexities, yet the overarching trend towards bio-derived products and functional versatility positions oleate esters for sustained growth throughout the forecast period.

- The Oleate Ester market is projected to grow at a robust CAGR of 7.8% from 2025 to 2033, reaching USD 1,602.8 Million by 2033.

- Increasing demand from personal care, cosmetics, and lubricant industries is a primary growth driver.

- The shift towards bio-based and sustainable chemical solutions is a significant market accelerator.

- Asia Pacific is anticipated to be a key growth region due to rapid industrial and consumer market expansion.

- Opportunities exist in novel applications and strategic collaborations focusing on specialized, high-performance formulations.

Oleate Ester Market Drivers Analysis

The global demand for oleate esters is primarily propelled by their versatile applications across numerous industries, coupled with a growing preference for sustainable chemical products. The personal care and cosmetics sector stands out as a significant driver, with oleate esters valued for their emollient, emulsifying, and skin-conditioning properties in lotions, creams, and makeup. This trend is amplified by increasing consumer awareness and demand for natural and bio-derived ingredients, pushing manufacturers to integrate plant-based oleate esters into their formulations. Simultaneously, the lubricants and metalworking fluids industry is increasingly adopting oleate esters due to their superior lubricity, biodegradability, and lower toxicity compared to traditional mineral oil-based alternatives, aligning with stricter environmental regulations and corporate sustainability goals. These sectors collectively underpin a strong and consistent demand for oleate esters globally.

Furthermore, the pharmaceutical industry utilizes oleate esters as excipients, solubilizers, and penetration enhancers in various drug delivery systems, benefiting from their low irritation potential and excellent compatibility with active pharmaceutical ingredients. The expanding pharmaceutical market, particularly in developing regions, consequently contributes to the growth of the oleate ester market. Advancements in food processing and packaging also see oleate esters used as emulsifiers, release agents, and anti-foaming agents, driven by the growth of the processed food industry and the need for improved product quality and shelf life. The multifaceted utility and increasing emphasis on sustainable sourcing across these critical sectors provide a strong foundation for continued market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Demand in Personal Care & Cosmetics | +2.5% | Global, particularly APAC & Europe | Short to Long Term |

| Increasing Adoption in Bio-Lubricants & Metalworking Fluids | +2.0% | North America, Europe, China | Mid to Long Term |

| Growing Preference for Bio-based & Sustainable Chemicals | +1.5% | Global, driven by regulatory push in developed economies | Short to Long Term |

| Expansion of Pharmaceutical & Food Applications | +1.0% | Global, with emphasis on emerging markets | Mid Term |

Oleate Ester Market Restraints Analysis

Despite robust growth, the Oleate Ester market faces several notable restraints that could temper its expansion. One significant challenge is the volatility in raw material prices, particularly for oleic acid derived from vegetable oils like palm, soybean, and sunflower. Fluctuations in agricultural yields, geopolitical events, and global supply chain disruptions can lead to unpredictable pricing for these key feedstocks, directly impacting the production costs of oleate esters and subsequently their market prices. This volatility can squeeze profit margins for manufacturers and make long-term planning difficult, potentially slowing investment in new production capacities. The reliance on agricultural commodities means the market is susceptible to environmental factors and commodity market dynamics.

Another restraint is the stringent regulatory landscape governing the use of chemicals in various end-use industries, particularly in cosmetics, pharmaceuticals, and food & beverages. Compliance with diverse national and international regulations, such as REACH in Europe or FDA guidelines in the US, can be complex and costly for manufacturers. The need for extensive testing, certifications, and adherence to specific purity standards adds to operational expenses and can extend the time-to-market for new products. Furthermore, competition from alternative emollients, lubricants, and emulsifiers, including synthetic esters and other bio-based compounds, poses a threat. While oleate esters offer distinct advantages, the availability of substitutes with similar functionalities at competitive prices can limit market penetration and pricing power, particularly in price-sensitive segments. These factors collectively require manufacturers to strategically manage their supply chains and product portfolios.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices (Oleic Acid) | -1.2% | Global, particularly Asia Pacific (major producers) | Short to Mid Term |

| Stringent Regulatory Landscape & Compliance Costs | -0.8% | Europe, North America | Mid Term |

| Competition from Alternative Chemicals & Substitutes | -0.5% | Global | Short to Mid Term |

| Complex Manufacturing Processes & Energy Intensity | -0.3% | Global | Long Term |

Oleate Ester Market Opportunities Analysis

The Oleate Ester market is ripe with opportunities, particularly driven by the accelerating global shift towards sustainable and environmentally friendly products. The increasing consumer and industrial demand for bio-based and biodegradable chemicals presents a significant avenue for growth, as oleate esters derived from natural sources like vegetable oils align perfectly with these preferences. This trend is creating substantial demand not only in established markets but also in developing economies where environmental consciousness is rapidly rising. Manufacturers investing in green chemistry and sustainable sourcing practices are well-positioned to capitalize on this growing market segment, securing long-term competitive advantages and expanding their market share in niche and premium applications. The development of new and innovative applications for oleate esters further enhances their market potential.

Another key opportunity lies in the expanding applications within emerging economies, particularly in Asia Pacific, Latin America, and the Middle East & Africa. Rapid industrialization, increasing disposable incomes, and the burgeoning growth of personal care, pharmaceutical, and automotive sectors in these regions are fueling demand for versatile chemical compounds like oleate esters. Companies can leverage these markets by establishing local production facilities, forging strategic partnerships, and tailoring products to specific regional needs and regulatory frameworks. Furthermore, continuous research and development into novel oleate ester derivatives with enhanced functional properties, such as improved thermal stability, broader pH compatibility, or specific rheological characteristics, will open up new high-value applications in advanced materials, specialized lubricants, and complex pharmaceutical formulations, securing future growth prospects for the market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Bio-based & Sustainable Products | +1.8% | Global, particularly Europe & North America | Short to Long Term |

| Expansion into Emerging Applications & Niche Markets | +1.5% | Global, driven by R&D | Mid to Long Term |

| Increased Adoption in Emerging Economies (APAC, LATAM) | +1.2% | Asia Pacific, Latin America, MEA | Short to Mid Term |

| Technological Advancements in Esterification Processes | +0.8% | Global | Mid Term |

Oleate Ester Market Challenges Impact Analysis

The Oleate Ester market faces several critical challenges that demand strategic responses from manufacturers and stakeholders. One significant hurdle is the potential for supply chain disruptions, particularly concerning the availability and quality of raw materials like oleic acid. The sourcing of oleic acid, primarily from agricultural products such as palm, soybean, and sunflower oils, makes the supply chain vulnerable to climatic conditions, crop diseases, and geopolitical tensions. Any significant disruption can lead to shortages, price spikes, and an inability to meet demand, directly impacting production schedules and profitability. Ensuring a stable and diversified supply of high-quality raw materials is crucial for maintaining market stability and growth.

Another formidable challenge is the increasing scrutiny over environmental impact and sustainability across the chemical industry. While oleate esters are often promoted as more environmentally friendly alternatives, concerns related to deforestation (for palm oil-derived oleic acid), land use change, and the overall carbon footprint of production processes can pose challenges. Companies must navigate complex sustainability certifications and consumer perceptions, requiring significant investment in transparent sourcing, sustainable manufacturing practices, and robust waste management systems. Furthermore, intense price competition, especially in commodity-grade oleate esters, can erode profit margins and limit investment in innovation. Manufacturers must find a balance between competitive pricing and maintaining high product quality, often necessitating process optimizations and differentiation through specialized high-performance products to overcome these challenges effectively.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Supply Chain Volatility & Disruptions | -1.0% | Global | Short to Mid Term |

| Environmental & Sustainability Concerns (e.g., Palm Oil Sourcing) | -0.7% | Europe, North America, key sourcing regions | Mid to Long Term |

| Intense Price Competition & Profit Margin Erosion | -0.5% | Global, particularly in commodity grades | Short to Mid Term |

| Achieving Consistent Product Quality & Purity for Niche Applications | -0.3% | Global | Long Term |

Oleate Ester Market - Updated Report Scope

This comprehensive market research report on the Oleate Ester market provides an in-depth analysis of market size, trends, drivers, restraints, opportunities, and challenges across various segments and key geographies. It offers strategic insights into market dynamics, competitive landscape, and future growth prospects, leveraging extensive primary and secondary research. The report aims to equip stakeholders with critical data to make informed business decisions, identify emerging opportunities, and develop effective market entry and expansion strategies within the evolving chemical industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 875.4 Million |

| Market Forecast in 2033 | USD 1,602.8 Million |

| Growth Rate | 7.8% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Croda International Plc, KLK Emmerich GmbH, IOI Oleo GmbH, Emery Oleochemicals, BASF SE, Stepan Company, Sasol Limited, Evonik Industries AG, Dow Inc., Esters & Emollients Corp., GreenChem Solutions, Agro-Bio Esters Inc., Specialty Lubricant Technologies, PharmaGrade Oleates Ltd., Cosmetic Ingredients Innovations, SynthEsters Global, Industrial Oils & Chemicals, Bio-Derived Solutions, Advanced Oleo Products, Universal Fatty Esters |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Oleate Ester market is meticulously segmented to provide a granular view of its diverse applications and product forms, enabling a comprehensive understanding of market dynamics and growth opportunities. These segmentations are critical for identifying key demand pockets and emerging trends across different end-use industries and product specifications. By understanding the performance of various oleate ester types, their sources, and their preferred applications, stakeholders can tailor their strategies to target the most lucrative segments and capitalize on specific market needs.

The market is primarily segmented by type, differentiating between various esters such as Methyl Oleate, Ethyl Oleate, Isopropyl Oleate, Butyl Oleate, Glycerol Oleate, and Sorbitan Oleate, each possessing unique properties suitable for distinct applications. Furthermore, the segmentation by application highlights the dominant end-use industries, including personal care and cosmetics, pharmaceuticals, lubricants and metalworking fluids, food and beverages, plastics, textiles, and agriculture. The source-based segmentation (plant-based vs. animal-based) reflects the industry's shift towards sustainable and renewable raw materials, with plant-based sources like soy, palm, sunflower, and rapeseed oleic acid gaining increasing prominence due to environmental concerns and consumer preferences for natural ingredients. This multi-dimensional segmentation allows for a precise analysis of market drivers and growth vectors within the oleate ester landscape.

- By Type:

- Methyl Oleate

- Ethyl Oleate

- Isopropyl Oleate

- Butyl Oleate

- Glycerol Oleate

- Sorbitan Oleate

- Other Oleate Esters

- By Application:

- Personal Care and Cosmetics

- Pharmaceuticals

- Lubricants and Metalworking Fluids

- Food and Beverages

- Plastics

- Textiles

- Agriculture

- Other Industrial Applications

- By Source:

- Plant-based

- Soy-based

- Palm-based

- Sunflower-based

- Rapeseed-based

- Olive-based

- Animal-based

- Plant-based

Regional Highlights

- North America: A mature market characterized by high demand for specialized and high-performance oleate esters in pharmaceuticals, premium personal care, and advanced lubricants. The region also emphasizes sustainable and bio-based solutions, driven by stringent environmental regulations and consumer preferences. The United States and Canada are key contributors to market revenue, focusing on innovation and quality.

- Europe: A leading region in the adoption of bio-based chemicals and sustainable manufacturing practices, largely influenced by REACH regulations and strong environmental policies. Germany, France, and the UK are significant consumers, particularly in the cosmetics, automotive, and industrial sectors, driving demand for eco-friendly lubricant and personal care formulations.

- Asia Pacific (APAC): Expected to exhibit the highest growth rate due to rapid industrialization, burgeoning populations, and increasing disposable incomes. China, India, Japan, and South Korea are major contributors, with booming personal care, pharmaceutical, and automotive industries fueling demand. The region also serves as a key manufacturing hub for oleate esters and their raw materials.

- Latin America: Demonstrates steady growth, primarily driven by expanding personal care and cosmetic industries, particularly in Brazil and Mexico. Increasing industrial activity and a growing focus on sustainable solutions are also contributing to the demand for oleate esters in lubricants and other industrial applications.

- Middle East and Africa (MEA): An emerging market with growth opportunities stemming from infrastructure development, expanding industrial sectors, and increasing demand for personal care products. Investments in manufacturing and diversification away from oil-dependent economies are expected to gradually boost the adoption of oleate esters in various applications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Oleate Ester Market.- Croda International Plc

- KLK Emmerich GmbH

- IOI Oleo GmbH

- Emery Oleochemicals

- BASF SE

- Stepan Company

- Sasol Limited

- Evonik Industries AG

- Dow Inc.

- Esters & Emollients Corp.

- GreenChem Solutions

- Agro-Bio Esters Inc.

- Specialty Lubricant Technologies

- PharmaGrade Oleates Ltd.

- Cosmetic Ingredients Innovations

- SynthEsters Global

- Industrial Oils & Chemicals

- Bio-Derived Solutions

- Advanced Oleo Products

- Universal Fatty Esters

Frequently Asked Questions

What are oleate esters primarily used for?

Oleate esters are versatile chemical compounds predominantly used as emollients and emulsifiers in personal care and cosmetics, as high-performance lubricants and metalworking fluids, and as excipients in pharmaceuticals. Their broad utility also extends to food, plastics, and textile industries.

What is the projected growth rate of the Oleate Ester market?

The Oleate Ester Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033, driven by increasing demand across various industrial applications and a shift towards sustainable chemical solutions.

What are the key drivers of the Oleate Ester market?

Key drivers include the rising demand for bio-based ingredients in personal care, the increasing adoption of oleate esters in high-performance and biodegradable lubricants, and their expanding applications in the pharmaceutical and food industries due to their functional properties.

Which regions are leading in the Oleate Ester market?

Asia Pacific is anticipated to be a major growth region due to rapid industrialization and growing consumer markets. North America and Europe are significant contributors, focusing on high-value applications and sustainable product development.

Are there sustainable options for oleate esters?

Yes, there is a significant market trend towards plant-based oleate esters derived from renewable sources like soy, palm, sunflower, and rapeseed oils, driven by increasing environmental consciousness and demand for sustainable chemical solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted