Offshore Support Vessel Market

Offshore Support Vessel Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706399 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Offshore Support Vessel Market Size

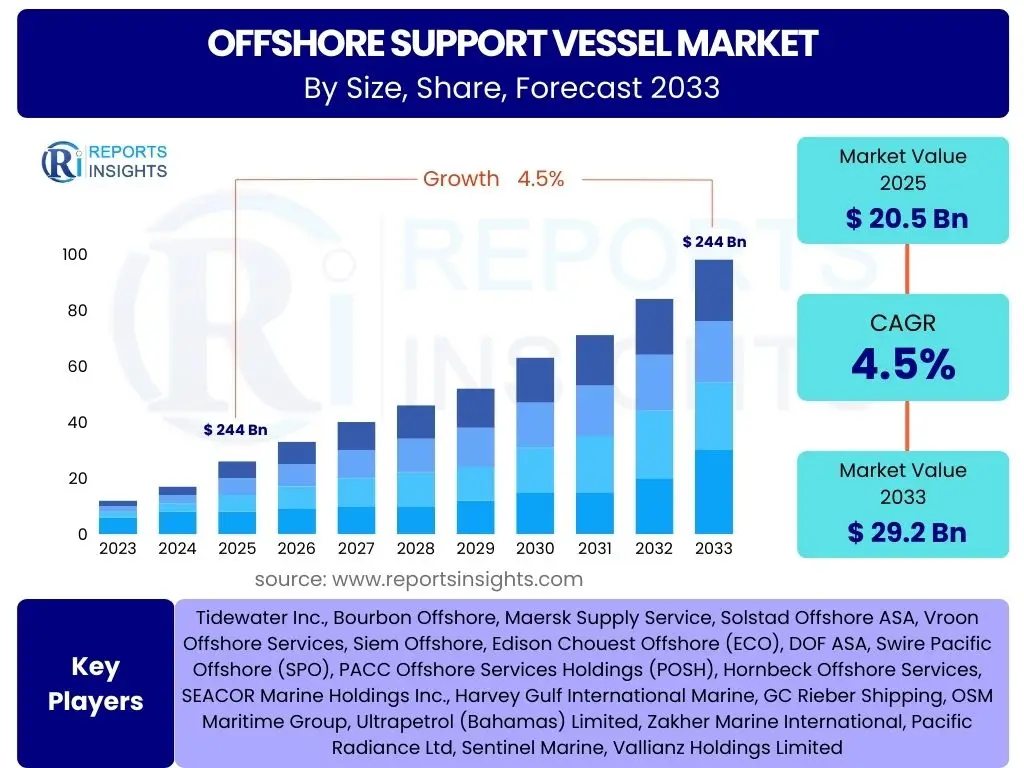

According to Reports Insights Consulting Pvt Ltd, The Offshore Support Vessel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033. The market is estimated at USD 20.5 billion in 2025 and is projected to reach USD 29.2 billion by the end of the forecast period in 2033.

Key Offshore Support Vessel Market Trends & Insights

The Offshore Support Vessel (OSV) market is currently undergoing a significant transformation driven by both traditional energy demands and the burgeoning offshore renewable sector. Industry stakeholders are keen to understand how technological advancements, particularly digitalization and automation, are reshaping operational efficiencies and safety protocols. There is a strong focus on the adoption of sustainable practices and alternative fuels, reflecting a global push towards decarbonization within the maritime industry. Furthermore, the evolving geopolitical landscape and fluctuating energy prices continue to influence investment decisions and fleet deployments.

User inquiries frequently highlight the shift from a predominantly oil and gas-centric market to one with diversified demand sources, including offshore wind farm construction and maintenance, as well as complex subsea activities. The increasing complexity of deepwater exploration and production, coupled with the rising number of decommissioning projects, necessitates more sophisticated and versatile OSVs. These trends collectively point towards a market prioritizing adaptability, technological integration, and environmental compliance as core competitive advantages for vessel operators and service providers.

- Digitalization and remote operations capabilities are enhancing vessel efficiency and reducing operational costs.

- The push for decarbonization is accelerating the adoption of alternative fuels and hybrid propulsion systems.

- Development and deployment of autonomous and semi-autonomous vessels are progressing to improve safety and reduce human error.

- Significant growth in the offshore wind energy sector is creating new demand for specialized support vessels.

- Integration of advanced sensors, data analytics, and artificial intelligence is optimizing vessel performance and predictive maintenance.

AI Impact Analysis on Offshore Support Vessel

The integration of Artificial Intelligence (AI) into the Offshore Support Vessel (OSV) sector is a subject of growing interest, with common user questions focusing on its practical applications, potential benefits, and associated challenges. AI is increasingly being recognized for its capacity to revolutionize operational efficiencies, enhance safety, and drive cost reductions within the maritime industry. Specifically, users are exploring how AI can contribute to predictive maintenance, optimizing voyage planning, and enabling more autonomous vessel operations, thereby reducing human intervention and minimizing risks in hazardous offshore environments.

Beyond operational improvements, the discussion around AI also touches on its role in data analysis for strategic decision-making and environmental compliance. While the potential for improved fuel efficiency through AI-driven routing and real-time performance monitoring is a key attraction, concerns about data security, integration complexities, and the need for a skilled workforce capable of managing AI systems are also prevalent. The industry is navigating the balance between leveraging AI's transformative power and addressing the practicalities and risks associated with its widespread adoption.

- AI-driven predictive maintenance significantly reduces downtime by anticipating equipment failures.

- Optimized voyage planning and dynamic positioning through AI algorithms lead to substantial fuel savings.

- Autonomous navigation systems, powered by AI, enhance safety and reduce the need for large onboard crews.

- Real-time data analytics from AI platforms provide critical insights for operational decision-making and resource allocation.

- Intelligent monitoring systems improve environmental compliance by optimizing emissions and waste management.

Key Takeaways Offshore Support Vessel Market Size & Forecast

Insights into the Offshore Support Vessel (OSV) market size and forecast consistently highlight a period of sustained growth, driven by a confluence of factors including renewed investments in offshore energy and the expanding scope of offshore wind projects. Users frequently inquire about the primary drivers behind this projected growth, with particular emphasis on geographical hotbeds of activity and the specific types of vessels or services expected to see the highest demand. The market's resilience, even amidst geopolitical and economic uncertainties, underscores the foundational role OSVs play in global energy infrastructure and maritime construction.

A key takeaway from market projections is the critical role of technological innovation in shaping future demand and operational paradigms. Forecasts suggest a strong emphasis on more environmentally friendly, efficient, and technologically advanced vessels. This includes vessels equipped with enhanced automation, hybrid propulsion systems, and capabilities tailored for complex subsea operations and specialized offshore wind support. Understanding these shifts is crucial for stakeholders aiming to capitalize on emerging opportunities and navigate the evolving regulatory and technological landscape of the OSV market.

- The Offshore Support Vessel market is poised for steady growth through 2033, driven by diversified energy demands.

- Offshore wind energy development represents a primary growth catalyst, requiring specialized construction and maintenance support vessels.

- Technological advancements, including automation and digitalization, are critical for enhancing operational efficiency and safety across the fleet.

- Increased focus on environmental sustainability is driving the demand for greener, more fuel-efficient OSVs.

- Emerging opportunities are present in offshore decommissioning, subsea mining, and other non-traditional maritime support services.

Offshore Support Vessel Market Drivers Analysis

The Offshore Support Vessel (OSV) market is significantly influenced by several key drivers that propel its growth and evolution. One of the foremost drivers is the enduring global demand for energy, which necessitates ongoing offshore oil and gas exploration, development, and production activities. Despite the global energy transition, conventional offshore resources continue to play a vital role in meeting immediate energy needs, thereby sustaining demand for a range of OSVs including Platform Supply Vessels (PSVs) and Anchor Handling Tug Supply (AHTS) vessels. This continued activity, particularly in regions with established offshore reserves and new frontiers, underpins a substantial portion of the market.

Another powerful driver is the rapid expansion of the offshore wind energy sector. As countries worldwide accelerate their transition to renewable energy sources, large-scale offshore wind farms are being developed, requiring specialized OSVs for construction, installation, maintenance, and repair. This includes vessels such as Service Operation Vessels (SOVs), Crew Transfer Vessels (CTVs), and various types of construction support vessels. Furthermore, increasing offshore decommissioning activities, particularly in mature basins like the North Sea, also contribute to demand for OSVs capable of supporting the dismantling and removal of aging infrastructure. These diverse applications collectively broaden the market's revenue streams and foster innovation.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Energy Demand & Offshore E&P | +1.2% | Middle East & Africa, Latin America | Short to Mid-term (2025-2030) |

| Offshore Wind Farm Development & Maintenance | +1.5% | Europe, Asia Pacific, North America | Long-term (2025-2033) |

| Increasing Offshore Decommissioning Activities | +0.8% | North Sea, Gulf of Mexico | Mid-term (2027-2033) |

| Advancements in Subsea Technology & Operations | +0.7% | Global, Deepwater Regions | Mid to Long-term (2026-2033) |

Offshore Support Vessel Market Restraints Analysis

The Offshore Support Vessel (OSV) market faces several notable restraints that can impede its growth trajectory. A primary concern is the inherent volatility of crude oil and natural gas prices. Fluctuations in energy commodity prices directly impact exploration and production budgets of oil and gas companies, leading to deferred or canceled offshore projects and subsequently reducing demand for OSVs. This price sensitivity introduces significant uncertainty and risk for OSV operators, making long-term investment planning challenging.

Another significant restraint comes from increasingly stringent environmental regulations and climate change policies. Governments worldwide are implementing stricter emissions standards and promoting decarbonization, which necessitates substantial investments in new, greener vessels or retrofitting existing fleets. While beneficial for the environment, these compliance costs can be substantial for OSV companies, potentially affecting profitability and competitiveness, especially for smaller operators. Furthermore, geopolitical tensions and regional conflicts can disrupt offshore operations and shipping lanes, creating an unpredictable operating environment that deters investment and reduces fleet utilization.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Crude Oil & Natural Gas Prices | -0.7% | Global | Short to Mid-term (2025-2028) |

| Stringent Environmental Regulations & Emissions Standards | -0.5% | Europe, North America, Global | Mid to Long-term (2026-2033) |

| High Capital Expenditure and Operating Costs | -0.4% | Global | Long-term (2025-2033) |

| Geopolitical Instability & Supply Chain Disruptions | -0.3% | Select Regional Hotspots | Short-term (2025-2026) |

Offshore Support Vessel Market Opportunities Analysis

The Offshore Support Vessel (OSV) market presents numerous strategic opportunities for growth and diversification. One of the most significant opportunities lies in the burgeoning offshore renewable energy sector, particularly offshore wind. As global electricity demand rises and countries commit to decarbonization, the development of vast offshore wind farms is accelerating. This creates substantial demand for specialized OSVs for turbine installation, cable laying, foundation transport, and ongoing operational maintenance, offering a new, stable revenue stream distinct from the volatile oil and gas market.

Furthermore, technological advancements in vessel design and propulsion offer significant opportunities for innovation and competitive differentiation. The shift towards hybrid, electric, and alternative fuel-powered OSVs not only addresses environmental concerns but also offers long-term operational cost savings and enhanced efficiency. Companies investing in research and development of such next-generation vessels can capture a premium market segment. Additionally, the expansion into niche maritime activities such as deep-sea mining, aquaculture support, and oceanographic research also provides avenues for diversification and leveraging existing vessel capabilities in new, emerging markets.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Offshore Wind Energy Market | +1.8% | Europe, Asia Pacific, North America | Long-term (2025-2033) |

| Development of Autonomous and Hybrid/Electric Vessels | +1.0% | Global | Mid to Long-term (2027-2033) |

| Expansion into New Maritime Sectors (e.g., Deep-sea Mining, Aquaculture) | +0.6% | Asia Pacific, Arctic, Coastal Regions | Long-term (2030-2033) |

| Increased Focus on Digitalization and Data-driven Operations | +0.5% | Global | Mid-term (2026-2031) |

Offshore Support Vessel Market Challenges Impact Analysis

The Offshore Support Vessel (OSV) market is confronted by several significant challenges that necessitate strategic responses from industry players. A prominent challenge is the aging global fleet, which often struggles to meet evolving environmental regulations and demands for greater efficiency. Many older vessels require substantial retrofitting to comply with new standards, or risk becoming obsolete, leading to increased capital expenditure for operators. This issue is compounded by the high cost of new vessel construction, which can deter fleet modernization initiatives.

Another critical challenge is the persistent shortage of skilled labor, including experienced mariners, engineers, and technical personnel. The specialized nature of offshore operations, combined with demographic shifts and competitive industries, makes it difficult to attract and retain qualified professionals. This labor gap can impact operational efficiency, safety standards, and the ability to adopt advanced technologies effectively. Furthermore, the increasing reliance on digital systems and automation introduces heightened cybersecurity risks, making vessels vulnerable to cyberattacks that could compromise navigation, communication, and operational integrity, requiring continuous investment in robust security measures.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Aging Global Fleet and Regulatory Compliance | -0.6% | Global | Mid-term (2026-2031) |

| Shortage of Skilled Workforce and Talent Attrition | -0.5% | Global | Long-term (2025-2033) |

| Cybersecurity Risks to Operational Technology | -0.3% | Global | Long-term (2025-2033) |

| Intense Competition and Market Oversupply in Niche Segments | -0.2% | Select Regional Markets | Short to Mid-term (2025-2029) |

Offshore Support Vessel Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Offshore Support Vessel market, encompassing historical data, current market dynamics, and future projections. The scope includes a thorough examination of market size and growth drivers, restraints, opportunities, and challenges impacting the industry. It offers detailed segmentation analysis across various parameters, provides extensive regional insights, and profiles key companies operating in the competitive landscape, delivering a holistic view for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 20.5 Billion |

| Market Forecast in 2033 | USD 29.2 Billion |

| Growth Rate | 4.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Tidewater Inc., Bourbon Offshore, Maersk Supply Service, Solstad Offshore ASA, Vroon Offshore Services, Siem Offshore, Edison Chouest Offshore (ECO), DOF ASA, Swire Pacific Offshore (SPO), PACC Offshore Services Holdings (POSH), Hornbeck Offshore Services, SEACOR Marine Holdings Inc., Harvey Gulf International Marine, GC Rieber Shipping, OSM Maritime Group, Ultrapetrol (Bahamas) Limited, Zakher Marine International, Pacific Radiance Ltd, Sentinel Marine, Vallianz Holdings Limited |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Offshore Support Vessel (OSV) market is comprehensively segmented to provide a granular understanding of its diverse components and dynamics. This segmentation allows for precise analysis of demand patterns, technological adoption, and regional specificities, enabling stakeholders to identify lucrative niches and tailor their strategies. By dissecting the market based on various operational and functional characteristics, the report illuminates the intricate relationships between vessel types, their specialized functions, the depths at which they operate, and the specific applications they serve across the global energy and marine sectors.

Understanding these segments is crucial for investors, operators, and service providers seeking to optimize their fleet utilization, target emerging opportunities, and navigate competitive pressures. For instance, the distinction between Platform Supply Vessels (PSVs) and Anchor Handling Tug Supply (AHTS) vessels highlights different operational requirements and market demands within the oil and gas sector, while the emergence of dedicated subsea support vessels underscores the growing complexity of underwater operations. This detailed segmentation provides the framework for assessing market attractiveness, forecasting future trends, and informing strategic business development within the dynamic OSV industry.

- Vessel Type: Categorization by the primary design and purpose of the vessel, including Anchor Handling Tug Supply (AHTS) vessels for rig movements, Platform Supply Vessels (PSVs) for cargo transport, Multipurpose Support Vessels (MSVs) for diverse tasks, Subsea Support Vessels for underwater operations, Crew Boats for personnel transfer, and Standby & Rescue Vessels for safety.

- Function: Classification based on the main operational role of the vessel, encompassing drilling support for exploration, production support for ongoing operations, construction support for new infrastructure, maintenance and repair activities, and decommissioning for end-of-life assets.

- Depth: Segmentation according to the typical water depth of operations, differentiating between shallow water, deepwater, and ultra-deepwater environments, each requiring specialized vessel capabilities.

- Application: Division based on the end-use industry or primary sector served, primarily covering the traditional oil and gas industry, the rapidly expanding offshore wind sector, and broader marine construction projects.

Regional Highlights

- North America: A mature market driven by activities in the Gulf of Mexico, with a focus on deepwater oil and gas operations and increasing investment in offshore wind projects along the East Coast. Decommissioning activity is also a significant driver.

- Europe: Leads in offshore wind development, particularly in the North Sea and Baltic Sea, driving demand for specialized construction, installation, and Service Operation Vessels (SOVs). Significant decommissioning activity also exists in the North Sea.

- Asia Pacific (APAC): Emerging as a high-growth region due to increasing energy demand, new oil and gas exploration in Southeast Asia, and aggressive offshore wind development plans in countries like China, Taiwan, and Vietnam.

- Latin America: Characterized by significant offshore oil and gas reserves, particularly in Brazil and Mexico, leading to sustained demand for OSVs to support deepwater exploration and production activities.

- Middle East and Africa (MEA): Experiences robust demand for OSVs driven by ongoing oil and gas production and new developments, particularly in the Arabian Gulf and West Africa, with a strong focus on maintaining existing infrastructure.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Offshore Support Vessel Market.- Tidewater Inc.

- Bourbon Offshore

- Maersk Supply Service

- Solstad Offshore ASA

- Vroon Offshore Services

- Siem Offshore

- Edison Chouest Offshore (ECO)

- DOF ASA

- Swire Pacific Offshore (SPO)

- PACC Offshore Services Holdings (POSH)

- Hornbeck Offshore Services

- SEACOR Marine Holdings Inc.

- Harvey Gulf International Marine

- GC Rieber Shipping

- OSM Maritime Group

- Ultrapetrol (Bahamas) Limited

- Zakher Marine International

- Pacific Radiance Ltd

- Sentinel Marine

- Vallianz Holdings Limited

Frequently Asked Questions

The Offshore Support Vessel (OSV) market generates common user questions centered around defining its scope, understanding vessel types, and the impact of evolving energy landscapes and technology. Inquiries often seek clarity on market drivers, the influence of offshore wind, and technological advancements like AI shaping future operations and growth. These questions highlight a broad interest in both foundational knowledge and forward-looking trends within the sector.What is an Offshore Support Vessel (OSV)?

An Offshore Support Vessel (OSV) is a specialized marine vessel designed to support various activities in the offshore oil and gas, renewable energy, and marine construction industries. OSVs transport supplies, equipment, and personnel, tow and anchor oil rigs, and provide subsea construction and maintenance services.

What are the primary types of OSVs?

Primary OSV types include Platform Supply Vessels (PSVs) for cargo transport, Anchor Handling Tug Supply (AHTS) vessels for towing and anchoring rigs, Multipurpose Support Vessels (MSVs) for diverse tasks, and specialized vessels like Service Operation Vessels (SOVs) for offshore wind farm support, and Crew Transfer Vessels (CTVs).

How is the offshore wind sector influencing the OSV market?

The offshore wind sector is a major growth driver for the OSV market, creating high demand for specialized vessels for turbine installation, cable laying, foundation transport, and ongoing operational maintenance and repair, diversifying the market beyond traditional oil and gas reliance.

What role does technology play in modern OSV operations?

Technology plays a crucial role in modern OSV operations, enabling enhanced efficiency, safety, and environmental performance. This includes digitalization for remote operations, AI for predictive maintenance and optimized routing, hybrid propulsion systems for fuel efficiency, and advanced dynamic positioning for precise maneuvering.

Which regions are key to the OSV market growth?

Key regions driving OSV market growth include Europe, particularly for offshore wind and decommissioning; North America, with active deepwater oil and gas and emerging wind projects; Asia Pacific, due to new energy exploration and substantial offshore wind investments; and Latin America and MEA, driven by ongoing oil and gas production.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted