O Arm Surgical Imaging System Market

O Arm Surgical Imaging System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702278 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

O Arm Surgical Imaging System Market Size

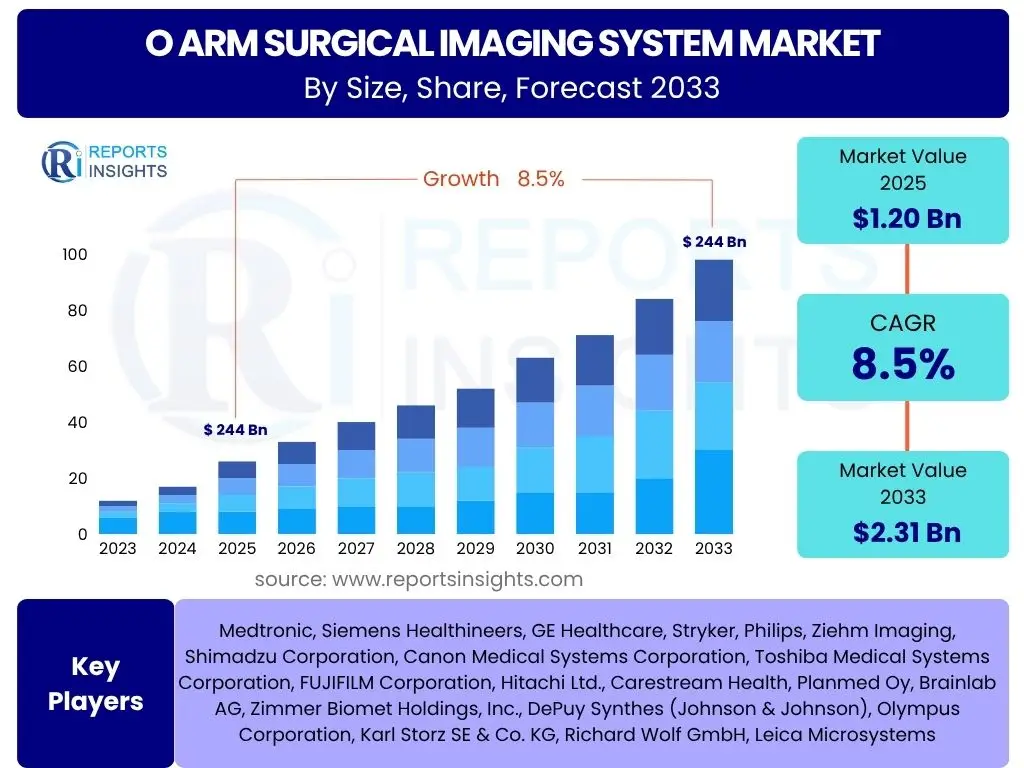

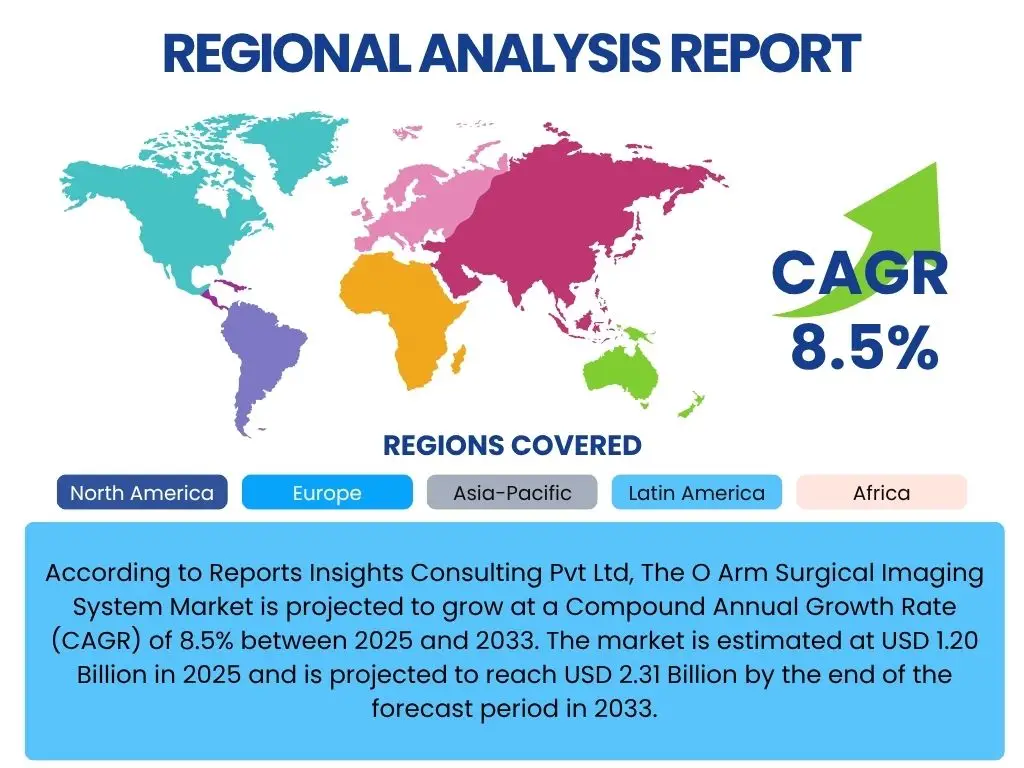

According to Reports Insights Consulting Pvt Ltd, The O Arm Surgical Imaging System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 1.20 Billion in 2025 and is projected to reach USD 2.31 Billion by the end of the forecast period in 2033.

Key O Arm Surgical Imaging System Market Trends & Insights

The O-Arm surgical imaging system market is experiencing significant shifts driven by technological innovation and evolving surgical practices. A prominent trend is the increasing adoption of minimally invasive surgical procedures, where O-Arm systems provide crucial intraoperative 3D imaging, enhancing precision and reducing patient recovery times. There is a growing demand for systems that integrate seamlessly with surgical navigation platforms, offering real-time guidance and improved accuracy, particularly in complex spinal, orthopedic, and neurosurgical interventions. Furthermore, the development of more compact, mobile, and user-friendly O-Arm units is expanding their accessibility and utility across a broader range of clinical settings, including smaller hospitals and ambulatory surgical centers.

Another key insight revolves around the continuous refinement of imaging capabilities, including higher resolution, reduced radiation dose, and faster image acquisition. This not only improves diagnostic quality but also enhances patient and clinician safety, addressing a critical concern in medical imaging. The market is also witnessing a trend towards subscription-based models or flexible financing options, making these high-cost systems more accessible to healthcare providers with varying budget constraints. This financial flexibility, coupled with the proven clinical benefits of O-Arm technology, is accelerating its market penetration globally, especially in emerging economies where healthcare infrastructure is rapidly developing.

- Increasing adoption of minimally invasive surgical techniques.

- Seamless integration with advanced surgical navigation systems.

- Development of compact, mobile, and user-friendly O-Arm units.

- Improvements in image resolution and dose reduction technologies.

- Emergence of flexible financing and subscription models for system acquisition.

AI Impact Analysis on O Arm Surgical Imaging System

The integration of Artificial Intelligence (AI) is poised to revolutionize the O-Arm surgical imaging system market by enhancing diagnostic capabilities, optimizing workflow efficiency, and improving surgical outcomes. Users frequently inquire about AI's role in automating image analysis, such as real-time identification of anatomical structures or potential complications, which can significantly reduce interpretation time and human error. AI algorithms are expected to provide predictive insights, helping surgeons anticipate challenges during complex procedures and personalize treatment plans more effectively. Furthermore, the potential for AI to refine radiation dose management based on patient-specific data, while maintaining image quality, is a major area of interest, addressing concerns about radiation exposure during prolonged surgeries.

Beyond image processing, AI's influence extends to operational aspects of O-Arm systems. It can facilitate predictive maintenance, reducing downtime and ensuring system availability, which is crucial in busy surgical environments. Concerns often arise regarding data privacy and security with the increased reliance on AI processing sensitive patient data, necessitating robust cybersecurity measures. Additionally, the need for comprehensive training for surgical teams to effectively utilize AI-powered features is a key expectation. Despite these considerations, the overarching expectation is that AI will transform O-Arm systems into more intelligent, autonomous, and invaluable tools, driving greater precision and safety in the operating room.

- Automated real-time image analysis for enhanced diagnostic accuracy.

- Optimized surgical planning and guidance through predictive analytics.

- Intelligent dose management systems for reduced radiation exposure.

- Enhanced workflow efficiency through automated calibration and system optimization.

- Predictive maintenance and remote troubleshooting capabilities.

Key Takeaways O Arm Surgical Imaging System Market Size & Forecast

The O-Arm surgical imaging system market is on a robust growth trajectory, demonstrating a significant increase in market size over the forecast period. This expansion is primarily driven by the escalating global demand for advanced intraoperative imaging solutions that enable minimally invasive surgeries with improved precision and patient safety. Healthcare providers are increasingly recognizing the value proposition of O-Arm systems in reducing surgical complications, shortening hospital stays, and enhancing overall surgical efficiency, which collectively contributes to better patient outcomes and cost-effectiveness in the long run. The projected growth underscores a fundamental shift in surgical practice towards technology-assisted interventions, where real-time, high-quality imaging is indispensable.

A crucial takeaway is the anticipated penetration of O-Arm technology into a wider range of surgical specialties beyond its traditional strongholds in spinal and orthopedic surgery, including neurosurgery, trauma, and potentially ENT. This diversification of applications, coupled with continuous technological advancements like AI integration and improved mobility, will further fuel market expansion. Geographically, while mature markets like North America and Europe will continue to be significant contributors due to established healthcare infrastructures and high adoption rates, emerging economies in Asia Pacific and Latin America are expected to exhibit accelerated growth, driven by increasing healthcare expenditure, medical tourism, and a growing patient pool requiring complex surgeries. The market's resilience and adaptability to evolving surgical needs and technological progress are key indicators of its promising future.

- Significant market expansion driven by demand for advanced intraoperative imaging.

- Technological advancements and AI integration are pivotal growth accelerators.

- Broadening application scope across diverse surgical specialties.

- Strong growth anticipated in emerging economies alongside sustained growth in mature markets.

- Increased focus on patient safety, reduced complications, and improved surgical efficiency.

O Arm Surgical Imaging System Market Drivers Analysis

The O-Arm surgical imaging system market is significantly propelled by several key drivers that reflect advancements in medical technology, evolving surgical practices, and increasing healthcare demands. A primary driver is the accelerating shift towards minimally invasive surgical (MIS) procedures across various disciplines, including spinal, orthopedic, and neurosurgery. O-Arm systems provide crucial intraoperative 3D imaging, enabling surgeons to visualize anatomical structures with high precision, verify implant placement in real-time, and detect complications without necessitating additional patient repositioning or transport to a separate imaging suite. This capability directly supports the goals of MIS, which include smaller incisions, reduced blood loss, decreased pain, shorter hospital stays, and faster patient recovery, making O-Arm systems an indispensable tool in modern operating rooms.

Furthermore, the rising global prevalence of chronic conditions requiring surgical intervention, such as degenerative spinal disorders, orthopedic trauma, and complex neurological conditions, is fueling the demand for advanced imaging solutions. As populations age and lifestyles change, the incidence of these conditions increases, leading to a greater volume of surgeries. Alongside this, continuous technological advancements within the O-Arm systems themselves, including improved image quality, reduced radiation dose, faster scan times, and enhanced integration with surgical navigation systems, are making these devices more appealing and clinically effective. Favorable reimbursement policies in key regions also play a vital role, making the acquisition and utilization of these high-cost systems more financially viable for healthcare institutions, thereby encouraging wider adoption and market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Adoption of Minimally Invasive Surgeries | +2.1% | Global, particularly North America, Europe, APAC | Short-term to Long-term |

| Technological Advancements in Imaging and Navigation | +1.8% | Global | Mid-term to Long-term |

| Rising Prevalence of Spinal & Orthopedic Disorders | +1.5% | Global | Mid-term |

| Growing Emphasis on Patient Safety & Reduced Radiation Exposure | +1.2% | Developed Markets (e.g., US, Germany, Japan) | Short-term |

| Favorable Reimbursement Policies and Healthcare Infrastructure Development | +0.9% | North America, Western Europe, Emerging APAC Economies | Mid-term |

O Arm Surgical Imaging System Market Restraints Analysis

Despite the strong growth drivers, the O-Arm surgical imaging system market faces several significant restraints that could impede its expansion. The most prominent restraint is the high initial capital investment required for purchasing and installing O-Arm systems. These advanced imaging devices represent a substantial expenditure for hospitals and surgical centers, making it challenging for smaller facilities or those with budget constraints to acquire them. This high cost extends beyond procurement to include ongoing maintenance, specialized training for staff, and potential upgrades, adding to the total cost of ownership. Such financial barriers can limit adoption, particularly in developing regions where healthcare budgets are often stretched.

Another considerable restraint involves the inherent risks associated with radiation exposure, both for patients and surgical staff. Although manufacturers are continuously working on dose reduction technologies, the use of X-ray-based imaging still carries a risk, which can lead to concerns and impact adoption rates, especially for procedures requiring multiple scans or for pediatric patients. Furthermore, the steep learning curve and the need for highly specialized training for surgeons and technicians to operate these complex systems efficiently can be a barrier. Insufficient trained personnel, particularly in regions with limited access to specialized medical education, can slow down the integration and utilization of O-Arm technology in clinical practice. Regulatory hurdles and the complexity of gaining approvals in various jurisdictions also pose challenges, potentially delaying market entry for new innovations and increasing development costs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Cost and Installation Requirements | -1.8% | Global, more pronounced in Emerging Economies | Short-term to Mid-term |

| Risks Associated with Radiation Exposure | -1.5% | Global | Short-term to Mid-term |

| Requirement for Specialized Training and Skilled Personnel | -1.2% | Global, especially Developing Regions | Mid-term |

| Stringent Regulatory Approval Processes | -0.8% | Global, particularly North America, Europe | Short-term |

| Limited Reimbursement in Certain Geographies/Procedures | -0.5% | Varies by Country/Region | Mid-term |

O Arm Surgical Imaging System Market Opportunities Analysis

The O-Arm surgical imaging system market is presented with numerous opportunities that can significantly accelerate its growth and expand its application scope. One major opportunity lies in the continued development and expansion of hybrid operating rooms (ORs). These integrated environments combine advanced imaging capabilities, such as those offered by O-Arms, with traditional surgical functionalities, creating a single space where complex procedures can be performed with maximum precision and real-time imaging guidance. The rising trend of hybrid ORs, driven by the increasing complexity of cardiovascular, neurosurgical, and orthopedic interventions, creates a natural demand for versatile intraoperative imaging solutions like the O-Arm, offering a seamless workflow and improved patient safety.

Another significant opportunity is the diversification of O-Arm system applications beyond traditional spinal and orthopedic surgeries. There is an emerging potential for these systems in other surgical specialties, including trauma surgery, ear, nose, and throat (ENT) procedures, and even specific general surgeries where precise anatomical visualization and real-time confirmation are critical. Manufacturers can leverage this by developing application-specific software and hardware enhancements. Furthermore, growth opportunities exist in emerging economies, where healthcare infrastructure is rapidly developing, and there is a growing demand for advanced medical technologies due to increasing healthcare expenditure and medical tourism. Partnerships with local distributors, tailored financing solutions, and educational initiatives can help unlock these untapped markets. Finally, the integration of advanced technologies like Artificial Intelligence (AI) and Machine Learning (ML) for enhanced image processing, automated planning, and predictive analytics presents a transformative opportunity, potentially leading to a new generation of smart O-Arm systems.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Hybrid Operating Rooms | +2.0% | Global, particularly Developed Markets | Mid-term to Long-term |

| Expansion into New Surgical Specialties (e.g., Trauma, ENT) | +1.7% | Global | Mid-term |

| Increasing Healthcare Expenditure in Emerging Economies | +1.5% | Asia Pacific, Latin America, Middle East | Mid-term to Long-term |

| Integration of AI and Advanced Analytics | +1.3% | Global | Long-term |

| Demand for Mobile and Compact Systems | +0.9% | Global, especially smaller facilities and ASCs | Short-term |

O Arm Surgical Imaging System Market Challenges Impact Analysis

The O-Arm surgical imaging system market faces several challenges that require strategic navigation to sustain growth and widespread adoption. One significant challenge is the intense competition among key market players. The market is characterized by the presence of a few dominant manufacturers alongside specialized niche players, leading to fierce competition in terms of product innovation, pricing strategies, and market share. This competitive landscape can exert downward pressure on prices, reduce profit margins, and necessitate continuous investment in research and development to maintain a competitive edge, which can be particularly challenging for smaller entrants.

Another critical challenge is the rapid pace of technological obsolescence. As new imaging technologies and surgical techniques emerge, O-Arm systems must continuously evolve to remain relevant. This requires significant ongoing investment in R&D to integrate the latest advancements, such as AI capabilities, enhanced robotics, and improved image detectors, which can be a financial strain for manufacturers. Furthermore, ensuring consistent quality and overcoming logistical hurdles in global supply chains, particularly for complex medical devices like O-Arms, poses a challenge. Regulatory changes and increasing scrutiny over medical device safety and efficacy also add complexity, requiring manufacturers to adapt swiftly to new compliance standards across different regions. Economic downturns or healthcare budget cuts in certain countries can also impact procurement decisions by hospitals, leading to delayed or reduced investments in high-value capital equipment like O-Arm systems, posing a macroeconomic challenge to market growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition and Pricing Pressures | -1.6% | Global | Short-term to Mid-term |

| Rapid Technological Obsolescence and R&D Investment | -1.3% | Global | Mid-term |

| Supply Chain Disruptions and Manufacturing Complexities | -1.0% | Global | Short-term |

| Strict Regulatory Landscape and Compliance Costs | -0.7% | North America, Europe, China | Short-term |

| Healthcare Budget Constraints and Economic Volatility | -0.4% | Global, particularly regions with public healthcare funding | Short-term to Mid-term |

O Arm Surgical Imaging System Market - Updated Report Scope

This market report provides an in-depth analysis of the O-Arm Surgical Imaging System Market, covering historical data, current market trends, and future projections. It offers a comprehensive overview of market size, growth drivers, restraints, opportunities, and challenges, alongside a detailed segmentation analysis by product type, application, end-use, and geographical region. The report also includes competitive landscape analysis, profiling key market players and their strategies, to offer a holistic view of the market dynamics and provide actionable insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.20 Billion |

| Market Forecast in 2033 | USD 2.31 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic, Siemens Healthineers, GE Healthcare, Stryker, Philips, Ziehm Imaging, Shimadzu Corporation, Canon Medical Systems Corporation, Toshiba Medical Systems Corporation, FUJIFILM Corporation, Hitachi Ltd., Carestream Health, Planmed Oy, Brainlab AG, Zimmer Biomet Holdings, Inc., DePuy Synthes (Johnson & Johnson), Olympus Corporation, Karl Storz SE & Co. KG, Richard Wolf GmbH, Leica Microsystems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The O-Arm surgical imaging system market is meticulously segmented to provide a detailed understanding of its diverse components and drivers. This comprehensive segmentation allows for a granular analysis of market dynamics, enabling stakeholders to identify key growth areas, competitive landscapes, and strategic opportunities across different product categories, application domains, and end-user facilities. Each segment reflects unique demand patterns, technological preferences, and regional adoption rates, collectively shaping the overall market trajectory. Understanding these segments is crucial for manufacturers to tailor their product offerings, for healthcare providers to make informed investment decisions, and for investors to identify lucrative market niches.

The segmentation by type distinguishes between various O-Arm system configurations, each offering specific advantages in terms of mobility, integration, and operational flexibility. Application-based segmentation highlights the primary surgical procedures where O-Arm systems are predominantly utilized, showcasing their clinical versatility and impact on patient outcomes across different medical specialties. Furthermore, the end-use segmentation categorizes the primary healthcare facilities adopting these systems, reflecting varied purchasing power, infrastructure capabilities, and procedural volumes. This multi-faceted approach to market segmentation provides a robust framework for assessing market potential and strategic positioning within the O-Arm surgical imaging landscape.

- By Type:

- Mobile O-Arm

- Fixed O-Arm

- Hybrid O-Arm

- By Application:

- Spinal Surgery

- Orthopedic Trauma

- Neurosurgery

- ENT Surgery

- Other Surgeries (e.g., General, Vascular)

- By End-use:

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Specialty Clinics

Regional Highlights

- North America: This region holds a dominant share in the O-Arm surgical imaging system market, primarily driven by a well-established healthcare infrastructure, high adoption rates of advanced medical technologies, and significant investments in research and development. The presence of leading market players, favorable reimbursement policies, and a high volume of complex spinal and orthopedic surgeries further contribute to its leading position. The United States, in particular, is a major contributor to market revenue due to its advanced healthcare facilities and continuous technological upgrades.

- Europe: Europe represents a mature and substantial market for O-Arm systems, characterized by increasing healthcare expenditure, a growing elderly population prone to orthopedic and spinal disorders, and a strong emphasis on precision medicine. Countries like Germany, France, and the UK are key markets, driven by technological advancements and the adoption of minimally invasive surgical techniques. Stringent regulatory frameworks also ensure high-quality standards for medical devices, fostering trust and adoption.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market, propelled by rapidly developing healthcare infrastructure, increasing medical tourism, a large patient pool, and rising awareness regarding advanced surgical procedures. Countries such as China, India, Japan, and South Korea are experiencing significant investments in healthcare, leading to the adoption of advanced imaging solutions. Economic growth, expanding access to healthcare, and a shift towards modern surgical practices are key drivers.

- Latin America: This region is an emerging market for O-Arm surgical imaging systems, with countries like Brazil, Mexico, and Argentina showing promising growth. Factors contributing to this growth include improving healthcare facilities, increasing government initiatives to modernize healthcare, and a growing demand for advanced surgical interventions. However, market penetration is relatively slower compared to developed regions due to budget constraints and infrastructure limitations.

- Middle East and Africa (MEA): The MEA region is witnessing gradual adoption, primarily driven by increasing healthcare spending, a rise in medical tourism in countries like UAE and Saudi Arabia, and efforts to enhance medical infrastructure. While the market is currently smaller, increasing awareness, government support for healthcare development, and the establishment of advanced surgical centers are creating new opportunities for O-Arm system manufacturers.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the O Arm Surgical Imaging System Market.- Medtronic

- Siemens Healthineers

- GE Healthcare

- Stryker

- Philips

- Ziehm Imaging

- Shimadzu Corporation

- Canon Medical Systems Corporation

- Toshiba Medical Systems Corporation

- FUJIFILM Corporation

- Hitachi Ltd.

- Carestream Health

- Planmed Oy

- Brainlab AG

- Zimmer Biomet Holdings, Inc.

- DePuy Synthes (Johnson & Johnson)

- Olympus Corporation

- Karl Storz SE & Co. KG

- Richard Wolf GmbH

- Leica Microsystems

Frequently Asked Questions

Analyze common user questions about the O Arm Surgical Imaging System market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is an O-Arm surgical imaging system?

An O-Arm surgical imaging system is an advanced medical device that provides high-quality 2D and 3D images of a patient's anatomy during surgery. It is a mobile, intraoperative fluoroscopic imaging system that allows surgeons to acquire real-time, comprehensive views, enhancing precision, particularly in complex spinal, orthopedic, and neurosurgical procedures, without moving the patient.

What are the primary applications of O-Arm systems?

The primary applications of O-Arm systems are in spinal surgery for pedicle screw placement verification, orthopedic trauma for complex fracture fixation, and neurosurgery for brain and spine procedures. They are increasingly being used in other specialties like ENT surgery and general surgery where accurate intraoperative imaging is crucial for precise intervention.

How does AI enhance O-Arm technology?

AI enhances O-Arm technology by enabling automated real-time image analysis, providing predictive insights for surgical planning, optimizing radiation dose management for patient safety, and improving workflow efficiency through intelligent system calibration and maintenance. AI can help surgeons interpret complex images faster and more accurately, leading to better surgical outcomes.

What factors are driving the growth of the O-Arm market?

The growth of the O-Arm market is primarily driven by the increasing global adoption of minimally invasive surgical procedures, continuous technological advancements in imaging and navigation systems, the rising prevalence of spinal and orthopedic disorders, and a growing emphasis on enhancing patient safety and surgical precision. Favorable reimbursement policies in key regions also contribute significantly.

What are the key challenges in the O-Arm surgical imaging market?

Key challenges in the O-Arm surgical imaging market include the high initial capital investment required for these advanced systems, the inherent risks associated with radiation exposure for patients and staff, the need for highly specialized training for clinical users, and intense market competition which can lead to pricing pressures and necessitate continuous research and development.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted