Non Gluten Food Market

Non Gluten Food Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705118 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

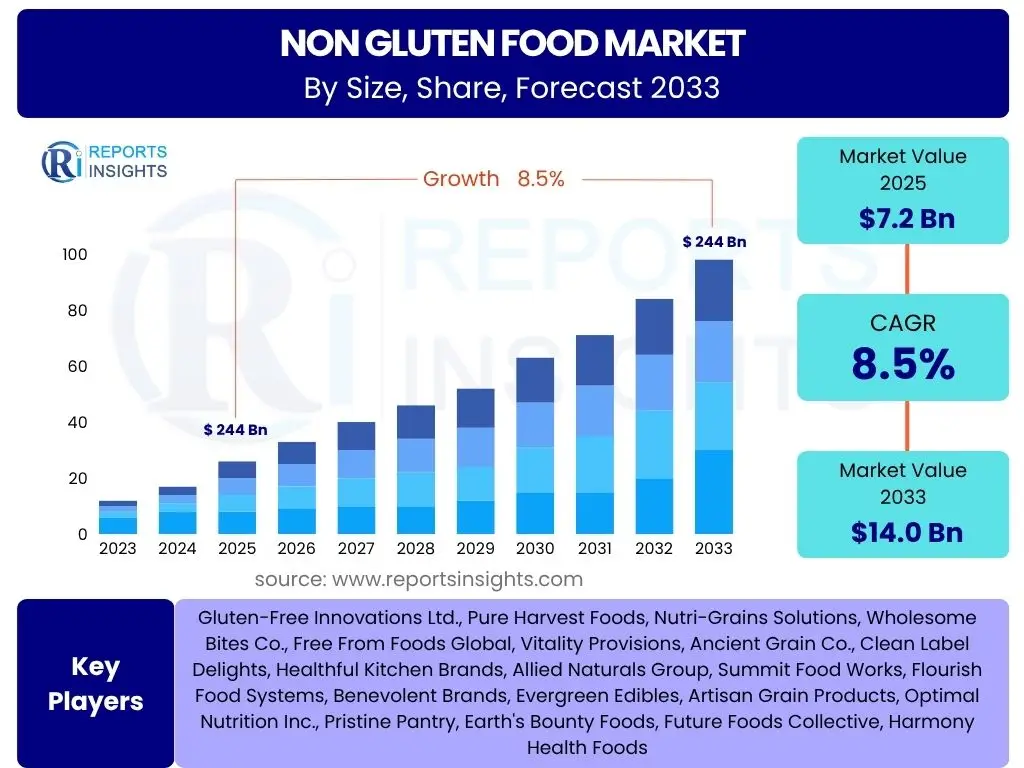

Non Gluten Food Market Size

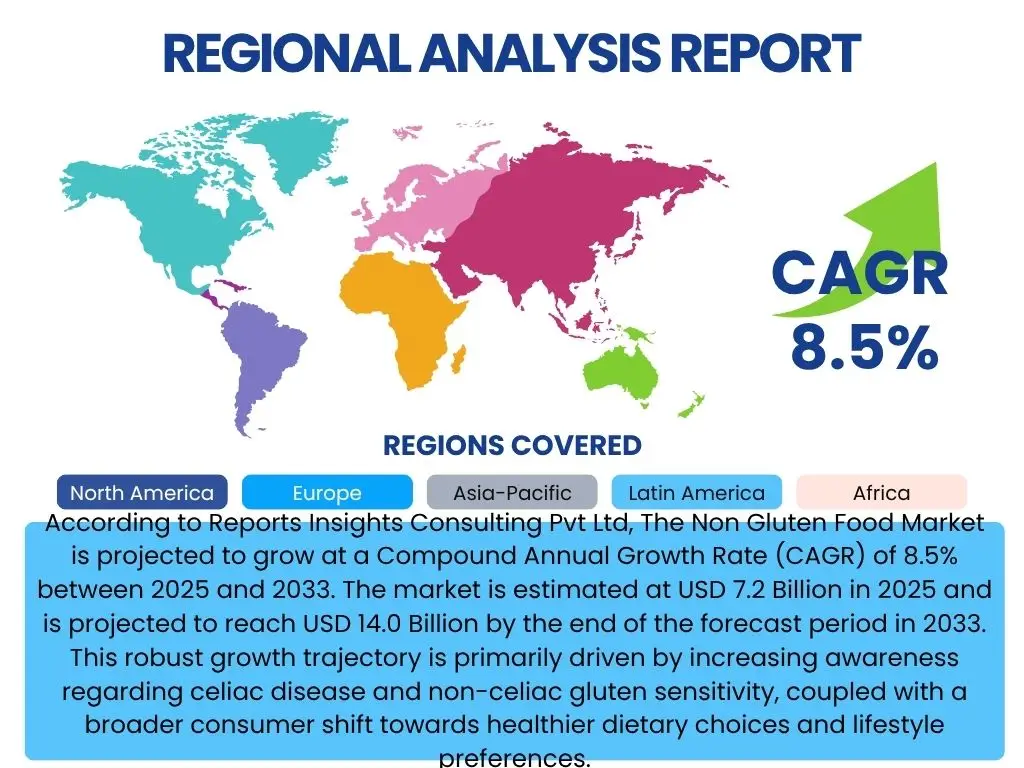

According to Reports Insights Consulting Pvt Ltd, The Non Gluten Food Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 7.2 Billion in 2025 and is projected to reach USD 14.0 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by increasing awareness regarding celiac disease and non-celiac gluten sensitivity, coupled with a broader consumer shift towards healthier dietary choices and lifestyle preferences.

The market's expansion is further supported by significant innovation in product development, leading to a wider availability of palatable and diverse non-gluten food options across various categories, including bakery, snacks, and ready meals. Manufacturers are continually investing in research and development to improve the taste, texture, and nutritional profile of non-gluten products, making them more appealing to a wider consumer base beyond those with medical conditions. This includes targeting health-conscious consumers who perceive non-gluten products as generally healthier or beneficial for digestive wellness.

Geographically, while North America and Europe currently represent the largest market shares due to higher diagnosis rates and well-established health food trends, emerging economies in Asia Pacific and Latin America are anticipated to exhibit rapid growth. This growth in developing regions is fueled by rising disposable incomes, urbanization, and increasing exposure to Western dietary trends, alongside growing awareness campaigns about gluten-related disorders. The market's resilience and adaptive nature suggest continued strong performance over the forecast period.

Key Non Gluten Food Market Trends & Insights

Common user questions regarding non-gluten food market trends often revolve around consumer adoption drivers, emerging product categories, and the influence of broader health and wellness movements. Consumers are increasingly seeking transparency in food labeling, nutritional benefits beyond just being gluten-free, and products that offer comparable taste and texture to their gluten-containing counterparts. There is a strong interest in how sustainable sourcing and clean label initiatives intersect with the non-gluten market, as well as the impact of plant-based diets on non-gluten product innovation. Furthermore, users frequently inquire about the expanding availability of non-gluten options in mainstream retail and foodservice channels.

The market is witnessing a significant shift from niche dietary requirement to a mainstream lifestyle choice for a growing segment of consumers. This is propelling innovation across various food categories, including functional non-gluten products fortified with added nutrients, probiotics, or fiber. The increasing sophistication of ingredient sourcing and processing technologies is enabling manufacturers to create more diverse and appealing products, addressing past criticisms regarding taste and texture. Furthermore, the rise of e-commerce platforms has significantly expanded the accessibility of specialty non-gluten products, allowing smaller brands to reach a broader audience and offering consumers greater choice and convenience.

- Broadened Consumer Appeal: Transition from niche dietary requirement to mainstream health and wellness trend.

- Product Innovation: Expansion into new categories like functional foods, ready-to-eat meals, and diverse snack options.

- Improved Sensory Attributes: Enhanced taste, texture, and aroma of non-gluten products rivaling traditional alternatives.

- Clean Label & Transparency: Growing demand for products with minimal ingredients and clear allergen information.

- E-commerce Growth: Increased accessibility and variety through online retail channels.

- Plant-Based Synergy: Strong intersection with the plant-based movement, offering dual benefits for consumers.

AI Impact Analysis on Non Gluten Food

User inquiries regarding the impact of Artificial Intelligence (AI) on the non-gluten food market typically focus on how AI can enhance product development, supply chain efficiency, and consumer personalization. Questions often arise about AI's role in ingredient sourcing, optimizing recipes for taste and texture, predicting consumer preferences, and ensuring product safety and quality. There is also interest in AI-driven solutions for managing cross-contamination risks and improving traceability throughout the supply chain. Consumers and businesses alike are keen to understand if AI can lead to more affordable non-gluten options or accelerate the introduction of novel, high-quality products.

AI is poised to revolutionize the non-gluten food sector by enabling more precise and efficient operations. In product development, AI algorithms can analyze vast datasets of ingredient properties and consumer feedback to formulate new recipes that optimize taste, texture, and nutritional profiles, significantly reducing development cycles. This includes identifying optimal non-gluten flours and starches, and predicting their interactions in complex food matrices. Furthermore, AI can enhance supply chain management by forecasting demand more accurately, optimizing inventory levels, and streamlining logistics, which can lead to reduced waste and improved cost-efficiency in sourcing and distribution. For manufacturers, this means a more agile response to market trends and consumer needs.

Beyond product creation and supply chain, AI holds immense potential for personalized nutrition and consumer engagement within the non-gluten market. AI-powered platforms can analyze individual dietary needs, preferences, and health goals to recommend tailored non-gluten meal plans or product suggestions, fostering a more personalized consumer experience. Additionally, AI-driven quality control systems, using computer vision and sensor technologies, can detect contaminants or deviations in product quality with high accuracy, ensuring compliance with strict non-gluten standards and enhancing consumer trust. This technological integration is expected to drive both innovation and operational excellence in the coming years.

- Accelerated Product Development: AI algorithms optimize recipes for taste, texture, and nutritional value.

- Enhanced Supply Chain Efficiency: AI improves demand forecasting, inventory management, and logistics for ingredients.

- Personalized Nutrition: AI-driven recommendations for non-gluten meal plans and product selections.

- Advanced Quality Control: AI-powered systems detect contaminants and ensure product integrity, minimizing cross-contamination risks.

- Market Trend Prediction: AI analyzes consumer data to identify emerging preferences and accelerate market responsiveness.

Key Takeaways Non Gluten Food Market Size & Forecast

Common user questions concerning key takeaways from the non-gluten food market size and forecast often focus on the longevity and sustainability of the market's growth, the primary drivers underpinning this expansion, and the areas presenting the most significant opportunities. Users are keen to understand if the market is nearing saturation or if there's still ample room for new entrants and continued innovation. They frequently inquire about the consumer segments contributing most to growth and the regional disparities in market development. The potential for further diversification of product offerings and the role of health awareness in shaping future demand are also recurring themes.

The non-gluten food market is poised for sustained, robust growth throughout the forecast period, reflecting a profound and ongoing shift in dietary patterns and health consciousness worldwide. Its expansion is not merely a transient fad but a fundamental response to increasing diagnoses of gluten-related conditions and a broader embrace of health-and-wellness lifestyles. The market's strength lies in its diversified product portfolio, which extends far beyond basic necessities to encompass a wide array of gourmet, convenience, and functional food options, catering to diverse consumer preferences and occasions. This adaptability ensures continued relevance and demand across multiple consumer segments.

A significant takeaway is the market's increasing penetration into mainstream retail channels and foodservice, making non-gluten options more accessible than ever before. This widespread availability, coupled with continuous improvements in product quality and taste, is dismantling barriers to adoption and attracting new consumers. Regional variations in growth highlight untapped potential in emerging economies, where rising awareness and disposable incomes are expected to fuel substantial market expansion. Overall, the non-gluten food market represents a dynamic and resilient segment of the food industry, characterized by continuous innovation and a strong consumer-driven demand.

- Sustained Growth Trajectory: Market to experience consistent expansion driven by health awareness and dietary shifts.

- Diversified Product Portfolio: Broad range of offerings, from staple alternatives to innovative gourmet items.

- Mainstream Integration: Increasing availability in conventional supermarkets and restaurants.

- Global Expansion: Significant growth opportunities in emerging markets alongside established regions.

- Consumer-Centric Innovation: Focus on improving taste, texture, and nutritional value to meet evolving demands.

Non Gluten Food Market Drivers Analysis

The Non Gluten Food Market is primarily propelled by a confluence of escalating health concerns, evolving consumer preferences, and significant product innovations. A fundamental driver is the rising incidence and diagnosis rates of celiac disease and non-celiac gluten sensitivity, which necessitate strict adherence to gluten-free diets. Beyond medical necessities, a growing number of consumers are voluntarily adopting non-gluten diets due to perceived health benefits such as improved digestion, reduced inflammation, and increased energy levels, contributing significantly to market expansion. This voluntary adoption is often influenced by health and wellness trends disseminated through social media and health advocacy groups.

Furthermore, increased disposable incomes in developing regions enable consumers to afford premium non-gluten products, while aggressive marketing and educational campaigns by manufacturers and health organizations enhance awareness and drive demand. The continuous innovation in food technology has also played a crucial role, allowing manufacturers to overcome historical challenges related to the taste and texture of non-gluten products. This has resulted in a wider range of palatable and appealing options across various food categories, making the transition to a non-gluten diet more convenient and enjoyable for consumers. The convenience of readily available non-gluten options in various retail formats further supports this growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Incidence of Celiac Disease & Gluten Sensitivity | +2.1% | North America, Europe | 2025-2033 (Mid to Long-term) |

| Increasing Health & Wellness Awareness | +1.8% | Global | 2025-2033 (Mid to Long-term) |

| Product Innovation & Diversification | +1.5% | Global | 2025-2033 (Mid to Long-term) |

| Growth of E-commerce & Online Retail | +1.0% | Global | 2025-2033 (Short to Mid-term) |

| Rising Disposable Incomes in Emerging Economies | +0.8% | Asia Pacific, Latin America | 2025-2033 (Mid to Long-term) |

| Strategic Marketing & Education Campaigns | +0.7% | Global | 2025-2033 (Short to Mid-term) |

| Cross-Contamination Prevention Technologies | +0.6% | Global | 2025-2033 (Mid-term) |

Non Gluten Food Market Restraints Analysis

Despite robust growth, the Non Gluten Food Market faces several significant restraints that can impede its full potential. A primary challenge is the generally higher cost of non-gluten products compared to their traditional counterparts. This price premium is often due to specialized production processes, the cost of gluten-free ingredients, and dedicated manufacturing facilities to prevent cross-contamination. This higher price point can deter price-sensitive consumers, particularly in regions with lower disposable incomes, limiting market penetration and mass adoption.

Another notable restraint is the ongoing challenge of achieving desirable taste and texture profiles in some non-gluten products. While significant advancements have been made, certain non-gluten items, especially bakery products, can still be perceived as inferior in sensory attributes compared to their gluten-containing equivalents. This can lead to consumer dissatisfaction and a reluctance to make repeat purchases. Furthermore, the risk of cross-contamination during manufacturing, processing, and even at the retail level remains a persistent concern for individuals with severe gluten allergies, necessitating stringent protocols that add to production complexity and cost.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Production Costs & Premium Pricing | -1.5% | Global | 2025-2033 (Mid to Long-term) |

| Perceived Inferior Taste & Texture | -0.9% | Global | 2025-2030 (Short to Mid-term) |

| Risk of Cross-Contamination | -0.7% | Global | 2025-2033 (Mid to Long-term) |

| Limited Awareness in Developing Regions | -0.5% | MEA, parts of Asia Pacific | 2025-2033 (Mid to Long-term) |

| Competition from "Free-From" Categories | -0.4% | Global | 2025-2033 (Mid to Long-term) |

Non Gluten Food Market Opportunities Analysis

The Non Gluten Food Market presents substantial opportunities for innovation and expansion, particularly driven by evolving consumer demands and technological advancements. One significant area of opportunity lies in the burgeoning trend of personalized nutrition, where consumers seek products tailored to their specific dietary needs and health goals. This opens doors for specialized non-gluten offerings that cater to multiple dietary restrictions or incorporate functional ingredients, such as added probiotics or fiber, appealing to a broader health-conscious demographic.

Emerging markets across Asia Pacific, Latin America, and the Middle East and Africa offer significant untapped potential. As these regions experience economic growth and increasing urbanization, awareness of dietary health issues and western dietary trends are on the rise, creating a new consumer base for non-gluten products. Furthermore, the expansion of the foodservice industry, including restaurants, cafes, and institutional catering, provides a robust channel for increasing the availability and visibility of non-gluten options, moving them beyond specialty stores into everyday dining experiences. Collaborations between non-gluten food producers and mainstream food service providers can unlock considerable market share.

The synergy with the rapidly growing plant-based food movement represents another powerful opportunity. Many non-gluten consumers are also exploring or adhering to plant-based diets, creating a demand for products that are both non-gluten and plant-derived. This dual appeal allows manufacturers to tap into multiple consumer segments with single product lines, maximizing market reach. Continuous research and development into novel non-gluten ingredients and advanced processing techniques can further enhance product quality and variety, addressing current sensory limitations and paving the way for truly innovative and delicious non-gluten offerings that will attract even more consumers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Markets | +1.9% | Asia Pacific, Latin America, MEA | 2025-2033 (Mid to Long-term) |

| Synergy with Plant-Based Food Trends | +1.7% | Global | 2025-2033 (Mid to Long-term) |

| Development of Functional Non-Gluten Products | +1.4% | North America, Europe | 2025-2033 (Mid-term) |

| Growth in Foodservice & Horeca Sector | +1.1% | Global | 2025-2033 (Mid to Long-term) |

| Technological Advancements in Ingredient Science | +0.9% | Global | 2025-2033 (Mid to Long-term) |

Non Gluten Food Market Challenges Impact Analysis

The Non Gluten Food Market faces several inherent challenges that demand strategic navigation from industry participants. A significant hurdle is the complexity of maintaining a fully gluten-free supply chain, from sourcing raw materials to final packaging. The risk of cross-contamination with gluten-containing grains during farming, storage, transport, and processing is ever-present, requiring stringent testing protocols and dedicated facilities. This complexity often translates to higher operational costs and can limit the pool of eligible suppliers, making it challenging to scale production efficiently while adhering to strict safety standards required for consumer trust and regulatory compliance.

Another formidable challenge is regulatory harmonization and enforcement across different regions. While major markets have established gluten-free labeling standards, variations exist, and enforcement can differ, leading to potential confusion for international trade and consumer trust. Furthermore, despite advancements, some consumers remain skeptical about the taste, texture, or nutritional value of non-gluten alternatives, particularly in categories traditionally reliant on gluten for structure, such as bread and pasta. Overcoming this skepticism requires continuous innovation and effective communication strategies to highlight product quality and benefits, ensuring consumer satisfaction and repeat purchases. Intense competition from conventional food products and other "free-from" categories also poses a challenge, requiring non-gluten brands to differentiate effectively in a crowded market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Supply Chain Management & Cross-Contamination Risks | -1.2% | Global | 2025-2033 (Mid to Long-term) |

| Maintaining Taste and Texture Parity | -0.8% | Global | 2025-2030 (Short to Mid-term) |

| Stringent Regulatory Compliance & Labeling | -0.6% | Global (varies by region) | 2025-2033 (Mid to Long-term) |

| Consumer Skepticism & Perception Barriers | -0.5% | Global | 2025-2033 (Mid to Long-term) |

| High Competition from Conventional Products | -0.4% | Global | 2025-2033 (Mid to Long-term) |

Non Gluten Food Market - Updated Report Scope

This report provides an in-depth analysis of the Non Gluten Food Market, offering a comprehensive overview of its current landscape, growth drivers, restraints, opportunities, and challenges. It delves into market sizing and forecasts, providing crucial insights into expected market progression. The scope encompasses detailed segmentation analysis across various product types, distribution channels, and regional markets, highlighting key trends and competitive dynamics. The report aims to equip stakeholders with actionable intelligence for strategic decision-making and market positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 7.2 Billion |

| Market Forecast in 2033 | USD 14.0 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Gluten-Free Innovations Ltd., Pure Harvest Foods, Nutri-Grains Solutions, Wholesome Bites Co., Free From Foods Global, Vitality Provisions, Ancient Grain Co., Clean Label Delights, Healthful Kitchen Brands, Allied Naturals Group, Summit Food Works, Flourish Food Systems, Benevolent Brands, Evergreen Edibles, Artisan Grain Products, Optimal Nutrition Inc., Pristine Pantry, Earth's Bounty Foods, Future Foods Collective, Harmony Health Foods |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Non Gluten Food Market is extensively segmented to provide granular insights into its diverse components, allowing for a detailed understanding of consumer preferences, product performance, and regional dynamics. This comprehensive segmentation helps identify high-growth areas and specific market niches, enabling businesses to tailor their strategies effectively. The market is broadly categorized by product type, source of ingredients, distribution channel, and end-user, each offering unique opportunities and challenges for stakeholders.

Within product types, bakery products and snacks continue to dominate due to their widespread consumption and continuous innovation in taste and texture. However, categories like ready meals and dairy alternatives are experiencing significant growth as consumers seek convenience and diversified options. The source segmentation highlights the shift towards alternative grains, nuts, and seeds as primary ingredients, driven by both dietary needs and nutritional benefits. Distribution channels illustrate the increasing importance of online retail alongside traditional brick-and-mortar stores, reflecting changing purchasing habits. Finally, the end-user segmentation differentiates between individual consumers and the expanding foodservice sector, both crucial to market development.

- By Product Type:

- Bakery Products

- Bread

- Cakes

- Cookies

- Pastries

- Muffins

- Snacks

- Chips

- Crackers

- Pretzels

- Bars

- Dairy Alternatives

- Meats & Seafood

- Ready Meals

- Pasta & Noodles

- Beverages

- Other Processed Foods

- Flours

- Mixes

- Breakfast Cereals

- Soups

- Bakery Products

- By Source:

- Grains

- Rice

- Corn

- Quinoa

- Buckwheat

- Millet

- Sorghum

- Oats (certified GF)

- Legumes

- Nuts

- Seeds

- Others (Potatoes, Tapioca)

- Grains

- By Distribution Channel:

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

- Foodservice (Restaurants, Cafes, Institutional)

- By End-User:

- Individual Consumers

- Foodservice Industry

Regional Highlights

- North America: This region holds the largest market share, driven by high awareness of celiac disease and gluten sensitivity, well-established health and wellness trends, and significant product innovation. The presence of major market players and a strong distribution network further contribute to its dominance. Consumer demand for diverse and convenient non-gluten options is consistently high.

- Europe: Europe represents a mature market with substantial consumer awareness and a strong preference for natural and organic non-gluten products. Countries like the UK, Germany, and Italy show robust growth, supported by national and EU-level initiatives promoting gluten-free labeling and availability. Traditional bakery sectors are increasingly adapting to offer non-gluten alternatives.

- Asia Pacific (APAC): Expected to be the fastest-growing region, fueled by increasing disposable incomes, urbanization, and a growing understanding of dietary health. The adoption of Western dietary habits and the rising prevalence of lifestyle diseases are driving demand. While still nascent in some areas, markets like China, India, and Australia are showing significant expansion potential.

- Latin America: This region is an emerging market with increasing health consciousness and growing consumer awareness of gluten-related issues. Economic development and rising disposable incomes are contributing to the demand for non-gluten products, particularly in Brazil, Mexico, and Argentina. The market is characterized by a gradual shift from basic staples to processed and convenience non-gluten foods.

- Middle East and Africa (MEA): Currently a smaller market, but exhibiting nascent growth driven by increasing health awareness, a growing expatriate population, and rising disposable incomes in select countries. Imports of non-gluten products are significant, and there's a growing interest in local production as awareness spreads. Opportunities exist for educational campaigns and targeted product introductions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Non Gluten Food Market.- Gluten-Free Innovations Ltd.

- Pure Harvest Foods

- Nutri-Grains Solutions

- Wholesome Bites Co.

- Free From Foods Global

- Vitality Provisions

- Ancient Grain Co.

- Clean Label Delights

- Healthful Kitchen Brands

- Allied Naturals Group

- Summit Food Works

- Flourish Food Systems

- Benevolent Brands

- Evergreen Edibles

- Artisan Grain Products

- Optimal Nutrition Inc.

- Pristine Pantry

- Earth's Bounty Foods

- Future Foods Collective

- Harmony Health Foods

Frequently Asked Questions

What is driving the growth of the Non Gluten Food Market?

The Non Gluten Food Market's growth is primarily driven by increasing diagnoses of celiac disease and non-celiac gluten sensitivity, a broader consumer shift towards healthier lifestyles, and continuous innovation in non-gluten product development, improving taste and variety.

What are the key challenges faced by the Non Gluten Food Market?

Key challenges include higher production costs leading to premium pricing, the persistent challenge of achieving optimal taste and texture parity with gluten-containing foods, and the critical need to prevent cross-contamination throughout the supply chain.

Which regions offer the most significant growth opportunities for non-gluten foods?

Emerging economies in Asia Pacific and Latin America present the most significant growth opportunities, driven by rising disposable incomes, increasing health awareness, and the adoption of Western dietary trends. North America and Europe remain strong, mature markets.

How is technology impacting the Non Gluten Food Market?

Technology, particularly AI, is impacting the market by accelerating new product development through optimized ingredient formulation, enhancing supply chain efficiency, enabling personalized nutrition recommendations, and improving quality control to ensure product safety.

What types of non-gluten products are gaining popularity?

Beyond traditional bakery and snack items, non-gluten ready meals, dairy alternatives, and functional non-gluten products (e.g., fortified with fiber or probiotics) are gaining significant popularity due to consumer demand for convenience, nutritional benefits, and diversified dietary options.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted