Nickel Market

Nickel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700686 | Last Updated : July 26, 2025 |

Format : ![]()

![]()

![]()

![]()

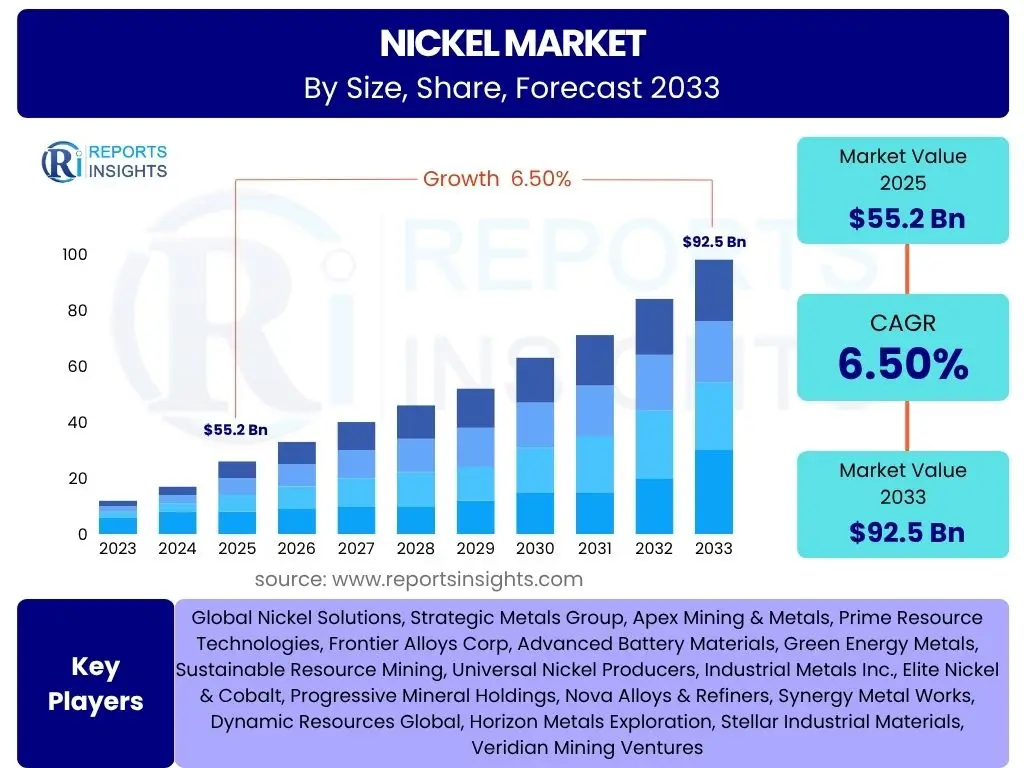

Nickel Market Size

Nickel Market is projected to grow at a Compound annual growth rate (CAGR) of 6.5% between 2025 and 2033, valued at USD 55.2 billion in 2025 and is projected to grow by USD 92.5 billion by 2033 the end of the forecast period.

Key Nickel Market Trends & Insights

The global nickel market is currently experiencing dynamic shifts driven by evolving industrial demands and technological advancements. Key trends shaping its trajectory include the exponential rise in electric vehicle battery production, a sustained demand from the stainless steel sector, and increasing focus on sustainable sourcing and recycling initiatives. Furthermore, geopolitical considerations are influencing supply chain diversification and investment patterns, while advancements in mining and processing technologies aim to enhance efficiency and reduce environmental impact. These interwoven trends highlight a market in transition, adapting to new growth vectors and sustainability imperatives.

- Surging demand from Electric Vehicle (EV) battery manufacturing.

- Consistent growth in the stainless steel production sector.

- Increasing emphasis on nickel recycling and circular economy principles.

- Technological advancements in nickel extraction and processing.

- Diversification of global nickel supply chains.

- Growing investments in high-purity nickel projects.

- Rising geopolitical influence on raw material supply.

AI Impact Analysis on Nickel

Artificial Intelligence (AI) is poised to revolutionize the nickel industry by enhancing efficiency, optimizing resource utilization, and fostering innovation across the value chain. From geological exploration to refining processes and demand forecasting, AI-driven solutions offer unprecedented analytical capabilities. This technological integration is enabling more precise mining operations, predictive maintenance for machinery, and intelligent management of complex supply networks, ultimately leading to significant operational cost reductions and improved output quality. The strategic adoption of AI tools is becoming a critical differentiator for market participants seeking to gain a competitive edge in a rapidly evolving global landscape.

- Optimized geological exploration and resource mapping through AI algorithms.

- Enhanced efficiency in mining operations via predictive analytics and automation.

- AI-powered process optimization in smelting and refining for improved yield.

- Advanced demand forecasting and supply chain management with machine learning.

- Development of novel nickel alloys and materials using AI-driven material discovery.

- Predictive maintenance for mining and processing equipment, reducing downtime.

Key Takeaways Nickel Market Size & Forecast

- The global nickel market is projected for robust growth, driven primarily by battery electric vehicle expansion.

- Stainless steel production remains a foundational demand driver, ensuring market stability.

- Technological innovation in extraction and processing methods is enhancing resource efficiency.

- Increased focus on sustainable and ethical sourcing is influencing investment and supply dynamics.

- Geopolitical factors and trade policies significantly impact global nickel supply and price volatility.

- Emerging markets in Asia Pacific are expected to lead both consumption and production growth.

- Recycling initiatives are gaining prominence, contributing to a circular economy for nickel.

- The market's future trajectory is closely tied to advancements in renewable energy storage technologies.

Nickel Market Drivers Analysis

The global nickel market's robust growth is fundamentally propelled by the escalating demand from key industrial sectors. The rapid expansion of the electric vehicle (EV) industry, in particular, stands out as a paramount driver, with nickel being a critical component in high-performance lithium-ion batteries. This surge is complemented by the consistent and indispensable demand from the stainless steel sector, which relies heavily on nickel for its corrosion resistance and durability properties. Furthermore, widespread infrastructure development globally, particularly in emerging economies, necessitates increasing volumes of nickel for construction, machinery, and various industrial applications.

Beyond these established sectors, the burgeoning renewable energy storage market, including grid-scale battery systems, is opening new avenues for nickel consumption. The aerospace and defense industries also contribute significantly, requiring nickel-based superalloys for their high-temperature and strength characteristics. The continued industrialization and urbanization in developing regions further underscore the pervasive need for nickel across diverse manufacturing and infrastructure projects, collectively fostering a sustained upward trajectory for the market.

Innovation in nickel production and processing, alongside growing investment in advanced material research, also serves as an underlying driver. These advancements aim to improve efficiency, reduce environmental impact, and expand the utility of nickel in novel applications. The confluence of these factors creates a dynamic and growth-oriented landscape for the global nickel market, attracting significant investment and fostering technological evolution to meet future demands.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Electric Vehicle (EV) Battery Demand | +2.5% | Global, particularly Asia Pacific (China, South Korea, Japan), Europe, North America | Long-term (2025-2033) |

| Growth in Stainless Steel Production | +1.8% | Asia Pacific (China, India), Europe, North America | Medium-term (2025-2030) |

| Infrastructure Development & Construction | +0.9% | Emerging Economies (India, Southeast Asia, Africa), China | Medium to Long-term |

| Renewable Energy Storage Solutions | +0.7% | Global, especially North America, Europe, Asia Pacific | Long-term |

| Increasing Use in Aerospace & Defense | +0.3% | North America, Europe, Asia Pacific | Consistent, Long-term |

| Industrialization in Emerging Economies | +0.6% | India, Southeast Asia, parts of Africa and Latin America | Medium to Long-term |

| Technological Advancements in Alloys | +0.5% | Global, R&D concentrated in developed economies | Continuous, Long-term |

Nickel Market Restraints Analysis

Despite its significant growth prospects, the global nickel market faces several inherent restraints that could temper its expansion. One of the most prominent challenges is the inherent price volatility of nickel on international commodity markets. Fluctuations are often driven by speculative trading, geopolitical events, and shifts in supply-demand dynamics, making long-term planning and investment uncertain for both producers and consumers. This unpredictability can deter new market entrants and impact the profitability of existing operations.

Environmental regulations and escalating concerns over the ecological footprint of mining and processing activities also pose significant restraints. Governments and international bodies are imposing stricter rules on emissions, waste management, and land use, particularly for high-energy and water-intensive nickel extraction methods like laterite processing. Compliance with these regulations often requires substantial capital investment in new technologies and processes, increasing operational costs and potentially slowing down project development or expansion plans.

Furthermore, geopolitical instability in key nickel-producing regions presents a considerable supply risk. Disruptions due to political unrest, trade disputes, or resource nationalism can severely impact global supply chains, leading to shortages and further price spikes. High energy costs, particularly for energy-intensive smelting and refining operations, also act as a constraint, squeezing profit margins and making less efficient operations economically unviable. Lastly, the potential for substitution by other materials in certain applications, driven by cost or performance considerations, remains a long-term threat that could limit nickel's market penetration in specific niches.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Nickel Price Volatility | -1.2% | Global Commodity Markets | Short to Medium-term |

| Strict Environmental Regulations | -0.8% | Europe, North America, increasingly Asia Pacific (Indonesia, Philippines) | Medium to Long-term |

| Geopolitical Instability in Key Producing Regions | -0.7% | Indonesia, Russia, Philippines, New Caledonia | Short-term, Event-driven |

| High Energy Costs for Production | -0.6% | Global, impacting high-energy intensity operations | Medium-term |

| Technological Advancements in Material Substitution | -0.4% | Global, R&D focused in developed economies | Long-term |

Nickel Market Opportunities Analysis

The global nickel market is ripe with diverse opportunities that can significantly accelerate its growth trajectory. A major area of potential lies in the burgeoning battery recycling sector. As the volume of electric vehicles and consumer electronics grows, the demand for sustainable and cost-effective methods to recover nickel from spent batteries is increasing. This not only mitigates reliance on primary mining but also aligns with global circular economy goals, creating a robust secondary market for nickel that offers significant environmental and economic advantages.

Beyond traditional applications, the emergence of green hydrogen production and storage technologies presents a novel opportunity for nickel. Nickel-based catalysts and alloys are crucial in electrolyzers and fuel cells, components vital for the nascent hydrogen economy. As the world transitions towards cleaner energy sources, the role of nickel in supporting this shift is expected to expand considerably. Furthermore, ongoing research and development in advanced alloys are continually discovering new applications for nickel in high-performance materials used in demanding environments like renewable energy infrastructure, medical devices, and specialized industrial machinery.

While controversial, the long-term prospect of deep-sea mining represents a potential future opportunity for nickel supply, provided environmental concerns can be adequately addressed through sustainable practices and robust regulatory frameworks. This avenue could unlock vast untapped reserves. Lastly, the continuous innovation in electronics and consumer goods provides a steady, though smaller, stream of new applications for nickel, driven by the need for durable, corrosion-resistant, and high-performance materials in these rapidly evolving sectors. These multifaceted opportunities collectively underscore the market's dynamic potential for expansion beyond its current core drivers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Nickel Battery Recycling | +1.5% | Global, prominent in Europe, North America, Asia Pacific | Long-term (2028-2033) |

| Growth in Green Hydrogen Production | +0.8% | Europe, North America, Australia, parts of Asia | Medium to Long-term |

| Development of Advanced Nickel Alloys | +0.6% | Global, R&D hubs in developed economies | Continuous, Long-term |

| New Applications in Electronics & Consumer Goods | +0.4% | Global, driven by technological innovation | Consistent, Medium-term |

| Sustainable Mining and Processing Innovations | +0.3% | Global, particularly in traditional mining regions | Long-term |

Nickel Market Challenges Impact Analysis

The global nickel market faces a complex array of challenges that can impede its otherwise promising growth trajectory. Significant among these is the inherent volatility of supply chains, particularly exacerbated by the concentrated nature of primary nickel production and refining in a few key regions. Geopolitical tensions, trade protectionism, and logistics bottlenecks can cause abrupt disruptions, leading to supply deficits or surpluses that destabilize prices and impact manufacturing schedules for end-use industries. This fragility necessitates greater diversification and resilience within the supply network.

Environmental, Social, and Governance (ESG) pressures represent another formidable challenge. Stakeholders, including investors, consumers, and regulatory bodies, are increasingly demanding more sustainable and ethical mining practices. This includes reducing carbon emissions, minimizing ecological impact, ensuring responsible waste disposal, and upholding labor standards. Meeting these stringent ESG criteria often requires substantial capital investment in new technologies and operational overhauls, which can increase production costs and slow down project development if not managed effectively.

Furthermore, the high capital expenditure required for new nickel mining and processing projects acts as a significant barrier to entry and expansion. Developing new mines or expanding existing ones involves multi-billion-dollar investments and lengthy approval processes, making it difficult to quickly respond to sudden shifts in demand. This long lead time can create periods of undersupply. Additionally, labor shortages, particularly for skilled workers in remote mining locations, and ongoing technological advancements in alternative materials or battery chemistries (e.g., sodium-ion batteries) pose competitive threats, potentially eroding nickel's market share in specific applications over the long term. Addressing these multifaceted challenges requires strategic foresight, sustained investment, and collaborative efforts across the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Bottlenecks & Disruptions | -1.0% | Global, impacting key trading routes and production hubs | Short to Medium-term |

| Increasing ESG Compliance Costs | -0.9% | Global, particularly Western markets and major producers | Medium to Long-term |

| High Capital Expenditure for New Projects | -0.7% | Global, impacting greenfield and brownfield expansions | Long-term |

| Labor Shortages and Skill Gaps | -0.5% | Major mining regions (Australia, Canada, Indonesia) | Medium-term |

| Technological Advancements in Alternatives | -0.3% | Global, R&D focused in advanced economies | Long-term |

Nickel Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global nickel market, offering critical insights into its current status and future projections. It meticulously examines market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. The report is designed to equip stakeholders with actionable intelligence for strategic decision-making, providing a detailed understanding of market dynamics, competitive landscape, and emerging trends impacting the nickel industry from 2019 through 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 55.2 billion |

| Market Forecast in 2033 | USD 92.5 billion |

| Growth Rate | 6.5% from 2025 to 2033 |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Nickel Solutions, Strategic Metals Group, Apex Mining & Metals, Prime Resource Technologies, Frontier Alloys Corp, Advanced Battery Materials, Green Energy Metals, Sustainable Resource Mining, Universal Nickel Producers, Industrial Metals Inc., Elite Nickel & Cobalt, Progressive Mineral Holdings, Nova Alloys & Refiners, Synergy Metal Works, Dynamic Resources Global, Horizon Metals Exploration, Stellar Industrial Materials, Veridian Mining Ventures |

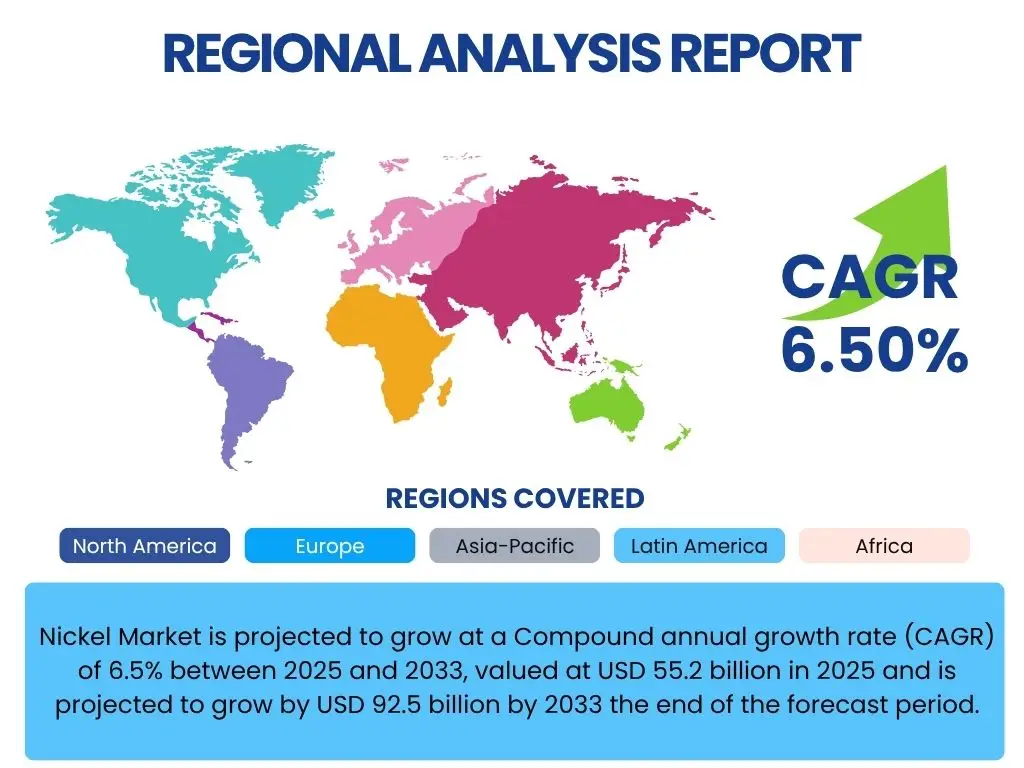

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global nickel market is extensively segmented to provide a granular understanding of its diverse components, allowing for precise market analysis and strategic planning. These segmentations enable stakeholders to identify niche opportunities, understand demand patterns, and assess competitive landscapes within specific market areas. The primary classifications revolve around the type of nickel produced, its myriad applications across various industries, and the forms in which it is primarily traded. The segmentation by type distinguishes between Class I and Class II nickel, reflecting the purity levels and intended uses. Class I nickel, known for its high purity (typically 99.8% or more), is predominantly used in applications demanding high-grade material, such as batteries for electric vehicles and specialized alloys. Class II nickel, with lower purity, finds its primary application in stainless steel production and nickel pig iron. Understanding these types is crucial for producers to align their output with market demand and for consumers to select appropriate grades for their manufacturing processes. Application-based segmentation highlights the diverse end-use industries driving nickel consumption. Stainless steel remains the largest application, leveraging nickel's corrosion resistance and strength. However, the fastest-growing segment is batteries, particularly lithium-ion batteries for EVs and energy storage systems, which require high-purity nickel. Other significant applications include various alloys used in aerospace, industrial machinery, and consumer goods, as well as electroplating for corrosion protection and decorative finishes. Minor applications encompass catalysts, pigments, coinage, and various chemical uses, showcasing nickel's versatility. Finally, the market is also segmented by the form of nickel, which includes Ferro Nickel, Nickel Pig Iron (NPI), and Refined Nickel. Ferro nickel and NPI are primarily used in stainless steel production, offering cost-effective nickel units. Refined nickel, available as cathodes, briquettes, or powders, serves higher-purity applications like battery manufacturing and specialty alloys. This multi-faceted segmentation provides a comprehensive framework for understanding the intricacies of the nickel market, allowing for targeted analysis and strategic insights across the entire value chain.- By Type:

- Class I Nickel: Characterized by high purity (typically 99.8% or more), this type is essential for demanding applications. It includes forms like cathodes, briquettes, and powders.

- Applications: Primarily used in EV batteries, specialty chemicals, electroplating, and superalloys where purity is critical.

- Class II Nickel: This category encompasses nickel with lower purity levels, often found in forms like nickel pig iron (NPI) and ferronickel.

- Applications: Predominantly consumed by the stainless steel industry due to its cost-effectiveness and suitability for bulk production.

- Class I Nickel: Characterized by high purity (typically 99.8% or more), this type is essential for demanding applications. It includes forms like cathodes, briquettes, and powders.

- By Application:

- Stainless Steel: The largest end-use segment, where nickel imparts corrosion resistance, ductility, and strength. Essential for construction, automotive, and consumer goods.

- Batteries: A rapidly expanding segment driven by the electric vehicle (EV) revolution and energy storage systems. Includes lithium-ion batteries (NMC, NCA chemistries) and nickel-metal hydride (NiMH) batteries.

- Alloys: Nickel is a key component in various alloys, including:

- Superalloys: Used in aerospace, gas turbines, and high-temperature industrial applications due to extreme heat and corrosion resistance.

- Castings: For durable and wear-resistant components.

- Steels: Beyond stainless steel, used in certain high-strength and low-temperature applications.

- Electroplating: Provides a decorative and protective finish for various components, enhancing corrosion resistance and hardness.

- Other: Includes diverse uses such as catalysts in chemical processes, pigments, coinage, and specialized chemical compounds.

- By Form:

- Ferro Nickel: An alloy of iron and nickel, primarily used as a raw material in stainless steel production.

- Nickel Pig Iron (NPI): A lower-grade, cost-effective substitute for refined nickel in stainless steel production, predominantly produced in China and Indonesia.

- Refined Nickel: High-purity nickel in various forms like:

- Cathodes: Produced through electrolysis, high purity, used in batteries and high-end alloys.

- Briquettes: Compacted nickel powder, used in a variety of high-pgrade applications.

- Powders: Used in specialized applications like additive manufacturing, catalysts, and chemicals.

Regional Highlights

The global nickel market exhibits distinct regional dynamics, influenced by varying levels of industrialization, resource availability, technological advancements, and regulatory landscapes. Understanding these regional highlights is crucial for identifying key growth pockets and strategic investment opportunities. Asia Pacific, particularly countries like China and Indonesia, stands out as a dominant force in both nickel production and consumption, driven by its extensive stainless steel industry and burgeoning electric vehicle battery manufacturing capacity. North America and Europe, while having significant industrial and manufacturing bases, are increasingly focused on sustainable sourcing, recycling initiatives, and advanced nickel applications, particularly in the aerospace, defense, and electric vehicle sectors. Latin America, with its rich mineral resources, contributes significantly to global nickel supply, while the Middle East and Africa are emerging as important regions for future mining developments and supply chain diversification. Each region presents a unique blend of opportunities and challenges that shape the global nickel market's trajectory.- Asia Pacific (APAC): The largest and fastest-growing region in the global nickel market, driven primarily by China's extensive stainless steel production and Indonesia's surging nickel pig iron (NPI) and battery-grade nickel output.

- China: Dominates nickel consumption for stainless steel and is a major player in EV battery manufacturing, creating massive demand for high-purity nickel. Its industrial expansion continues to fuel demand across various sectors.

- Indonesia: A global leader in nickel ore production and a rapidly growing producer of NPI and increasingly battery-grade nickel, leveraging its rich laterite deposits. Government policies support downstream processing.

- South Korea & Japan: Key players in the EV battery supply chain and advanced electronics manufacturing, requiring high-grade nickel. Focus on technology and sustainable sourcing.

- India: Growing industrialization and infrastructure development are boosting demand for stainless steel and other nickel-containing alloys.

- Europe: A significant consumer of nickel, particularly for specialty steels, alloys, and the rapidly expanding EV battery sector. Strong emphasis on sustainability, recycling, and responsible sourcing.

- Germany: A major automotive manufacturing hub and industrial powerhouse, driving demand for nickel in EVs and high-performance alloys.

- Finland & Norway: Key nickel producers in Europe, focusing on sustainable mining practices and high-purity nickel production.

- North America: Exhibits robust demand from stainless steel, aerospace, and defense industries, with increasing focus on EV battery manufacturing and domestic supply chain resilience.

- United States: Large market for stainless steel, superalloys, and a burgeoning EV production capacity, necessitating secure nickel supply. Investments in battery gigafactories are a key driver.

- Canada: A significant global producer of nickel, particularly Class I nickel, with ongoing exploration and development projects.

- Latin America: Important for nickel supply, with countries like Brazil being major producers. Focus on mining expansion and addressing infrastructure challenges.

- Brazil: A prominent nickel producer, contributing to global supply, especially for the stainless steel market.

- Middle East & Africa (MEA): Emerging as regions for future nickel resource development and downstream processing, attracting investment due to untapped mineral wealth.

- South Africa: A notable producer of nickel, primarily as a by-product of platinum group metals mining.

Top Key Players:

The market research report covers the analysis of key stake holders of the Nickel Market. Some of the leading players profiled in the report include -- Global Nickel Solutions

- Strategic Metals Group

- Apex Mining & Metals

- Prime Resource Technologies

- Frontier Alloys Corp

- Advanced Battery Materials

- Green Energy Metals

- Sustainable Resource Mining

- Universal Nickel Producers

- Industrial Metals Inc.

- Elite Nickel & Cobalt

- Progressive Mineral Holdings

- Nova Alloys & Refiners

- Synergy Metal Works

- Dynamic Resources Global

- Horizon Metals Exploration

- Stellar Industrial Materials

- Veridian Mining Ventures

- Zenith Metals Processing

- Aurora Nickel Systems

Frequently Asked Questions:

What is the primary driver of nickel demand?

The primary driver of nickel demand is the rapidly expanding electric vehicle (EV) battery sector, particularly for high-performance lithium-ion batteries. While traditional applications like stainless steel manufacturing remain significant, the growth in EV production is the most dynamic force shaping the nickel market.How is nickel used in Electric Vehicle (EV) batteries?

In Electric Vehicle (EV) batteries, nickel is a crucial component of the cathode material, especially in lithium-ion battery chemistries such as Nickel Manganese Cobalt (NMC) and Nickel Cobalt Aluminum (NCA). Its high energy density allows for longer driving ranges and improved battery performance, making it essential for high-performance EV applications.What are the main types of nickel available in the market?

The main types of nickel available in the market are Class I nickel and Class II nickel. Class I nickel has high purity (typically 99.8% or more) and is used in batteries and specialty alloys. Class II nickel has lower purity and is primarily used in stainless steel production, often in forms like nickel pig iron (NPI) and ferro nickel.What are the key challenges facing the nickel market?

Key challenges facing the nickel market include price volatility on global commodity exchanges, stringent environmental regulations increasing production costs, geopolitical instability impacting supply chains, and the substantial capital expenditure required for new mining and processing projects. Additionally, potential material substitution in some applications poses a long-term challenge.Which region dominates global nickel production and consumption?

The Asia Pacific (APAC) region currently dominates both global nickel production and consumption. This is primarily driven by significant nickel mining and processing activities in countries like Indonesia and the Philippines, coupled with massive demand from industrial sectors, particularly stainless steel and EV battery manufacturing, in China, South Korea, and Japan.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted