Neo and Challenger Bank Market

Neo and Challenger Bank Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701300 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

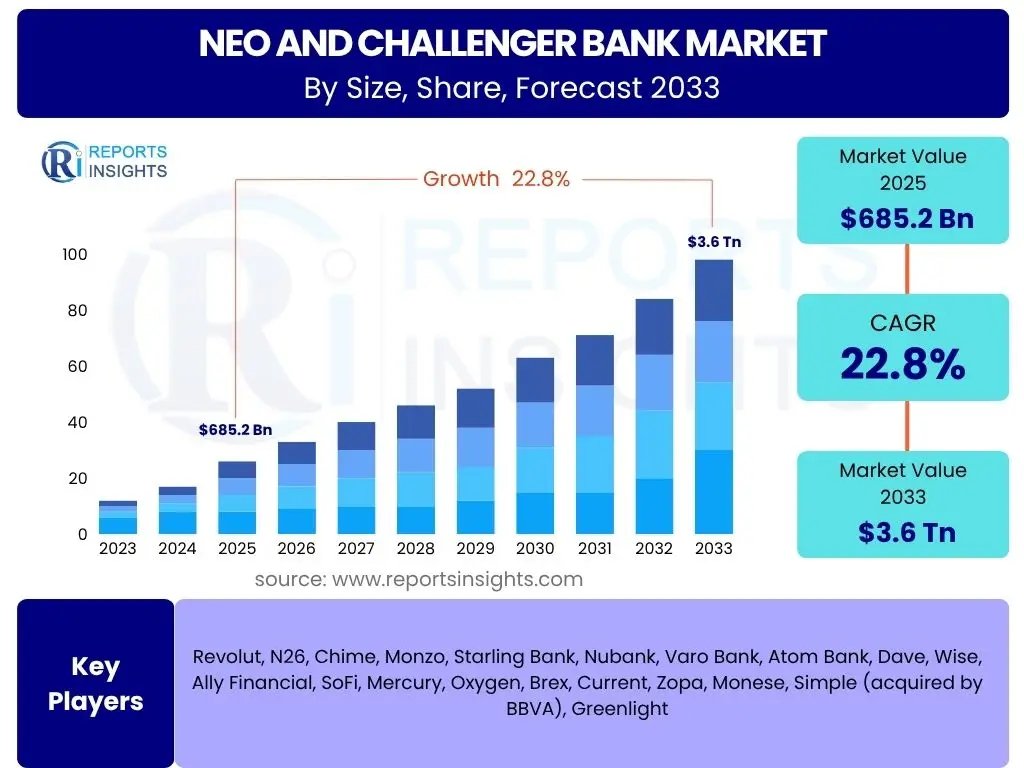

Neo and Challenger Bank Market Size

According to Reports Insights Consulting Pvt Ltd, The Neo and Challenger Bank Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 22.8% between 2025 and 2033. The market is estimated at USD 685.2 Billion in 2025 and is projected to reach USD 3.6 Trillion by the end of the forecast period in 2033.

Key Neo and Challenger Bank Market Trends & Insights

User queries regarding the Neo and Challenger Bank market frequently center on identifying the overarching shifts and innovative approaches shaping the sector. Common questions explore the adoption of new technologies, the evolution of customer expectations, and the competitive landscape with traditional financial institutions. Analysis reveals a prominent drive towards hyper-personalization of financial products, leveraging data analytics and artificial intelligence to offer tailored services. Another key insight is the increasing integration of embedded finance solutions, where banking services are seamlessly incorporated into non-financial platforms, expanding accessibility and user convenience.

The market is also witnessing a significant trend towards sustainability and ethical banking, with a growing number of neo banks focusing on ESG (Environmental, Social, and Governance) principles to attract socially conscious consumers. Furthermore, the expansion into underserved market segments, including SMEs and niche demographics, presents a substantial growth avenue. Open banking initiatives continue to foster collaboration and innovation, enabling a broader ecosystem of financial services. These trends collectively underscore a pivot towards a more customer-centric, technologically advanced, and socially responsible banking paradigm.

- Hyper-Personalization and Customization of Financial Products.

- Integration of Embedded Finance Solutions across various industries.

- Increased Focus on ESG (Environmental, Social, Governance) Principles.

- Expansion into Underserved Market Segments (SMEs, Freelancers, Niche Demographics).

- Leveraging Open Banking APIs for broader financial ecosystem integration.

- Adoption of Advanced Analytics and Artificial Intelligence for enhanced insights.

- Shift towards a Branchless, Digital-First Customer Experience.

AI Impact Analysis on Neo and Challenger Bank

User inquiries regarding the impact of Artificial Intelligence (AI) on the Neo and Challenger Bank sector commonly revolve around its applications in improving efficiency, enhancing customer experience, and mitigating risks. Users are particularly interested in how AI contributes to personalized financial advice, fraud detection, and automated customer service. The analysis reveals that AI is a foundational technology for these digital-first banks, enabling them to process vast amounts of data to derive actionable insights, automate routine tasks, and deliver highly customized interactions at scale. This allows neo banks to operate with lower overheads compared to traditional banks, translating into more competitive product offerings and a superior user experience.

AI's influence extends deeply into operational aspects, from predictive analytics for credit scoring and loan approvals to sophisticated algorithms for market trend analysis and investment recommendations. Moreover, AI-powered chatbots and virtual assistants are revolutionizing customer support, providing instant responses and resolving complex queries efficiently, which significantly boosts customer satisfaction. While the benefits are substantial, user concerns also touch upon data privacy, algorithmic bias, and the ethical implications of AI in financial decision-making. Despite these considerations, the overarching sentiment is that AI is an indispensable tool driving innovation, scalability, and competitive advantage within the neo and challenger banking landscape.

- Enhanced Fraud Detection and Security Protocols through machine learning algorithms.

- Personalized Financial Advice and Product Recommendations powered by AI analytics.

- Automated Customer Service via AI-driven Chatbots and Virtual Assistants.

- Optimized Credit Scoring and Lending Decisions using predictive modeling.

- Operational Efficiency Gains through automation of back-office processes.

- Predictive Analytics for Customer Behavior and Market Trends.

- Improved Risk Management and Compliance Monitoring.

Key Takeaways Neo and Challenger Bank Market Size & Forecast

User questions about the Neo and Challenger Bank market size and forecast frequently seek clarity on the driving forces behind its rapid expansion, the sustainability of its growth trajectory, and the primary regions contributing to its market dominance. Analysis indicates that the market is poised for significant, sustained growth, fueled by increasing digital literacy, dissatisfaction with traditional banking services, and the agility of neo banks to innovate and adapt to evolving consumer demands. The forecasted impressive CAGR underscores a fundamental shift in banking preferences, moving towards digital-only, customer-centric models that prioritize convenience, transparency, and tailored experiences.

A crucial takeaway is the increasing convergence between traditional financial institutions and fintech, with established banks often adopting neo-bank-like features or investing in challenger banks. This suggests a future where digital-first banking is not just an alternative but a core expectation. The market's growth is largely concentrated in regions with high smartphone penetration and a tech-savvy population, such as North America, Europe, and parts of Asia Pacific. Furthermore, the ability of neo and challenger banks to address niche market needs and offer specialized financial solutions will be a key determinant of their continued success and market penetration.

- Market demonstrates robust and sustained growth, driven by digital adoption.

- Significant shift in consumer preference towards digital-first banking models.

- Increasing competition and collaboration between neo banks and traditional institutions.

- North America, Europe, and Asia Pacific are primary growth engines.

- Focus on niche markets and specialized services critical for differentiation.

Neo and Challenger Bank Market Drivers Analysis

The Neo and Challenger Bank market is fundamentally propelled by several powerful macro and microeconomic drivers, collectively fostering a fertile ground for digital-first financial services. A paramount driver is the widespread dissatisfaction with traditional banking models, often perceived as slow, bureaucratic, and lacking in digital innovation. Consumers, especially younger generations and tech-savvy individuals, increasingly seek seamless, intuitive, and mobile-first banking experiences that traditional banks have struggled to provide at scale.

Furthermore, the rapid global expansion of smartphone penetration and internet accessibility has created a vast addressable market for digital-only banking. This technological ubiquity enables neo banks to reach customers without the need for physical branches, significantly reducing operational costs and allowing for more competitive pricing. Regulatory support for open banking initiatives in many jurisdictions also acts as a significant catalyst, encouraging data sharing and fostering an ecosystem where fintechs can integrate with existing financial infrastructures, thereby stimulating innovation and competition.

Lastly, the inherent agility and innovation capacity of neo and challenger banks, driven by their digital-native architecture, allows them to quickly iterate on products, integrate cutting-edge technologies like AI and blockchain, and respond to market demands with speed unmatched by legacy institutions. This agility translates into highly personalized services, faster transactions, and a customer-centric approach that resonates deeply with modern consumers seeking greater control and convenience over their finances.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Digitalization and Smartphone Penetration | +5.5% | Global, particularly Emerging Markets | Short to Medium Term (2025-2029) |

| Dissatisfaction with Traditional Banking Services | +4.8% | North America, Europe, APAC | Short to Medium Term (2025-2029) |

| Favorable Regulatory Environment for Fintech & Open Banking | +4.2% | Europe (PSD2), UK, India, Brazil | Medium Term (2026-2030) |

| Lower Operational Costs and Higher Efficiency of Digital Models | +3.9% | Global | Long Term (2028-2033) |

| Demand for Personalized and Niche Financial Services | +3.5% | North America, Europe, Asia Pacific | Short to Medium Term (2025-2029) |

Neo and Challenger Bank Market Restraints Analysis

Despite the rapid growth, the Neo and Challenger Bank market faces significant restraints that could temper its expansion. One of the most critical challenges is the complex and evolving regulatory landscape. Operating across multiple jurisdictions requires adherence to diverse and often stringent financial regulations, including anti-money laundering (AML), know-your-customer (KYC) rules, data privacy laws (like GDPR), and consumer protection frameworks. Navigating this labyrinth of compliance adds substantial operational costs and can slow down market entry and product innovation, particularly for smaller entities.

Another prominent restraint is the inherent challenge in building customer trust and brand loyalty, especially when compared to centuries-old traditional banks. While digital convenience is a draw, many consumers still harbor concerns regarding the security of their funds, data privacy, and the long-term viability of relatively new, branchless institutions. High-profile data breaches or service outages, even if rare, can severely undermine public confidence and create a significant barrier to widespread adoption, particularly among older demographics or those less comfortable with purely digital interactions.

Furthermore, achieving sustained profitability remains a significant hurdle for many neo banks. While they boast lower operational costs per customer, the intense competition often leads to a race to the bottom on fees, slim margins on core products, and high customer acquisition costs. Many challenger banks are still operating at a loss, relying heavily on venture capital funding. The path to profitability often involves diversifying revenue streams beyond basic banking services, which requires further investment and strategic agility, presenting a considerable long-term restraint on growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Regulatory Compliance and Licensing Requirements | -3.0% | Global, particularly highly regulated markets | Short to Medium Term (2025-2029) |

| Challenges in Building Customer Trust and Brand Loyalty | -2.5% | Global, particularly among older demographics | Medium to Long Term (2027-2033) |

| Cybersecurity Risks and Data Privacy Concerns | -2.2% | Global | Short Term (2025-2027) |

| Achieving Sustainable Profitability and Scalability | -2.0% | Global | Medium to Long Term (2028-2033) |

| Intense Competition from Traditional Banks and Other Fintechs | -1.8% | Mature Markets (North America, Europe) | Short to Medium Term (2025-2029) |

Neo and Challenger Bank Market Opportunities Analysis

The Neo and Challenger Bank market is ripe with opportunities that can significantly accelerate its growth trajectory and expand its influence within the financial sector. One major opportunity lies in targeting underserved markets and niche customer segments that traditional banks have historically neglected or poorly served. This includes freelancers, gig economy workers, small and medium-sized enterprises (SMEs), and specific demographic groups with unique financial needs. By developing tailored products and services, neo banks can capture a loyal customer base and establish strong market positions in these less-contested areas.

Another significant opportunity stems from the increasing demand for integrated financial ecosystems and embedded finance. As digital platforms become central to daily life, there is a growing desire for banking services to be seamlessly integrated into non-financial applications, such as e-commerce platforms, social media, and business management tools. Neo banks, with their API-first architecture, are ideally positioned to partner with these platforms, offering banking-as-a-service (BaaS) solutions that expand their reach and generate new revenue streams without direct customer acquisition costs.

Furthermore, the global shift towards digital payments and the burgeoning interest in sustainable and ethical finance present substantial avenues for growth. Neo banks can differentiate themselves by offering innovative payment solutions, including cross-border remittances with lower fees, and by emphasizing environmentally conscious banking practices or socially responsible investment options. The continuous evolution of technology, particularly in areas like blockchain for secure transactions and AI for hyper-personalization, also provides ongoing opportunities for neo banks to innovate and offer superior, future-proof services that attract and retain customers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Underserved Markets and Niche Segments | +4.5% | Emerging Markets (LatAm, APAC, MEA) | Medium to Long Term (2027-2033) |

| Development of Embedded Finance and Banking-as-a-Service (BaaS) | +4.0% | Global, particularly for B2B partnerships | Medium Term (2026-2031) |

| Growth in Cross-Border Payments and Remittances | +3.8% | Global, particularly corridor-specific regions | Short to Medium Term (2025-2030) |

| Demand for Sustainable and Ethical Banking Products | +3.5% | Europe, North America | Medium to Long Term (2028-2033) |

| Leveraging Emerging Technologies (e.g., Blockchain for DeFi) | +3.2% | Global, particularly tech-forward economies | Long Term (2030-2033) |

Neo and Challenger Bank Market Challenges Impact Analysis

While opportunities abound, the Neo and Challenger Bank market is not without its significant challenges, which can impede growth and sustainability. A primary challenge is the intense and escalating competition within the fintech space. Not only do neo banks compete with each other for market share, but they also face increasing pressure from incumbent traditional banks that are now actively investing in their own digital transformations, launching digital-first sub-brands, or acquiring successful fintechs. This heightened competition can lead to increased customer acquisition costs and a commoditization of basic banking services, making it harder for individual neo banks to achieve differentiation and scale profitably.

Another critical challenge revolves around maintaining robust cybersecurity and ensuring data privacy amidst a rapidly evolving threat landscape. As purely digital entities, neo banks are highly reliant on secure data infrastructure. Any security breach or perceived vulnerability can severely damage their reputation, erode customer trust, and lead to significant financial and regulatory penalties. The continuous investment required to fend off sophisticated cyber threats and comply with ever-tightening data protection regulations places a substantial financial and operational burden on these agile firms.

Furthermore, the path to long-term profitability and sustainable business models remains a significant hurdle for many challenger banks. While customer acquisition numbers may be high, converting users into profitable customers, especially beyond basic transactional accounts, requires offering compelling, revenue-generating products like lending, investments, or premium services. Many neo banks have struggled to diversify their revenue streams effectively, often relying on interchange fees which can be thin. Achieving sufficient scale to cover operational expenses and generate consistent profits without constant capital injections is a complex challenge that necessitates strong strategic execution and a clear monetization strategy.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition from Incumbents and Other Fintechs | -2.8% | Mature Markets (Europe, North America) | Short to Medium Term (2025-2029) |

| High Customer Acquisition Costs (CAC) | -2.4% | Global | Short Term (2025-2027) |

| Ensuring Robust Cybersecurity and Data Protection | -2.1% | Global | Continuous Impact |

| Achieving Sustainable Profitability and Diversified Revenue Streams | -1.9% | Global | Long Term (2028-2033) |

| Talent Acquisition and Retention in a Competitive Tech Landscape | -1.5% | Global, particularly tech hubs | Medium Term (2026-2030) |

Neo and Challenger Bank Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global Neo and Challenger Bank market, examining its current size, historical performance, and future growth projections. It offers detailed insights into key trends, growth drivers, prevailing restraints, emerging opportunities, and significant challenges shaping the industry. The report also includes a thorough segmentation analysis across various categories, providing a granular view of market dynamics and identifying high-growth segments. Regional breakdowns highlight specific market characteristics and opportunities in different geographical areas, while a dedicated section profiles leading market players, offering competitive intelligence.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 685.2 Billion |

| Market Forecast in 2033 | USD 3.6 Trillion |

| Growth Rate | 22.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Revolut, N26, Chime, Monzo, Starling Bank, Nubank, Varo Bank, Atom Bank, Dave, Wise, Ally Financial, SoFi, Mercury, Oxygen, Brex, Current, Zopa, Monese, Simple (acquired by BBVA), Greenlight |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Neo and Challenger Bank market is comprehensively segmented to provide a detailed understanding of its diverse components and evolving dynamics. This segmentation helps identify specific growth avenues, competitive landscapes within sub-sectors, and tailored strategies for market penetration. By categorizing the market based on various attributes, stakeholders can gain precise insights into consumer preferences, technological adoption rates, and regional demand patterns. Each segment represents a distinct facet of the neo banking ecosystem, reflecting different service offerings, technological foundations, and target audiences.

- By Type: Retail Banking, SME Banking, Corporate Banking

- By Service: Payments, Savings Accounts, Lending (Personal, SME), Wealth Management, Insurance, Digital-only Accounts, Credit Cards

- By Technology: Artificial Intelligence (AI), Machine Learning (ML), Blockchain, Cloud Computing, API Integration, Big Data Analytics

- By End-User: Individuals, Small & Medium Enterprises (SMEs), Large Enterprises

Regional Highlights

- North America: The United States and Canada represent a highly competitive and rapidly evolving market, driven by a tech-savvy population, significant venture capital investment, and increasing consumer demand for convenient digital banking solutions. The presence of numerous fintech startups and a supportive regulatory push for open banking contribute to its prominence.

- Europe: A pioneering region for neo and challenger banks, particularly the UK, Germany, and the Netherlands, benefiting from robust regulatory frameworks like PSD2 (Payment Services Directive 2) and strong consumer adoption of digital financial services. The market here is characterized by diverse offerings and intense competition among established players.

- Asia Pacific (APAC): Emerging as a powerhouse for neo banking, with countries like India, China, Singapore, and Australia leading the charge. High smartphone penetration, a large unbanked or underbanked population, and government initiatives promoting digital payments and financial inclusion are key drivers of growth in this region.

- Latin America: Experiencing explosive growth, especially in Brazil and Mexico, fueled by a large unbanked population seeking accessible financial services and a youthful demographic embracing mobile technology. Local players are rapidly scaling, often focusing on addressing specific socio-economic challenges.

- Middle East and Africa (MEA): A nascent but rapidly growing market, with countries like the UAE, Saudi Arabia, and South Africa showing significant potential. Increased internet penetration, government digital transformation agendas, and a demand for modern banking solutions are propelling the adoption of neo and challenger banks in this region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Neo and Challenger Bank Market.- Revolut

- N26

- Chime

- Monzo

- Starling Bank

- Nubank

- Varo Bank

- Atom Bank

- Dave

- Wise

- Ally Financial

- SoFi

- Mercury

- Oxygen

- Brex

- Current

- Zopa

- Monese

- Greenlight

- Capital One (digital-first initiatives)

Frequently Asked Questions

What is a neo bank or challenger bank?

A neo bank or challenger bank is a financial technology (fintech) company that operates purely online, without physical branches, offering banking services typically through mobile apps and web platforms. They aim to challenge traditional banks by providing a more modern, customer-centric, and often more cost-effective banking experience.

How do neo and challenger banks differ from traditional banks?

Neo and challenger banks primarily differ from traditional banks by operating without physical branches, relying entirely on digital channels. They often offer a simplified fee structure, faster account opening, real-time notifications, personalized insights, and focus heavily on user experience and innovative technology, in contrast to the often slower, more complex services of legacy institutions.

Are neo and challenger banks safe and regulated?

The safety and regulation of neo and challenger banks vary by region and specific institution. Many operate under banking licenses, meaning deposits are protected by government-backed insurance schemes (e.g., FDIC in the US, FSCS in the UK). Others operate as financial technology companies partnering with licensed traditional banks. Consumers should always verify the licensing and deposit protection status of a neo bank before opening an account.

What services do neo and challenger banks typically offer?

Neo and challenger banks typically offer core banking services such as current accounts, savings accounts, debit cards, and payment services. Many also expand into lending (personal loans, overdrafts), budgeting tools, international money transfers, wealth management, and sometimes even insurance products, all accessible through their digital platforms.

What is the future outlook for the neo and challenger bank market?

The future outlook for the neo and challenger bank market is highly positive, projecting significant growth driven by increasing digital adoption, continuous innovation in financial technology, and a sustained demand for convenient, personalized, and cost-effective banking solutions. The market is expected to expand globally, with a focus on niche markets and embedded finance opportunities, while competition will likely intensify.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted