Multimedia Chipset Market

Multimedia Chipset Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706983 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

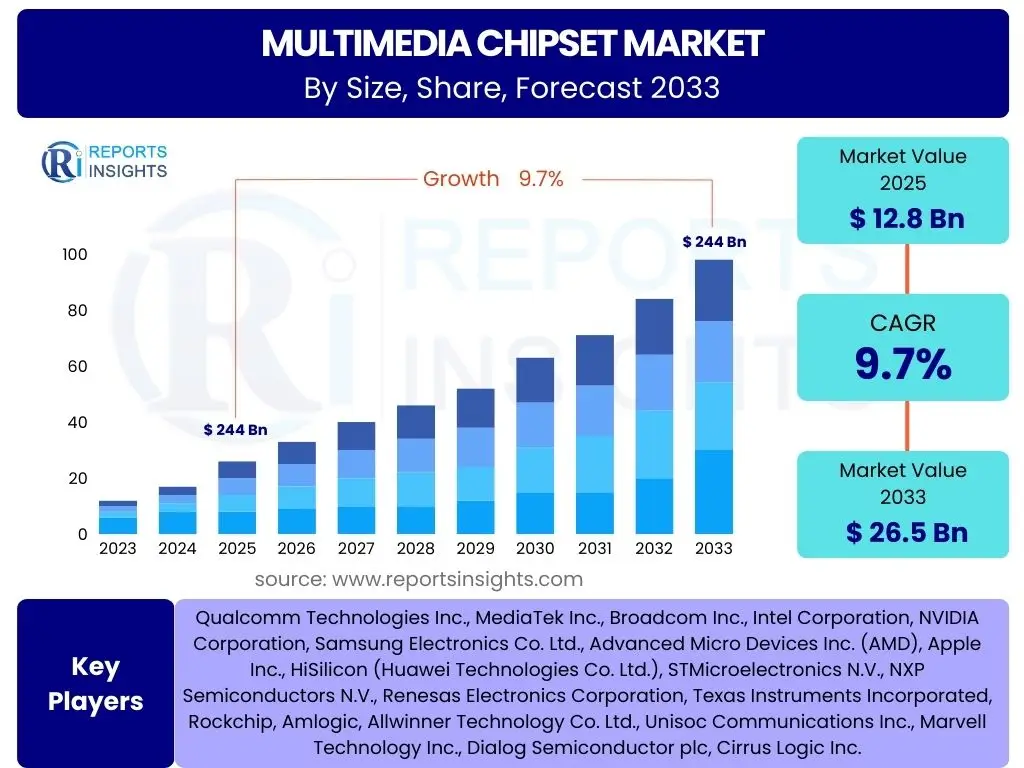

Multimedia Chipset Market Size

According to Reports Insights Consulting Pvt Ltd, The Multimedia Chipset Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.7% between 2025 and 2033. The market is estimated at USD 12.8 Billion in 2025 and is projected to reach USD 26.5 Billion by the end of the forecast period in 2033.

Key Multimedia Chipset Market Trends & Insights

The Multimedia Chipset Market is undergoing significant transformation, driven by a confluence of technological advancements and evolving consumer demands. User inquiries frequently highlight the impact of emerging display technologies, advanced audio processing, and the proliferation of high-bandwidth connectivity standards. There is a strong interest in understanding how chipsets are adapting to deliver richer multimedia experiences, from 8K video streaming to immersive augmented and virtual reality applications, alongside the integration of sophisticated AI capabilities at the edge. The demand for seamless, low-latency, and power-efficient processing across a diverse range of devices is shaping the direction of innovation within this sector.

Furthermore, the market is seeing a growing emphasis on specialized processing units and System-on-Chips (SoCs) that can handle complex multimedia tasks more efficiently. This includes dedicated hardware accelerators for video encoding/decoding, advanced audio codecs, and graphics rendering. The trend towards greater integration and miniaturization, enabling powerful multimedia capabilities in compact form factors, is also a prominent area of interest. These advancements are critical for meeting the increasing expectations for high-fidelity content consumption and creation across consumer electronics, automotive infotainment, and industrial applications.

- Integration of AI/ML for enhanced processing (e.g., upscaling, noise reduction, personalization).

- Proliferation of 5G connectivity driving demand for high-bandwidth multimedia streaming.

- Advancements in display technologies (8K, HDR, variable refresh rates) requiring more powerful chipsets.

- Increasing adoption of augmented reality (AR) and virtual reality (VR) devices demanding specialized multimedia processing.

- Development of energy-efficient chipsets for extended battery life in portable devices.

- Shift towards edge computing for real-time multimedia analytics and processing.

AI Impact Analysis on Multimedia Chipset

User inquiries about AI's impact on multimedia chipsets frequently revolve around its role in enhancing user experience, enabling intelligent processing, and driving new application possibilities. There is a keen interest in how Artificial Intelligence (AI) and Machine Learning (ML) are being integrated directly into chipset architectures to perform tasks such as real-time image and video enhancement, predictive content caching, natural language processing for voice assistants, and adaptive audio adjustments. Users are looking for insights into how these AI capabilities contribute to more immersive, personalized, and efficient multimedia consumption and creation, while also raising questions about the computational demands and power efficiency of such integrations.

The core theme emerging from these inquiries is the transformation of multimedia chipsets from mere processors into intelligent engines capable of understanding, optimizing, and even generating content. AI integration allows for more sophisticated noise reduction, super-resolution algorithms, object recognition for smarter camera functionalities, and adaptive streaming that adjusts to network conditions and user preferences in real-time. This profound shift is driving the need for specialized AI accelerators and neural processing units (NPUs) within multimedia chipsets, moving complex AI computations closer to the data source and reducing reliance on cloud-based processing. Concerns about data privacy and the ethical implications of AI-powered multimedia processing are also becoming increasingly relevant.

- AI-driven image and video enhancement (e.g., super-resolution, noise reduction, de-blurring).

- Integration of Neural Processing Units (NPUs) for on-device AI inference.

- Enhanced voice and audio processing for smart assistants and noise cancellation.

- Facial and object recognition capabilities for advanced camera systems.

- Personalized content recommendation and adaptive streaming algorithms.

- Optimization of power consumption through AI-managed workload distribution.

Key Takeaways Multimedia Chipset Market Size & Forecast

The Multimedia Chipset Market is poised for substantial expansion, with key takeaways often focusing on the primary drivers behind this growth and the transformative technological shifts expected. User questions frequently center on the overall market trajectory, the underlying reasons for its projected CAGR, and which segments or applications will be the most significant contributors to this growth. The overarching sentiment is that the relentless pursuit of higher fidelity, more immersive experiences, and ubiquitous connectivity will fuel continuous innovation and demand in this sector. The forecast indicates a robust market, shaped by both consumer and enterprise needs.

A critical insight is that the market's growth is not merely volumetric but also driven by increasing complexity and value per unit, as chipsets integrate more advanced features like AI, 5G modems, and sophisticated graphics capabilities. The shift towards edge AI processing, the emergence of the metaverse, and the sustained demand for premium entertainment experiences across various devices are identified as pivotal elements influencing the market's upward trajectory. Furthermore, the competitive landscape is expected to remain dynamic, with continuous innovation in power efficiency, performance, and cost-effectiveness being key determinants of market leadership and sustained growth throughout the forecast period.

- Strong growth trajectory driven by demand for high-quality content and immersive experiences.

- Significant value addition from integrated AI/ML and 5G capabilities.

- Consumer electronics, automotive, and AR/VR segments are key growth drivers.

- Increasing average selling prices (ASPs) due to advanced feature integration.

- Emphasis on power efficiency and performance optimization will define market leaders.

Multimedia Chipset Market Drivers Analysis

The Multimedia Chipset Market is fundamentally driven by the escalating global demand for enhanced digital content consumption and creation, pushing the boundaries of technological capabilities. A primary driver is the pervasive adoption of smart devices across various form factors, including smartphones, smart televisions, and wearable technology, all requiring robust multimedia processing capabilities. The continuous evolution of display technologies, such as 4K and 8K resolutions and High Dynamic Range (HDR), necessitates more powerful chipsets to render and process vast amounts of visual data with unparalleled clarity and color depth. This upward trend in visual fidelity directly translates into increased demand for advanced multimedia chip solutions that can handle these complex requirements efficiently and smoothly.

Another significant driver is the rapid deployment and expansion of 5G networks globally, which enable ultra-high-speed data transfer and ultra-low latency. This connectivity revolution unlocks new possibilities for streaming high-resolution content, cloud gaming, and real-time immersive experiences like augmented and virtual reality, all of which heavily rely on sophisticated multimedia chipsets for processing and rendering. Furthermore, the integration of Artificial Intelligence (AI) and Machine Learning (ML) capabilities into chipsets is propelling innovation, allowing for intelligent content processing, personalized user experiences, and advanced computational photography, thus adding significant value and driving demand for next-generation multimedia solutions. The confluence of these factors creates a fertile ground for sustained market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for High-Resolution Content & Devices | +2.5% | Global, particularly APAC (China, India), North America, Europe | 2025-2033 |

| Proliferation of 5G Connectivity and IoT Devices | +2.0% | Global, especially North America, Europe, APAC (South Korea, Japan) | 2025-2033 |

| Integration of AI and Machine Learning Capabilities | +1.8% | Global, with strong innovation hubs in North America, APAC | 2025-2033 |

| Growing Adoption of AR/VR and Immersive Technologies | +1.5% | North America, Europe, APAC (Gaming and Enterprise) | 2026-2033 |

| Expansion of Automotive Infotainment Systems | +1.0% | Europe, North America, APAC (China, Japan, South Korea) | 2025-2033 |

Multimedia Chipset Market Restraints Analysis

Despite the robust growth opportunities, the Multimedia Chipset Market faces several significant restraints that could impede its full potential. One major challenge is the inherently high cost associated with research and development (R&D) of advanced chipset architectures. Designing and manufacturing cutting-edge multimedia chipsets, especially those integrating complex AI accelerators or next-generation connectivity modules, requires substantial investments in intellectual property, highly specialized engineering talent, and advanced fabrication facilities. These high R&D expenditures often lead to increased product costs, which can impact market adoption, particularly in price-sensitive emerging markets or for lower-end consumer devices, thus potentially slowing down overall market expansion.

Another crucial restraint is the intense competition and market saturation in certain mature segments, particularly smartphones. While demand for high-end multimedia capabilities remains strong, the commoditization of mid-range and entry-level chipsets puts significant pressure on profit margins. Furthermore, the global semiconductor supply chain vulnerability, exacerbated by geopolitical tensions and natural disasters, poses a continuous threat. Disruptions in the supply of critical raw materials or manufacturing capacities can lead to delays in product launches, increased production costs, and ultimately, a shortfall in market supply. Moreover, the rapid pace of technological obsolescence means that significant R&D investments can quickly become outdated, further increasing financial risks for market players and creating a challenging environment for sustained profitability and growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Research & Development (R&D) Costs | -1.2% | Global | 2025-2033 |

| Intense Competition and Price Pressure | -1.0% | Global, particularly APAC (mass market) | 2025-2033 |

| Global Semiconductor Supply Chain Volatility | -0.8% | Global, especially regions reliant on specific foundries | 2025-2028 (mitigating later) |

| Rapid Technological Obsolescence | -0.7% | Global | 2025-2033 |

| Intellectual Property (IP) Litigation Risks | -0.5% | North America, Europe, APAC (Patent-heavy regions) | 2025-2033 |

Multimedia Chipset Market Opportunities Analysis

The Multimedia Chipset Market is rich with untapped potential, driven by technological evolution and the emergence of new application areas. A significant opportunity lies in the burgeoning market for specialized AI accelerators and neural processing units (NPUs) within multimedia chipsets. As AI becomes more integral to multimedia processing, from real-time video analysis to personalized content delivery, the demand for highly efficient, low-power AI inference capabilities on the edge is surging. This opens avenues for innovation in dedicated AI hardware, allowing chip manufacturers to differentiate their offerings and capture a share of the rapidly expanding AI-driven application market across various sectors including smart homes, surveillance, and autonomous systems.

Furthermore, the increasing adoption of augmented reality (AR), virtual reality (VR), and mixed reality (MR) devices presents a substantial opportunity for multimedia chipset manufacturers. These immersive technologies require extremely high-performance graphics processing, low-latency rendering, and advanced sensor fusion capabilities, pushing the boundaries of current chipset designs. Developing specialized chipsets optimized for the unique demands of AR/VR, including power efficiency for untethered devices and seamless integration with complex tracking systems, can unlock significant growth. Additionally, the expansion of the automotive sector, particularly with advanced driver-assistance systems (ADAS) and in-car infotainment systems demanding cinematic experiences and robust connectivity, offers another lucrative pathway for multimedia chipset innovation and market penetration. Lastly, the development of integrated solutions for next-generation smart cities and industrial IoT applications, which rely heavily on real-time video analytics and sensor data processing, represents a promising long-term growth frontier.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Edge AI and Dedicated AI Accelerators | +1.8% | Global, especially North America, Europe, APAC (China) | 2025-2033 |

| Growth in AR/VR/MR Device Market | +1.5% | North America, APAC (Japan, South Korea), Europe | 2026-2033 |

| Expansion in Automotive Infotainment & ADAS | +1.2% | Europe, North America, APAC (China, Japan) | 2025-2033 |

| Demand from Industrial IoT & Smart City Applications | +1.0% | North America, Europe, APAC (China, Singapore) | 2027-2033 |

| Specialized Chipsets for Metaverse and Web3 Applications | +0.8% | Global | 2028-2033 |

Multimedia Chipset Market Challenges Impact Analysis

The Multimedia Chipset Market, while dynamic, faces several significant challenges that necessitate strategic navigation from market players. One critical challenge is the exceptionally rapid pace of technological advancements and the resulting quick obsolescence of existing chipsets. Companies must continually invest heavily in R&D to stay competitive, releasing new generations of chipsets with enhanced capabilities (e.g., higher resolutions, faster processing, better power efficiency) at an accelerated rate. Failure to innovate swiftly can lead to market share erosion, as product lifecycles are increasingly compressed, making it difficult to recoup development costs and maintain a leading edge. This creates significant pressure on research and development budgets and time-to-market strategies.

Another major challenge is ensuring interoperability and compatibility across a vast and fragmented ecosystem of devices, operating systems, and content formats. Multimedia chipsets must seamlessly integrate with diverse hardware components and software platforms, often from different manufacturers, to deliver a consistent and high-quality user experience. This requires adherence to numerous industry standards and extensive testing, which can be time-consuming and resource-intensive. Furthermore, the global shortage of skilled semiconductor engineers and design talent poses a constraint on innovation and production capacity. Geopolitical tensions and trade disputes also introduce uncertainty into the supply chain, potentially disrupting access to critical components or markets. These multifaceted challenges demand robust strategic planning, strong partnerships, and continuous investment in talent and technology to overcome and sustain growth in this complex market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence & Short Product Lifecycles | -1.5% | Global | 2025-2033 |

| Ensuring Interoperability Across Diverse Ecosystems | -1.0% | Global | 2025-2033 |

| Global Talent Shortage in Semiconductor Design | -0.9% | Global, particularly North America, Europe, East Asia | 2025-2033 |

| Intellectual Property (IP) Disputes and Licensing Costs | -0.7% | Global | 2025-2033 |

| Cybersecurity Risks & Data Privacy Concerns | -0.6% | Global | 2025-2033 |

Multimedia Chipset Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Multimedia Chipset Market, offering a detailed segmentation by various parameters including application, type, and connectivity, alongside a thorough regional assessment. The scope encompasses a historical review from 2019 to 2023, providing context for current market dynamics, and offers a robust forecast through 2033. Key market trends, drivers, restraints, opportunities, and challenges are meticulously examined to present a holistic view of the market's trajectory and influencing factors. The report also highlights the competitive landscape, profiling key market players and their strategic initiatives, and includes critical insights into the impact of emerging technologies such as Artificial Intelligence and 5G on the market's evolution.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.8 Billion |

| Market Forecast in 2033 | USD 26.5 Billion |

| Growth Rate | 9.7% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Qualcomm Technologies Inc., MediaTek Inc., Broadcom Inc., Intel Corporation, NVIDIA Corporation, Samsung Electronics Co. Ltd., Advanced Micro Devices Inc. (AMD), Apple Inc., HiSilicon (Huawei Technologies Co. Ltd.), STMicroelectronics N.V., NXP Semiconductors N.V., Renesas Electronics Corporation, Texas Instruments Incorporated, Rockchip, Amlogic, Allwinner Technology Co. Ltd., Unisoc Communications Inc., Marvell Technology Inc., Dialog Semiconductor plc, Cirrus Logic Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Multimedia Chipset Market is extensively segmented to provide a granular understanding of its diverse components and evolving applications. This segmentation is crucial for identifying specific growth pockets, understanding technological niches, and analyzing the competitive landscape more effectively. The primary categories for segmentation include application, chipset type, and connectivity, reflecting the multifaceted nature of multimedia processing demands across various industries and consumer devices. Each segment is driven by unique technological requirements and market dynamics, contributing distinctively to the overall market's expansion.

Analyzing these segments helps in discerning the specific drivers and challenges pertinent to each category. For instance, the smartphone segment primarily demands highly integrated, power-efficient SoCs, while AR/VR devices prioritize ultra-low latency graphics and specialized sensory processing. Similarly, the type of chipset, whether it is a dedicated audio DSP or a powerful GPU, dictates its primary market and the technological innovations required. This detailed breakdown ensures a comprehensive view of how different market forces interact and shape the Multimedia Chipset Market as a whole, facilitating targeted strategic planning and investment decisions for stakeholders.

- By Application:

- Smartphones: Dominant segment, driven by high-end multimedia features, gaming, and AI.

- Tablets: Steady demand for entertainment and productivity.

- Smart TVs: Requires advanced video processing, streaming, and smart functionalities.

- Gaming Consoles: Demands high-performance GPUs and integrated solutions for immersive gaming.

- Automotive Infotainment: Growing segment driven by in-car entertainment, navigation, and ADAS integration.

- Wearables: Focus on compact, low-power, and efficient multimedia processing for smartwatches, fitness trackers.

- AR/VR Devices: High demand for ultra-low latency, high-resolution graphics, and sensor fusion.

- Drones: Requires image processing, real-time video streaming, and stable connectivity.

- Others: Includes professional displays, digital signage, surveillance cameras, and industrial applications.

- By Type:

- Audio Chipsets: Dedicated processors for high-fidelity audio, noise cancellation, and voice processing.

- Video Chipsets: Specialized for video encoding, decoding, and processing for various resolutions.

- Graphics Processing Units (GPUs): Essential for rendering complex visuals and accelerating AI workloads.

- Integrated Chipsets (SoCs): Combine CPU, GPU, memory, and other components for a complete solution.

- AI Accelerators / NPUs: Dedicated hardware for efficient AI model inference and machine learning tasks.

- By Connectivity:

- 5G: High-bandwidth, low-latency communication enabling advanced multimedia streaming and cloud gaming.

- Wi-Fi 6/6E: High-speed local wireless connectivity for smart home devices and high-density environments.

- Bluetooth: Standard for short-range wireless audio and peripheral connections.

- Others: Includes GPS for navigation, NFC for payments, and various other communication protocols.

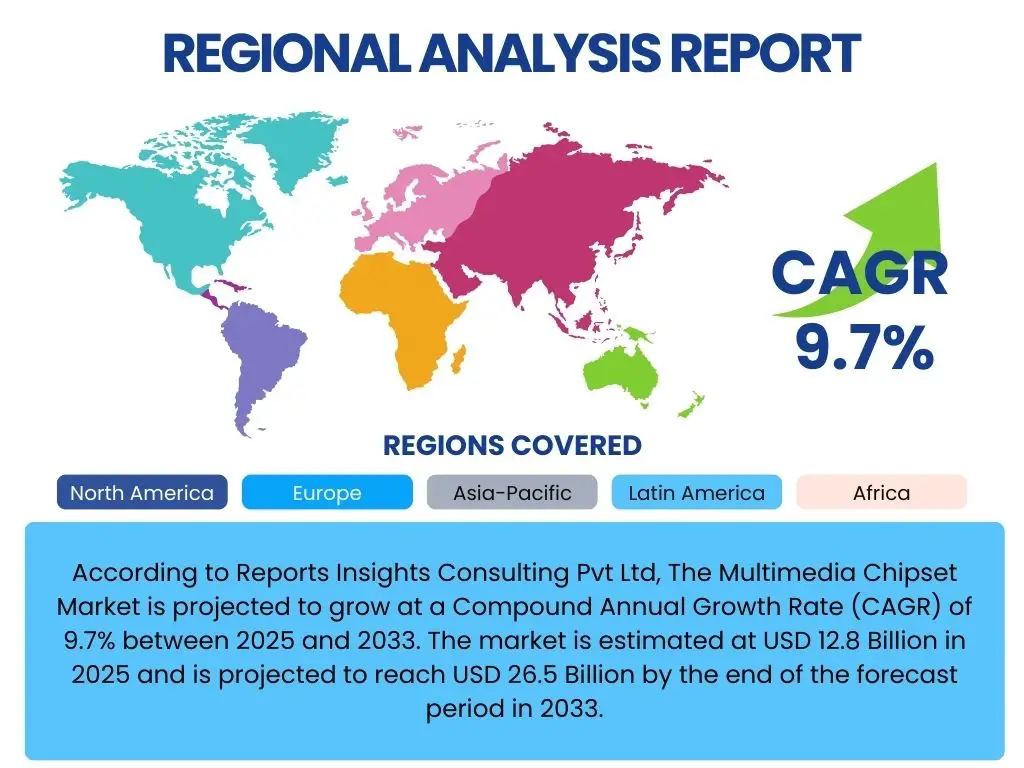

Regional Highlights

- North America: This region is characterized by early adoption of cutting-edge technologies and a strong presence of leading chipset manufacturers and technology innovators. High consumer disposable income and a robust telecommunications infrastructure, coupled with significant investments in AR/VR and AI, drive demand for premium multimedia chipsets. The region is a hub for R&D and sees strong growth in automotive infotainment and advanced consumer electronics.

- Europe: Europe exhibits a mature market with a focus on smart home integration, automotive innovations, and a growing gaming industry. Stringent regulatory frameworks for data privacy and cybersecurity also influence chipset design. Western European countries like Germany, France, and the UK are key contributors to market revenue, driven by technological advancements and high consumer electronics penetration.

- Asia Pacific (APAC): APAC is the largest and fastest-growing market for multimedia chipsets, primarily driven by massive consumer bases in China and India, rapidly expanding smartphone and smart TV markets, and increasing adoption of 5G infrastructure. Countries like South Korea and Japan are leaders in semiconductor manufacturing and technological innovation, fostering significant R&D and production activities. The region also sees burgeoning demand from the gaming, smart home, and surveillance sectors.

- Latin America: This region is an emerging market with increasing internet penetration and a growing middle class, leading to rising demand for affordable smartphones and smart TVs. While not as technologically advanced as APAC or North America, there is significant potential for growth as digital infrastructure improves and consumer preferences shift towards more advanced multimedia experiences.

- Middle East and Africa (MEA): MEA presents a developing market for multimedia chipsets, influenced by increasing mobile connectivity, urbanization, and government initiatives aimed at digital transformation. While current market size is smaller, sustained infrastructure development and economic growth are expected to drive demand for multimedia-enabled devices, particularly in sectors like smart cities and entertainment.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Multimedia Chipset Market.- Qualcomm Technologies Inc.

- MediaTek Inc.

- Broadcom Inc.

- Intel Corporation

- NVIDIA Corporation

- Samsung Electronics Co. Ltd.

- Advanced Micro Devices Inc. (AMD)

- Apple Inc.

- HiSilicon (Huawei Technologies Co. Ltd.)

- STMicroelectronics N.V.

- NXP Semiconductors N.V.

- Renesas Electronics Corporation

- Texas Instruments Incorporated

- Rockchip

- Amlogic

- Allwinner Technology Co. Ltd.

- Unisoc Communications Inc.

- Marvell Technology Inc.

- Dialog Semiconductor plc

- Cirrus Logic Inc.

Frequently Asked Questions

Analyze common user questions about the Multimedia Chipset market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a multimedia chipset and what are its primary functions?

A multimedia chipset is an integrated circuit or a set of circuits designed to process and manage various multimedia data, including audio, video, graphics, and connectivity. Its primary functions include decoding and encoding multimedia formats, rendering graphics, processing audio signals, managing display outputs, and handling high-speed data transfer for applications like streaming, gaming, and immersive experiences.

How is 5G impacting the demand for multimedia chipsets?

5G connectivity significantly boosts the demand for multimedia chipsets by enabling ultra-high-speed data transfer and extremely low latency. This facilitates seamless streaming of 4K/8K content, real-time cloud gaming, and more immersive AR/VR experiences, all of which require advanced chipsets capable of handling high data throughput and complex processing with minimal delay.

What role does AI play in modern multimedia chipsets?

AI integration into multimedia chipsets is pivotal for enhancing user experience and enabling intelligent processing. AI capabilities, often via Neural Processing Units (NPUs), allow for tasks like real-time image and video enhancement (e.g., super-resolution, noise reduction), advanced voice processing, facial recognition, and personalized content delivery, making devices smarter and more responsive.

Which applications are driving the growth of the multimedia chipset market?

The multimedia chipset market's growth is primarily driven by applications requiring high-performance processing and rich media experiences. Key drivers include smartphones, smart TVs, gaming consoles, and the rapidly expanding segments of automotive infotainment systems, AR/VR devices, and specialized chipsets for edge AI in smart homes and industrial IoT.

What are the main challenges facing multimedia chipset manufacturers?

Multimedia chipset manufacturers face challenges such as high research and development costs, rapid technological obsolescence leading to short product lifecycles, intense market competition and price pressures, and vulnerabilities in the global semiconductor supply chain. Ensuring interoperability across diverse ecosystems and addressing the global shortage of skilled engineering talent also pose significant hurdles.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted