Multilayer Film Market

Multilayer Film Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701396 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

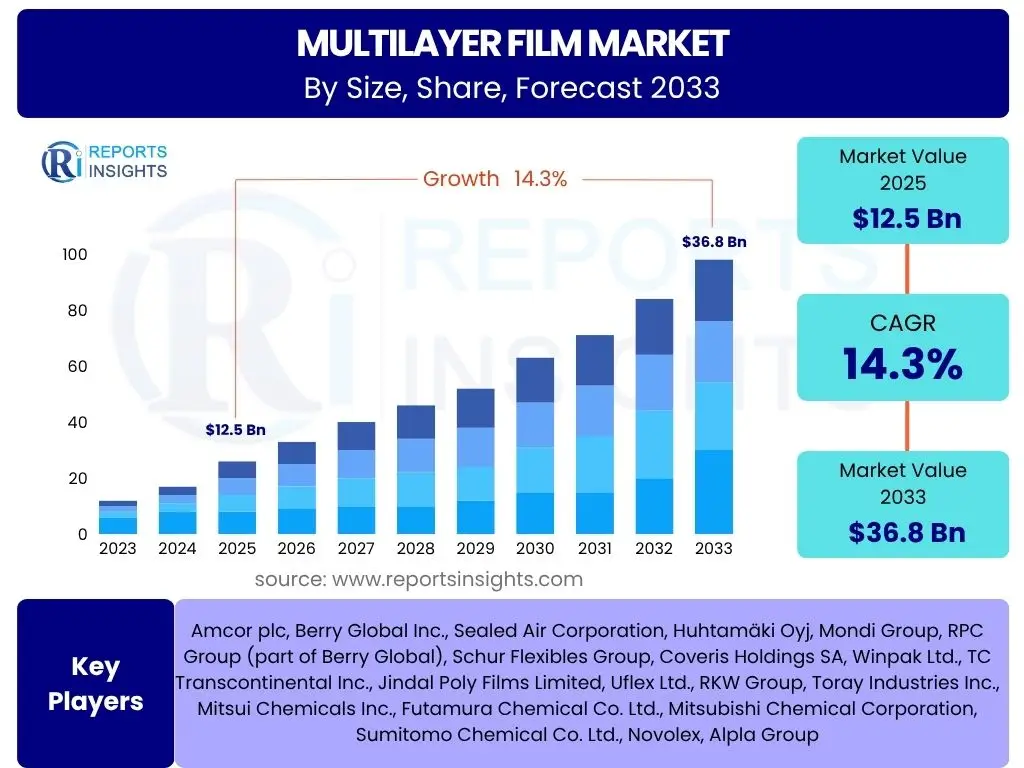

Multilayer Film Market Size

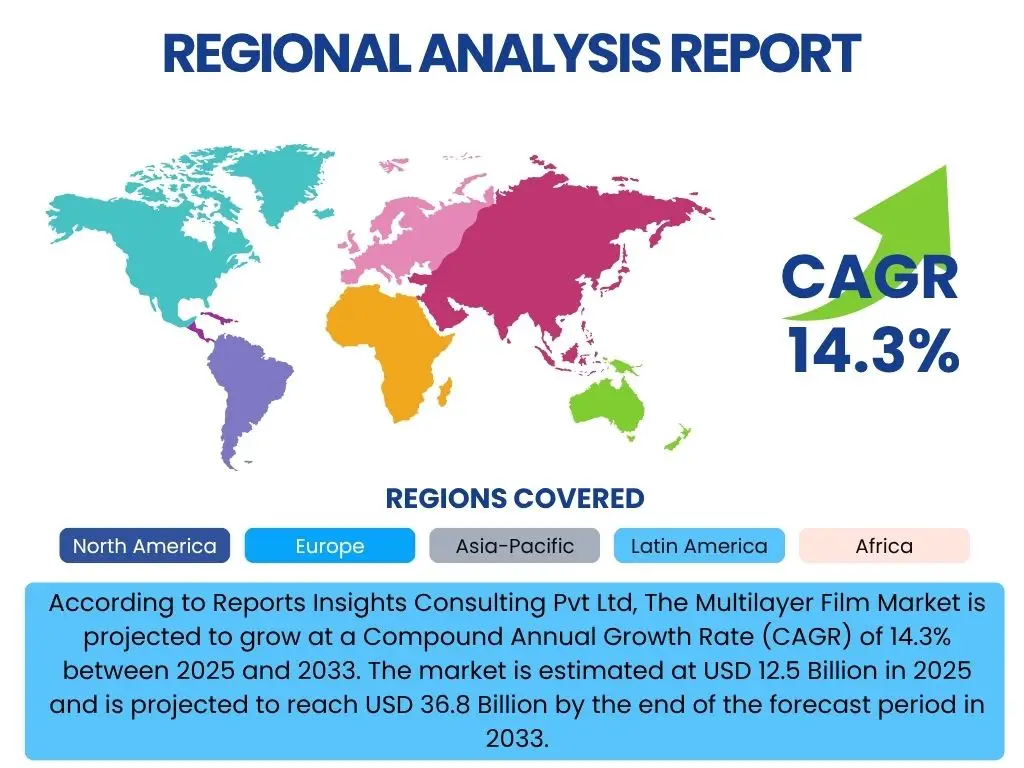

According to Reports Insights Consulting Pvt Ltd, The Multilayer Film Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 14.3% between 2025 and 2033. The market is estimated at USD 12.5 Billion in 2025 and is projected to reach USD 36.8 Billion by the end of the forecast period in 2033.

Key Multilayer Film Market Trends & Insights

The global multilayer film market is currently undergoing significant transformation, driven by evolving consumer demands, stringent regulatory landscapes, and rapid technological advancements. A primary trend observed is the increasing emphasis on sustainable packaging solutions, pushing manufacturers to innovate in recyclable, biodegradable, and compostable multilayer films. This shift is directly influenced by heightened environmental awareness among consumers and growing governmental initiatives to reduce plastic waste. Furthermore, advancements in barrier technologies are allowing for thinner, yet more effective, films that extend product shelf life, reduce food waste, and minimize material usage.

Another prominent insight revolves around the expansion of e-commerce, which necessitates robust, lightweight, and protective packaging, boosting the demand for high-performance multilayer films. The pharmaceutical and healthcare sectors are also demonstrating a strong uptake, driven by the need for sterile, secure, and tamper-evident packaging. Customization and specialization are becoming critical, with manufacturers offering tailored film structures designed to meet specific product requirements, whether it's oxygen barrier for food, moisture barrier for electronics, or chemical resistance for industrial applications. The integration of smart packaging features, though nascent, represents a future growth avenue, enabling functionalities like temperature monitoring or authenticity verification.

- Increasing demand for sustainable and eco-friendly multilayer films, including recyclable, compostable, and bio-based options.

- Advancements in barrier technologies enhancing film performance for extended shelf life and product protection.

- Rising adoption of multilayer films in the rapidly expanding e-commerce sector for protective packaging.

- Growth in demand from the pharmaceutical and healthcare industries for sterile and secure packaging solutions.

- Development of thinner, high-performance films to reduce material consumption and transportation costs.

- Focus on specialized and customized film structures to meet diverse industry-specific requirements.

- Emergence of smart packaging functionalities integrating sensors and indicators within multilayer films.

AI Impact Analysis on Multilayer Film

Artificial intelligence (AI) is poised to significantly impact the multilayer film industry by optimizing various stages of the value chain, from raw material sourcing to production and quality control. Users often inquire about AI's role in improving manufacturing efficiency, predicting material performance, and enabling more sophisticated R&D. AI-driven predictive analytics can forecast demand fluctuations, allowing for optimized inventory management and reduced waste. In manufacturing, AI algorithms can monitor production lines in real-time, identifying anomalies, predicting equipment failures, and fine-tuning extrusion processes to minimize defects and improve film consistency, leading to substantial cost savings and enhanced product quality. This level of precision is critical for the complex co-extrusion processes inherent in multilayer film production.

Beyond operational efficiencies, AI is expected to accelerate innovation in material science for multilayer films. Machine learning models can analyze vast datasets of material properties, polymer interactions, and additive effects, enabling faster discovery of novel film formulations with desired barrier, mechanical, or sustainable characteristics. This can drastically reduce the time and cost associated with traditional R&D cycles. Furthermore, AI can aid in simulating the performance of new film structures under various environmental conditions, providing insights before physical prototyping. The integration of AI in quality assurance systems, utilizing computer vision for defect detection, represents another transformative application, ensuring higher product standards and reducing customer complaints. Overall, AI’s influence will lead to more efficient, intelligent, and sustainable multilayer film production.

- Optimized production processes through AI-driven real-time monitoring and predictive maintenance, reducing downtime and waste.

- Enhanced quality control using AI-powered computer vision for rapid and accurate defect detection in film manufacturing.

- Accelerated material discovery and formulation development through machine learning analysis of polymer properties and interactions.

- Improved supply chain efficiency and demand forecasting with AI analytics, leading to optimized inventory and logistics.

- Development of smart films with integrated AI functionalities for enhanced product monitoring and consumer interaction.

- Reduced energy consumption and environmental footprint through AI-optimized manufacturing parameters.

- Simulation of film performance under various conditions, enabling faster prototyping and product validation.

Key Takeaways Multilayer Film Market Size & Forecast

The multilayer film market is set for robust growth over the forecast period, driven by a confluence of evolving industry needs and technological advancements. A crucial takeaway is the projected substantial increase in market valuation, highlighting the enduring demand for high-performance barrier packaging across diverse sectors. This growth is intrinsically linked to the expanding applications of multilayer films, particularly in sectors requiring extended shelf life, product protection, and enhanced material efficiency. The market’s resilience and upward trajectory underscore its critical role in modern packaging solutions, adapting to dynamic consumer and regulatory landscapes.

Furthermore, the forecast emphasizes a significant shift towards sustainable solutions within the multilayer film domain. The imperative to reduce environmental impact is not merely a trend but a fundamental driver shaping future product development and market dynamics. Manufacturers are increasingly investing in research and development for recyclable, biodegradable, and compostable film structures, indicating a long-term commitment to eco-friendly innovations. This focus on sustainability, coupled with continuous advancements in material science and processing technologies, positions the multilayer film market for sustained expansion and evolution, catering to both economic and environmental objectives.

- The Multilayer Film Market is projected for substantial growth, reaching USD 36.8 Billion by 2033 with a CAGR of 14.3%.

- Strong demand from food & beverage, pharmaceutical, and personal care industries remains a primary growth catalyst.

- Sustainability initiatives are heavily influencing market direction, driving innovation in recyclable and bio-based films.

- Technological advancements in barrier properties and co-extrusion techniques are enhancing film performance and efficiency.

- E-commerce expansion significantly contributes to the increased adoption of protective multilayer packaging.

- Asia Pacific is expected to be a key growth region due to rapid industrialization and consumer market expansion.

Multilayer Film Market Drivers Analysis

The primary drivers propelling the multilayer film market are multifaceted, stemming from global consumer trends, technological advancements, and the evolving demands of end-use industries. The escalating global demand for packaged food and beverages, driven by urbanization, changing lifestyles, and the need for convenience, directly fuels the growth of multilayer films due to their superior barrier properties which extend product shelf life and prevent spoilage. This is particularly crucial for perishable goods, ensuring food safety and reducing waste across supply chains.

Furthermore, the burgeoning e-commerce sector represents a significant growth catalyst. The need for robust, lightweight, and protective packaging that can withstand the rigors of transit without compromising product integrity has increased the reliance on multilayer films. These films offer excellent puncture resistance and cushioning, making them ideal for shipping a wide array of products. Innovations in material science, leading to the development of thinner yet stronger films with enhanced barrier capabilities, also contribute to market expansion by offering more efficient and cost-effective packaging solutions across various applications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for packaged food and beverages | +0.8% | Global, particularly Asia Pacific & Latin America | 2025-2033 (Long-term) |

| Expansion of the e-commerce sector | +0.7% | Global, particularly North America, Europe, & Asia Pacific | 2025-2030 (Mid-term) |

| Technological advancements in film properties and manufacturing | +0.6% | Global | 2025-2033 (Long-term) |

| Increased focus on food safety and shelf-life extension | +0.5% | Global | 2025-2033 (Long-term) |

| Rising demand from pharmaceutical and healthcare industries | +0.4% | North America, Europe, Asia Pacific | 2025-2030 (Mid-term) |

Multilayer Film Market Restraints Analysis

Despite significant growth prospects, the multilayer film market faces several notable restraints that could temper its expansion. One primary concern is the increasing stringency of environmental regulations regarding plastic waste and single-use plastics. Governments and regulatory bodies globally are implementing bans and taxes on certain plastic products, pushing industries to seek alternative packaging materials or invest heavily in recycling infrastructure. While multilayer films offer performance benefits, their multi-material composition often complicates recycling, posing a significant challenge to achieving circular economy goals.

Another key restraint is the volatility in raw material prices. Multilayer films largely rely on petrochemical-derived polymers such as polyethylene (PE), polypropylene (PP), and polyamide (PA). Fluctuations in crude oil prices directly impact the cost of these raw materials, leading to unpredictable production costs for film manufacturers. This volatility can erode profit margins and make long-term planning difficult, potentially slowing down investment in new capacity or innovation. Furthermore, the capital-intensive nature of co-extrusion equipment and the complexity of manufacturing processes also present barriers to entry for new players and can limit the expansion capabilities of existing ones.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent environmental regulations and plastic waste concerns | -0.9% | Europe, North America, specific Asian countries | 2025-2033 (Long-term) |

| Volatility in raw material prices (polymers) | -0.6% | Global | 2025-2030 (Mid-term) |

| Complexity and high capital investment in manufacturing | -0.4% | Global | 2025-2033 (Long-term) |

| Challenges in recycling multi-material film structures | -0.7% | Global | 2025-2033 (Long-term) |

| Competition from alternative packaging materials (e.g., paper, glass) | -0.3% | Global | 2025-2030 (Mid-term) |

Multilayer Film Market Opportunities Analysis

Significant opportunities are emerging within the multilayer film market, primarily driven by the growing emphasis on sustainable packaging solutions and the advent of advanced materials. The development and commercialization of recyclable, biodegradable, and compostable multilayer films represent a substantial avenue for growth. As consumer awareness about environmental impact rises and regulatory pressures intensify, manufacturers who can offer high-performance, eco-friendly alternatives will gain a competitive edge and tap into a rapidly expanding market segment. Investment in bio-based polymers and innovative film structures that maintain barrier properties while being compostable or easily recyclable presents a clear path for future market penetration.

Beyond sustainability, the increasing demand for smart packaging solutions offers a niche yet high-value opportunity. Integrating features like RFID tags, QR codes, or even embedded sensors for temperature monitoring or freshness indication within multilayer films can add significant value, particularly in sensitive sectors such as pharmaceuticals, food and beverage, and logistics. Emerging economies, especially in Asia Pacific and Latin America, present vast untapped markets for multilayer films due to their expanding middle class, rapid urbanization, and growing organized retail sectors. These regions are witnessing increased adoption of packaged goods, creating new demand for advanced barrier films. Furthermore, specialized applications in healthcare, electronics, and automotive industries continue to offer opportunities for tailor-made, high-performance multilayer film solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of sustainable and recyclable multilayer films | +1.2% | Global | 2025-2033 (Long-term) |

| Growing demand for smart packaging and functional films | +0.9% | North America, Europe, Asia Pacific | 2028-2033 (Long-term) |

| Expansion into emerging economies and untapped markets | +0.8% | Asia Pacific, Latin America, MEA | 2025-2033 (Long-term) |

| Niche applications in medical, electronics, and automotive sectors | +0.7% | Global | 2025-2030 (Mid-term) |

| Advancements in bio-based and compostable polymer technologies | +1.0% | Europe, North America | 2027-2033 (Long-term) |

Multilayer Film Market Challenges Impact Analysis

The multilayer film market faces several significant challenges that could impede its growth trajectory and demand strategic responses from industry players. One major challenge is the inherent complexity of recycling multi-material film structures. While individual layers may be recyclable, the combination of different polymers (e.g., PE, PA, EVOH, PET) makes separation and reprocessing extremely difficult, leading to a significant portion of multilayer film waste ending up in landfills or incineration. This issue is exacerbated by increasing global pressure to establish circular economies and reduce plastic pollution, forcing manufacturers to invest heavily in mono-material alternatives or advanced recycling technologies that are still in their nascent stages.

Another formidable challenge is the volatile pricing and supply chain disruptions of raw materials. The multilayer film industry is heavily reliant on petrochemical derivatives, whose prices are subject to global oil market fluctuations and geopolitical instability. Such volatility can unpredictably impact production costs, squeeze profit margins, and complicate long-term strategic planning. Furthermore, geopolitical tensions or natural disasters can disrupt global supply chains, leading to raw material shortages and production delays. Maintaining consistent product quality across various layers and ensuring optimal adhesion between different polymer types during the co-extrusion process also presents technical challenges, requiring continuous innovation and stringent process control to meet diverse customer specifications.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Difficulty in recycling multi-material film structures | -1.0% | Global | 2025-2033 (Long-term) |

| Volatile raw material prices and supply chain disruptions | -0.8% | Global | 2025-2028 (Short-term to Mid-term) |

| High production costs and energy consumption | -0.5% | Global | 2025-2033 (Long-term) |

| Intense competition and pricing pressure from regional players | -0.4% | Global | 2025-2033 (Long-term) |

| Maintaining consistent quality and performance across diverse applications | -0.3% | Global | 2025-2033 (Long-term) |

Multilayer Film Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Multilayer Film Market, offering a detailed understanding of its size, growth trends, key drivers, restraints, opportunities, and challenges across various segments and regions. It encompasses a historical review of market performance from 2019 to 2023, coupled with a robust forecast spanning 2025 to 2033, enabling stakeholders to make informed strategic decisions. The report delves into the impact of emerging technologies and sustainability mandates, providing a holistic view of the market's evolving landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 36.8 Billion |

| Growth Rate | 14.3% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amcor plc, Berry Global Inc., Sealed Air Corporation, Huhtamäki Oyj, Mondi Group, RPC Group (part of Berry Global), Schur Flexibles Group, Coveris Holdings SA, Winpak Ltd., TC Transcontinental Inc., Jindal Poly Films Limited, Uflex Ltd., RKW Group, Toray Industries Inc., Mitsui Chemicals Inc., Futamura Chemical Co. Ltd., Mitsubishi Chemical Corporation, Sumitomo Chemical Co. Ltd., Novolex, Alpla Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The multilayer film market is extensively segmented by material, application, end-use industry, and layer type, providing a granular view of market dynamics and growth opportunities within specific categories. This detailed segmentation allows for a precise understanding of which materials are gaining traction, which applications are driving demand, and where the most significant growth pockets lie across various industrial sectors. Each segment exhibits unique characteristics and growth drivers, reflecting the diverse requirements of modern packaging and industrial applications.

The material segmentation highlights the dominance of polyethylenes and polypropylenes, alongside the increasing adoption of specialized barrier resins like EVOH and PA for enhanced product protection. Application-wise, food packaging remains the largest segment, but pharmaceutical and industrial packaging are demonstrating robust growth. End-use industries such as food & beverage and healthcare are pivotal consumers, with expanding demand from e-commerce and agriculture. The varying layer types signify the complexity and performance requirements of films, from simpler 3-layer structures to advanced 9-layer and 11-layer configurations offering superior barrier and mechanical properties. This comprehensive segmentation is crucial for stakeholders to identify key market niches and tailor their strategies effectively.

- By Material:

- Polyethylene (PE)

- Polypropylene (PP)

- Polyamide (PA)

- Ethylene Vinyl Alcohol (EVOH)

- Polyethylene Terephthalate (PET)

- Polyvinylidene Chloride (PVDC)

- Others (e.g., PLA, PHA, PVC)

- By Application:

- Food Packaging

- Pharmaceutical Packaging

- Personal Care Packaging

- Industrial Packaging

- Agricultural Films

- Medical Films

- Consumer Goods Packaging

- Others

- By End-Use Industry:

- Food & Beverage

- Healthcare

- Personal Care & Cosmetics

- Automotive

- Electrical & Electronics

- Agriculture

- Building & Construction

- Industrial

- Others

- By Layer Type:

- 3-Layer

- 5-Layer

- 7-Layer

- 9-Layer

- 11-Layer and Above

Regional Highlights

- North America: This region maintains a significant market share driven by advanced packaging technologies, high consumer demand for convenience foods, and stringent food safety regulations. Innovation in sustainable and smart packaging solutions is a key trend, with substantial investments in recycling infrastructure and bio-based materials.

- Europe: Europe is a mature market characterized by strong regulatory emphasis on sustainability and circular economy principles. The region is at the forefront of developing recyclable and compostable multilayer films, driven by consumer preference for eco-friendly packaging and government initiatives to reduce plastic waste. Germany, France, and the UK are key contributors.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, primarily due to rapid industrialization, increasing disposable incomes, and the booming food & beverage, pharmaceutical, and e-commerce sectors in countries like China, India, and Japan. The expanding middle class and urbanization are fueling demand for packaged goods, leading to robust market expansion.

- Latin America: This region exhibits steady growth, influenced by improving economic conditions, a growing retail sector, and increasing demand for packaged food and personal care products. Brazil and Mexico are key markets, showing rising adoption of advanced packaging solutions.

- Middle East and Africa (MEA): The MEA market is experiencing gradual growth, propelled by expanding food processing industries, increasing population, and rising foreign investments. Infrastructure development and a shift towards modern retail formats are contributing to the demand for multilayer films, particularly in the GCC countries and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Multilayer Film Market.- Amcor plc

- Berry Global Inc.

- Sealed Air Corporation

- Huhtamäki Oyj

- Mondi Group

- Schur Flexibles Group

- Coveris Holdings SA

- Winpak Ltd.

- TC Transcontinental Inc.

- Jindal Poly Films Limited

- Uflex Ltd.

- RKW Group

- Toray Industries Inc.

- Mitsui Chemicals Inc.

- Futamura Chemical Co. Ltd.

- Mitsubishi Chemical Corporation

- Sumitomo Chemical Co. Ltd.

- Novolex

- Alpla Group

- Toyobo Co. Ltd.

Frequently Asked Questions

What is the projected growth rate of the Multilayer Film Market?

The Multilayer Film Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 14.3% between 2025 and 2033, reaching an estimated value of USD 36.8 Billion by 2033.

Which factors are primarily driving the Multilayer Film Market?

Key drivers include the surging global demand for packaged food and beverages, the rapid expansion of the e-commerce sector requiring robust packaging, and continuous technological advancements in film properties and manufacturing processes that enhance product shelf life and protection.

What are the main challenges faced by the Multilayer Film Market?

Major challenges involve the complexity and difficulty in recycling multi-material film structures, leading to environmental concerns, and the volatility of raw material prices coupled with potential supply chain disruptions.

How is sustainability impacting the Multilayer Film Market?

Sustainability is a crucial trend, driving significant innovation towards recyclable, biodegradable, and compostable multilayer film solutions. This shift is influenced by stringent environmental regulations and increasing consumer demand for eco-friendly packaging alternatives.

Which region is expected to lead the growth in the Multilayer Film Market?

The Asia Pacific (APAC) region is anticipated to be the fastest-growing market for multilayer films, fueled by rapid industrialization, urbanization, increasing disposable incomes, and the booming food & beverage and e-commerce sectors in countries like China and India.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted