MPL and SD WAN Market

MPL and SD WAN Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708109 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

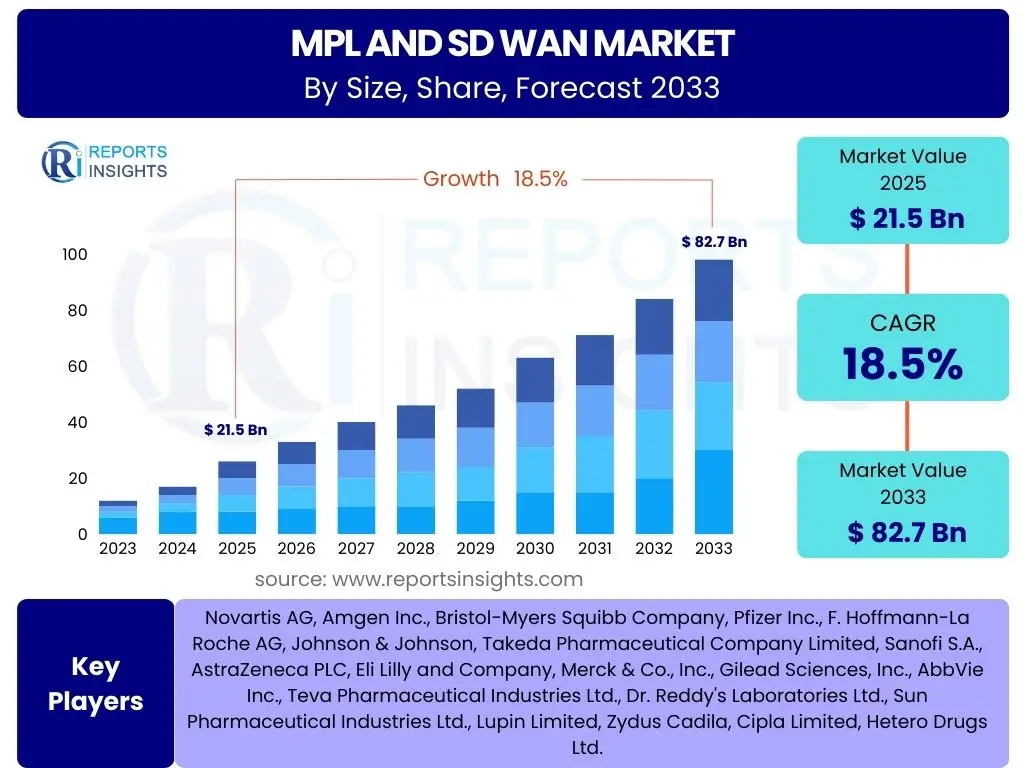

MPL and SD WAN Market Size

According to Reports Insights Consulting Pvt Ltd, The MPL and SD WAN Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 21.5 billion in 2025 and is projected to reach USD 82.7 billion by the end of the forecast period in 2033.

Key MPL and SD WAN Market Trends & Insights

The MPL and SD WAN market is experiencing dynamic shifts driven by the evolving needs of modern enterprises for robust, flexible, and secure network infrastructure. Organizations are increasingly migrating from traditional MPLS networks to software-defined wide area networks (SD WAN) to support cloud-first strategies, distributed workforces, and escalating bandwidth demands. This transition is not merely about technology adoption but reflects a fundamental rethinking of network architecture to achieve greater agility, cost efficiency, and enhanced application performance across diverse environments.

A significant trend involves the convergence of networking and security functions, leading to the rise of Secure Access Service Edge (SASE) solutions. Enterprises are seeking integrated platforms that combine SD WAN capabilities with comprehensive security features like firewall-as-a-service, secure web gateways, and zero-trust network access. This integrated approach simplifies management, improves security posture, and optimizes the user experience, particularly for remote and mobile users. Furthermore, automation and artificial intelligence are playing a crucial role in enhancing network operations, enabling proactive management, and optimizing resource allocation within these hybrid networking environments.

- Accelerated adoption of cloud-native applications and services.

- Increased demand for SASE (Secure Access Service Edge) architecture.

- Growing emphasis on network automation and orchestration.

- Integration of advanced security features at the network edge.

- Shift towards hybrid WAN deployments combining MPLS and SD WAN.

- Expansion of managed SD WAN services for simplified operations.

- Prioritization of application performance and user experience.

AI Impact Analysis on MPL and SD WAN

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is profoundly transforming the MPL and SD WAN landscape, moving beyond basic network management to enable highly autonomous and optimized network operations. Users frequently inquire about how AI can provide predictive analytics for network performance, proactively identify anomalies, and automate complex troubleshooting, thereby reducing human intervention and improving operational efficiency. The expectation is that AI will make networks more intelligent, capable of self-healing and dynamic resource allocation, adapting to real-time traffic conditions and security threats.

Furthermore, there is significant interest in AI's role in enhancing network security within SD WAN environments. AI-powered systems can analyze vast amounts of network traffic data to detect sophisticated cyber threats, identify unusual user behaviors, and automatically enforce security policies, significantly bolstering defense mechanisms against evolving attack vectors. For generative engine optimization (GEO), the focus often centers on the tangible benefits such as cost reduction through optimized bandwidth utilization, improved application uptime, and a more secure infrastructure that can dynamically respond to challenges without manual configuration. This leads to a network that is not only agile but also resilient and intelligent, providing a competitive edge for businesses navigating complex digital transformations.

- Enhanced network visibility and monitoring through predictive analytics.

- Automated threat detection and response capabilities for improved security.

- Intelligent traffic steering and routing optimization based on real-time conditions.

- Proactive identification of network anomalies and performance degradation.

- Automated resource allocation and bandwidth management.

- Simplified network operations and reduced manual configuration efforts.

- Improved troubleshooting and root cause analysis.

Key Takeaways MPL and SD WAN Market Size & Forecast

The MPL and SD WAN market is poised for substantial growth over the next decade, reflecting a fundamental shift in enterprise networking strategies. The projected Compound Annual Growth Rate (CAGR) of 18.5% highlights the strong market momentum driven by the imperative for digital transformation, cloud adoption, and the increasing complexity of distributed IT environments. This robust growth signifies that organizations are actively investing in modern network solutions that offer greater agility, cost efficiency, and enhanced performance compared to traditional networking approaches. The significant increase from USD 21.5 billion in 2025 to USD 82.7 billion by 2033 underscores the widespread recognition of SD WAN's capabilities in addressing contemporary business demands.

Key insights reveal that this market expansion is not solely about technology adoption but encompasses a broader strategic re-evaluation of network infrastructure to support a future-ready enterprise. The market forecast indicates a sustained period of innovation, with continued integration of advanced features such as AI, machine learning, and comprehensive security solutions into SD WAN platforms. The substantial growth figures also suggest a maturing market where enterprises are moving beyond initial pilot projects to full-scale deployments, further solidifying SD WAN as a foundational component of modern IT landscapes. This indicates a strong market confidence in the long-term value and transformative potential of these networking technologies.

- The market exhibits robust double-digit growth, indicating strong enterprise adoption.

- Significant market expansion is driven by digital transformation and cloud-first initiatives.

- SD WAN is rapidly becoming the preferred wide area network solution for modern enterprises.

- Future growth will be fueled by continuous innovation and integration with emerging technologies.

- The market shift from traditional MPLS to SD WAN is a long-term strategic trend.

- Increased investment in network modernization is a core driver of market value.

- The market is expected to quadruple in value between 2025 and 2033, reflecting widespread demand.

MPL and SD WAN Market Drivers Analysis

The MPL and SD WAN market is significantly propelled by the accelerated pace of digital transformation across all industries. Enterprises are increasingly reliant on cloud-based applications and services, which necessitate a network infrastructure capable of delivering consistent, high-performance connectivity from any location to any cloud. Traditional MPLS networks, while reliable, often struggle with the agility and cost-effectiveness required to route traffic optimally to multiple cloud environments, making SD WAN an attractive alternative. The demand for flexible and scalable networking solutions that can adapt quickly to changing business requirements without incurring prohibitive costs is a primary force driving market growth.

Furthermore, the growing adoption of hybrid work models and the proliferation of internet-connected devices (IoT) at the edge demand a network that is secure, responsive, and easy to manage across a geographically dispersed footprint. SD WAN addresses these challenges by offering centralized control, simplified deployment, and robust security features that can be extended to remote offices and mobile users. The ability to prioritize critical application traffic, optimize bandwidth utilization, and reduce operational expenses through automation further strengthens the business case for SD WAN, encouraging widespread adoption across small, medium, and large enterprises seeking to modernize their networking capabilities and enhance overall operational efficiency.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Cloud Adoption | +4.2% | Global (North America, Europe, APAC) | Short-term to Long-term |

| Digital Transformation Initiatives | +3.8% | Global (All Regions) | Short-term to Long-term |

| Demand for Network Flexibility & Agility | +3.5% | Global | Medium-term |

| Cost Optimization & Operational Efficiency | +3.0% | Global (Emerging Markets) | Medium-term |

| Growth of Hybrid Work Models | +2.5% | North America, Europe | Short-term |

MPL and SD WAN Market Restraints Analysis

Despite the numerous advantages, the MPL and SD WAN market faces several significant restraints that could temper its growth. One primary challenge is the high initial investment required for deploying new SD WAN infrastructure, especially for large enterprises with extensive legacy networks. Migrating from established MPLS environments involves not only hardware and software costs but also substantial resources for planning, integration, and training, which can be a deterrent for organizations with limited capital budgets. This financial hurdle can prolong the adoption cycle, particularly for small and medium-sized enterprises.

Another key restraint involves the complexity associated with integrating SD WAN solutions into existing diverse IT ecosystems. Many organizations operate hybrid networks that combine MPLS, broadband, and various legacy systems, making seamless interoperability and unified management a significant technical challenge. Concerns over security are also prevalent, as moving to a more distributed network architecture can introduce new vulnerabilities if not properly secured, leading to hesitancy among enterprises, especially those in highly regulated industries. Furthermore, the lack of skilled personnel capable of designing, deploying, and managing advanced SD WAN architectures presents an operational bottleneck, impacting the speed and success of implementations globally.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Deployment Costs | -2.8% | Global (SMEs, Emerging Markets) | Short-term to Medium-term |

| Complexity of Migration & Integration | -2.5% | Global (Large Enterprises) | Short-term to Medium-term |

| Perceived Security Concerns | -2.0% | Global (Highly Regulated Industries) | Medium-term |

| Lack of Skilled Workforce | -1.8% | Global | Medium-term to Long-term |

MPL and SD WAN Market Opportunities Analysis

The MPL and SD WAN market presents numerous opportunities for growth and innovation, particularly with the continued proliferation of emerging technologies and evolving business models. One significant avenue lies in the expansion of managed SD WAN services, as many enterprises, especially SMEs, lack the in-house expertise or resources to deploy and manage complex networking solutions. Service providers offering comprehensive managed SD WAN, including design, implementation, and ongoing support, can tap into this demand, allowing businesses to leverage advanced networking capabilities without the operational burden, thereby accelerating market adoption and penetration.

Another substantial opportunity emerges from the convergence of SD WAN with edge computing and 5G technologies. As businesses increasingly process data closer to its source for real-time insights and reduced latency, SD WAN can provide the optimized and secure connectivity required for edge deployments. Similarly, the rollout of 5G networks offers high-bandwidth, low-latency wireless connectivity that can be seamlessly integrated into SD WAN architectures, expanding network reach and providing diverse transport options. The growing market for Secure Access Service Edge (SASE) also represents a significant opportunity, as it combines SD WAN with comprehensive security functions, catering to the increasing demand for integrated networking and security solutions, particularly crucial for distributed workforces and cloud environments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Managed SD WAN Services | +3.5% | Global (SMEs, Enterprises seeking operational simplicity) | Short-term to Long-term |

| SASE (Secure Access Service Edge) Convergence | +3.2% | Global (Enterprises with distributed workforce & cloud) | Short-term to Long-term |

| Integration with Edge Computing & 5G | +2.8% | North America, Europe, Asia Pacific | Medium-term to Long-term |

| Vertical-Specific SD WAN Solutions | +2.0% | Global (Healthcare, Retail, Manufacturing, BFSI) | Medium-term |

MPL and SD WAN Market Challenges Impact Analysis

The MPL and SD WAN market, while experiencing rapid growth, faces several challenges that require strategic navigation. One major hurdle is ensuring consistent application performance across diverse underlying transport networks, including a mix of broadband, MPLS, and 5G. Maintaining quality of service (QoS) for critical applications, especially voice and video, can be complex in dynamic SD WAN environments where traffic is routed over various paths, some of which may be less reliable. This complexity can lead to user dissatisfaction and negate some of the anticipated benefits of SD WAN if not meticulously managed and optimized.

Another significant challenge revolves around managing the security implications of a more decentralized network perimeter. As traffic bypasses traditional centralized data center security stacks and goes directly to cloud services or remote branches, ensuring consistent security policy enforcement across all endpoints becomes critical. Interoperability issues with existing legacy systems and varying vendor solutions also pose a challenge, leading to vendor lock-in concerns and hindering seamless integration. Furthermore, regulatory compliance and data privacy concerns, particularly for organizations operating across multiple jurisdictions, add layers of complexity to SD WAN deployments, requiring careful planning and adherence to diverse legal frameworks. Addressing these challenges is paramount for sustained market growth and successful enterprise adoption.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring Consistent Application Performance | -2.3% | Global | Short-term to Medium-term |

| Managing Security in Distributed Environments | -2.0% | Global | Short-term to Medium-term |

| Interoperability with Legacy Systems & Vendor Lock-in | -1.7% | Global (Large Enterprises) | Medium-term |

| Regulatory Compliance & Data Privacy | -1.5% | Global (Highly Regulated Industries) | Long-term |

MPL and SD WAN Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global MPL and SD WAN market, offering critical insights into its current size, historical growth, and future projections. The scope encompasses detailed market segmentation, identification of key growth drivers, significant restraints, emerging opportunities, and prevailing challenges influencing market dynamics. The report leverages a robust research methodology to present an accurate and actionable understanding of the market landscape for stakeholders, investors, and industry participants.

Focused on delivering strategic intelligence, the report also includes an exhaustive regional analysis, spotlighting key geographical markets and their unique contributions to the overall market trajectory. A competitive landscape section profiles major market players, detailing their strategic initiatives, product offerings, and market positioning. Furthermore, the report integrates an AI impact analysis to shed light on how artificial intelligence is reshaping network capabilities and operational efficiencies within the MPL and SD WAN domain, providing a holistic view of the market's technological evolution and future potential.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 21.5 billion |

| Market Forecast in 2033 | USD 82.7 billion |

| Growth Rate | 18.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Cisco Systems Inc., VMware Inc., Fortinet Inc., Versa Networks, Juniper Networks Inc., Aryaka Networks Inc., Palo Alto Networks Inc., Citrix Systems Inc., Silver Peak (HPE), Zscaler Inc., Cato Networks, Nokia Corporation, Huawei Technologies Co. Ltd., Dell Technologies, Barracuda Networks Inc., Check Point Software Technologies Ltd., Extreme Networks Inc., Riverbed Technology LLC, Oracle Corporation, Ericsson AB |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The MPL and SD WAN market is comprehensively segmented to provide a granular view of its diverse components and adoption patterns across various enterprise demographics and industries. This detailed segmentation allows for a deeper understanding of market dynamics, identifying specific growth areas, and recognizing the unique requirements of different user groups. The market is primarily broken down by component, deployment type, enterprise size, and vertical, reflecting the multifaceted nature of network solution adoption in today's digital landscape.

By dissecting the market along these lines, the report provides critical insights into which solution categories are experiencing the most significant demand, whether cloud-based or on-premise deployments are preferred, and how adoption varies between small, medium, and large enterprises. Furthermore, the vertical segmentation highlights how specific industries, such as BFSI, IT & Telecom, and Healthcare, are leveraging MPL and SD WAN technologies to address their distinct operational and regulatory challenges. This comprehensive analysis helps stakeholders identify lucrative niches and tailor their strategies to target specific market segments effectively, optimizing their market penetration and growth opportunities.

- By Component: This segment distinguishes between the tangible elements and the service-based offerings.

- Solutions: Includes the underlying hardware and software infrastructure that enables SD WAN functionality.

- Hardware: Physical appliances, routers, and other network devices.

- Software: Control plane, management plane, orchestration platforms, and virtual network functions.

- Services: Encompasses the support and management offerings provided by vendors and third parties.

- Managed Services: Outsourced management of the SD WAN infrastructure.

- Professional Services: Consulting, design, and implementation assistance.

- Consulting Services: Strategic advice and guidance for network transformation.

- Solutions: Includes the underlying hardware and software infrastructure that enables SD WAN functionality.

- By Deployment: Categorizes solutions based on their hosting environment.

- On-Premise: SD WAN infrastructure deployed and managed within the enterprise's own data centers or branch offices.

- Cloud-Based: SD WAN services delivered and managed entirely from the cloud.

- Hybrid: A combination of on-premise and cloud-based deployments, offering flexibility.

- By Enterprise Size: Differentiates adoption based on the scale of the organization.

- Small & Medium Enterprises (SMEs): Businesses with limited IT resources and budget, often opting for managed services.

- Large Enterprises: Organizations with extensive and complex networks, requiring scalable and customizable solutions.

- By Vertical: Examines market penetration across different industry sectors.

- BFSI (Banking, Financial Services, and Insurance): Driven by security, compliance, and high availability needs.

- Retail & E-commerce: Focused on branch connectivity, secure transactions, and enhanced customer experience.

- IT & Telecom: Early adopters leveraging SD WAN for internal infrastructure and offering services to customers.

- Healthcare: Emphasizing secure data transfer, remote access, and reliable connectivity for critical applications.

- Government & Public Sector: Prioritizing secure communication, cost efficiency, and wide-area network modernization.

- Manufacturing: Optimizing connectivity for IoT, industrial automation, and supply chain management.

- Energy & Utilities: Ensuring reliable communication for distributed infrastructure and operational technology.

- Media & Entertainment: Requiring high bandwidth for content delivery and production workflows.

- Others: Including education, logistics, and transportation sectors.

Regional Highlights

The global MPL and SD WAN market exhibits significant regional variations, influenced by differing levels of digital maturity, regulatory landscapes, and investment capacities. North America currently holds the largest market share, driven by a high concentration of advanced technology enterprises, early adoption of cloud computing, and a robust focus on network modernization and security. The presence of key market players and a strong demand for agile network infrastructures to support extensive distributed workforces further contribute to the region's dominance. Investment in advanced managed services and SASE architectures is particularly pronounced in this region, setting global trends.

Europe represents another significant market, characterized by a strong emphasis on data privacy and regulatory compliance, such as GDPR, which shapes SD WAN deployment strategies. The region sees steady growth as businesses migrate from legacy systems to embrace digital transformation and support cross-border operations. Asia Pacific (APAC) is projected to be the fastest-growing region, fueled by rapid economic development, increasing internet penetration, and aggressive cloud adoption across emerging economies like China and India. Government initiatives for smart cities and digital infrastructure development are accelerating SD WAN deployments. Latin America, the Middle East, and Africa (MEA) are emerging markets, with growth primarily driven by infrastructure development, increasing enterprise connectivity needs, and the expansion of cloud services, though adoption rates may vary due to economic factors and technological readiness.

- North America: Dominant market share due to high technology adoption, cloud-first strategies, and mature IT infrastructure. Key countries include the United States and Canada.

- Europe: Significant market with steady growth, driven by digital transformation, stringent regulatory environments (e.g., GDPR), and a strong demand for hybrid network solutions. Key countries include Germany, the United Kingdom, France, and Nordic countries.

- Asia Pacific (APAC): Fastest-growing region, propelled by rapid economic expansion, increasing internet penetration, cloud services adoption, and government support for digital initiatives. Key countries include China, India, Japan, Australia, and South Korea.

- Latin America: Emerging market with growing adoption fueled by increasing enterprise connectivity, infrastructure development, and demand for cost-effective network solutions. Key countries include Brazil and Mexico.

- Middle East and Africa (MEA): Developing market driven by investment in smart cities, digital transformation projects, and the expansion of cloud computing, particularly in the Gulf Cooperation Council (GCC) countries and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the MPL and SD WAN Market.- Cisco Systems Inc.

- VMware Inc.

- Fortinet Inc.

- Versa Networks

- Juniper Networks Inc.

- Aryaka Networks Inc.

- Palo Alto Networks Inc.

- Citrix Systems Inc.

- Silver Peak (HPE)

- Zscaler Inc.

- Cato Networks

- Nokia Corporation

- Huawei Technologies Co. Ltd.

- Dell Technologies

- Barracuda Networks Inc.

- Check Point Software Technologies Ltd.

- Extreme Networks Inc.

- Riverbed Technology LLC

- Oracle Corporation

- Ericsson AB

Frequently Asked Questions

What is SD WAN and how does it compare to MPLS?

SD WAN (Software-Defined Wide Area Network) is a virtual WAN architecture that allows enterprises to leverage various transport services, including MPLS, broadband internet, and 5G, to securely connect users to applications. Unlike traditional MPLS, which uses dedicated circuits for traffic, SD WAN provides centralized control and intelligence to dynamically route traffic over the most efficient and cost-effective path, enhancing agility, performance, and reducing operational costs for cloud-centric environments.

What are the primary benefits of adopting SD WAN for an enterprise?

Enterprises adopting SD WAN experience several key benefits, including significant cost savings by reducing reliance on expensive MPLS circuits, improved application performance through intelligent traffic steering, enhanced network agility and flexibility, simplified network management with centralized control, and robust security features integrated at the network edge. It enables efficient connectivity for distributed workforces and cloud applications.

How does AI impact the future of MPLS and SD WAN networks?

AI significantly impacts networking by enabling predictive analytics for performance optimization, automated threat detection and response, intelligent traffic management, and proactive identification of anomalies. In SD WAN, AI facilitates self-healing networks, dynamic resource allocation, and simplified operations, moving towards more autonomous and secure network infrastructures that adapt to real-time conditions without manual intervention.

What are the main security considerations when deploying an SD WAN solution?

Security considerations for SD WAN include ensuring consistent policy enforcement across all distributed sites and cloud environments, integrating robust encryption for data in transit, implementing secure access service edge (SASE) principles, and deploying advanced threat protection at the network edge. It is crucial to have a comprehensive security framework that covers firewalls, intrusion prevention, and secure web gateways to protect against evolving cyber threats.

What industries are most actively adopting SD WAN and why?

Industries most actively adopting SD WAN include IT & Telecom, Retail & E-commerce, BFSI, and Healthcare. These sectors benefit from SD WAN's ability to support cloud applications, enhance branch connectivity, ensure secure transactions, improve customer experience, and meet stringent regulatory compliance requirements while optimizing network costs and performance for their distributed operations.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted