Mono Ethylene Glycol Market

Mono Ethylene Glycol Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710216 | Last Updated : December 30, 2025 |

Format : ![]()

![]()

![]()

![]()

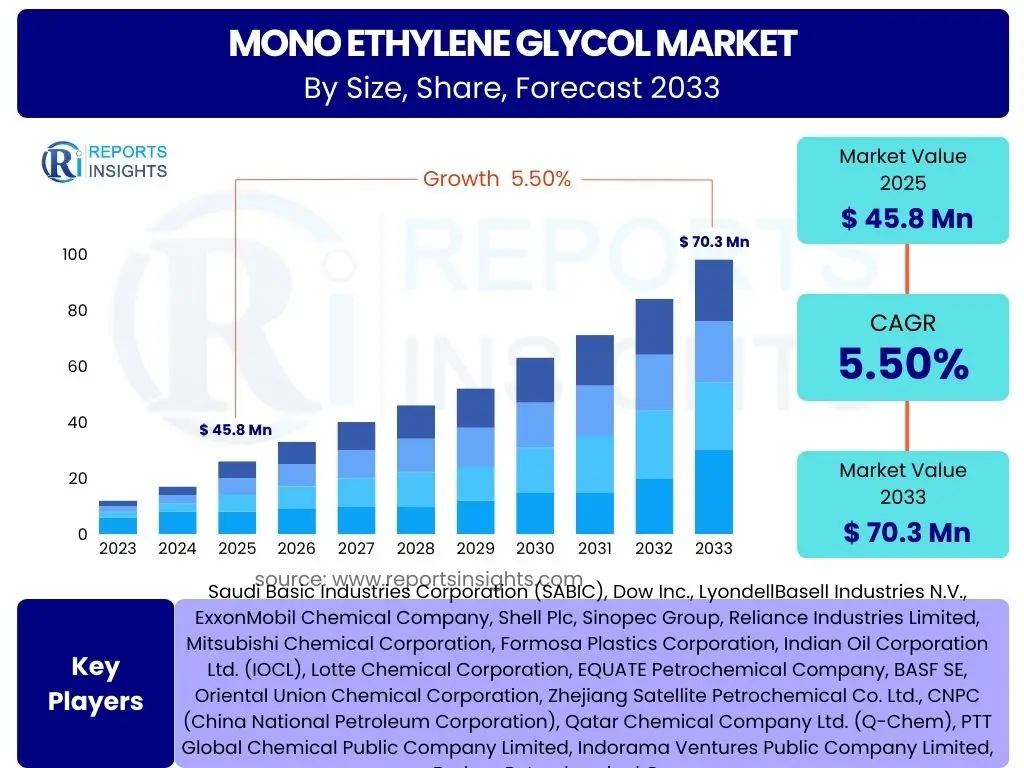

Mono Ethylene Glycol Market Size

According to Reports Insights Consulting Pvt Ltd, The Mono Ethylene Glycol Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2025 and 2033. The market is estimated at USD 45.8 billion in 2025 and is projected to reach USD 70.3 billion by the end of the forecast period in 2033.

Key Mono Ethylene Glycol Market Trends & Insights

The Mono Ethylene Glycol (MEG) market is currently undergoing significant transformation, driven by evolving consumer demands, technological advancements, and a heightened focus on environmental sustainability. Stakeholders are keen to understand the primary forces shaping demand, such as the growth of the polyester and PET packaging industries, particularly in emerging economies. There is also considerable interest in how geopolitical factors and raw material price volatility influence market stability and investment decisions. Furthermore, the industry is witnessing a shift towards greener production methods and bio-based MEG, reflecting a broader commitment to reducing carbon footprints and enhancing circularity in chemical manufacturing processes.

Digitalization and automation are increasingly being integrated into MEG production to optimize efficiency and reduce operational costs. This includes advanced process control systems and predictive maintenance technologies that enhance plant reliability and output. The market is also observing a regional divergence in growth patterns, with Asia Pacific continuing to dominate both production and consumption, while North America and Europe focus on higher-value applications and sustainable solutions. The interplay of these trends suggests a dynamic market landscape where innovation and strategic adaptation will be crucial for competitive advantage and sustained growth.

- Surging demand from the polyester fiber and PET resin industries, particularly in Asia Pacific.

- Growing adoption of bio-based Mono Ethylene Glycol (Bio-MEG) driven by sustainability initiatives.

- Increasing investment in capacity expansion in feedstock-rich regions like the Middle East and North America.

- Technological advancements in production processes aimed at improving energy efficiency and reducing emissions.

- Fluctuations in crude oil and natural gas prices directly impacting ethylene feedstock costs and MEG pricing.

- Emergence of new applications in automotive coolants, heat transfer fluids, and construction materials.

AI Impact Analysis on Mono Ethylene Glycol

The chemical industry, including Mono Ethylene Glycol production, is increasingly exploring the transformative potential of Artificial intelligence (AI). Common inquiries revolve around how AI can enhance operational efficiency, optimize supply chain logistics, and contribute to sustainable practices within MEG manufacturing. Users are particularly interested in AI's role in predictive maintenance to prevent costly downtimes, real-time process optimization to improve yield and reduce energy consumption, and intelligent inventory management systems to minimize waste and storage costs. The integration of AI for advanced data analytics is expected to provide deeper insights into market dynamics, enabling more informed decision-making regarding production planning and raw material procurement.

While the benefits are clear, there are also concerns and expectations regarding the practical implementation of AI in existing infrastructure, the need for skilled personnel, and the data privacy and security implications. The long-term outlook suggests that AI will not only streamline current operations but also drive innovation in discovering new catalysts, improving chemical synthesis pathways for MEG, and accelerating the development of novel sustainable MEG alternatives. AI's ability to process vast datasets quickly offers a significant competitive advantage for companies that can effectively deploy these technologies, leading to more resilient, efficient, and environmentally responsible MEG production. This shift is expected to enhance overall profitability and market responsiveness for leading producers.

- Enhanced operational efficiency through AI-powered predictive maintenance and process optimization.

- Improved supply chain management, including demand forecasting and logistics optimization.

- Development of advanced catalysts and material science through AI-driven research and development.

- Reduction in energy consumption and waste generation through intelligent process control systems.

- Real-time quality control and anomaly detection, ensuring consistent product specifications.

- Data-driven decision-making for raw material procurement and production scheduling.

Key Takeaways Mono Ethylene Glycol Market Size & Forecast

Stakeholders frequently seek concise insights into the most critical aspects of the Mono Ethylene Glycol market’s projected growth and overall health. Key questions often center on the primary drivers of market expansion, the influence of evolving global economic conditions, and the potential impact of sustainability initiatives on future demand and production strategies. Understanding the regional market dynamics, particularly the continued dominance of the Asia Pacific region and the strategic shifts in developed markets, is also a common focus. Furthermore, insights into the resilience of the MEG market against raw material price volatility and geopolitical uncertainties are highly valued for strategic planning.

The market forecast reveals a robust growth trajectory, primarily fueled by sustained demand from the polyester and PET sectors, alongside increasing applications in the automotive and construction industries. The emphasis on bio-based MEG and recycling initiatives will progressively reshape the competitive landscape, creating new opportunities for innovation and differentiation. Companies that can effectively navigate regulatory complexities, invest in advanced production technologies, and establish resilient supply chains are poised to capitalize on this growth. The long-term outlook suggests a market characterized by continuous innovation and a growing imperative for sustainable practices across the value chain.

- The Mono Ethylene Glycol market is set for consistent growth, primarily driven by strong demand from polyester fiber and PET resin manufacturing.

- Asia Pacific will remain the dominant region, offering significant opportunities for market expansion and capacity additions.

- Sustainability initiatives, including the adoption of bio-based MEG and recycling technologies, are pivotal for long-term market evolution.

- Volatile raw material prices and geopolitical factors will necessitate agile supply chain management and diversified sourcing strategies.

- Technological advancements in production efficiency and carbon footprint reduction are becoming key competitive differentiators.

Mono Ethylene Glycol Market Drivers Analysis

The Mono Ethylene Glycol market is primarily driven by the robust expansion of its key end-use industries, particularly the textile and packaging sectors. The escalating global demand for polyester fibers in apparel, home furnishings, and industrial applications continues to be a foundational driver. Simultaneously, the pervasive use of Polyethylene Terephthalate (PET) resins in beverage bottles, food containers, and various packaging solutions contributes significantly to MEG consumption. Economic growth, especially in emerging economies, further fuels this demand by increasing consumer spending on packaged goods and synthetic textiles. The increasing population and urbanization trends worldwide also translate into higher consumption of these products, directly boosting the need for MEG.

Beyond these established applications, the market also benefits from a growing demand for MEG in antifreeze and coolant formulations for the automotive sector, driven by increasing vehicle production and maintenance requirements. Furthermore, its role as a chemical intermediate in various industrial processes, including the production of unsaturated polyester resins and de-icing fluids, supports its consistent market expansion. Strategic investments in infrastructure development, such as roads and buildings, indirectly spur demand for MEG derivatives used in construction materials. These multifaceted drivers create a strong positive feedback loop, ensuring sustained growth for the Mono Ethylene Glycol market over the forecast period.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Polyester Fiber Demand | +1.8% | Asia Pacific (China, India) | Long-term (2025-2033) |

| Expansion of PET Packaging Industry | +1.5% | Global, especially Emerging Economies | Medium to Long-term (2025-2033) |

| Increased Automotive Coolant Applications | +0.8% | North America, Europe, Asia Pacific | Medium-term (2025-2030) |

| Urbanization and Infrastructure Development | +0.7% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

| Technological Advancements in Production | +0.5% | Global | Medium-term (2025-2030) |

Mono Ethylene Glycol Market Restraints Analysis

The Mono Ethylene Glycol market faces several significant restraints that could temper its growth trajectory. One of the primary concerns is the volatility in raw material prices, particularly ethylene, which is derived from crude oil and natural gas. Fluctuations in energy markets directly impact the cost of MEG production, leading to unpredictable profit margins for manufacturers and potential price instability for end-users. This price sensitivity can deter new investments and hinder long-term planning, particularly for smaller market players. Geopolitical instability in key oil-producing regions can further exacerbate these price swings, adding another layer of uncertainty to the supply chain.

Another substantial restraint is the increasing environmental scrutiny and stringent regulatory frameworks concerning petrochemical production. Growing pressure to reduce carbon emissions and minimize the environmental footprint of chemical processes necessitates significant investment in cleaner technologies and sustainable practices, which can increase operational costs. The shift towards a circular economy and the development of alternative materials, while creating opportunities in some areas, also presents a long-term threat to traditional MEG demand. Additionally, the oversupply of MEG in certain regions due to large-scale capacity additions has occasionally led to downward pressure on prices, impacting profitability and market stability. These combined factors require careful strategic navigation from market participants.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (Ethylene) | -1.2% | Global | Long-term (2025-2033) |

| Stringent Environmental Regulations | -0.9% | Europe, North America, Asia Pacific | Long-term (2025-2033) |

| Oversupply in Key Regions | -0.7% | Asia Pacific, Middle East | Medium-term (2025-2030) |

| Competition from Alternative Materials | -0.5% | Global | Long-term (2028-2033) |

| Fluctuations in End-User Demand | -0.4% | Global | Short to Medium-term (2025-2028) |

Mono Ethylene Glycol Market Opportunities Analysis

Significant opportunities are emerging within the Mono Ethylene Glycol market, primarily driven by the increasing global emphasis on sustainability and the ongoing development of innovative production technologies. The rising demand for bio-based MEG, produced from renewable feedstocks, presents a substantial growth avenue for companies looking to align with eco-friendly initiatives and meet consumer preferences for sustainable products. This shift not only addresses environmental concerns but also offers a pathway to reduce reliance on fossil fuels, creating a more resilient supply chain. Investments in research and development for advanced catalytic processes and alternative feedstock utilization are opening new doors for cost-effective and environmentally sound production methods, which could significantly differentiate market players.

Furthermore, the expanding application scope of MEG in sectors such as electric vehicle coolants, energy storage systems, and specialized industrial fluids offers diversified growth prospects beyond traditional polyester and PET markets. Strategic collaborations and partnerships between chemical manufacturers, technology providers, and end-use industries can accelerate the commercialization of these new applications and production techniques. The growing middle class in developing nations, coupled with rapid urbanization, continues to drive demand for consumer goods and infrastructure, indirectly boosting the need for MEG and its derivatives. These opportunities emphasize innovation, sustainable practices, and strategic market diversification as key elements for long-term success in the evolving MEG landscape.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bio-based MEG | +1.5% | Europe, North America, Asia Pacific | Long-term (2025-2033) |

| Expansion into New Applications (e.g., EVs) | +1.0% | Global | Medium to Long-term (2026-2033) |

| Technological Innovations in Production Efficiency | +0.8% | Global | Medium-term (2025-2030) |

| Recycling and Circular Economy Initiatives | +0.7% | Europe, North America | Long-term (2027-2033) |

| Growing Demand in Developing Economies | +0.6% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

Mono Ethylene Glycol Market Challenges Impact Analysis

The Mono Ethylene Glycol market encounters several significant challenges that demand strategic responses from industry participants. One prominent challenge is the increasing environmental and regulatory pressure to reduce the carbon footprint associated with petrochemical production. This necessitates substantial investment in sustainable manufacturing processes, carbon capture technologies, and the transition to cleaner energy sources, which can be capital-intensive and impact profitability. Companies must navigate a complex landscape of evolving environmental standards and consumer expectations for greener products, requiring continuous adaptation and innovation in their operations and product portfolios.

Moreover, the highly competitive nature of the market, particularly with the entry of new players and expansion of existing capacities in feedstock-advantaged regions, can lead to oversupply and pricing pressures. Managing supply-demand imbalances, especially during periods of economic downturns or global crises, poses a substantial challenge for maintaining stable pricing and market share. Additionally, the complexity of global supply chains for both raw materials and finished products makes the industry vulnerable to geopolitical disruptions, trade barriers, and logistical bottlenecks. Ensuring resilient and diversified supply chains while maintaining cost-effectiveness remains a critical challenge for MEG producers in a volatile global environment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intensifying Environmental Regulations & Sustainability Mandates | -1.0% | Europe, North America | Long-term (2025-2033) |

| Global Supply-Demand Imbalances | -0.8% | Asia Pacific, Middle East | Medium-term (2025-2030) |

| Geopolitical Instability and Trade Barriers | -0.7% | Global | Short to Medium-term (2025-2028) |

| High Capital Investment for New Capacity & Technology | -0.6% | Global | Long-term (2025-2033) |

| Disruption from Emerging Bio-based Alternatives | -0.5% | Global | Long-term (2028-2033) |

Mono Ethylene Glycol Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Mono Ethylene Glycol (MEG) market, encompassing historical data, current market conditions, and future growth projections from 2025 to 2033. The scope includes a detailed examination of market size, trends, drivers, restraints, opportunities, and challenges across various segments and key geographic regions. The report further incorporates an AI impact analysis to assess the influence of artificial intelligence on production, supply chain, and sustainability within the MEG industry. It offers strategic insights for stakeholders, enabling informed decision-making and competitive positioning within the dynamic chemical market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 45.8 Billion |

| Market Forecast in 2033 | USD 70.3 Billion |

| Growth Rate | 5.5% CAGR |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Saudi Basic Industries Corporation (SABIC), Dow Inc., LyondellBasell Industries N.V., ExxonMobil Chemical Company, Shell Plc, Sinopec Group, Reliance Industries Limited, Mitsubishi Chemical Corporation, Formosa Plastics Corporation, Indian Oil Corporation Ltd. (IOCL), Lotte Chemical Corporation, EQUATE Petrochemical Company, BASF SE, Oriental Union Chemical Corporation, Zhejiang Satellite Petrochemical Co. Ltd., CNPC (China National Petroleum Corporation), Qatar Chemical Company Ltd. (Q-Chem), PTT Global Chemical Public Company Limited, Indorama Ventures Public Company Limited, Fushun Petrochemical Company. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Mono Ethylene Glycol (MEG) market is meticulously segmented to provide a granular understanding of its diverse applications, end-use industries, product grades, and production methods. This segmentation allows for a detailed analysis of demand patterns, regional consumption trends, and technological shifts across various market verticals. By breaking down the market into these distinct categories, stakeholders can identify high-growth areas, assess competitive landscapes, and formulate targeted strategies for product development and market penetration. Each segment's performance is influenced by unique drivers and restraints, making a comprehensive segmentation analysis crucial for strategic planning.

For instance, the application segment highlights the dominance of polyester fibers and PET resins, which together account for the lion's share of MEG consumption, particularly in the thriving Asian markets. The end-use industry segmentation further clarifies where this demand originates, pointing to the textile, packaging, and automotive sectors as primary consumers. Analyzing these segments not only reveals current market dynamics but also projects future growth avenues, such as the increasing role of MEG in electric vehicle coolants or sustainable packaging solutions. Understanding these intricate layers of segmentation is essential for any comprehensive market assessment of Mono Ethylene Glycol.

- By Application:

- Polyester Fibers

- PET Resins

- Antifreeze & Coolants

- Films

- Other Applications (e.g., heat transfer fluids, chemical intermediates, solvents)

- By End-use Industry:

- Textiles

- Packaging

- Automotive

- Construction

- Consumer Goods

- Other Industries (e.g., pharmaceuticals, agriculture)

- By Grade:

- Fiber Grade

- Industrial Grade

- Antifreeze Grade

- By Production Process:

- Ethylene Oxide Process (Conventional)

- Bio-based Process (from bio-ethanol, syngas)

- Coal-to-MEG Process (CTMEG)

Regional Highlights

- Asia Pacific: Dominates the global Mono Ethylene Glycol market in terms of both production and consumption. Driven by rapid industrialization, increasing population, and robust growth in the textile, packaging, and automotive industries, particularly in countries like China, India, and Southeast Asian nations.

- North America: Characterized by stable demand and a focus on specialty applications, particularly in the automotive and construction sectors. The region benefits from abundant shale gas resources, providing cost-effective ethylene feedstock, leading to significant export capabilities.

- Europe: A mature market with stringent environmental regulations, driving a strong emphasis on sustainable production methods and the adoption of bio-based MEG. Demand is consistent from the packaging and automotive industries, with innovation focused on circular economy principles.

- Middle East & Africa (MEA): A major hub for MEG production due to its strategic location and extensive reserves of crude oil and natural gas, offering competitive feedstock advantages. The region is a significant exporter of MEG, supplying markets in Asia and Europe.

- Latin America: Experiencing growing demand for MEG, fueled by expanding industrial activities, particularly in the packaging and textile sectors. Countries like Brazil and Mexico are witnessing increased investments in chemical manufacturing capacities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Mono Ethylene Glycol Market.- Saudi Basic Industries Corporation (SABIC)

- Dow Inc.

- LyondellBasell Industries N.V.

- ExxonMobil Chemical Company

- Shell Plc

- Sinopec Group

- Reliance Industries Limited

- Mitsubishi Chemical Corporation

- Formosa Plastics Corporation

- Indian Oil Corporation Ltd. (IOCL)

- Lotte Chemical Corporation

- EQUATE Petrochemical Company

- BASF SE

- Oriental Union Chemical Corporation

- Zhejiang Satellite Petrochemical Co. Ltd.

- CNPC (China National Petroleum Corporation)

- Qatar Chemical Company Ltd. (Q-Chem)

- PTT Global Chemical Public Company Limited

- Indorama Ventures Public Company Limited

- Fushun Petrochemical Company

Frequently Asked Questions

Common user questions about the Mono Ethylene Glycol market reveal a desire for clear, concise answers on market dynamics, growth drivers, sustainability, and regional importance. These inquiries reflect the key areas of interest for investors, industry professionals, and researchers seeking to understand the current state and future trajectory of the MEG market.What is Mono Ethylene Glycol (MEG) and its primary uses?

Mono Ethylene Glycol (MEG) is a clear, odorless, and viscous liquid primarily used as a raw material in the production of polyester fibers and polyethylene terephthalate (PET) resins. It is also a key component in antifreeze and coolant formulations, de-icing fluids, and as a chemical intermediate in various industrial applications.

Which region dominates the global Mono Ethylene Glycol market?

The Asia Pacific region, particularly countries like China and India, currently dominates the global Mono Ethylene Glycol market. This dominance is driven by significant production capacities and robust demand from the rapidly expanding textile, packaging, and automotive industries in these nations.

What are the key drivers for the growth of the Mono Ethylene Glycol market?

The primary drivers for the MEG market's growth include the surging demand for polyester fibers in textiles and industrial applications, the expanding use of PET resins in packaging, increasing automotive production requiring antifreeze, and overall industrial growth and urbanization in emerging economies.

How is sustainability impacting the Mono Ethylene Glycol industry?

Sustainability is significantly impacting the MEG industry by driving demand for bio-based MEG (Bio-MEG) from renewable feedstocks and promoting recycling initiatives for PET. Regulatory pressures and consumer preferences are pushing manufacturers to adopt greener production processes and reduce their carbon footprint.

What are the main challenges faced by the Mono Ethylene Glycol market?

Key challenges for the MEG market include the volatility of raw material prices (ethylene), stringent environmental regulations, potential oversupply in certain regions, and geopolitical instabilities affecting global trade and supply chains. These factors can impact profitability and market stability.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted