Military Laser Target Designator Market

Military Laser Target Designator Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707410 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

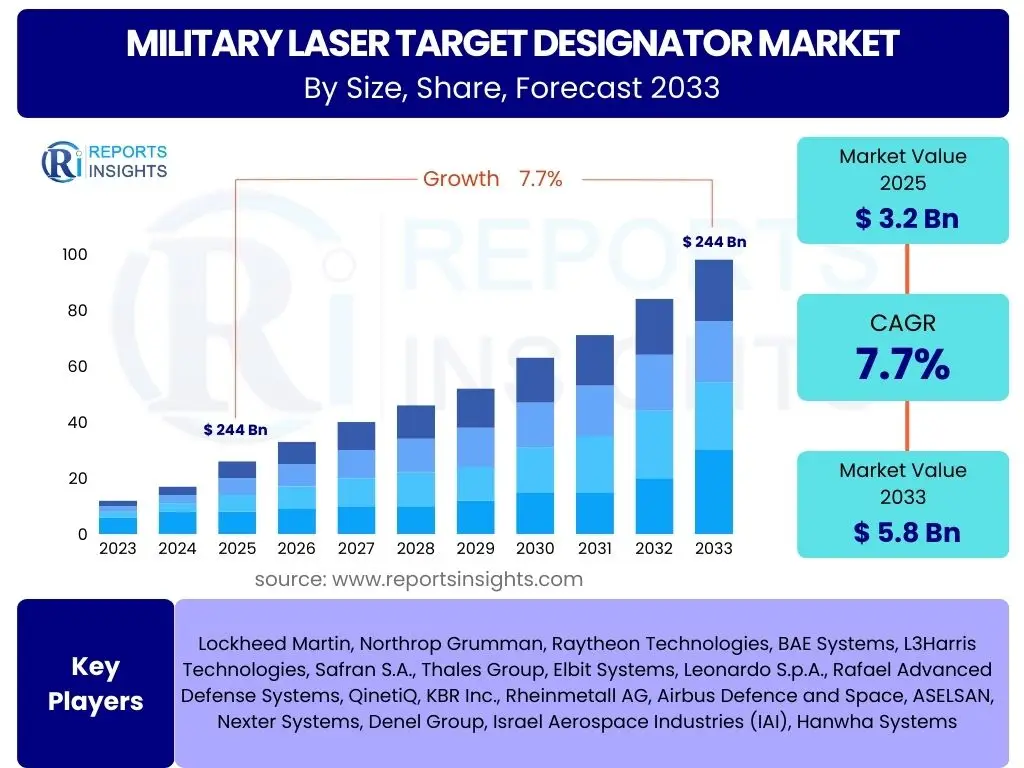

Military Laser Target Designator Market Size

According to Reports Insights Consulting Pvt Ltd, The Military Laser Target Designator Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.7% between 2025 and 2033. The market is estimated at USD 3.2 Billion in 2025 and is projected to reach USD 5.8 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by escalating global defense expenditures, a heightened focus on precision warfare capabilities, and ongoing military modernization programs across various nations. The increasing demand for advanced targeting solutions that enhance situational awareness and strike accuracy in complex operational environments is a significant contributor to this market expansion.

The consistent investment in next-generation military technologies, coupled with the strategic imperative to reduce collateral damage and optimize resource allocation during combat operations, underscores the market's upward trend. Furthermore, the proliferation of unmanned aerial vehicles (UAVs) and other unmanned systems, which often require integrated laser target designators for effective engagement, is opening new avenues for market growth. Geopolitical tensions and regional conflicts also fuel the procurement of sophisticated defense systems, positioning laser target designators as indispensable tools for modern armed forces.

Key Military Laser Target Designator Market Trends & Insights

The Military Laser Target Designator market is witnessing a transformative phase, driven by technological advancements and evolving strategic defense priorities. Users frequently inquire about the integration of multi-spectral capabilities, the miniaturization of systems for enhanced portability, and the seamless networking of designators with command, control, communications, computers, intelligence, surveillance, and reconnaissance (C4ISR) systems. There is also a pronounced interest in the development of longer-range and more precise designators, alongside concerns regarding their resilience against jamming and environmental factors. These inquiries highlight a collective focus on enhancing operational effectiveness, reducing system footprint, and improving data interoperability in real-time combat scenarios.

Another significant area of user interest revolves around the adoption of laser target designators in diverse operational contexts, including counter-terrorism, border security, and naval operations. The demand for systems that can operate effectively in adverse weather conditions, through obscurants, and across various terrains is frequently emphasized. Furthermore, the lifecycle costs, maintenance requirements, and upgrade pathways for these advanced targeting systems are critical considerations for military procurement agencies. These trends collectively point towards a market that prioritates versatility, robustness, and cost-efficiency alongside cutting-edge performance.

- Multi-spectral targeting capabilities enabling operation across various electromagnetic spectrums.

- Miniaturization and weight reduction of designator units for enhanced soldier portability and integration with smaller platforms.

- Seamless integration with advanced C4ISR networks for real-time data sharing and improved situational awareness.

- Development of longer-range and higher-accuracy designators for stand-off targeting capabilities.

- Increased demand for ruggedized systems capable of operating in extreme environmental conditions and contested electromagnetic environments.

- Integration with Unmanned Aerial Systems (UAS) and other robotic platforms for autonomous targeting.

- Focus on modular designs allowing for rapid upgrades and adaptability to new threats.

AI Impact Analysis on Military Laser Target Designator

The integration of Artificial Intelligence (AI) is poised to revolutionize the Military Laser Target Designator market, addressing common user questions related to automation, enhanced precision, and data processing. Users frequently inquire how AI can improve target recognition, optimize laser beam control, and provide predictive analytics for engagement scenarios. The core expectation is that AI will move these systems beyond manual operation, offering advanced capabilities such as autonomous target tracking, sophisticated data fusion from multiple sensors, and adaptive targeting algorithms that account for environmental variables and target movement in real-time. This integration promises to reduce operator workload, accelerate the decision-making cycle, and significantly increase strike accuracy.

Furthermore, AI's influence extends to enabling more resilient and adaptive designator systems. User concerns about counter-measures, jamming, and the need for robust performance in contested environments are directly addressed by AI's potential for self-correction and anomaly detection. AI-powered algorithms can analyze vast amounts of sensor data to differentiate between legitimate targets and decoys, predict optimal engagement parameters, and even recommend alternative targeting solutions if primary methods are compromised. This advanced analytical capability transforms laser target designators into highly intelligent and adaptive components of modern precision warfare, leading to more efficient and effective military operations.

- Enhanced target recognition and classification through AI-powered image processing and pattern recognition.

- Automated target tracking and locking, reducing operator fatigue and increasing reaction speed.

- Predictive targeting analytics for optimized engagement parameters, considering environmental factors and target dynamics.

- Sensor fusion capabilities, integrating data from multiple sources (EO/IR, radar) for a comprehensive target picture.

- Adaptive beam control and power management to counter atmospheric interference or jamming attempts.

- Autonomous mission planning and re-tasking for networked laser designator systems.

- Improved BDA (Battle Damage Assessment) through AI-assisted post-strike analysis.

Key Takeaways Military Laser Target Designator Market Size & Forecast

The Military Laser Target Designator market is on a solid growth trajectory, driven by a global emphasis on precision strike capabilities and military modernization. Common user questions about the market forecast often revolve around the most significant growth drivers, the impact of emerging technologies like AI, and the key regions poised for substantial investment. The primary takeaway is that increasing defense budgets globally, particularly in developing economies, are creating robust demand for advanced targeting systems. This is further bolstered by ongoing geopolitical instability and the imperative for armed forces to minimize collateral damage while maximizing operational effectiveness. The market's expansion is not merely incremental but reflective of a strategic shift towards smarter, more integrated warfare capabilities.

Technological advancements, including miniaturization, multi-spectral design, and enhanced networking capabilities, are pivotal in shaping the market's future. The integration of artificial intelligence is expected to be a game-changer, improving accuracy, automation, and decision support. Another key takeaway is the sustained demand for portable and vehicle-mounted systems, highlighting the need for versatile solutions adaptable to various operational platforms. As nations prioritize the upgrade of their defense arsenals, the market for military laser target designators will continue to be a high-growth segment, presenting lucrative opportunities for innovation and strategic partnerships.

- Significant market expansion projected, driven by rising global defense expenditures.

- Technological advancements in precision, miniaturization, and multi-spectral capabilities are key enablers.

- AI integration is a critical accelerator, enhancing automation, accuracy, and decision support.

- Strong demand across all military branches for improved targeting and intelligence gathering.

- Asia Pacific and North America are expected to remain dominant regions in terms of investment and adoption.

- Focus on reducing collateral damage and improving operational efficiency drives system procurement.

Military Laser Target Designator Market Drivers Analysis

The Military Laser Target Designator market is significantly influenced by several key drivers that collectively propel its growth and technological evolution. A primary driver is the increasing global defense spending, particularly in response to geopolitical tensions and regional conflicts, which necessitates the acquisition of advanced precision weaponry. Nations are continuously investing in modernizing their armed forces to achieve superior tactical advantages, and laser target designators are integral to these modernization efforts. Furthermore, the growing emphasis on precision warfare and the imperative to minimize collateral damage in urban and complex environments amplify the demand for highly accurate targeting solutions. This strategic shift necessitates systems that can precisely designate targets for guided munitions, ensuring effective engagement while adhering to stricter rules of engagement.

Another crucial driver is the rapid advancement in military optics and sensor technologies. Innovations such as enhanced range capabilities, improved beam stability, and the development of multi-spectral designators are making these systems more versatile and effective in diverse operational scenarios. The proliferation of unmanned aerial vehicles (UAVs) and other unmanned systems in military applications also significantly drives the market. Laser target designators are essential components for arming and guiding munitions from these unmanned platforms, expanding their operational utility and tactical reach. This trend toward integrated, networked combat systems highlights the indispensable role of advanced targeting solutions in contemporary warfare.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Defense Spending and Military Modernization Programs | +2.5% | North America, Asia Pacific, Europe, Middle East | Short to Mid-Term (2025-2030) |

| Growing Emphasis on Precision Warfare and Reduction of Collateral Damage | +1.8% | Global | Mid to Long-Term (2027-2033) |

| Technological Advancements in Optics, Sensors, and System Integration | +1.5% | Global | Short to Mid-Term (2025-2030) |

| Rising Adoption of Unmanned Aerial Vehicles (UAVs) in Military Operations | +1.2% | North America, Asia Pacific, Europe | Mid to Long-Term (2027-2033) |

Military Laser Target Designator Market Restraints Analysis

Despite the robust growth prospects, the Military Laser Target Designator market faces several significant restraints that could impede its full potential. One major challenge is the high cost associated with the research, development, and production of advanced laser target designator systems. These systems incorporate highly sophisticated components, including specialized optics, high-power lasers, and complex electronics, driving up their acquisition and maintenance expenses. Budgetary constraints in certain national defense sectors, particularly in smaller economies or those facing economic downturns, can limit procurement volumes and delay modernization efforts. The substantial investment required can be a barrier for many potential buyers, leading to slower adoption rates or the prioritization of alternative, less costly solutions.

Another critical restraint is the stringent regulatory environment and export control policies governing military-grade technologies. Laser target designators are considered dual-use technologies and are subject to strict international agreements and national regulations such as the Wassenaar Arrangement and ITAR (International Traffic in Arms Regulations). These controls often restrict the transfer of sensitive technologies to certain countries, limiting market reach and complicating international collaborations. Furthermore, the long procurement cycles inherent in defense contracting, coupled with complex bureaucratic processes, can significantly delay product deployment. This protracted timeline from development to operational use can hinder market responsiveness to emerging threats and technological advancements, affecting overall market dynamism.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Research & Development and Procurement Costs | -1.5% | Global, particularly smaller economies | Short to Mid-Term (2025-2030) |

| Stringent Export Control Regulations and International Policies | -1.0% | Global, especially developing nations | Short to Long-Term (2025-2033) |

| Complex and Lengthy Defense Procurement Cycles | -0.8% | Global | Short to Mid-Term (2025-2030) |

| Risk of Technological Obsolescence due to Rapid Innovation | -0.5% | Global | Mid to Long-Term (2027-2033) |

Military Laser Target Designator Market Opportunities Analysis

Significant opportunities exist within the Military Laser Target Designator market, primarily driven by the continuous demand for enhanced precision and integration across diverse platforms. One key opportunity lies in the development of multi-functional laser systems that combine targeting, rangefinding, and communication capabilities into a single, compact unit. This integration reduces the logistical footprint and enhances operational efficiency for military personnel. Furthermore, the increasing focus on networked warfare and the interoperability of systems creates substantial avenues for growth. Designators that can seamlessly integrate with various C4ISR networks, allowing for real-time information sharing and coordinated strikes, will be highly sought after by modern armed forces seeking to optimize their operational capabilities.

Another promising opportunity involves the expansion of applications beyond traditional ground and air forces to naval and special operations domains. The demand for ruggedized, marine-grade laser target designators for naval vessels and special forces operating in maritime environments is growing, presenting a niche but high-value market. Moreover, the global push for counter-drone capabilities offers a new application for these systems, where laser designators can be adapted for precise tracking and engagement of small, fast-moving unmanned aerial threats. Finally, strategic partnerships and collaborations between defense contractors, technology providers, and academic institutions can accelerate innovation, reduce development costs, and facilitate the transfer of cutting-edge technologies, thus unlocking new market segments and enhancing competitive advantage.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Next-Generation Unmanned Systems and Robotic Platforms | +1.5% | North America, Europe, Asia Pacific | Mid to Long-Term (2027-2033) |

| Development of Multi-functional Systems (Targeting, Rangefinding, Communications) | +1.2% | Global | Short to Mid-Term (2025-2030) |

| Expansion into New Applications (e.g., Counter-UAS, Naval Operations) | +0.9% | Global | Mid to Long-Term (2027-2033) |

| Strategic Partnerships and Technology Transfer Initiatives | +0.7% | Global | Short to Long-Term (2025-2033) |

Military Laser Target Designator Market Challenges Impact Analysis

The Military Laser Target Designator market faces several critical challenges that demand strategic responses from manufacturers and defense agencies. One significant challenge is the increasing sophistication of countermeasures and electronic warfare (EW) techniques designed to disrupt or neutralize laser systems. Adversaries are continuously developing methods to jam, spoof, or blind laser designators, posing a direct threat to their effectiveness and reliability in contested environments. This necessitates continuous investment in anti-jamming technologies, improved beam resilience, and advanced filtering mechanisms to maintain operational superiority, adding to the complexity and cost of system development.

Another pervasive challenge is ensuring supply chain stability and security, particularly for high-precision optical components and rare-earth materials essential for laser manufacturing. Geopolitical tensions, trade disputes, and global events can disrupt the supply of critical components, leading to production delays, increased costs, and potential vulnerabilities. Furthermore, the integration of these advanced systems into existing military infrastructures presents significant technical and logistical hurdles. Interoperability issues with legacy systems, the need for extensive training for military personnel, and the complexity of secure data transfer across diverse platforms can hinder seamless adoption and maximize operational efficiency. Overcoming these integration complexities requires substantial investment in research, development, and robust testing protocols, adding another layer of challenge to market growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Countermeasures and Electronic Warfare Threats | -1.2% | Global | Short to Mid-Term (2025-2030) |

| Supply Chain Disruptions and Reliance on Critical Components | -0.9% | Global | Short-Term (2025-2027) |

| Integration Complexities with Existing Military Infrastructure | -0.7% | Global | Mid to Long-Term (2027-2033) |

| Ethical and Legal Concerns Regarding Autonomous Targeting Systems | -0.4% | Global | Long-Term (2030-2033) |

Military Laser Target Designator Market - Updated Report Scope

This report provides a comprehensive analysis of the Military Laser Target Designator market, offering in-depth insights into its size, growth trajectory, key trends, and influencing factors. It covers market segmentation by type, application, technology, and wavelength, providing a detailed breakdown of each segment's performance and future outlook. The scope extends to a thorough regional analysis, identifying prominent markets and their specific growth drivers and challenges. The report also includes an exhaustive profiling of leading market players, evaluating their strategies, product portfolios, and market positions to offer a holistic view of the competitive landscape. Through this detailed examination, the report aims to equip stakeholders with actionable intelligence for strategic decision-making and investment planning in this dynamic defense sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.2 Billion |

| Market Forecast in 2033 | USD 5.8 Billion |

| Growth Rate | 7.7% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Lockheed Martin, Northrop Grumman, Raytheon Technologies, BAE Systems, L3Harris Technologies, Safran S.A., Thales Group, Elbit Systems, Leonardo S.p.A., Rafael Advanced Defense Systems, QinetiQ, KBR Inc., Rheinmetall AG, Airbus Defence and Space, ASELSAN, Nexter Systems, Denel Group, Israel Aerospace Industries (IAI), Hanwha Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Military Laser Target Designator market is comprehensively segmented to provide a granular understanding of its diverse components and their respective growth trajectories. These segmentations allow for a detailed analysis of market dynamics, identifying specific areas of high demand, technological preference, and operational application. By categorizing the market based on various technical and functional attributes, stakeholders can better understand niche markets, emerging requirements, and opportunities for specialized product development. This detailed breakdown facilitates targeted strategic planning and resource allocation for market participants.

The market is primarily segmented by Type, encompassing handheld, vehicle-mounted, airborne, and naval designators, reflecting their deployment platforms and operational requirements. Wavelength segmentation differentiates systems based on their laser emission characteristics, crucial for performance in varying atmospheric conditions and target types. Technology-based segmentation highlights the underlying laser generation methods, impacting efficiency, size, and power. Finally, segmentation by Application illustrates the primary military branches utilizing these systems, showcasing their strategic importance across ground, air, naval, and special operations forces. Each segment presents unique market drivers, challenges, and opportunities, contributing to the overall market complexity and growth.

- By Type:

- Handheld Laser Target Designators

- Vehicle-Mounted Laser Target Designators

- Airborne Laser Target Designators

- Naval Laser Target Designators

- By Wavelength:

- 1064 nm

- 1570 nm

- Other Wavelengths

- By Technology:

- Diode-Pumped Laser Designators

- Flashlamp-Pumped Laser Designators

- Fiber Laser Designators

- By Application:

- Ground Forces

- Naval Forces

- Air Force

- Special Operations Forces

Regional Highlights

The global Military Laser Target Designator market exhibits distinct regional dynamics driven by varying defense budgets, geopolitical landscapes, and technological adoption rates. North America, particularly the United States, represents a dominant market share due to its significant defense spending, continuous investment in advanced military technologies, and robust research and development infrastructure. The region is a hub for innovation in precision warfare, with a strong focus on integrating laser target designators into next-generation combat systems and unmanned platforms.

Europe also holds a substantial market share, driven by ongoing military modernization efforts, the imperative to enhance collective security within NATO, and responses to regional security threats. Countries like the United Kingdom, France, and Germany are key contributors, investing in highly sophisticated targeting solutions for their armed forces. The Asia Pacific region is anticipated to demonstrate the highest growth rate during the forecast period. This surge is fueled by escalating defense expenditures from countries like China, India, and South Korea, driven by territorial disputes, regional power dynamics, and the urgent need to upgrade military capabilities with advanced precision strike systems. Latin America, the Middle East, and Africa (MEA) are also experiencing growth, albeit at a slower pace, primarily due to increasing internal security challenges, counter-terrorism operations, and a gradual shift towards modernizing their defense arsenals, often through imports and technology transfers from more established defense markets.

- North America: Dominant market due to extensive defense budgets, advanced technological capabilities, and focus on precision-guided munitions. The United States is a primary driver with continuous R&D investment and procurement of state-of-the-art targeting systems.

- Europe: Significant market share, propelled by military modernization programs, NATO defense spending commitments, and ongoing security concerns. Key players include the United Kingdom, France, and Germany, emphasizing interoperability and advanced ground and air targeting.

- Asia Pacific (APAC): Expected to exhibit the highest CAGR, driven by rising defense expenditures in countries like China, India, and South Korea, coupled with regional geopolitical tensions and ambitious military expansion plans. Demand for advanced long-range targeting is particularly strong.

- Latin America: Gradual growth attributed to efforts in combating internal security threats, drug trafficking, and limited military modernization. Procurement often involves less technologically advanced but robust systems.

- Middle East and Africa (MEA): Growing market, primarily influenced by persistent regional conflicts, counter-terrorism operations, and substantial defense imports. Investments focus on enhancing precision strike capabilities for air and ground forces to address complex security challenges.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Military Laser Target Designator Market.- Lockheed Martin

- Northrop Grumman

- Raytheon Technologies

- BAE Systems

- L3Harris Technologies

- Safran S.A.

- Thales Group

- Elbit Systems

- Leonardo S.p.A.

- Rafael Advanced Defense Systems

- QinetiQ

- KBR Inc.

- Rheinmetall AG

- Airbus Defence and Space

- ASELSAN

- Nexter Systems

- Denel Group

- Israel Aerospace Industries (IAI)

- Hanwha Systems

Frequently Asked Questions

What is the projected growth rate for the Military Laser Target Designator Market?

The Military Laser Target Designator Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.7% between 2025 and 2033, driven by increasing global defense expenditures and the demand for precision warfare capabilities.

How will AI impact the future of Military Laser Target Designators?

AI is expected to significantly enhance military laser target designators by enabling autonomous target tracking, improved target recognition through advanced algorithms, sensor fusion for comprehensive data, and predictive analytics for optimal engagement, reducing operator workload and increasing accuracy.

What are the primary applications of Military Laser Target Designators?

Military Laser Target Designators are primarily used by ground forces for infantry and artillery support, air forces for guiding bombs and missiles, naval forces for maritime target engagement, and special operations forces for precise tactical operations across various platforms.

Which regions are leading the market for Military Laser Target Designators?

North America currently leads the market due to high defense spending and technological advancements, while the Asia Pacific region is projected to exhibit the fastest growth due to increasing military modernization efforts and geopolitical tensions.

What are the main drivers of growth in this market?

Key drivers include rising global defense budgets, the increasing focus on precision warfare to minimize collateral damage, continuous technological advancements in optics and sensors, and the growing integration of designators with unmanned aerial vehicles (UAVs) and other advanced military platforms.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted