Microprocessor Market

Microprocessor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704028 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Microprocessor Market Size

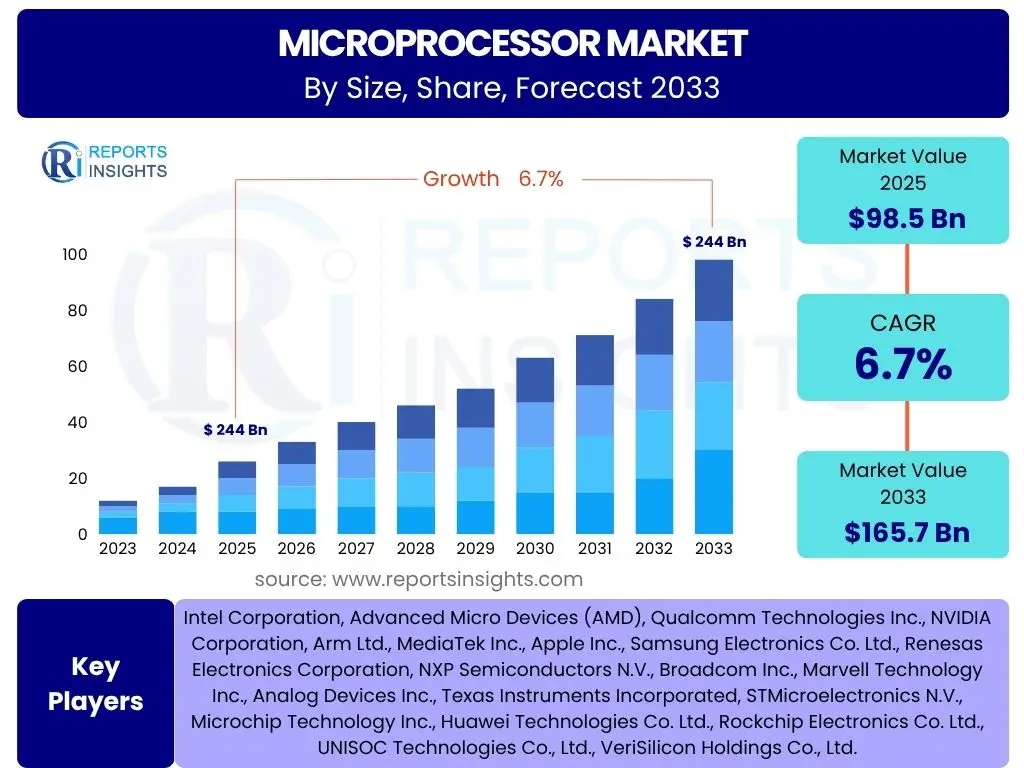

According to Reports Insights Consulting Pvt Ltd, The Microprocessor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 98.5 billion in 2025 and is projected to reach USD 165.7 billion by the end of the forecast period in 2033. This substantial growth is primarily driven by the escalating demand for advanced computing capabilities across diverse industries, fueled by the proliferation of artificial intelligence, IoT devices, and high-performance computing applications.

The increasing integration of microprocessors into embedded systems, automotive electronics, and consumer devices further contributes to this expansive market trajectory. Miniaturization, enhanced power efficiency, and the development of specialized processing units are key factors enabling this consistent expansion. The market's resilience is also attributed to continuous innovation in semiconductor manufacturing processes and architectural designs, addressing evolving performance requirements.

Key Microprocessor Market Trends & Insights

The Microprocessor market is currently shaped by several transformative trends, reflecting the evolving landscape of digital technology and computational demands. Common user inquiries often revolve around the dominant technological shifts, the push towards specialized hardware, and the implications of geopolitical factors on supply chains. The market is witnessing a profound shift from general-purpose CPUs to highly specialized processors, alongside a growing emphasis on energy efficiency and the integration of AI capabilities directly into chip architectures. Furthermore, supply chain resilience and regional manufacturing diversification are emerging as critical strategic considerations for market players.

- Shift towards specialized processing units (GPUs, NPUs, ASICs) for AI and machine learning workloads.

- Increasing demand for edge computing microprocessors, enabling real-time data processing closer to the source.

- Growing adoption of RISC-V architecture for custom silicon and open-source hardware development.

- Advancements in packaging technologies (e.g., 3D stacking, chiplets) to enhance performance and reduce power consumption.

- Focus on energy-efficient designs to address power consumption challenges in data centers and portable devices.

- Integration of advanced security features at the hardware level to protect against cyber threats.

- Expansion of automotive microprocessors driven by autonomous driving and advanced driver-assistance systems (ADAS).

- Persistent challenges and strategic efforts to diversify global semiconductor supply chains.

AI Impact Analysis on Microprocessor

Artificial intelligence is profoundly reshaping the microprocessor landscape, driving a paradigm shift in architectural design and performance requirements. User inquiries frequently highlight the need for processors capable of handling immense datasets and complex algorithms efficiently, alongside concerns about power consumption and latency. AI's pervasive influence has led to an explosion in demand for specialized hardware accelerators, moving beyond traditional CPUs to embrace GPUs, ASICs, and dedicated Neural Processing Units (NPUs) engineered for parallel processing and AI inference at both the cloud and edge. This demand is pushing innovation in chip design, necessitating architectures that prioritize throughput, memory bandwidth, and energy efficiency specifically for AI workloads.

The integration of AI capabilities is not limited to high-performance computing; it extends to embedded systems, IoT devices, and consumer electronics, fostering the development of "AI-ready" microprocessors. This trend means that future microprocessors will inherently incorporate AI co-processors or highly optimized instruction sets to enable on-device AI functions, reducing reliance on cloud infrastructure for certain tasks. The push for real-time AI processing at the edge is particularly impactful, driving the need for compact, low-power, yet powerful AI-capable microprocessors, fundamentally altering development roadmaps and market strategies for semiconductor manufacturers.

- Spurred demand for specialized AI accelerators (NPUs, GPUs, ASICs).

- Driven architectural innovation towards parallel processing and dataflow computing.

- Increased emphasis on power efficiency for AI workloads at the edge.

- Facilitated the integration of AI capabilities directly into mainstream CPUs and SoCs.

- Accelerated research into in-memory computing and neuromorphic architectures.

Key Takeaways Microprocessor Market Size & Forecast

The Microprocessor market is poised for significant expansion, reflecting its indispensable role across an ever-widening array of technological applications. Common user questions often seek to understand the underlying drivers of this growth and where the most impactful opportunities lie. The forecast indicates robust growth primarily propelled by the exponential rise of AI and machine learning, alongside the pervasive proliferation of IoT devices and the ongoing expansion of cloud computing infrastructure. This dynamic environment necessitates continuous innovation in chip design, manufacturing processes, and specialized architectures, pushing market players to adapt to evolving performance and efficiency demands.

A critical insight is the shift from a singular focus on general-purpose processing to a more diversified landscape where specialized processors (e.g., for AI, graphics, or specific industrial applications) are gaining prominence. This specialization, combined with advancements in packaging technologies and manufacturing techniques, will be crucial for meeting the performance and power requirements of next-generation technologies. The market's growth also underscores the increasing strategic importance of semiconductor technology at a national and geopolitical level, influencing investment in domestic manufacturing and supply chain resilience.

- Robust market growth driven by AI, IoT, and cloud computing adoption.

- Increasing specialization of microprocessors for specific workloads (e.g., AI accelerators).

- Significant investment in advanced manufacturing processes and chiplet architectures.

- Rising importance of power efficiency and thermal management in chip design.

- Emergence of diverse regional ecosystems for semiconductor manufacturing and R&D.

Microprocessor Market Drivers Analysis

The Microprocessor market is driven by a confluence of technological advancements and expanding application areas. The global digital transformation initiative, encompassing everything from smart cities to industrial automation, hinges on increasingly powerful and efficient processing capabilities. The continuous evolution of semiconductor manufacturing processes, such as moving to smaller nodes (e.g., 5nm, 3nm), enables higher transistor density, improved performance, and reduced power consumption, directly fueling demand. Furthermore, the relentless pace of innovation in software and data-intensive applications necessitates corresponding advancements in hardware, creating a self-sustaining cycle of demand and supply.

The proliferation of interconnected devices within the Internet of Things (IoT) ecosystem significantly contributes to market expansion, as each device, from simple sensors to complex embedded systems, requires some form of processing unit. Similarly, the automotive sector's shift towards electric and autonomous vehicles is a major driver, demanding high-performance microprocessors for ADAS, infotainment, and powertrain management. The expansion of 5G networks and the underlying data center infrastructure further accelerate demand for advanced microprocessors capable of handling massive data throughput and complex computations, emphasizing low latency and high reliability.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Adoption of Artificial Intelligence and Machine Learning | +1.5% | Global (North America, APAC, Europe) | Long-term (2025-2033) |

| Proliferation of IoT Devices and Edge Computing | +1.2% | Global (APAC, North America) | Medium-term (2025-2030) |

| Expansion of Data Centers and Cloud Computing | +1.0% | North America, Europe, APAC | Long-term (2025-2033) |

| Advancements in Automotive Electronics and Autonomous Vehicles | +0.8% | Europe, North America, APAC (China, Japan) | Medium to Long-term (2025-2033) |

| Rise of 5G Technology and Next-Gen Communication Infrastructure | +0.7% | APAC, North America, Europe | Medium-term (2025-2030) |

Microprocessor Market Restraints Analysis

Despite the robust growth, the Microprocessor market faces several notable restraints that could impact its expansion trajectory. The most prominent challenge involves the escalating costs associated with research and development, particularly for designing and fabricating chips at advanced process nodes (e.g., sub-7nm). These costs, driven by the complexity of design tools, lithography equipment, and materials, necessitate massive capital expenditure, limiting the number of players capable of competing at the bleeding edge. Furthermore, the inherent complexity of modern processor architectures makes design and verification increasingly challenging, extending development cycles and increasing the risk of design flaws.

Another significant restraint is the volatility and vulnerability of the global semiconductor supply chain. Geopolitical tensions, natural disasters, and unexpected demand surges can lead to severe chip shortages, impacting production across various industries reliant on microprocessors. Power consumption and thermal management also remain persistent hurdles, particularly as processors become more powerful and densely packed. Ensuring efficient heat dissipation while maintaining performance is a continuous engineering challenge, especially for high-performance computing and compact embedded systems. Lastly, intellectual property (IP) infringement and the increasing prevalence of patent disputes pose legal and financial risks, potentially stifling innovation and market entry for smaller players.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Research and Development (R&D) Costs | -0.9% | Global | Long-term (2025-2033) |

| Supply Chain Disruptions and Geopolitical Tensions | -0.7% | Global (Specific Impact on APAC, North America) | Medium-term (2025-2030) |

| Increasing Power Consumption and Thermal Management Issues | -0.5% | Global | Long-term (2025-2033) |

| Complexity in Chip Design and Manufacturing | -0.4% | Global | Long-term (2025-2033) |

Microprocessor Market Opportunities Analysis

The Microprocessor market is rich with opportunities driven by emerging technologies and expanding application frontiers. A significant area of growth lies in the burgeoning field of Edge AI, where the demand for specialized, low-power microprocessors capable of performing AI inference directly on devices is escalating. This eliminates the need to send all data to the cloud, improving latency, privacy, and power efficiency for applications ranging from smart cameras to industrial automation and autonomous drones. The growing ecosystem around custom silicon and application-specific integrated circuits (ASICs) also presents substantial opportunities, as companies seek to differentiate their products with highly optimized, proprietary processing solutions tailored for unique workloads, often leveraging open-source architectures like RISC-V.

The ongoing digital transformation across industries, including healthcare, manufacturing (Industry 4.0), and retail, continues to open new avenues for microprocessor integration, from advanced medical devices to predictive maintenance systems. Furthermore, the long-term potential of quantum computing and neuromorphic computing, while nascent, represents significant future opportunities for specialized processor development. As these technologies mature, they will require entirely new classes of microprocessors to manage their complex operations. The increasing focus on sustainability and energy efficiency also creates opportunities for companies to innovate in ultra-low-power processor designs, catering to battery-powered devices and reducing the carbon footprint of data centers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Edge AI and On-Device Processing | +1.3% | Global (APAC, North America, Europe) | Medium to Long-term (2025-2033) |

| Increasing Adoption of Custom Silicon and RISC-V Architecture | +1.0% | Global (North America, APAC) | Medium-term (2025-2030) |

| Expansion into New Verticals (e.g., Advanced Robotics, Digital Health) | +0.8% | Global | Long-term (2025-2033) |

| Development of Neuromorphic and Quantum Computing Processors | +0.6% | North America, Europe | Long-term (2030-2033) |

Microprocessor Market Challenges Impact Analysis

The Microprocessor market is confronted by several significant challenges that necessitate strategic responses from industry players. One major hurdle is the escalating manufacturing complexity and cost, particularly as semiconductor fabrication moves to increasingly smaller nodes. Achieving high yields and maintaining precision at the atomic scale requires enormous investment in advanced lithography tools, materials, and cleanroom facilities, making it challenging for all but the largest companies to compete at the forefront. This contributes to a concentrated supply chain, increasing the risk of disruption.

Another critical challenge is managing the heat generated by increasingly powerful and compact microprocessors. Thermal management solutions are becoming more complex and costly, impacting overall system design and often limiting the performance potential of chips. Furthermore, the global shortage of skilled labor, particularly in advanced semiconductor design, verification, and manufacturing, poses a significant constraint on innovation and production capacity. Maintaining intellectual property (IP) security and preventing counterfeiting also present ongoing challenges, particularly in a globally interconnected supply chain, impacting revenue and brand reputation for legitimate manufacturers. Navigating complex geopolitical landscapes and evolving trade policies, especially concerning critical technology exports and imports, adds another layer of complexity and uncertainty to market operations.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Escalating Manufacturing Complexity and Capital Expenditure | -0.8% | Global (APAC, North America) | Long-term (2025-2033) |

| Thermal Management and Power Density Issues | -0.6% | Global | Long-term (2025-2033) |

| Shortage of Skilled Workforce in Semiconductor Industry | -0.5% | Global (North America, Europe, APAC) | Long-term (2025-2033) |

| Intellectual Property (IP) Security and Counterfeiting Concerns | -0.3% | Global | Medium to Long-term (2025-2033) |

Microprocessor Market - Updated Report Scope

This report provides a comprehensive analysis of the global Microprocessor market, offering a detailed overview of its size, segmentation, trends, drivers, restraints, and opportunities. The scope encompasses an in-depth assessment of market dynamics, competitive landscape, and regional insights, designed to equip stakeholders with actionable intelligence for strategic decision-making. It covers historical data from 2019 to 2023, providing a robust baseline for the forecast period spanning 2025 to 2033, and incorporates insights on the transformative impact of emerging technologies like AI.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 98.5 Billion |

| Market Forecast in 2033 | USD 165.7 Billion |

| Growth Rate | 6.7% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Intel Corporation, Advanced Micro Devices (AMD), Qualcomm Technologies Inc., NVIDIA Corporation, Arm Ltd., MediaTek Inc., Apple Inc., Samsung Electronics Co. Ltd., Renesas Electronics Corporation, NXP Semiconductors N.V., Broadcom Inc., Marvell Technology Inc., Analog Devices Inc., Texas Instruments Incorporated, STMicroelectronics N.V., Microchip Technology Inc., Huawei Technologies Co. Ltd., Rockchip Electronics Co. Ltd., UNISOC Technologies Co., Ltd., VeriSilicon Holdings Co., Ltd. |

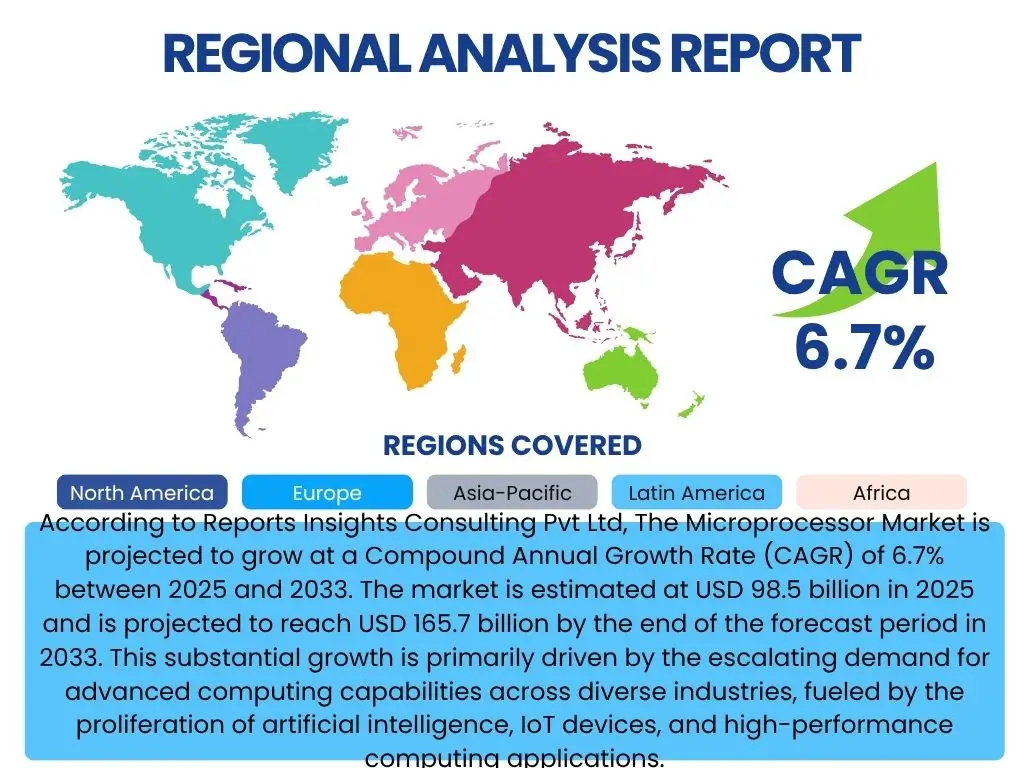

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Microprocessor market is extensively segmented to provide a granular understanding of its diverse components and evolving demand patterns. This segmentation allows for precise analysis of market performance across different product types, core architectures, technological nodes, and end-use applications, reflecting the specialized requirements of various industries. The market's complexity necessitates such detailed breakdown to identify specific growth engines and areas requiring strategic focus, from high-performance computing to embedded systems.

The segmentation highlights the market's transition towards specialized processing units, driven by demand for AI and specific applications, as well as the continuous push towards smaller manufacturing nodes for enhanced performance and efficiency. Understanding these segments is crucial for market players to tailor their product offerings and strategic investments, ensuring alignment with the distinct needs of each application and end-use industry. This comprehensive segmentation framework underscores the dynamic and multifaceted nature of the global microprocessor landscape.

- By Type: CISC Microprocessors, RISC Microprocessors, ASIC Microprocessors, GPU Microprocessors, NPU Microprocessors, Others

- By Core Type: Single-Core, Multi-Core (Dual-Core, Quad-Core, Octa-Core, Other Multi-Core)

- By Technology: 3nm, 5nm, 7nm, 10nm, 14nm, 28nm and above

- By Application: Consumer Electronics (Smartphones, Laptops, Wearables, Gaming Consoles, Smart Home Devices), Automotive (ADAS, Infotainment, Engine Control Units), Industrial Automation, Data Centers & Cloud Computing, Telecommunications (5G Infrastructure), Medical Devices, Aerospace & Defense, Others

- By End-Use Industry: IT & Telecommunications, Automotive, Healthcare, Manufacturing, Government & Defense, Consumer Goods, Energy & Utilities, Education, Research & Development

Regional Highlights

- North America: This region holds a significant market share, driven by robust R&D activities, early adoption of advanced technologies like AI and cloud computing, and the presence of leading semiconductor design companies. The demand from data centers, automotive, and defense sectors is particularly strong.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, primarily due to its dominant position in semiconductor manufacturing, a large consumer electronics market, and rapid industrialization. Countries like China, Taiwan, South Korea, and Japan are at the forefront of both production and consumption. The expansion of 5G infrastructure and IoT adoption further fuels growth.

- Europe: Europe exhibits substantial growth driven by its strong automotive industry, increasing investment in industrial automation (Industry 4.0), and a growing focus on edge computing and specialized AI applications. Government initiatives to boost domestic semiconductor production also contribute to market expansion.

- Latin America: This region shows steady growth, primarily influenced by increasing internet penetration, rising adoption of smartphones and consumer electronics, and developing IT infrastructure. Investment in digital transformation across various sectors also drives demand.

- Middle East and Africa (MEA): The MEA market is expanding, spurred by digital transformation initiatives, smart city projects, and diversification efforts away from oil economies. Investments in data centers and telecommunications infrastructure are key growth drivers, alongside a burgeoning consumer electronics market.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Microprocessor Market.- Intel Corporation

- Advanced Micro Devices (AMD)

- Qualcomm Technologies Inc.

- NVIDIA Corporation

- Arm Ltd.

- MediaTek Inc.

- Apple Inc.

- Samsung Electronics Co. Ltd.

- Renesas Electronics Corporation

- NXP Semiconductors N.V.

- Broadcom Inc.

- Marvell Technology Inc.

- Analog Devices Inc.

- Texas Instruments Incorporated

- STMicroelectronics N.V.

- Microchip Technology Inc.

- Huawei Technologies Co. Ltd.

- Rockchip Electronics Co. Ltd.

- UNISOC Technologies Co., Ltd.

- VeriSilicon Holdings Co., Ltd.

Frequently Asked Questions

What is the projected growth rate of the Microprocessor market?

The Microprocessor market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033, reaching an estimated value of USD 165.7 billion by 2033.

Which factors are primarily driving the Microprocessor market growth?

Key drivers include the escalating adoption of Artificial Intelligence (AI) and Machine Learning (ML), the widespread proliferation of IoT devices and edge computing, the expansion of data centers and cloud computing, and advancements in automotive electronics.

How is AI impacting microprocessor design and demand?

AI is significantly impacting the market by driving demand for specialized processors like NPUs and GPUs, fostering architectural innovations for parallel processing, and increasing the need for energy-efficient chips capable of on-device AI inference.

What are the main challenges faced by the Microprocessor market?

Major challenges include high research and development costs, complexities in chip design and manufacturing, supply chain disruptions, escalating power consumption, and the global shortage of skilled semiconductor professionals.

Which regions are leading in the Microprocessor market?

Asia Pacific (APAC) is anticipated to be the fastest-growing region due to its manufacturing dominance and large consumer base, while North America holds a significant market share driven by strong R&D and early technology adoption.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted